|

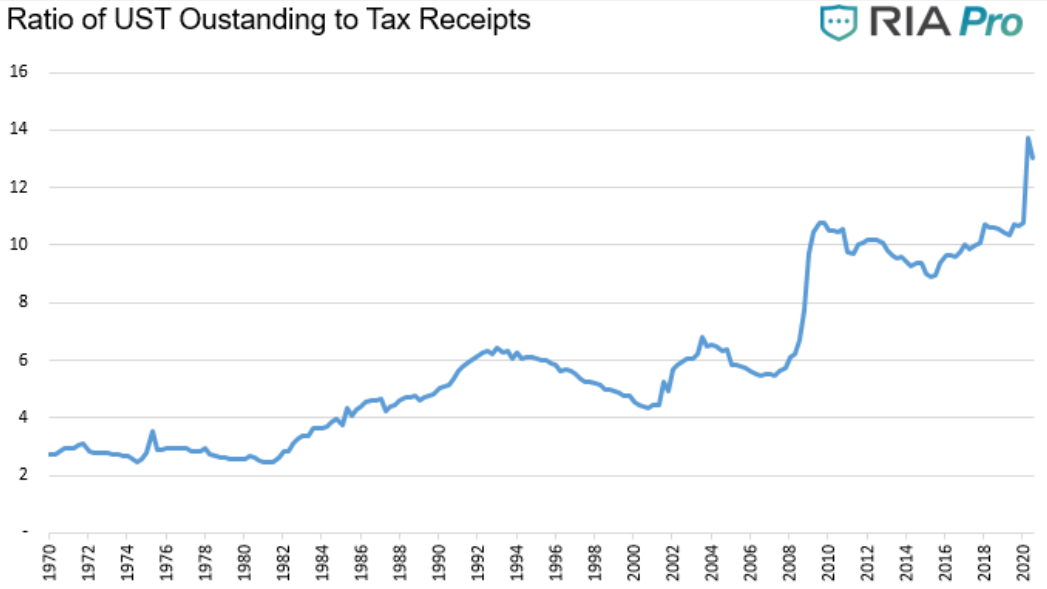

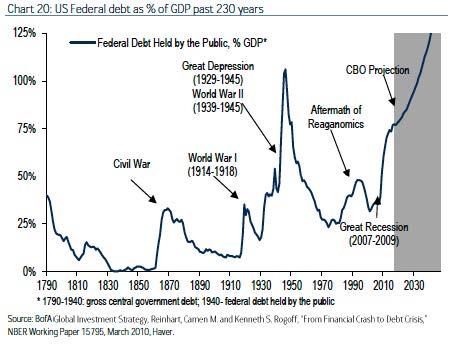

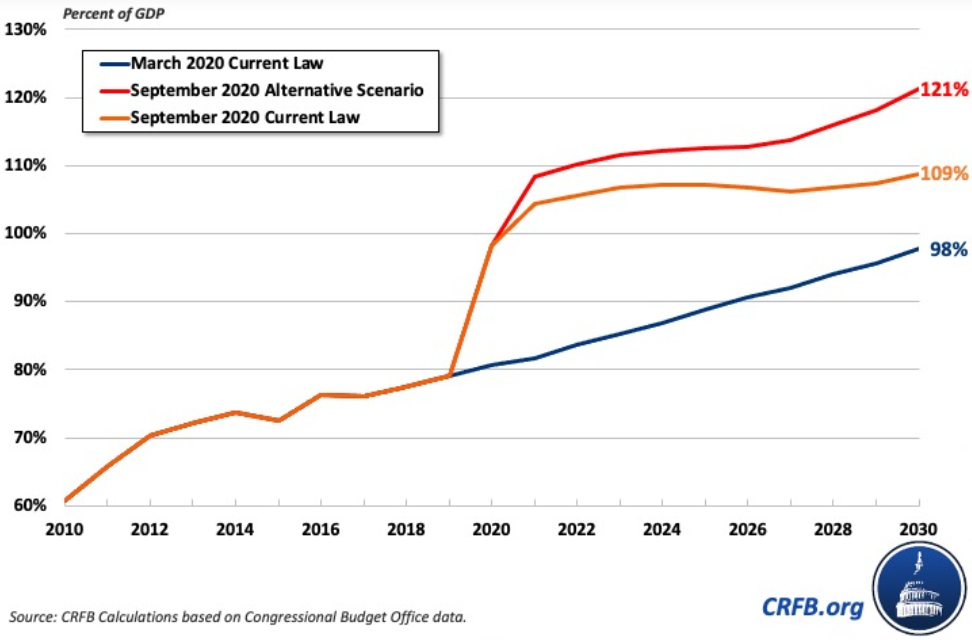

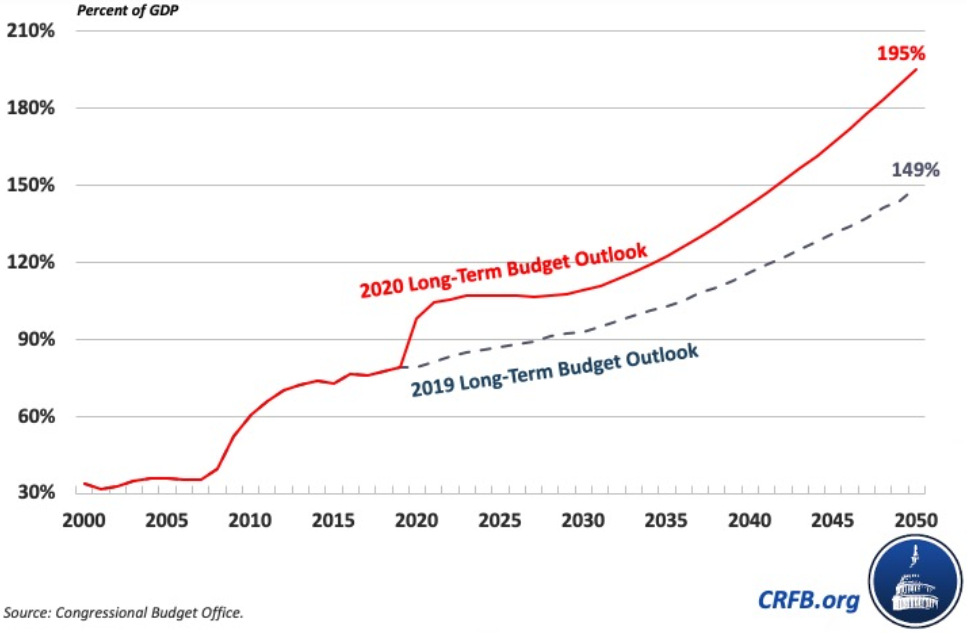

Without surprise, due to the 2020 bond bonanza and the vaccine-plus-stimulus-driven inflation euphoria, economists surveyed by Bloomberg were forecasting the 10-year UST yield to reach 1.24% by Q4 2021, from 0.93% at the time that article was written. Of course, since this was cast before the Georgia Senate run-off when it was assumed the GOP was going to keep the majority of that chamber, with the Blue sweep in Congress the expectation for the Treasuries yields are surely a bit higher now. Nevertheless, two weeks ago, on January 12, the yield on the 10-year got to 1.18%, which it could very well be the top for this year. Although there are some who are trying to make a big hoopla about the debts that are coming due this year, it has come largely unnoticed and unworthy of being a topic du jour. At first this may seem positive seeing that analysts and talking heads are ostensibly dismissing the "too much debt/many bonds" concept. Actually, they still believe this, though they think the only way that interest rates are not skyrocketing is because of the large-scale asset purchases schemes pursued by central bankers. Is this so? To begin with, let us check whether or not there is too much debt - considering only US government debt. To be clear, being a free-market advocate and a defender of laissez-faire capitalism, I take the view any government intervention, besides being immoral, creates all kinds of distortions in the economy that hinders economic activity and progress. Notwithstanding, the "too much debt", in this context, is the idea that the issuance of a ton of Treasury securities is going to not only lead to a surge in yields causing the debt servicing expenses to balloon, but also prompting an inflationary conflagration in the economy and the complete destruction of the US dollar. Looking at the chart below, it certainly appears Uncle Sam has increasingly been out of control ever since Ronald Reagan set foot in the Oval Office. After all, the amount of federal debt far exceeds the tax revenue.  In September, the Congressional Budget Office (CBO) projected debt would rise from over 98% of GDP at the end of Fiscal Year (FY) 2020 to 109% by 2030. Under an alternative scenario where lawmakers enact another $1 trn of stimulus, allow expiring tax provisions to continue, and grow annual appropriations with the economy, debt would reach 121% of GDP by 2030. Since the bottom left chart was published, CBO noted that FY 2020 ended with debt over 100% of GDP. Specifically, FY 2020 federal debt came out at $21 trn, with the debt-to-GDP ratio reaching 100.1%. This estimate marks the first time debt has eclipsed the size of the economy since 1946, when the national debt totaled 106% of GDP (top graph). Congress also enacted another relief package in late December with over $900 bn in additional COVID relief and extending many expiring tax provisions, two of the three elements of this alternative scenario. Prior to the COVID crisis, CBO estimated debt would total 1.5 times the size of the economy within 30 years – well above the prior record of 106% of GDP set just after World War II. Under CBO's latest long-term projections, debt will be almost twice as large as the economy by 2050. CBO estimates that such unprecedented debt levels could slow economic growth by about 20 basis points per year and reduce projected income by $6,300 per person. To make matters worse, debt could rise to nearly 250% of GDP if policymakers allow irresponsible tax cuts and spending increases to continue.

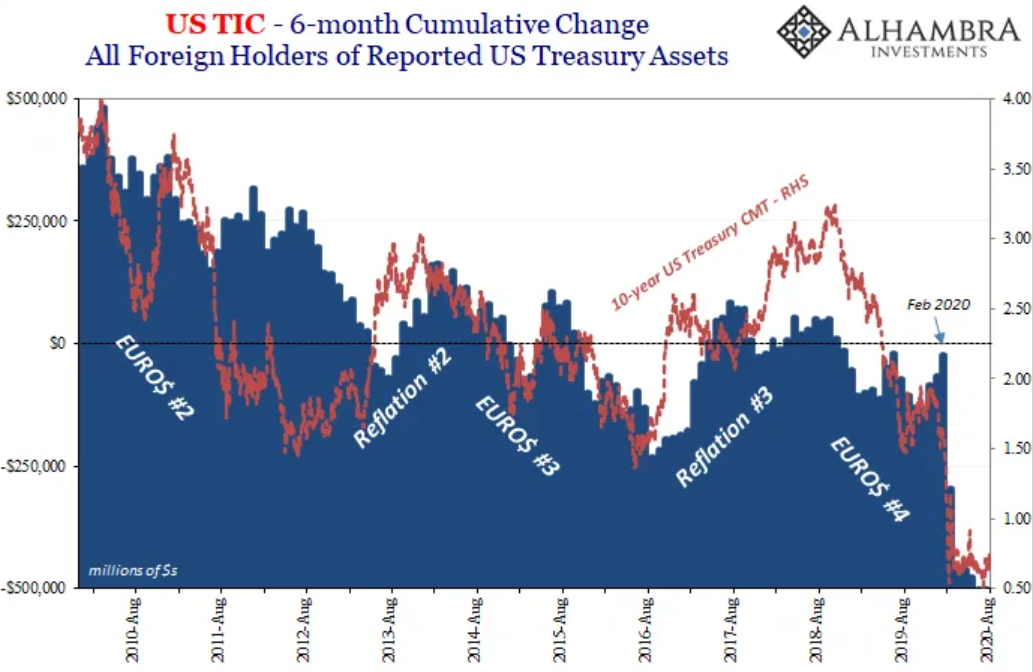

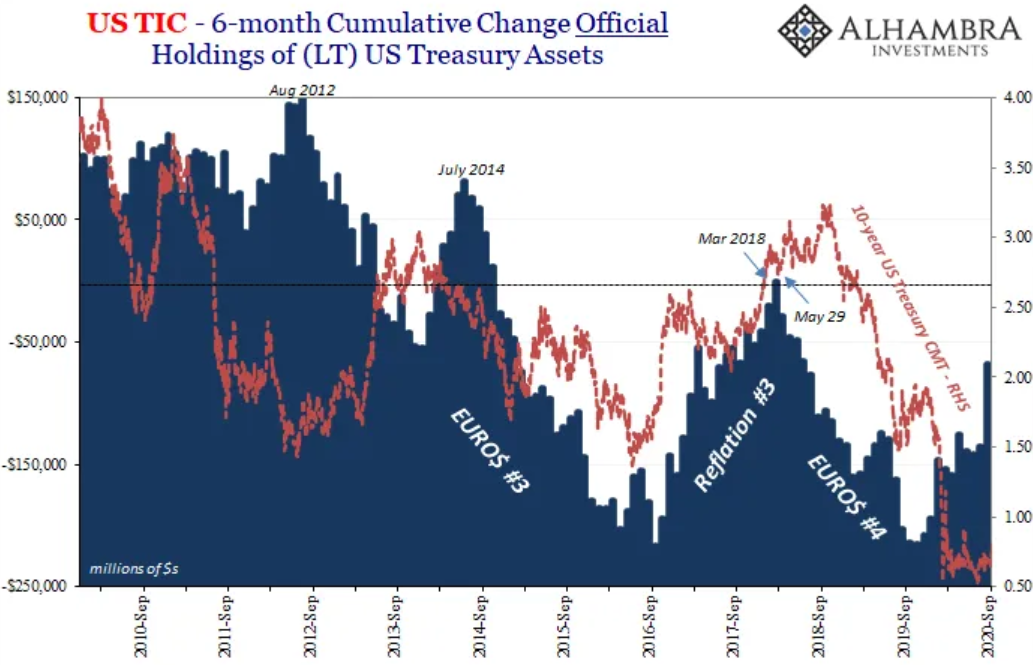

In addition, the foreign holdings of USTs have been dwindling. Particularly, the private holders are apparently - to those on the inflation camp - more sagacious than the monethary authorities, because they are dumping these "toxic" assets before the bond rout commences. Regardless of such putative selling, somebody else has to be buying (with an enthusiastic fervor, no less!). Otherwise, their yields would not have plummeted (next couple of charts). As I stated four months ago, on the October 24 post, "another common argument the inflationists and dollar bears usually make is that the contracting holdings of Treasuries by foreigners during periods of financial distress is proof the dollar is on the brink of losing its world reserve status." I went on claiming that "throughout the March panic, foreigners liquidated some of their Treasuries to satiate their need for dollars, which were extraordinarily scarce at the time. As financial conditions began to improve (because of the economy reopening), their holdings rose, though only up to July. However, at the end of August, the amount went down again, indicating that the dollar shortage is very much present." By glancing over at the most recent data, foreign holdings of Treasury securities continued to diminish up to November. Thus, even with the announcements of vaccine creations and the antecipation of bigger fiscal stimulus (due to the democrats winning the presidential election), the dollar shortage kept on ravishing the global economy.

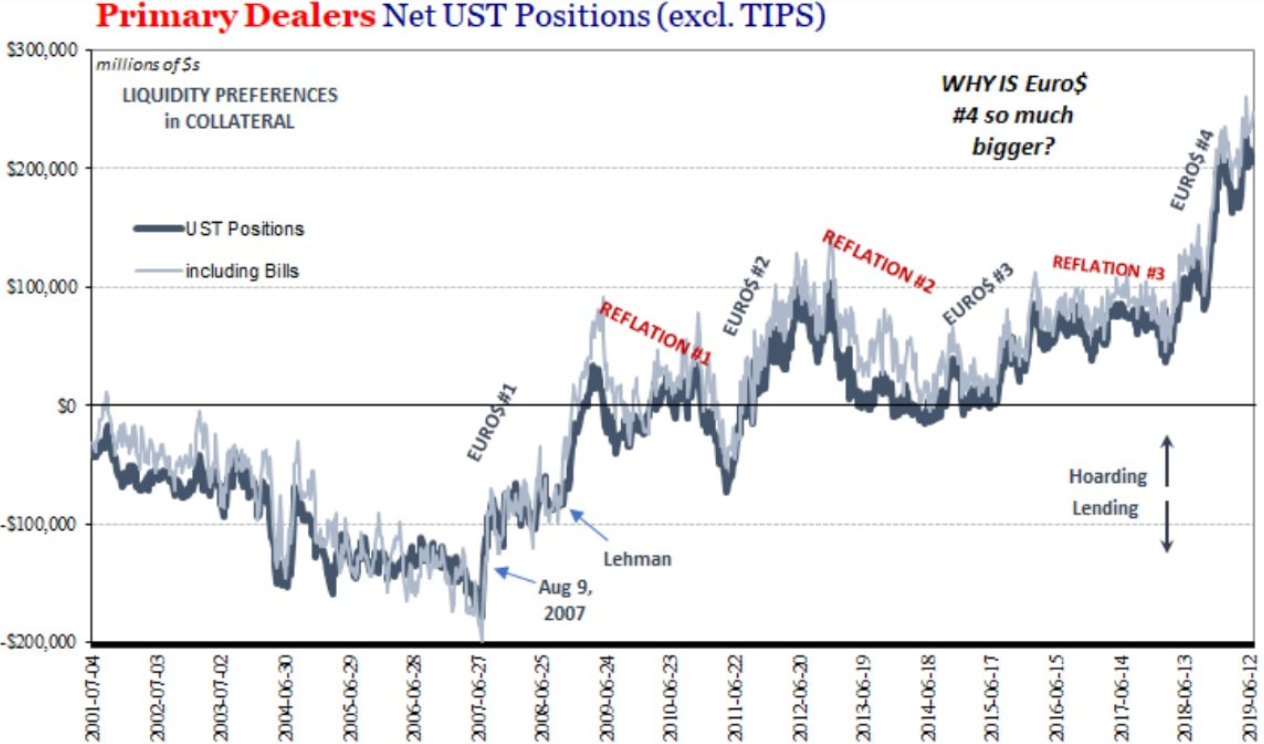

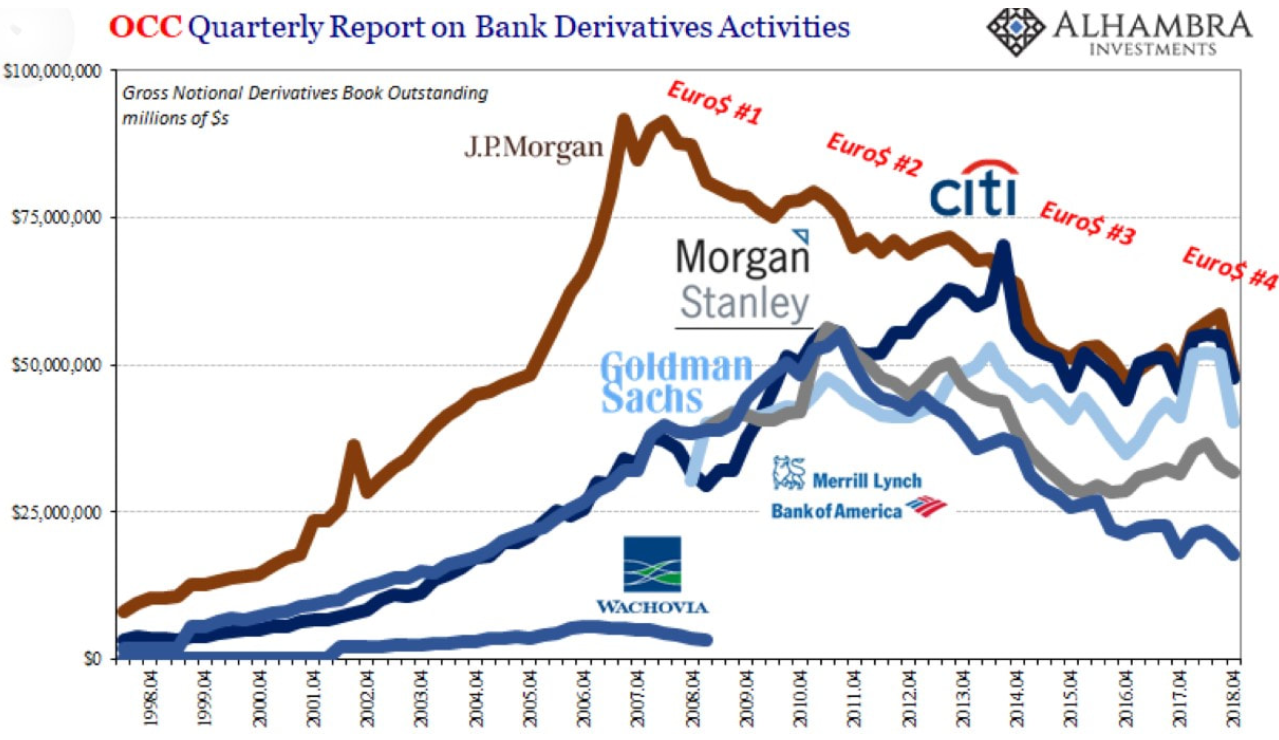

Like I expounded on that post, the banks are the ones who are leading this epic charge in demand for Treasuries. This is nothing new, as the next graph on the left demonstrates. Once again, we ought to revisit a previous post, this time the second instalment of the Eurodollar system: the untamable beast series - an extremely important reading, btw. "With the growing awareness of the perceived risk in the system, banks started positioning in an ever safer stance. When the GFC kicked off, the primary dealers reversed course and began accumulating US Treasury securities, especially after the Lehman insolvency." Moreover, "[b]ecause structured products that are used as collateral, like MBS, CLO and other ABS, are deemed riskier during periods of financial distress, banking institutions stop accepting them as collateral in the repo operations." This takes us to what the chart on the right implies. Accordingly, "in each episode of financial distress, the banks grew more wary of the risks in the system. In spite of their derivative holdings being reduced after each event, by and large, the banks would eventually return to expanding their derivative activities, indicating the shadow banking system was becoming more vivacious."

Strolling down memory lane, to the heyday of the Eurodollar system, before the GFC brought it to its knees, so much of Wall Street’s efforts during the housing bubble were focused on making markets, or market-based inputs, to price these ABS, like those well-known MBS which were obviously in vogue at that time. In spite of existing several different kinds, what they all have in common is that they transform illiquid assets into a liquid security. Hence, this process is called securatisation. Unsurprisingly, this brings about implications for the repo markets. As you know, the cash owner, the interbank repo lender, wants collateral that is highly liquid because that way the cash owner knows the collateral being received is not going to move much while in his possession. Supposing that someone arrived at the desk of one of those money dealers with a lot of papers holding title to thousands of mortgages. Were the borrower to default by not returning the cash, and the dealer now being stuck with all those individual mortgages, he cannot simply liquidate them tomorrow to get his money back. So as to solve this, these are pooled together in a securitised structure. In fact, it is possible to pool many different types of assets and securitise them: pools of plain mortgages; pools of subprime mortgages; pools of tranched pieces of pools of mortgages, or pools of pools (CDO-squared). What comes out in the end is a security which, if it has a market, then it becomes repo gold. Nevertheless, in order to have a (functioning) market, tradeable characteristics (haircuts, basically) have to remain inside acceptable limits and tolerances. By remaining so, even that toxic subprime mortgage rubbish was acceptable as "pristine" repo collateral. In spite of the whole system appearing to be perfectly safe and efficient, doubts about the quality of the collateral began to emerge, impacting the repo characteristics. If the repo funding begins with an asset like this, it starts out with prices and therefore repo characteristics (haircuts) based on liquid trading. However, in the case of a lot of mortgage-related structures in 2007 and 2008, that liquid pricing just disappeared. To anyone holding the bag (of subprime MBS in this instance), he was left stranded between a rock and a hard place. On the one hand, in view of the cash owner demanding a much greater haircut, if he were to sell this security into an illiquid market, he would take an enormous loss which might confirm to the rest of the world that he really was in tremendous distress. On the other hand, and if he did not possess another type of security that was more repo-able, he could not get the cash to fund his operations. In the end, there was no way out. Although these modern world alchemists seemed to have invented the golden financial setup that easily curbed risk and avoided losses, reality eventually set in. Sooner or later, illiquid assets show their true colours, making the derivative products impossible to use for liquidity functions like repo. Be that as it may, it was only the lower tranches (with higher deliquencies and default probabilities, etc) of these MBS and other ABS that were wiped out. The senior and super senior tranches, on the contrary, never booked cash losses, only price impairments due to illiquid market conditions. During a crisis like the one in 2008, for having an otherwise reliable asset experiencing wild swings in its price - or perhaps no price whatsoever -, that security is no longer repo-able collateral. In such a scenario, were one to dump it, he can only sell it to a vulture fund type for pennies on the dollar, being made to book huge losses that will only make his situation worse. If only he had enough pristine collateral on his books, as a back-up, where he could substitute that unassailable security in repo and, consequently, maintain the funding he needs, burying that illiquid junk somewhere on the balance sheet until the storm passes – and its value goes back up to reflect a more reasonable and fundamental valuation. The question that arises now is which securities are taken for pristine collateral? If you answered US Treasuries specially the T-bills, then you are almost 100% correct. The completely correct answer is on-the-run (OTR) US Treasuries. At any rate, a bond, note or bill just auctioned is the most liquid because it contains the most direct and quantifiable characteristics. Once a security is replaced by the next auction in the series, that security becomes highly liquid OTR, condemning the previous OTR ones into trading obscurity (off-the-run).

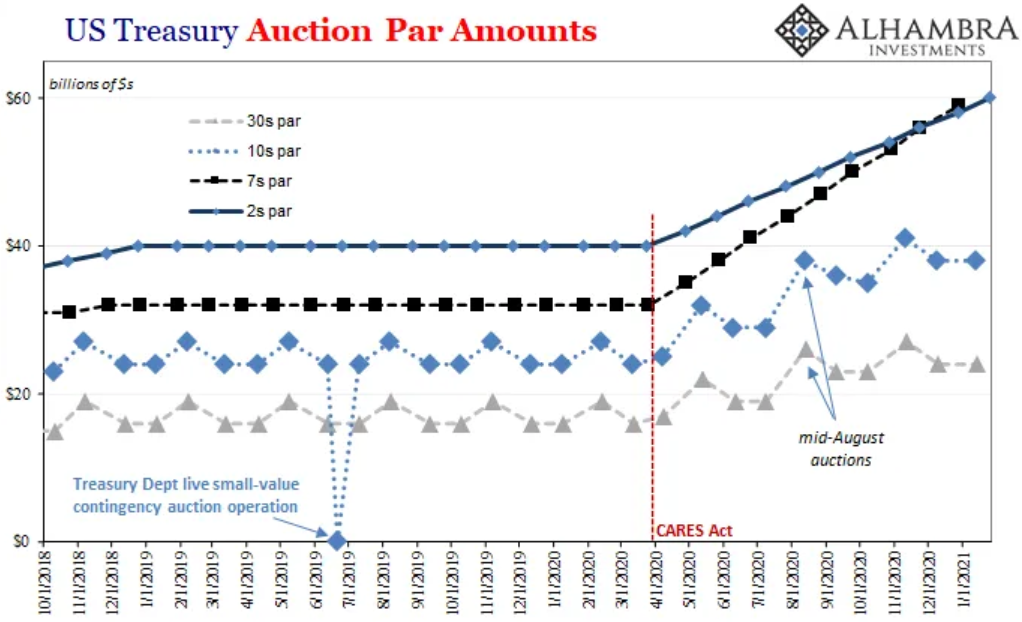

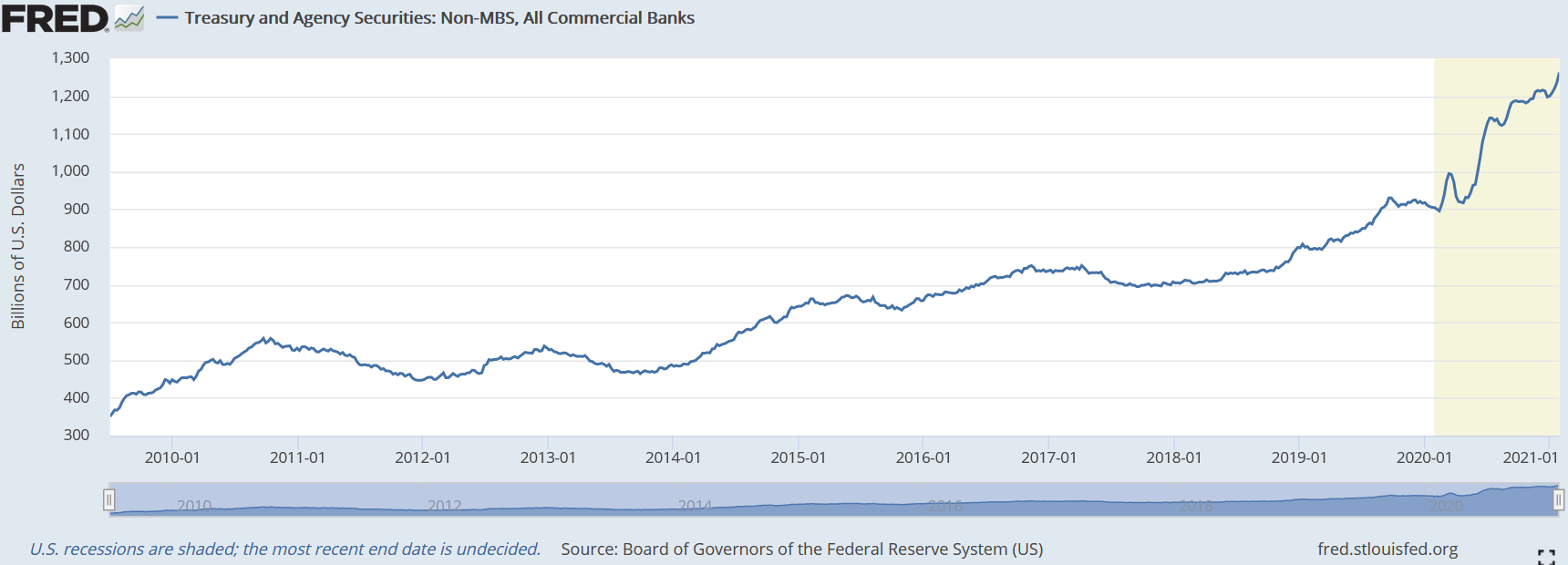

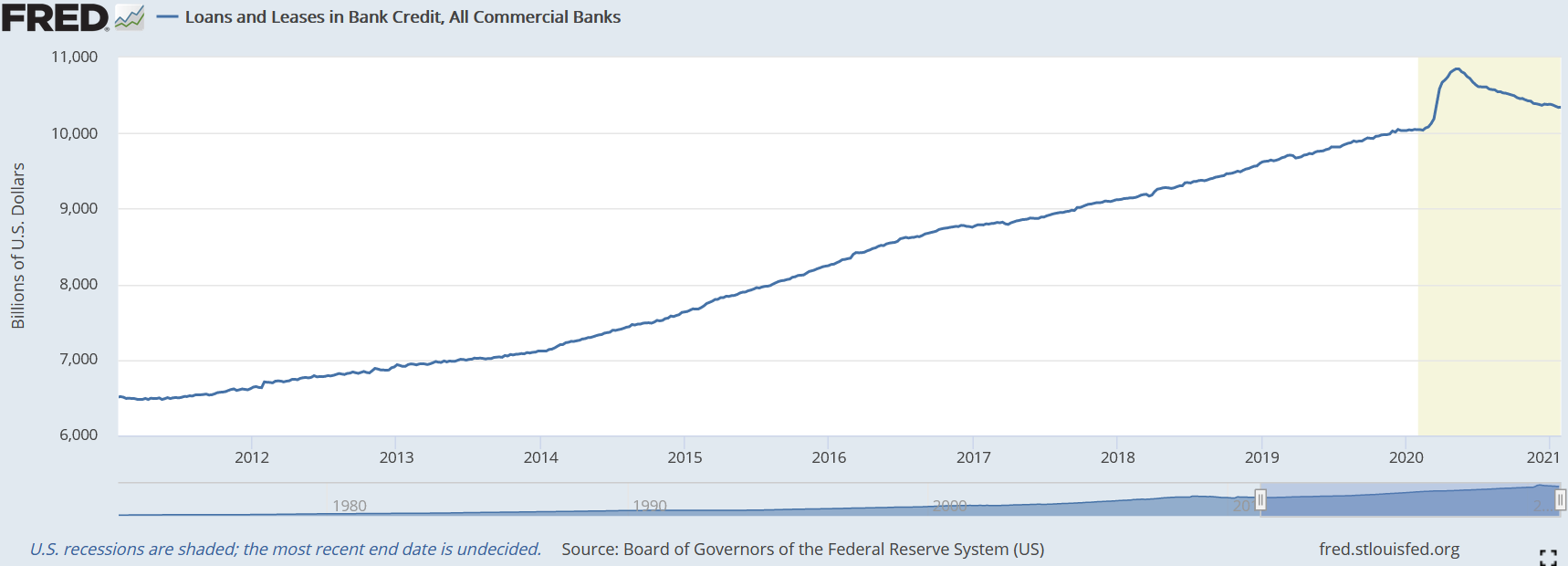

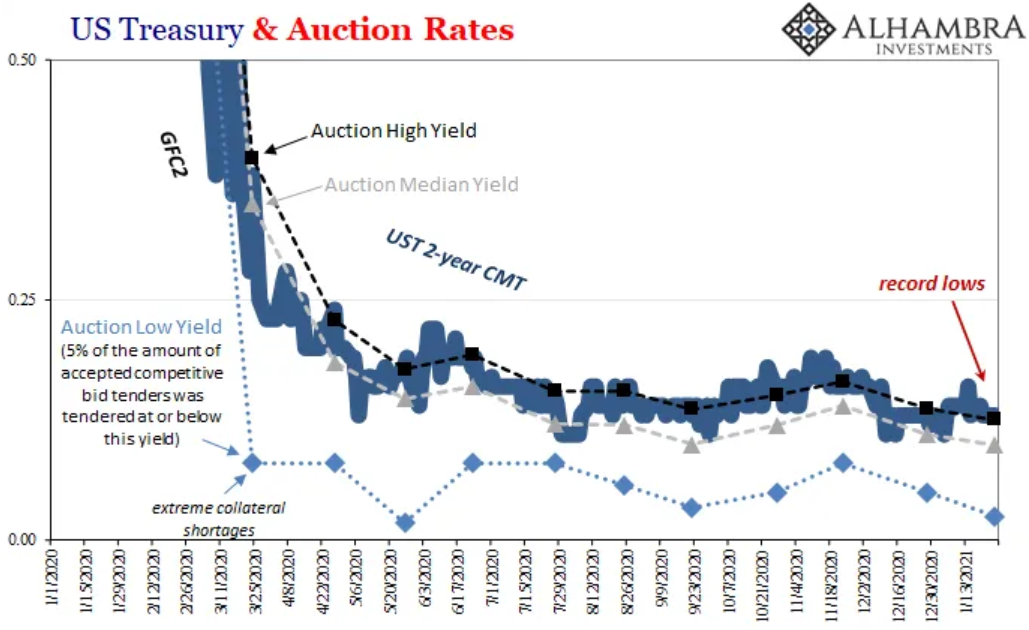

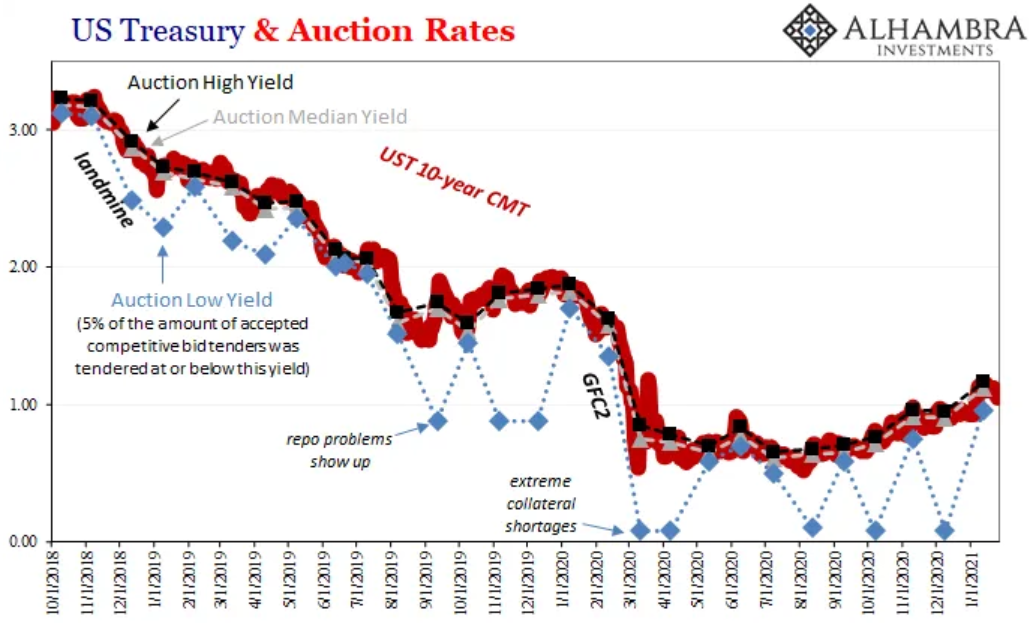

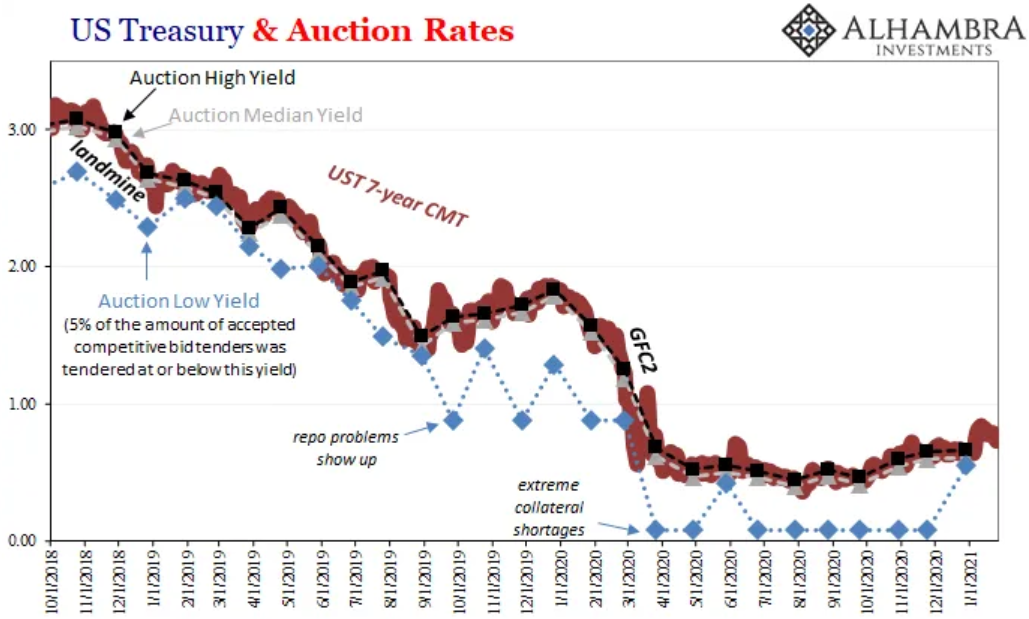

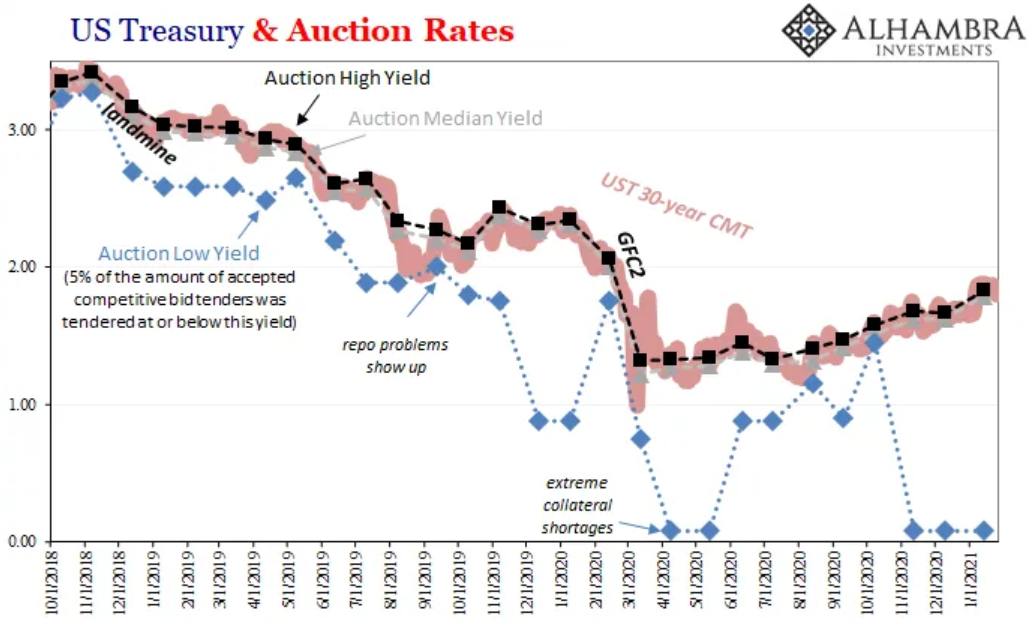

The most important lesson that banks and overall financial institutions have taken with them from the GFC is the need to build up a cushion of pristine collateral for when financial turmoil ensues, having the potential to freeze the markets of these risky ABS. Therefore, they better have some OTR Treasuries lying around on their balance sheets, in case markets turn illiquid again. To sum up, they cannot afford being caught without what are, essentially, repo reserves. That is what UST are, or German bunds across the pond in Europe. Basically, these are balance sheet tools and it truly does not matter what their return might be. Ergo, record low and negative yields in Europe and Japan (and the US is surely about to follow). In fact, the credit characteristics of the US government make no difference. The financial institutions hold them in inventory simply because of their liquidity characteristics. That is exactly what the four graphs above reflect: the insatiable desire for pristine collateral. Furthermore, if overseas monetary officials – Foreign Institutions and Monethary Authorities (FIMA) - are outright selling, as they have been pretty regularly for about seven years (like I showed further above), at the very least they are not going to be buying up as much of what is being auctioned. Owing to the way these Treasury auctions work, it would fall to the primary dealers, in addition to the direct bidders (non-primary dealers), which both bid at auction for their own house account, to make up any deficit left behind as FIMA really have retreated from UST. By performing their function as intermediaries, standing between the issuer and the public, making judgements and taking risks so that this absolutely vital (not just UST) financial space and the auctions in it operate without a hitch, the primary dealers will happily absorb the Treasuries they manage to get their hands on. Notice that I said happily and not begrudgingly or something like that. Even though they are obligated to buy whatever is left at Treasury auctions, they do it gladly. After the non-competitive bids get deducted, sorted, and wait to be filled, Treasury then conducts a Dutch tender for the remaining offer. So, primary dealers bid for it, up to position limits, submitting competitive figures for what they think they will be able to profit from: i) for their own house accounts in the sense of their bank book (holding the securities) betting on the price going higher; ii) for what their brokerage network is telling them they can sell off to the public at even higher prices; or iii) for reasons that have more to do with survival (stockpiling OTR repo collateral in their house account), of their own or intending to profit off the survival risks of others (anticipating hefty fees by lending out OTR repo collateral acquired for their house account to other financial firms very likely to be desperate for this exact OTR stuff). As the chart below suggests, despite the record amounts of Treasuries in each successive auction, these securities have no shortage of contenders. Evidently, the supply has been easily met by overwhelming demand, as indicated by the low yields at auction (above graphs), as a result signaling the obvious dollar shortage.  Thus, if the "too many bonds" theory was anywhere close to correct, we would have witnessed the price of competitive bids drop through the floor. In other words, if dealers were getting stuck with UST paper they otherwise did not want, believing this auction stuff to be nothing more than a huge headache, possibly a dangerous problem (the incorrect version of what was going on in repo), then competitive auction bids would have repeatedly reflected such dealer disdain, as dealers would have required lower and lower prices (higher yields) to compensate them for so much alleged pain. Just in case you are wondering whether the dealers or any other bidder is trying to front-run the Federal Reserve and its QE programme, to put it in plain and simple words, the Fed is irrelevant. Surprisingly to most, foreigners matter very little (still more than the Fed, though). One key reason why is that when foreigners are selling their Treasury securities, thus refraining from the same level of UST auction participation, that hints at "tight money" stuff which, rather than being a danger to the UST market, proves to be the reason for heightened demand in it, especially OTR, coming from dealers whose thirst for liquidity appears to know no bounds (top chart). Hence, their holdings of UST continue to mushroom, while the credit origination to the real economy (bottom chart) keeps on the downward trend kicked off in April.   In conclusion, this whole thing reminds of Mr Creosate from Monty Python's The Meaning of Life. Everybody thinks the Treasury market is on the brink of exploding with too many UST. Just one more tiny, little billion dollars for the bond rout and inflation to be unleashed .

Although I am sure there is some breaking point, since after all everything has one, the UST market seems to defy the laws of physics. Nevertheless, it does not defy the laws of (monetary) economics, regardless of what all the analysts and economists spout to the public. Perhaps, it is not like Mr Creosate. Now that I think of it, there is another film that provides a better analogy, The Blob. A theme for another day.

0 Comments

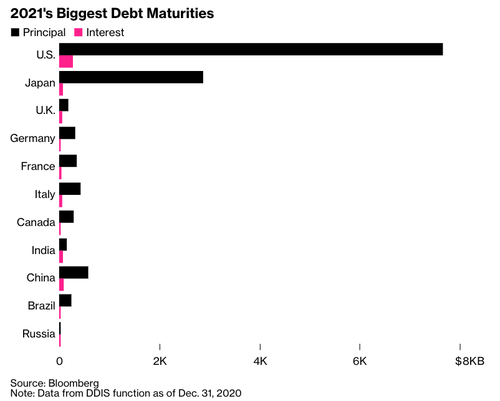

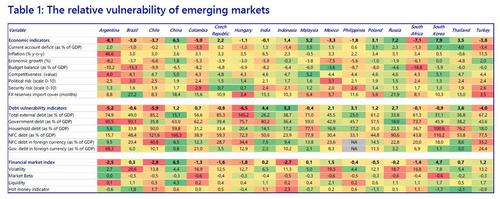

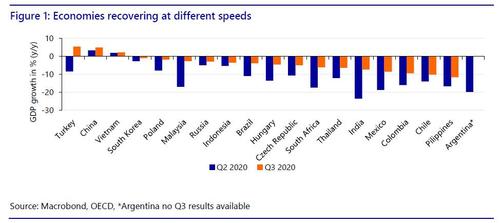

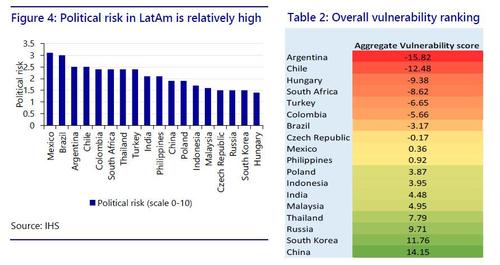

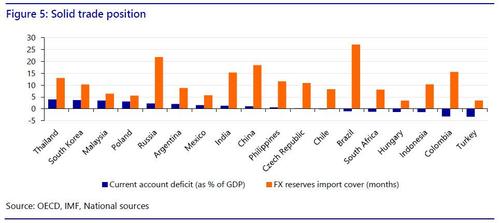

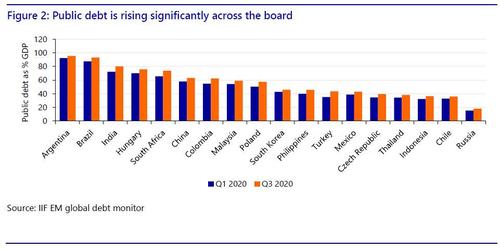

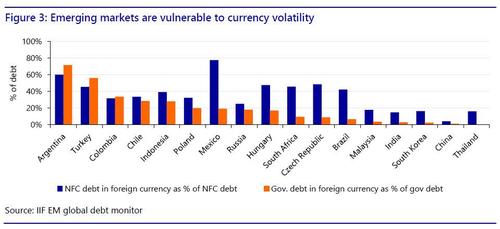

To kick off the New Year, the world's largest economies face a massive global debt overhang brought about by the corona-phobia. In round numbers, some $13 trn in debt is coming due and will need to be refinanced in an ultra-low rate environment. Basically, seven top economies plus several major emerging markets "face the heaviest bond maturities in at least a decade, much of the borrowings to dig their economies out of the worst slump since the Great Depression," according to Bloomberg, adding that these governments will need to roll over at least half of this debt in 2021. Although this sounds alarming, I agree with Gregory Perdon, co-chief investment officer at Arbuthnot Latham, when he affirmed that "government debt ratios have exploded, but I believe that the short-term worrying over a rising debt is fruitless." Notwithstanding, I take issue with his other claim that "debt is leverage and assuming it's not abused, it's one of the most successful tools for growing wealth." Undoubtedly debt can be a tool for acquiring or creating wealth. However, when it is government debt that is in consideration, this is only a boon for those well-positioned cronies who have a relationship and are in contact with the legislators or the whole bureaucracy in general. To wit, the largest government debt refinancing will be in the US, with $7.7 trn of debt coming due, followed by Japan with $2.9 trn. To boot, China has $577 bn coming due, Italy has $433 bn, followed by France's $348 bn and Germany has $325 bn.  Contrary to popular opinion, the low-rate paradigm is not a product of central banking machinations, but a product of a deflationary economic environment with too much risk for too little reward. Thus, as I stated on the December 30 post, "liquidity has been the top concern for participants in the financial markets (...) Accordingly, investment grade bonds have been an oasis of liquidity during this inhospitable desert that has been the 2020 economy. (...) No matter by how long or how much they do their QEs, credit and "liquidity" facilities, YCC, etc, these are all smoke and mirrors aimed at duping you into believing they possess the mastery over financial markets." Nevertheless, with sovereign yields plunging to record lows, it is only reasonable that governments across the world flood the market with as much debt as possible so as to turn this rebound into an actual recovery - good luck! - or, at the very least, preventing it from rolling over. However, this panorama of ultra-low yields is being experienced almost exclusively among the developed economies. In the emerging markets domain, the contraints on the Eurodollar system, prompted by the colossal loss of activity coupled with tremendous uncertainties about the future, have put these economies under grave peril. In order to have a sense of the vulnerabilities to the current (euro)dollar shortage these countries are carrying, Rabobank has come out with a compelling and succint report on this issue.  According to this report, the most important factor explaining the rebound magnitude on Q3 (Q2 in China's case) was the level of containment of the virus. Moreover, the countries' dependency on the tourism sector was also detriment for the economic performance on the third quarter, with Thailand and the Philippines having a lousy Q3 figure. On the flipside, countries that either lifted their restrictions on movement and activities or happened to export a lot of in-demand medical and electronic goods, or a combination of both, underwent a relatively robust rebound. In addition, as you can clearly see, the more sluggish economies tended to be the ones in the southern hemisphere where the third quarter lands on their winter season, rendering the best environment for influenza-like illnesses to thrive. Evidently, economic activity remained very constrained in Q3 mainly because of government imposition.  On the left graph (below), in which countries are ordered by their ratios of government debt, Argentina, Brazil and India are the ones that are most in jeopardy of losing control of their finances, solely bearing this indicator in mind - the others being presented by the heatmap above. Seeing that individuals and businesses were in dreadful need of some financial relief, these countries, as was the case all over the globe, have increased their public debt. Among the biggest debtors, Argentina's debt rose 6% of GDP, Brazil 8.4% of GDP and India 8.5% of GDP. In view of the fact that high debt levels are a constraint to future economic growth, they have to be avoided. Furthermore, the governments' capacity to spend could be restricted by higher market-imposed interest rates due to higher default/foreign exchange risks, as well as by a higher share of the government budget that has to be allocated towards debt repayments and not towards "stimulating" the economy. Moving on to debt denominated in foreing currency (below on the right), Argentina, Turkey and Indonesia are the ones most at risk of devaluation of their respective domestic currencies. Even though the writer of the report claims that "[t]his dependence on foreign capital constrains the set of monetary or fiscal mechanisms that can be used to stimulate the economy" and that "cutting central bank interest rates depreciates the local currency, indirectly increasing government debt levels in terms of the local currency", it is better to revisit what I wrote a few weeks ago, on the Christmas day post, to understand the true workings behind these operations and, consequently, comprehend what is wrong with his statement. In the foreign exchange (FX) markets, "these countries' [EM's] currencies are not transacted as much nor are these exalted the same way as the major currencies from the putative developed economies, owing to being less liquid (smaller market with fewer buyers and sellers) and/due to market participants having less confidence and use for these currencies - afterall, this is the Eurodollar system. Hence, the monetary situation in the EMs are extremely dependent on the volume of foreign exchange that goes through their economies, chiefly the US dollar (check out the US vs the World part I and II)." Therefore, the EM central banks are incapable of depreciating their currencies by cutting interest rates. In fact, the plummeting value of an EM currency and lower interest rates are both symptoms of the same condition, the dollar shortage. More of this later on.

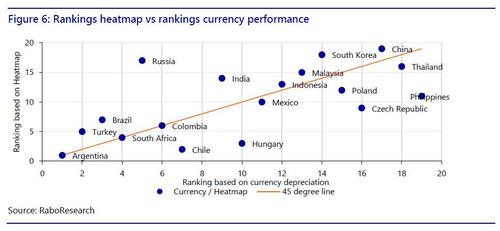

Among this group of EM countries, and compiling the data from the heatmap, Rabobank developed a vulnerability score for each economy, which was then disposed in a ranking layout (Table 2 on the right). Overall, Asian countries appear to be the most resilient, followed by the East European ones and lastly those in Latin American, which also carry the greatest political risk, albeit low in absolute terms.   In order to analyse the chart above, let's once more return to the Christmas day post for it kicks off the explanation rather nicely. Keeping in mind that the monetary conditions of the EM economies are based on the flow of FX - US dollar having the biggest weight - in their monetary/banking systems, "in periods of (euro)dollar shortage resulting from global trade contracting (or perhaps just slowing down) and/or financial institutions that take part in the Eurodollar regime being (even more) unwilling, for whatever reason, to supply these very vital dollars (or euros, yens, etc), the banking activity in the form of credit creation is severely impacted in these developing economies." Too confusing? Perhaps I should have started from the beginning. To make this easily digestable, I am going to keep this simple and brief. As you know, money (or currency or credit, whatever you want to call it) is originated by the banking institutions and to some extent the central banks. What's more, because, like I said before, EM currencies are less liquid, these countries are pushed into using the major currencies that have reached the status of global reserves, with the USD being the supreme one. For the sake of argument, and since this is the Eurodollar system, I am just going to consider the USD, though other major currencies, especially the euro, are rather relevant. All the same, insofar the world economy is growing and the global trade is running smoothly, as well as growth prospects are conducive to make the Eurodollar banking institutions willing to provide credit, the amount of dollars that go through the domestic monetary systems of the EMs balloons, leading to more credit creation and, hence, a larger domestic currency/money supply. In turn, their economies can grow. Now I think you can grasp what I said above. As the keynesian textbooks argue for, central banks should accumulate a cushion of reserves, so that during bad times (dollar shortages) they can use them to fulfill the need for dollars (or euros, etc). In spite of sounding reasonable, there are two problems with this reasoning that I am going to demonstrate afterwards. To conclude the report, Rabobank shows the correlation between its vulnerability ranking and the countries' currencies performance ranking. Unsurprisingly, the more vulnerable ones have also experienced the greatest currency depreciation, in general.  Despite the discovery of multiple vaccines and the promise of unlimited fiscal and monetary stimuli, I am afraid things will first get worse before they start to get better. To be clear, I am refering to the economic and social fabric, not the kung-flu per se, obviously, since it never posed any serious danger. Be that as it may, you may already know how the story goes in the media. To spur the economy for it to get back on track, central banks must cut interest rates so as to increase bank credit to support economic growth. Although that is how it is taught in college and pontificated by the press, in reality the story has a completely different plot. Resuming where we left off in the discussion about the reserves cushion of central banks - once again, considering just the USD. As I contended, two dilemmas arise when a central bank liquidates its dollar-denominated assets, which are almost fully made up of US Treasury securities, to dole out to whatever entities feeling the full force of the dollar shortage. Firstly, as soon as the central bank does this to preclude its currency from depreciating against the dollar, the currency does, in any event, fall. Why? Because the central bank is sending a telegram to everyone revealing that the economy is in trouble and its agents (businesses, financial institutions, households and maybe government) are in great distress. Otherwise, if there were no significant woes, the central bank would stay put. Secondly, and more salient one, these dollar reserves account as assets on the central banks' balance sheets. Ergo, when a central bank decides to pursue that effort, the left side (assets) of the balance sheet shrinks. As a result, the right side has to follow, which means the money supply needs to contract to maintain the value of the currency. Alternatively, therefore, if the diminishing monetary aggregate is to be avoided, then the currency value has to drop. If you thought central bankers in the developed economies were powerless, then what to say about their counterparts in the developing countries. At least Powell, Lagarde, Kuroda and the like can pretend as if they possess the mastery of the economy and the markets. Unfortunately (to them), those poor EM central bankers cannot even do that. Despite all of this, the keynesian perscription continues to be shamelessly put forth, by economists and the media, and sadly put into action. According to the most recent Bloomberg’s quarterly review of monetary policy, "[c]entral banks are set to spend 2021 maintaining their ultra-easy monetary policies even with the global economy expected to accelerate away from last year’s coronavirus-inflicted recession." So many things wrong in such a short paragraph - and that was the first one of the article. To be fair, the writers state that accomodative policies have been hard to pursue by EM central bankers, on account of prices soaring within or above their target ranges. This has mainly been the result of the upswing in the dollar during the March meltdown, which struggled to come down, against EM currencies, to its pre-panic level (next graph). Furthermore, these Bloomberg writers, as is the case with the Rabobank report's analyst, are expecting the dollar to keep plunging. But why should it keep on falling? Before I proceed with the explanation, there is a caveat to consider: the divergence in monetary and fiscal policies will be one of the main drivers in relative performance of the EM local currencies.  In spite of the monumental magnitude of "stimuli" and the vaccines that will, hopefully, open the economy (if our overlords allow it), the economic depression is going to prolong, for the slowdown - check out part I, II, III and bonus about this - witnessed throughout the summer has extended to the fall, reaching winter to what may turn out to be yet another contraction, particularly in Europe.

At any rate, the EM nations are feeling the stress of the dollar shortage prompted by the economic shutdown and restrictions that followed, with the poorest ones already being in dire straits, as the Washington Post reports. "Thirty-eight low-income countries are either in debt distress, according to the IMF, or at high risk of falling into it. Unless private creditors and wealthy nations step up and agree to concessions or outright debt forgiveness, the pandemic's fiscal shock could hurl some of those, as well as highly leveraged middle-income countries such as Costa Rica, toward catastrophic national bankruptcies." To conclude, and now it all comes together - cue Steve Carell in The Office -, EM economies are stranded between a rock and a hard place. On the one hand, if fiscal and monetary technocrats of some country just sit idly by or close to it, due to being wary of opening the inflation spigots, kind of like China or Russia are doing, businesses and individuals are going to go through a massive insolvency event where they will not manage to service their debts, because they will not be able to obtain the income nor will central banks be inclined to supply the dollars so that the dollar-denominated debt can be serviced. The latter being the essence of the problem being discussed. On the other hand, if the technocrats happen to be overly eager to act, they put their countries at risk of turning into a basket case, like Zambia as outlined in the WaPo article. "The sub-Saharan nation fell into default in November, a result of its high reliance on foreign debt; a pandemic blow to the price of copper, its main commodity; and one of its worst droughts in 40 years. The country is now printing money to survive, forcing a devaluation of the kwacha and creating spiraling inflation that's spreading misery at the worst possible time." Finally, as I proclaimed on Christmas day, there are two ways these countries will end up: "1) a sovereign debt crisis with some high inflation as the ones in Latin America in the 80's or in Eastern Europe in the 90's, or 2) a hyperinflationary crisis of the likes of Venezuela or Zimbabwe that occurred recently." Either way, as you see, culminates in misery and inflation, forget about growth and development. For the time being, though it may last for awhile, that is what the E in EM stands for. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed