|

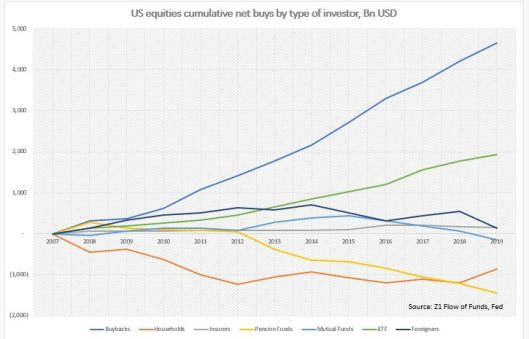

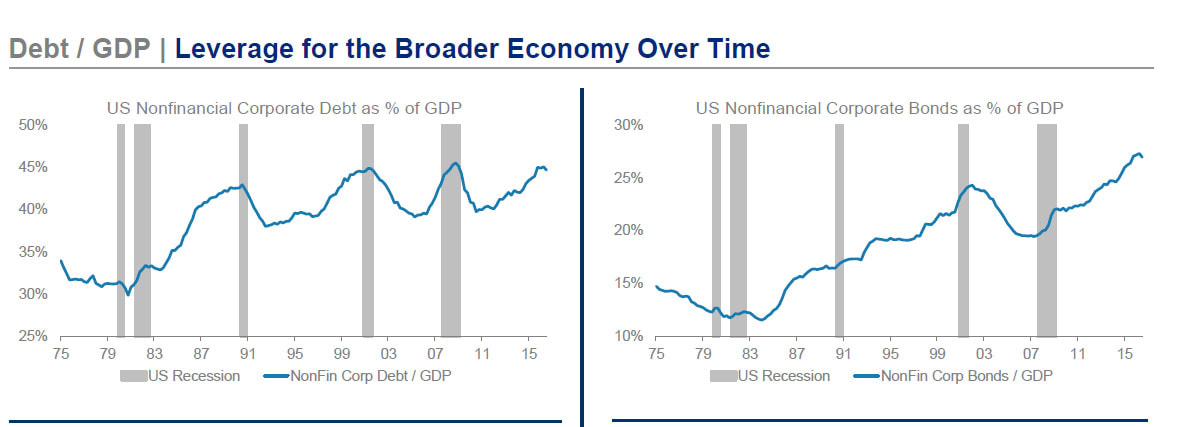

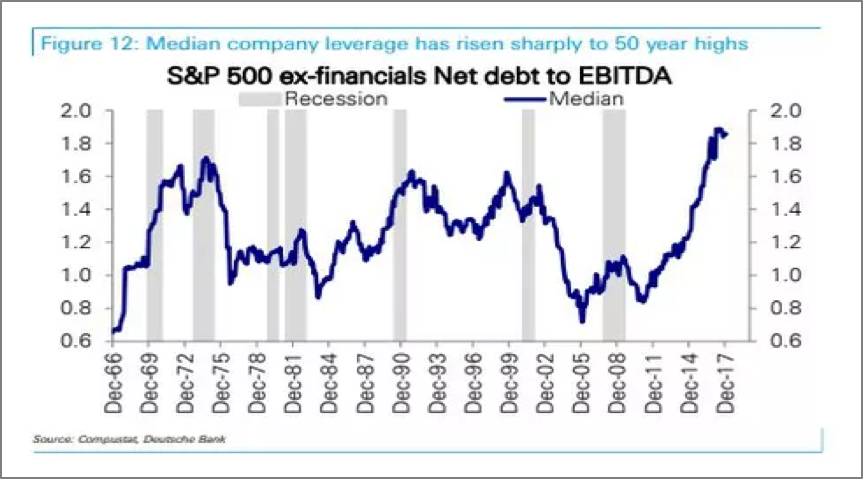

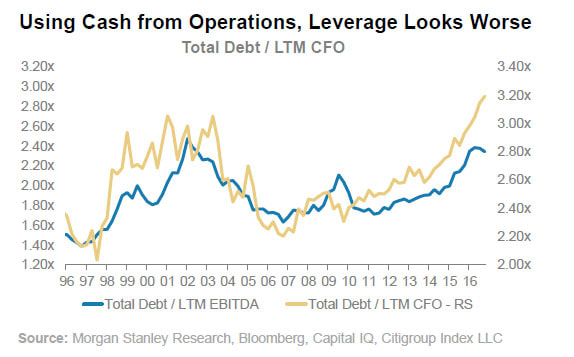

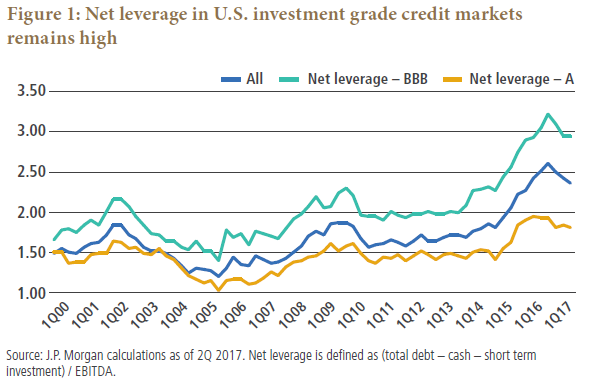

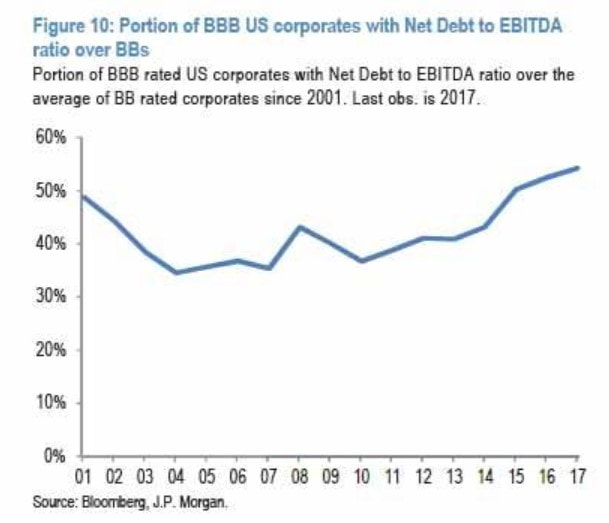

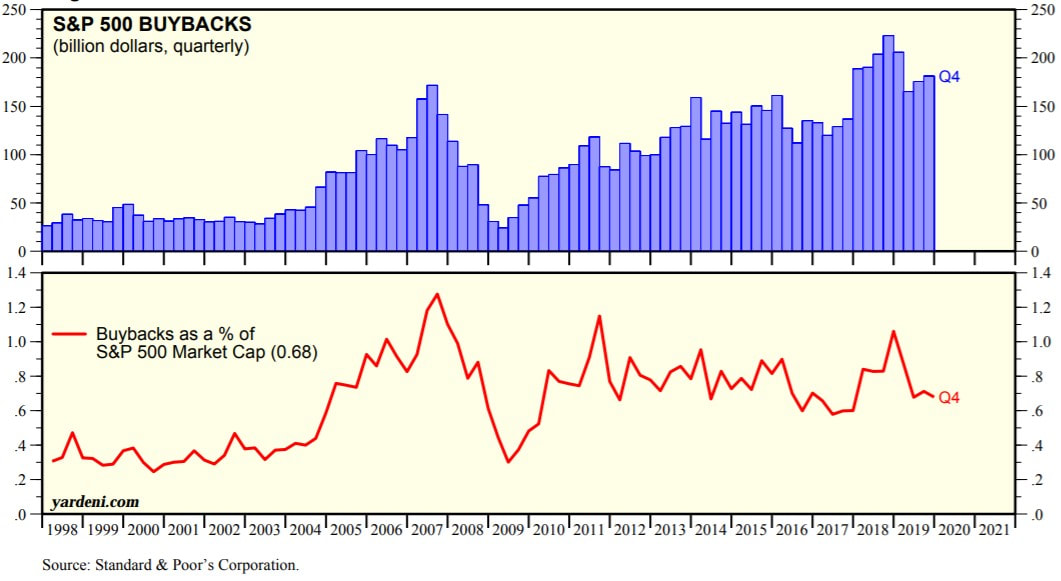

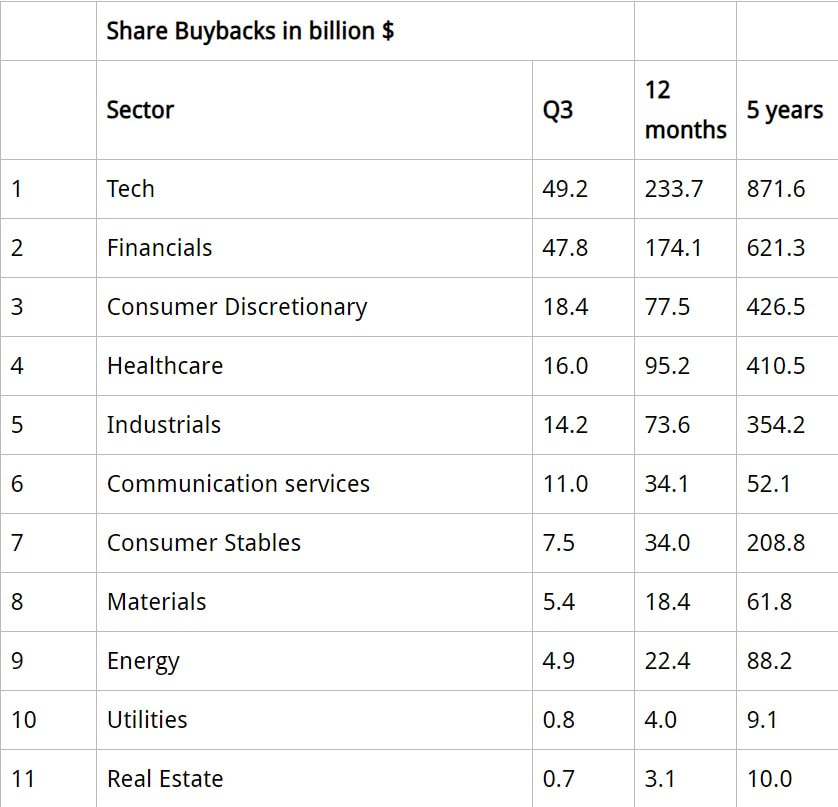

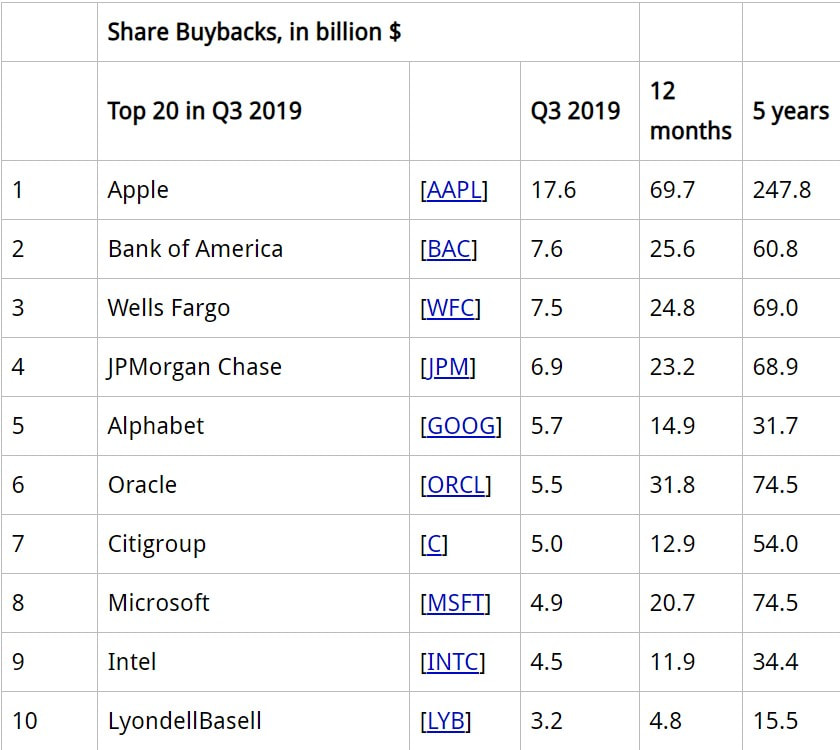

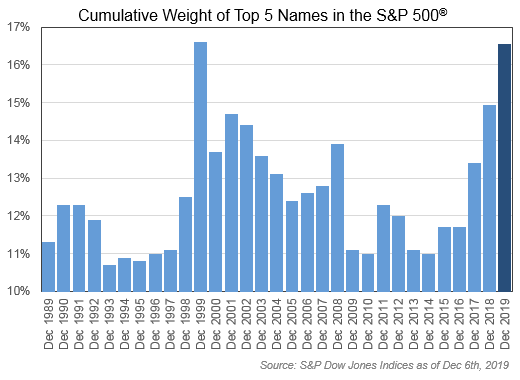

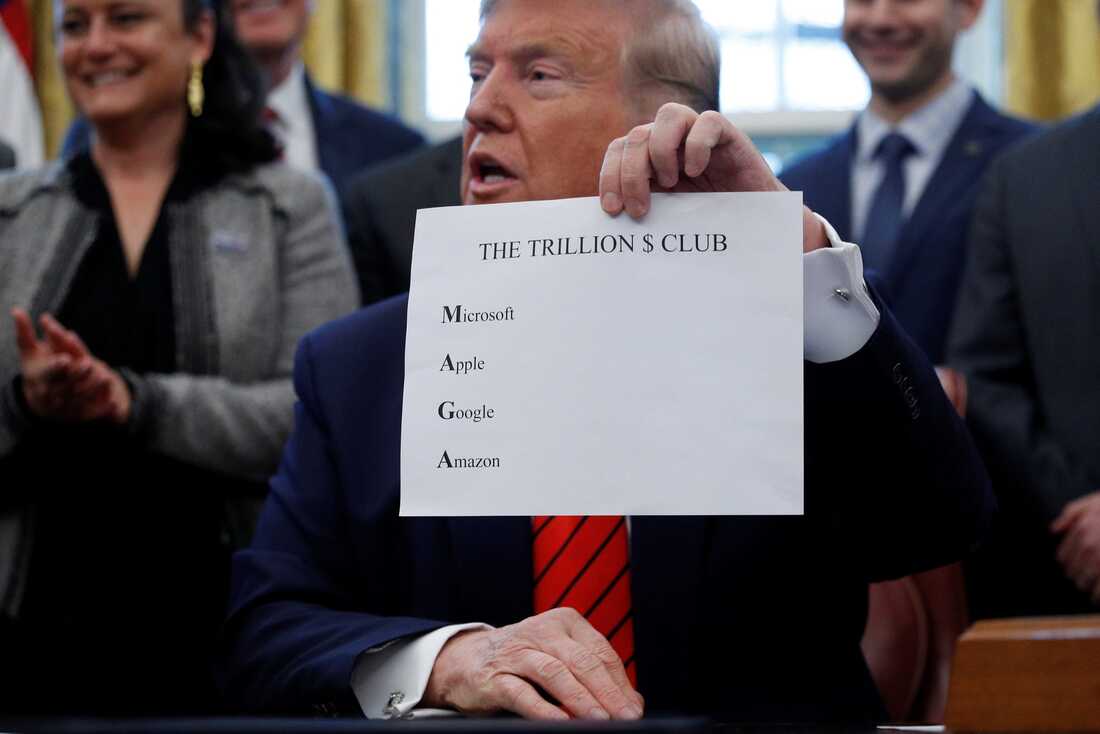

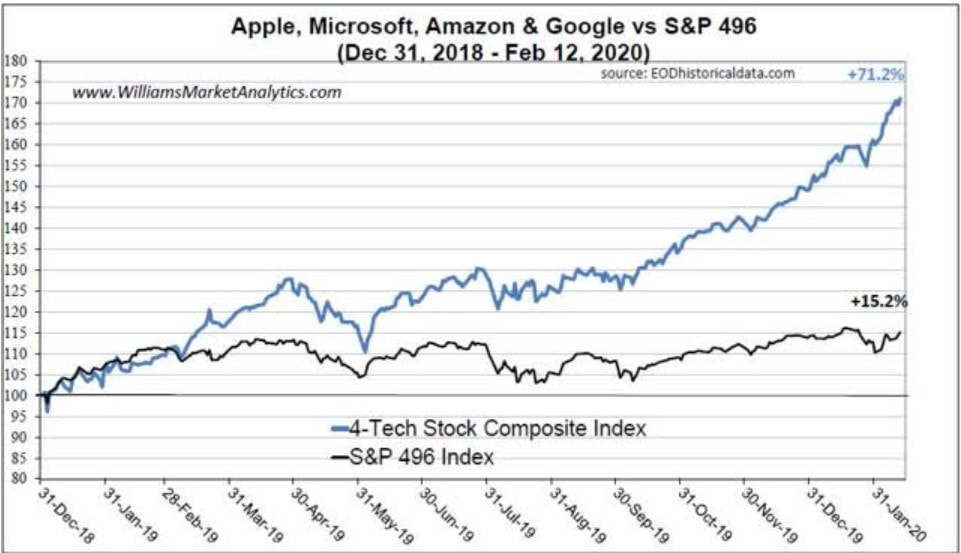

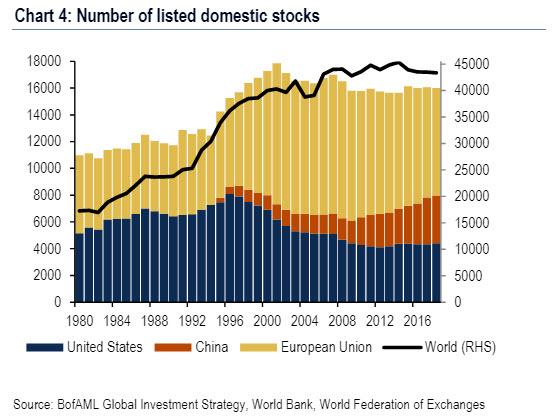

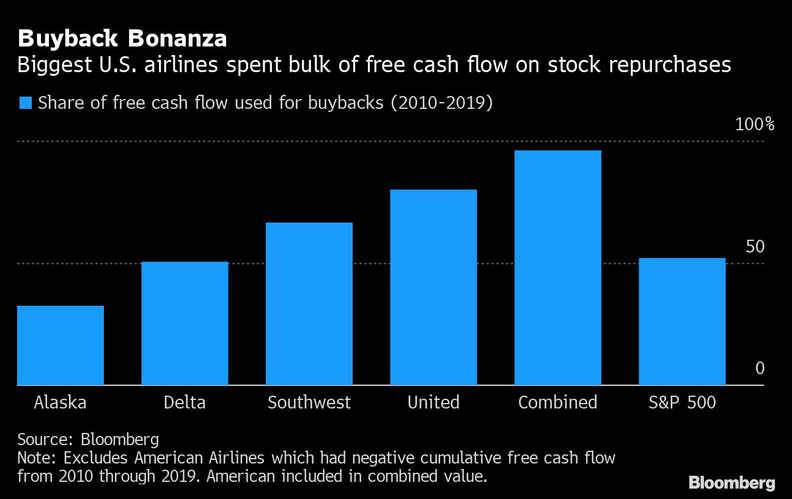

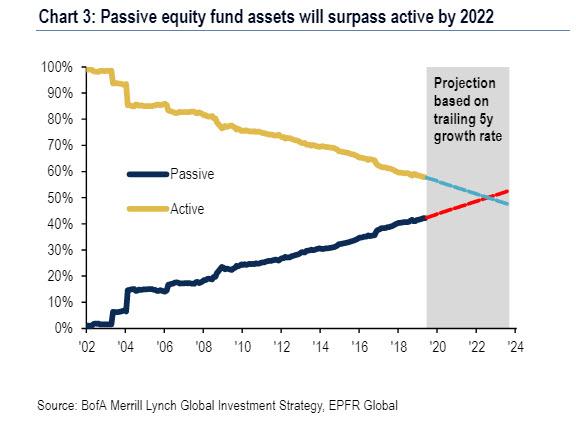

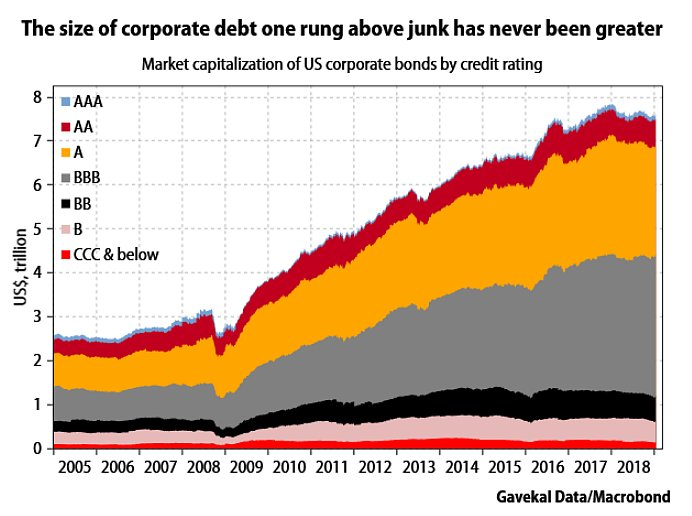

The biggest buyers of US equities since the GFC were corporations. With the buybacks coming to a halt due to the meltdown of the corporate bond market, and the financial system in general, corporations can no longer get the cheap and easy financing to buy their own shares. Therefore, the stock market will only surge again if some other market participants step up. If you have been following this blog recently, then you already know which one will be. As I just stated, buybacks were by far the biggest contributors for the longest bull market in the history of the US, followed by the passive investment in ETFs. Additionally, foreigners and insurance companies were buyers too, though insignificantly. On the opposite side, mutual funds, pension funds and households were all sellers.  The corporations took advantage of the ZIRP and the liquidity provided by the Fed to lever up to record levels. Furthermore, because investors were in search for yield in a low interest rate environment, they were forced to pursue greater risk in their portfolios. As a result, the demand for corporate bonds increased and the corporations were happy to supply them.  In addition, it was not just a few bad apples that got themselves into so much debt and, consequently, made corporations as an aggregate look reckless. By looking at the chart below, it is clear this strategy was pervasive. The net debt (debt minus cash and cash equivalents) to EBITDA (earnings before interest, taxes, depreciation and amortisation) reached levels never seen before.  Likewise, the debt to cash flows of the last twelve months from operations also arrived at historical magnitudes. This means the ability to pay their liabilities became relatively very diminished.  Moreover, 50% of the investment-grade bond market sitted (until a month ago) on the lowest rung of the investment-grade ladder. In a recession, BBB-rated bonds are the most vulnerable of all investment-grade bonds. According to Moody’s, 10% of BBB-rated corporate bonds are downgraded to “junk” status in a recession. Since the number of BBB-rated bonds has exploded, we will see more such cases than ever before in this one. Taking a look at the graphs below, you can see BBB-rated corporations have been especially reckless, with more of them setting themselves up to being downgraded to junk.   Furthermore, one of the reasons companies accrued so much debt was to repurchase their own shares. Despite the absolute amount having piled on year after year, the buybacks in relation to the market capitalisation actually stayed below the levels of the housing bubble.  In terms of sectors, tech companies bought back $49.2 billion shares in Q3 2019, while the financial institutions repurchased $47.8 billion, for an aggregate amount of $97 billion, which means those two sectors made up for 55% of all share buybacks.  The four beloved banks – Bank of America, Wells Fargo, JP Morgan Chase, and Citibank, in that order – among the top seven share-buyback queens below, between them bought back $86 billion of their own shares from the start of Q4 2018 to Q3 2019, and thereby reduced their equity capital by $86 billion, which is what share buybacks do - when a company buys back its own shares, it pays cash for those shares, the shares get canceled and disappear, and the cash is gone, and the company's equity on the balance sheet drops by that amount. Yet, those $86 billion could have come in handy right now so as to deal with their losses on their loans to commercial real estate projects, to businesses, and to consumers. Instead, those $86 billion have gone to waste.   In addition, of the five most valuable US corporations - up to mid-February -, four make the list above: Apple, Google (Alphabet), Microsoft and Facebook, only Amazon was left out. These companies are the spurs that made this bull ferocious, being the only ones that significantly surged in the last decade. Thus, their weight in the S&P 500 index gradually rose. Even though the graph below shows that the their cumulative weight did not pass by the end of last year the 1999 level, by February 11 of this year, which was pretty much the market high, the top five made up 18% of the S&P 500, breaking the record.  Likewise, the MAGA stocks (Microsoft, Apple, Google and Amazon) were given this nickname this year when all of them achieved the trillion dollar valuation, prompting President Trump to exalt.  Anyway, these corporations carried the whole S&P 500 on their backs. On an equal-weighted index comprised of the MAGA, from the start of 2019 till February 12 of this year, they shot up 71.2%. Still, the index composed of the other S&P 500 companies, the S&P 496, throughout the same interval, only rose 15.2%.  Additionally, like I said above, the low rate environment enabled corporations to lever up. In spite of the mounting risk associated with lending to such indebted entities, seeing that the appetite for yield could not be satisfied with low-risk assets, investors had to satiate themselves with risky assets such as corporate bonds. Consequently, the demand hardly decreased when the leverage intensified, keeping yields at quite modest levels. However, the party has come to an end. The spreads are widening and the easy financing is no more.  Since the start of the bear market, there has been record inflows to cash and cash equivalents, on one side, and, on the other, unimaginable record outflows from bonds - data until March 25. Because investors are fleeing the corporate bond market, their prices are plunging, resulting in the expanding spreads between theirs and the Treasuries' yields.  However, the MAGA posse continues to attract investors, which may be making their weight in the S&P 500 to swell.  Moreover, the cheap and easy currency creation provided by the Fed leads CEOs and CFOs to invest in themselves. The rationale is that the interest rates are cyclical. Hence, when these start to climb, the companies finance themselves more so through share issuance. Critics of the buybacks complain that companies should be taking advantage of the low interest rates to invest in productive capacity and R&D, as well as pay bigger wages to their workers. Well, they already do these things. Although it would be nice if they did even more, the reality is that there is a limit for such actions. That limit is the demand. Consumers are extremely indebted and, as a result, they cannot indulge themselves in impulsive shopping sprees. By looking below, consumers are still recovering from the GFC.  Financial engineering is what share buybacks are all about. They lower the shares outstanding, and so earnings are divided by a smaller number of shares, which produces a larger earnings per share figure, when in fact the actual profit of the company has not changed.  The question of how stocks can keep rising in the face of these massive outflows from stocks emerges, although as BofA's CIO Michael Hartnett writes, the puzzle of record equity prices and sustained equity outflows is solved by i) US corporate Great Rotation... from 2013 to 2018, US corporate debt issuance = $10.5tn, stock buybacks = $4.2tn; and number of listed US stocks down from 8090 to 4397 past two decades, up to 2018, in sharp contrast to Europe, China & rest of the world. As I have been discussing in this blog, it is certain that a complete meltdown of the financial system is cropping up. Likewise, the economy is set to enter in a depression. Many businesses are starting to close their doors and millions of Americans will lose their jobs. According to a projection by the St. Louis Fed, the unemployment rate may reach 32%. Thus, a colossal series pf defaults is ensuing, halting the debt-based financial system. Therefore, the Fed is going to have to crank up its interventions in the markets to save the whole system. This includes the infamous helicopter money. The $1,200 is just the beginning. The Fed and the Treasury will take this policy to an absurd extent, letting the inflation Titan break free from Tartarus. Americans are going to need a demi-god like Paul Volcker to imprison it once again. Unfortunately, neither Powell nor any keynesian technocrat could play the part. Furthermore, corporations could have used the easy money policy to build up some savings in cash for a rainy day. Because most of them wasted that opportunity, the US government and the Fed will most likely bail them out. Take the airlines for instance, from 2010 to 2019, they spent 96% of their combined free cash flow on buybacks. Now that the proverbial has hit the fan, they are going bankrupt.  Additionally, once the dollar starts falling due to massive currency printing, the government is going to have to increase the checks to citizens for goods, especially the basic ones, since these are getting more expensive (and it will accelerate as time goes by). This makes the Treasury to issue more debt. Seeing that there would be no more buyers of Treasuries (at such low yields), the Fed is going to monetise them all, creating further debasement of the greenback. Consequently, the government increases its check amounts to the citizens and... America gets trapped in a vicious cycle of inflation. Inasmuch as this will impoverish individuals, taking them to third-world wealth, they will not be in financial conditions to gamble in the stock market. More importantly, people are definitely not going to be buying US equities in the near future because their earnings are going to stay at very low levels. Hence, households, mutual funds and other financial institutions will not be acquiring US stock. Moving to ETFs, in spite of the transformation of the financial services industry from a human to a robot-led one rendering the trend depicted on the graph below, I take the view this trend will reverse. Investors are going to be looking for experts that can find the best opportunities in the new paradigm. Obviously, I do not know which particular companies, markets and instruments will perform the best. Yet, it is indisputable the US, in general, is going to become extremely toxic for investors. Therefore, ETFs and other investment funds as well are not going to be the ones pushing US equities into a new bull market. By the way, the same goes to foreign investors.  In conclusion, with corporations being unable to get cheap funding due to the financial system being in shambles, the only way the Fed could try to get the stock market to rally, so as to get the wealth effect desired by the keynesians, is to purchase the shares itself. Therefore, the Fed will start acquiring the means of production. Like I discussed in The Road to Serfdom is reaching its destination, America will turn increasingly more in a marxist socialist nation.

Despite the country becoming the United Socialist States of America, USSA, because of all the Fed-induced inflation the prices of the US shares may achieve levels that go far beyond anybody's wildest fantasies, as I compared it to the Caracas stock market in a previous post. Thus, the silver lining is the next bull market will make this last one look like a newborn calf - in nominal terms, of course.

0 Comments

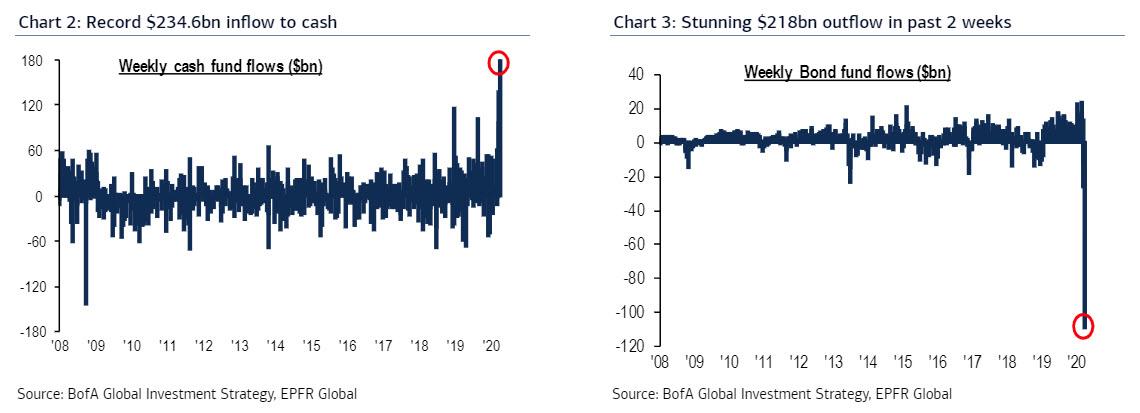

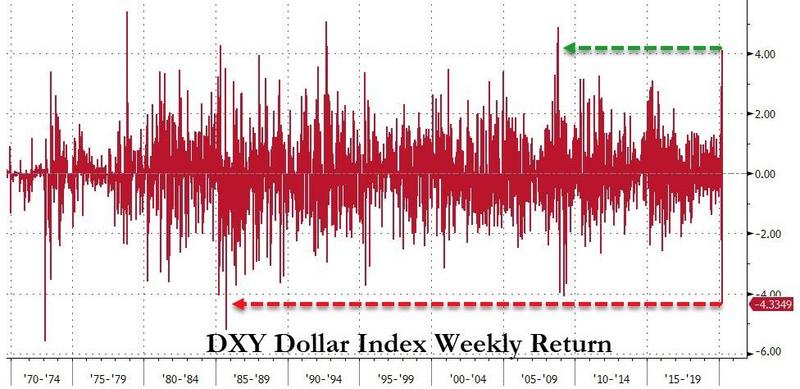

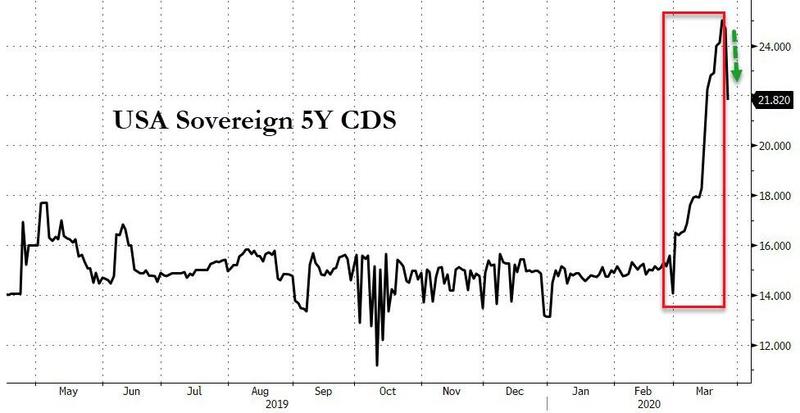

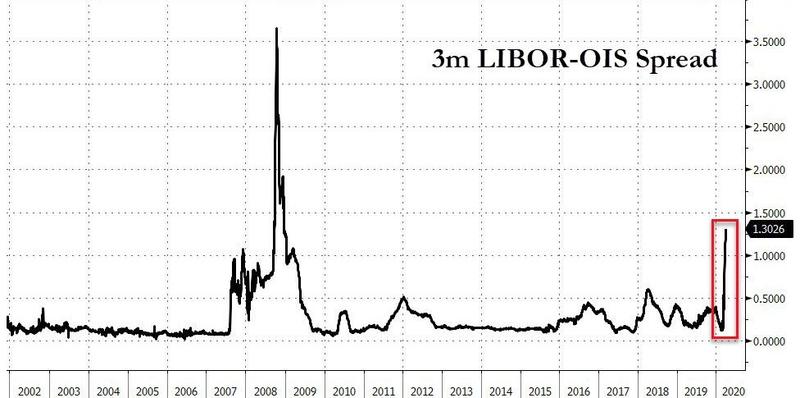

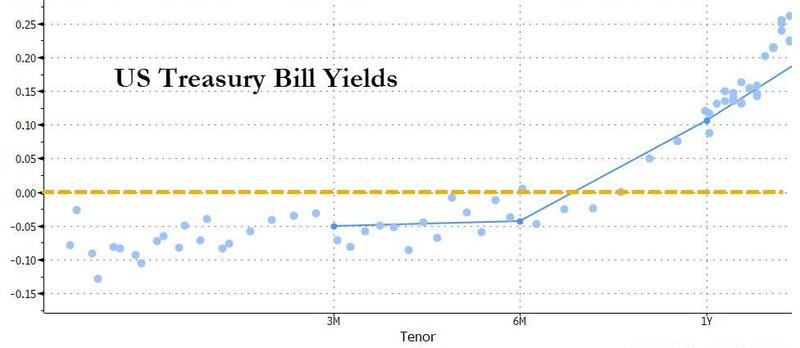

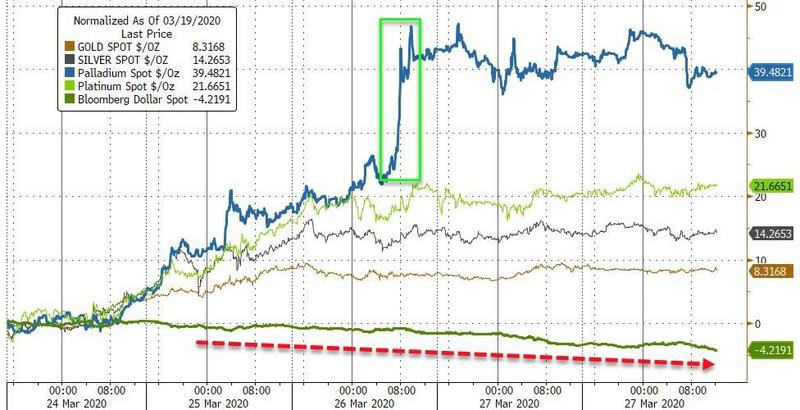

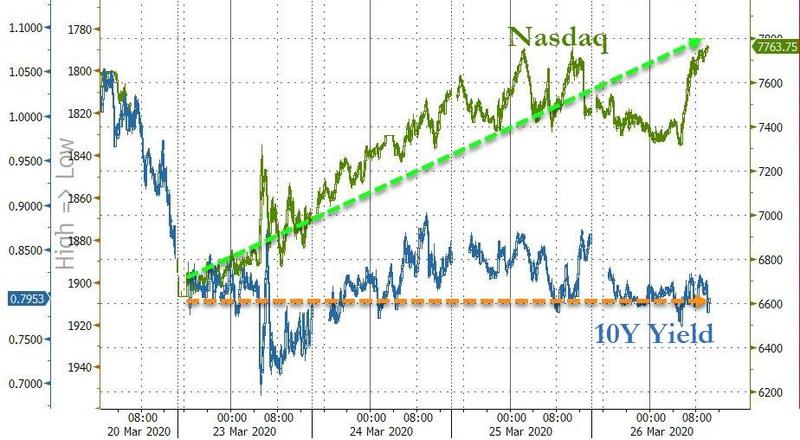

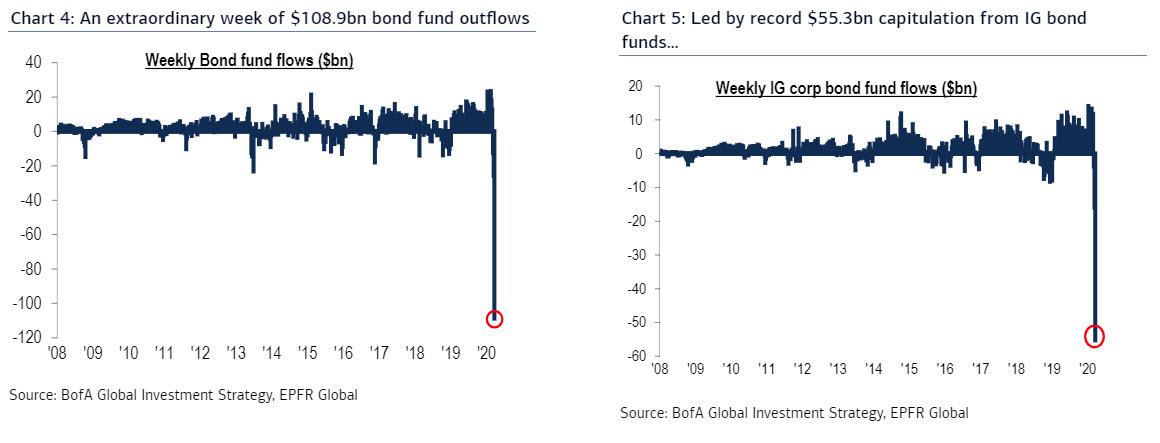

By looking at the stock market this week, one would assume the lockdowns have been lifted and the economy was back on track. Business as usual, right? Do not get fooled by the stock's head fake. Once you delve into the other financial markets, you will find out more problems are arising. To begin with, there are three reasons behind this week's surge in the stock market: the passing of a $2 trillion "stimulus bill" in the Senate; the acceptance of equity securities (shares) as collateral in the Fed's Primary Dealer Credit Facility; and the spurt of the Fed's balance sheet.   Although stocks may have soared this week, with the Dow having its best weekly performance since August 1932 - from Tuesday's open to the close in Thursday, it even achieved bull market status, having jacked up 21.3% -, the greenback had its worst since September 1985, right when the Plaza Accord took place.  In additin, the US dollar is going down while there is still extreme dollar shortages, as the spread between the forward rate agreements (FRA) and the overnight index swaps (OIS) continues to widen.  Moreover, the Treasury notes and bonds (2 to 30 year maturities) were all bid this week. To be more specific, their prices and, consequently, their yields remained approximately the same until Thursday and then yesterday investors rushed to get them, with the long-end (10 and 30 year) outperforming.  Additionally, after rising up to Thursday, the perceived risk of a US government default plummeted yesterday to such an extent that this indicator went down for the week, which explains the move on the Treasuries.  Furthermore, banks are no longer trusting each other. The expanding spread between the LIBOR and the OIS hints at swelling counterparty risk and, thus, ever more troubles in the credit market.  In addition, investors are preferring to park their dollars in T-bills than in the banks, even as these yield negative returns. Obviously, this is related to the graph above. Investors would rather lose a little bit of their money than most. or even all, of it in a Lehman-type event.  Despite the scrambling for liquidity due to dollar shortages, the precious metals have all climbed for the week.  Finally, the massive drop in the dollar this week, whilst the shortage of dollars persists, signals that the faith in the greenback is dwindling. Inversely, the creditworthiness of the US Treasury seems to be holding, even though President Trump approved the $2 trillion stimulus bill and the economic activity is coming to a halt, as the surge to 3.28 million in jobless claims depicts.

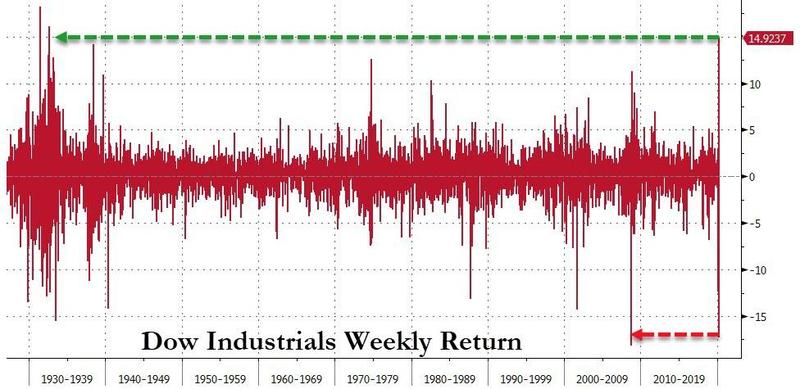

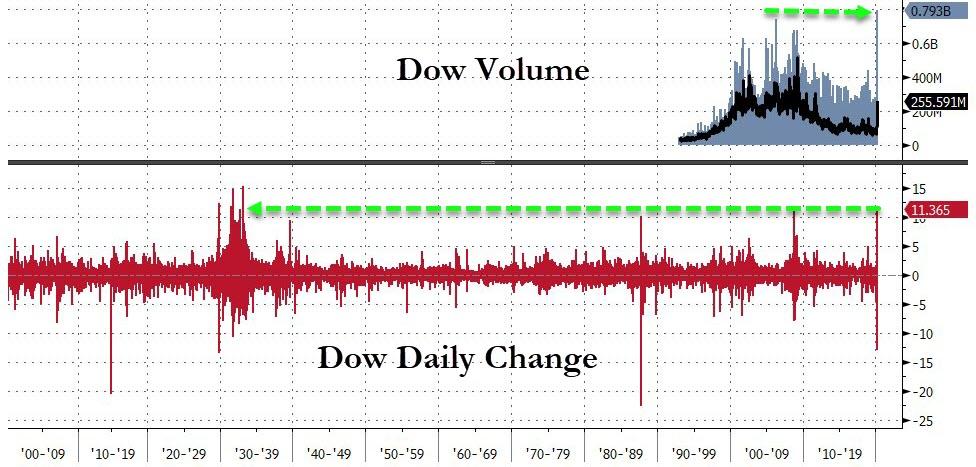

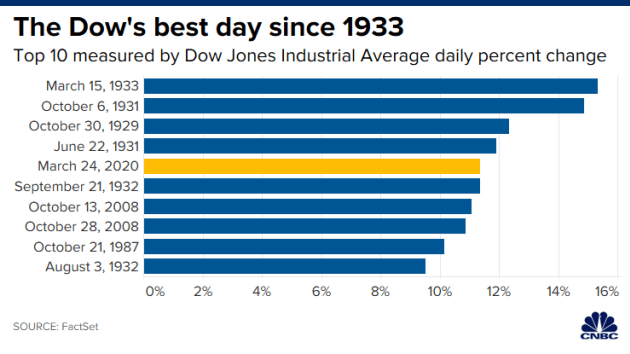

Moreover, the growing counterparty risk among financial intitutions is making them dependent on the Fed and the Treasury to get liquidity and to store their cash. Once investors lose confidence in the ability of the Treasury to pay its debt, a tremendous selloff of USTs will ensue and, hence, the Fed will have to absorb them all, inflating the currency supply. As a result, the dollar will carry on devaluing, completely destroying the trust in it. To conclude, the financial system as we know it revolves around the US dollar and the Treasuries. The greeback is the world's reserve currency. With the US having negative Current Accounts, rendering it a debtor country, the globe is flood with dollars. The rest of the world then uses those and purchases dollar-denominated assets, specially USTs for being the safest ones. To make long story short, all financial markets are built upon the confidence the world as a whole has on the dollar and the Treasuries. Accordingly, the diminishing faith in them both is going to lead to the collapse of the dollar standard. Amidst a bear market, there are always upward corrections referred to as bear market rallies. This Tuesday, March 24, the Dow Jones Industrial Average index had its fourth greatest daily percentage gain ever at 11.36%, being surpassed only by the Great Depression, as the graphs below show. In addition, the S&P 500, at 9.38%, had its ninth biggest climb ever.

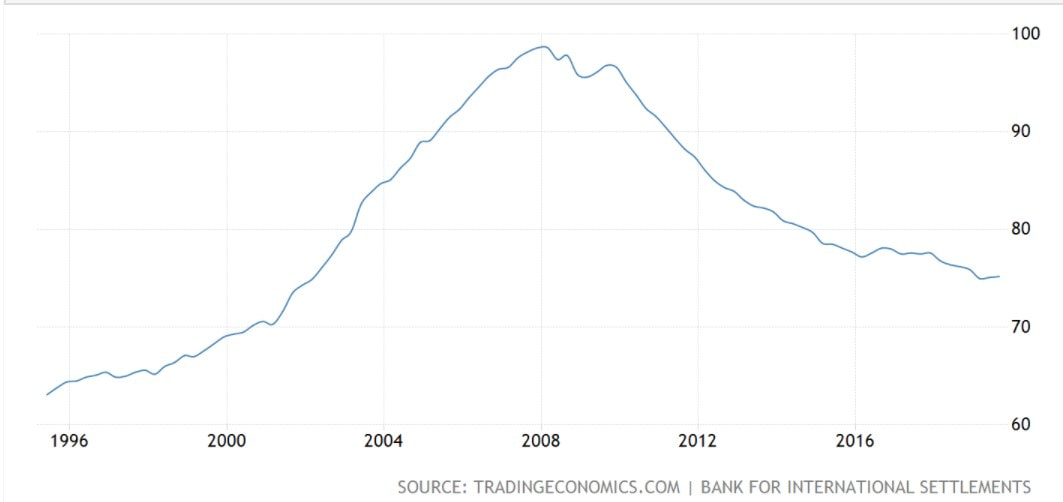

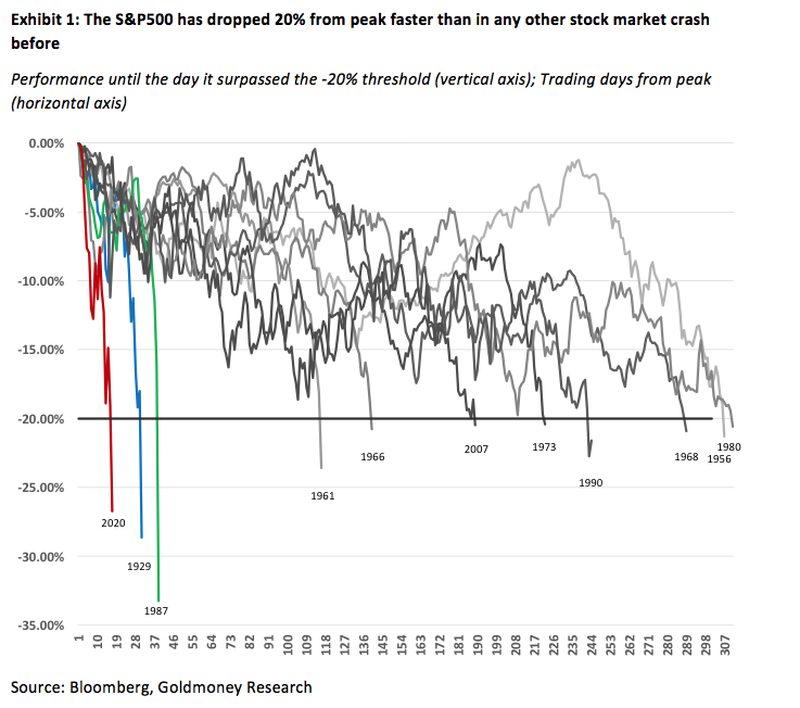

As you can see, the largest upward moves have come about during the most severe financial crisis. Accordingly, the biggest gains occurred on the Great Deppression, which happened to be the greatest financial meltdown and economic downfall in American history. Furthermore, the current crash is taking the ominous contours of the Global Financial Crisis and, looking at the graph below (data up until March 25), the 1930's Depression.  On all occasions, the highest dead cat bounces follow the most intense collapses. Additionally, the S&P 500 was down 32% in the one month period ending on Monday, March 23. Albeit the Dow and the S&P 500 having soared, respectively, 21.3% and 17.55% in the last three days (from March 24 to 26), considering the analogue with the Great Depression, such a rally may not be a sign that a turnaround is on the cards but be a harbinger that we are far from the bottom. Bearing in mind the US and the planet in general are experiencing a widespread lockdown to tackle the spread of the COVID-19, the financial markets at large will bounce along the way, though maybe only after more short-term pain. Additionally, in 1929, the S&P 500 and the Dow fell 45% and 48% in the first two months of the bear market, respectively. In spite of the recent uptick, those indexes are prone to tumble as much as in 1929. Hence, the present crash will not match perfectly, still it should rhyme. Moreover, after the two-month plunge in 1929, there were 50% and 60% retracements respectively in the Dow and the S&P 500 that lasted about four months, throughout early 1930. Despite taking the view the current situation is not comparable to that one due to the impact of the Wu flu, the stock market may experience a relief rally at least as strong and enduring, though a little later in the down cycle. Thus, before the markets are granted that long awaited relief, there is a strong likelihood this initial down phase of the stock market will drop lower than the 1929 one. In addition, after the four-month relief rally into April 1930, during the Great Depression, the market headed down again in a big way before throughing two years later in 1932, with the Dow and the S&P 500 down 89% and 86%, respectively. Although the market crash and global recession being a month old, stocks are expected to be substantially lower from here until the bottom of this epic economic downturn is hit. Furthermore, total US market cap to GDP is only retesting the levels at the peak of the housing bubble, as is shown below. Undoubtly, the stock market is falling from truly absurd valuation levels.  Likewise, the prices of corporate bonds, both IG and HY, have also been surging since the announcement made by the Fed, this Monday, that it was going to purchase IG corporate bonds and ETFs which tracked such bonds.  Inversely, Treasury bonds seem to tell a different story. Inasmuch as bonds have been going sideways while stocks have shot up, this signals there is still a lot of fear among market participants, and the trust in the creditworthiness of the US government as well as the confidence in the dollar persist (for now!).  Finally, the reasons why the Great Depression unfolded are somewhat discussed in Keynesians and the Chicago school, but, in a nutshell, it was due to central planning and government meddling. Additionally, it was a period marked by deflation with a lot of liquidation and debt (money supply) contraction, such as today. However, corporatism was not as prevalent as nowadays (see the previous post) and the mainstream economists and technocrats at the Fed and the government did not see inflation as the cure to all evils. Therefore, unlike today, the government did not bail anybody out nor the Fed increased its balance sheet via QE, TARP, repo operations and the like. To conclude, the stock market is going to much lower magnitudes. Yet, because of the keynesian mindset and Wall Street plus corporatistic cronyism, the Fed will print as much needed to keep financial markets afloat and maintain the status quo. As I have been explaining, this will likely create massive debasement of the dollar, resulting in rising prices in consumer goods and assets like shares. Consequently, the US stock market could in a few years resemble its Venezuelan namesake.  Evidently, like in Venezuela's case, were this to occur in the US, it would not mean the market is a reflection of a booming economy. Instead, it would simply hint at an ever more worthless currency, with the dollar following the steps of the bolívar.

On the year 1944, the Austrian economist Friedrich A. Hayek released its magnum opus, The Road to Serfdom. In this book, he argued that the capitalist model of the US and the UK was morphing into its antagonistic form, socialism. As a reminder, socialism comes in various forms, which are similar in kind, like nazism and communism.

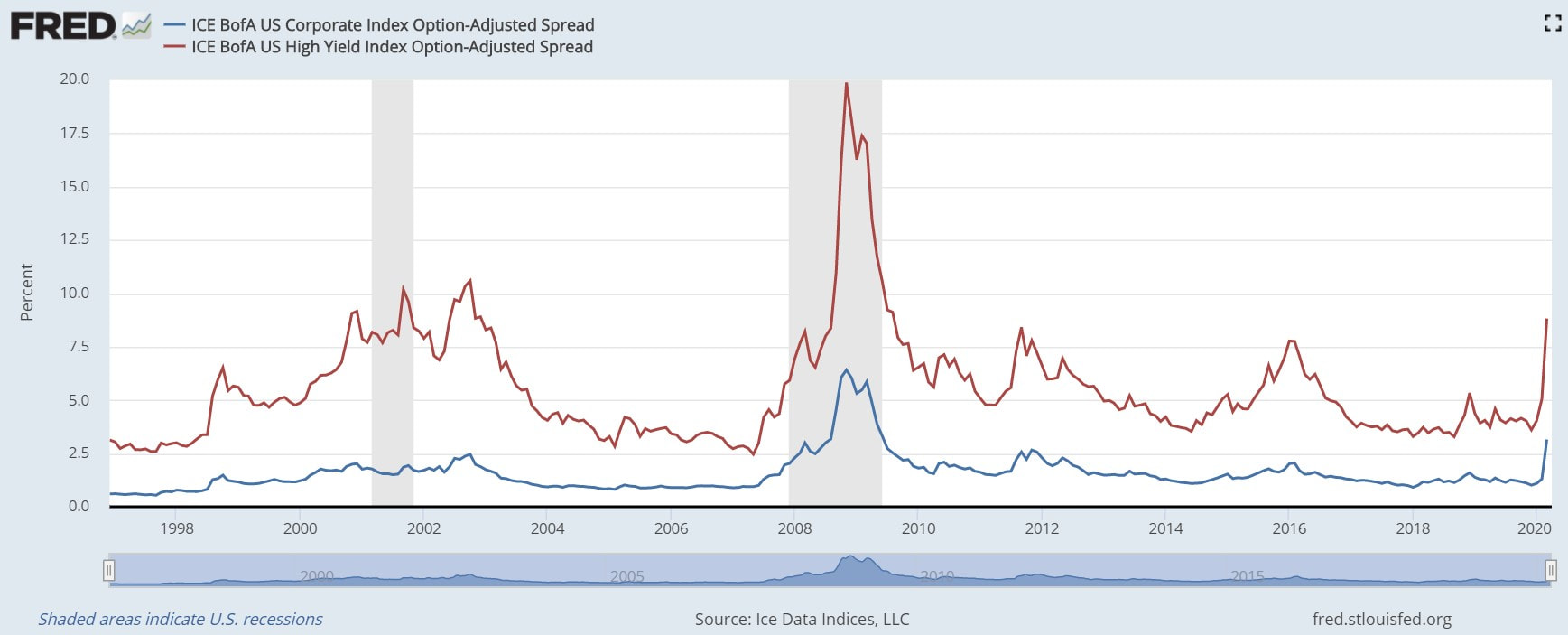

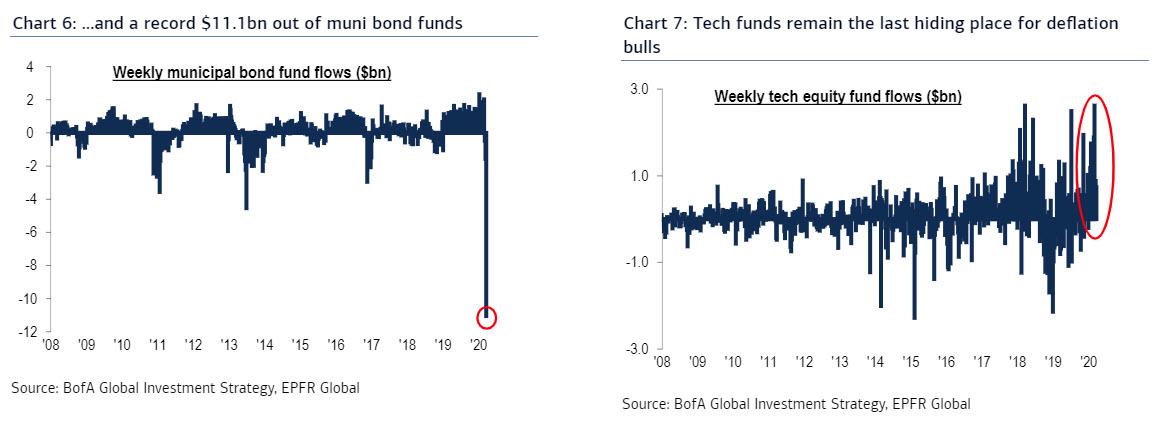

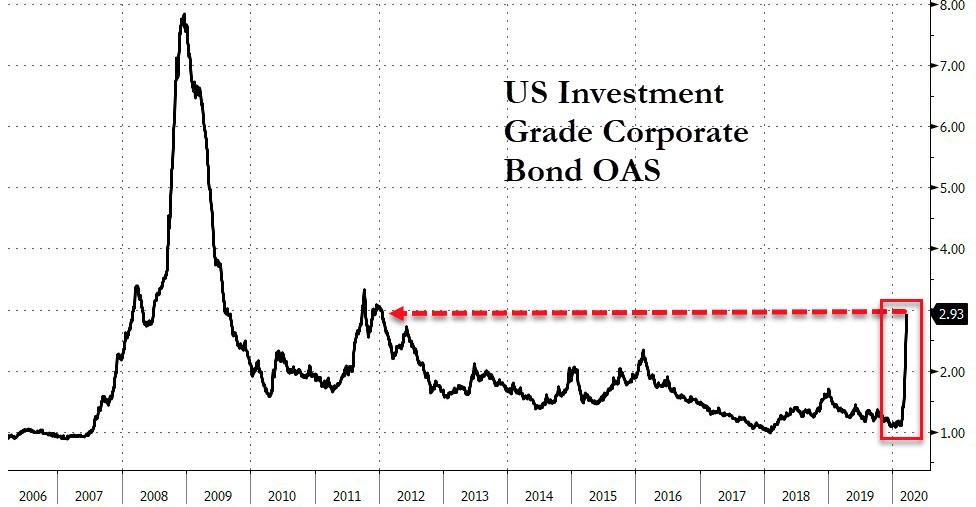

In addition, he demonstrated that every step away from the free market and toward government planning represented a compromise of human freedom and a step toward a form of dictatorship, despite the claims that government control was really only a means of increasing social well-being. Hayek said that government planning would make society less liveable, more brutal and more despotic. Therefore, socialism in all its forms is contrary to freedom. Although this book came out 76 years ago, it remains as relevant or more so than ever. In that era, Hayek noticed that considering America and England were fighting a war against the nazis, it made the apparent acceptance of increasing government intervention very peculiar. Moreover, I may add this shift towards interventionism continued during the Cold War period, which again is interesting when bearing in mind that the American and British ideological position was diametrically opposed to the Soviet Union. Looking at the current state of affairs, one may think that in spite of the nazis and the Soviets losing WWII and the Cold War, respectively, they won the ideologic war, with socialism having conquered the world, including the "capitalist" western bloc. Once you read the section Economic History, you recognise that because of the innovative insights made in the Scottish Enlightment age by David Hume and Adam Smith, the anglo-saxons, i.e. British and Americans, unshackled themselves from the outdated and perverse mercantilistic regime, giving rise to the liberal era. Likewise, liberalism unleashed the greatest period of prosperity the world has ever seen, with the US leading the way. Unfortunately, this experiment came to an end by the turn of the twentienth century, when progressive ideals, such as direct (income) taxation, antitrust laws and central banking, began rising in popularity, kicking off the slow march towards socialism. Additionally, this has been the case for North America, Western Europe and some other regions around the globe. These places have had varying degrees of interventionism and central planning among them and through time as well, having several of them tried out fascism, though this was decades ago. Nevertheless, government planning never disappeared. Since the fall of the Berlin Wall and the breakdown of the USSR, the world became pretty homogeneous, in economic and political terms. As of now, the entire world, minus a few communist countries and tax havens, is ruled under a mix of fascism and democratic socialism, where the government is conducted, not by the rule of law, but by special interest groups. Accordingly, the United States of America is no exception. Firstly, since the Progressive Era, the welfare state, business regulations and central banking have been, in general, growing. These being interdependent, they can only balloon ultimately due to the central bank, the Fed. In addition, most sectors of the economy function in the corporatistic system, which means that those sectors are mostly controlled by businesses setting out with the policy makers the rules and regulations for their industries. Moreover, on other sectors deemed of public interest, like education, public transport and public utilities, it is the workers' unions who prevail when negotiating the laws, rendering these sectors aproximate to syndicalism, which is a movement that advocates establishing a social order based on workers organised in production units. Secondly, during the 2008 GFC, the last remnant of the capitalist regime was thrown away: letting losers lose. In capitalism, when the risk of one's endeavour pays off, he profits. However, when it does not pay off, he has to deal with the losses, even if it means bankruptcy. Throughout the GFC, several businesses and banks, as well as individuals, became insolvent. Yet, the Fed and the government bailed everybody out, due to operating under corporatism. Obviously, the moral hazard that this generated is outrageous. Thus, a system of pernecious incentives became embedded in Wall Street culture and in the management of corporations. Finally, in this financial meltdown, because of the excessive risk taking and extreme leveraging pursued by financial institutions and corporations, as well as the ever expanding deficit spending by the government since the GFC, the Fed is requiring far bigger and faster money printing presses. Likewise, the Fed is widening its scope of measures and facilities. Comparing to the GFC, the Fed is using every facility it did in 2008, though this time it has cranked up every single one of them: the repo operations, the Primary Dealer Credit Facility, the Money Market Mutual Fund Liquidity Facility, the Commercial Paper Funding Facility, Term Asset-Backed Securities Loan Facility (TALF), Central Bank Liquidity Swap Lines and of course, everyone's favourite, Quantitative Easing. Just to have an idea of the size of these operations, in QE3, which was the biggest of all, the commitment was $85 billion a month of mortage-backed securities (MBS) and Treasuries. The commitment for this week's QE is $125 billion each day, $75 billion being of Treasuries and the remainder of MBS, including commercial MBS which was not covered in 2008. Additionally, the Fed announced that QE was open-ended. Consequently, the amounts are certainly going to keep on soaring. Furthermore, the Fed has introduced some new measures. To begin with, the Secondary Market Corporate Credit Facility has been established to purchase investment grade corporate bonds and also ETFs that track the American IG corporate bond market. I knew it was only a matter of time for the Fed to implement a facility of this sort, as I mentioned in the previous post. Moreover, the discount rate on the primary credit - to the primary dealers - narrowed its spread relative to the general level of overnight interest rates "to help encourage more active use of the [discount] window by depository institutions to meet unexpected funding needs". More noteworthy, the Fed is now accepting equity as collateral via the Primary Dealer Credit Facility: "Collateral eligible for pledge under the PDCF includes all collateral eligible for pledge in open market operations (OMO); plus investment grade corporate debt securities, international agency securities, commercial paper, municipal securities, mortgage-backed securities, and asset-backed securities; plus equity securities." The pledged collateral will be valued by Bank of New York Mellon, according to a schedule designed to be similar to the margin schedule for lending by the discount window, to the extent possible. This means that dealers can now buy stocks at what are still massively overinflated valuations thanks to trillions in central bank liquidity, knowing they can then turn around and pledge them to the Fed at a collateral value that is determined by an easily biddable back-office minion. Despite equity securities had been used during the GFC, that was only made in backstage negotiations. Additionally, there will be a program worth $300 billion to support the flow of credit to employers, consumers and businesses. At last, there is going to be a lending program to Main Street businesses in order to help "support lending to eligible small and medium-sized businesses, complementing efforts by the SBA." To conclude, lending with equity as collateral may be the final nail of capitalism's coffin. Although this program is supposed to be a temporary measure until the crisis passes and normality is restored, those stocks could stay in the Fed's balance sheet for years, simply because the monetary and financial system may very well collapse, as I have been arguing. Since the economic and financial crisies will only get worse, the primary dealers will use this procedure increasingly more often or, as things are going, the Fed might even commit to straight out purchase equity securities. Therefore, the stocks in the Fed's balance sheet may multiply very soon, quickly expanding its participation in corporations. Accordingly, in such a terrifyingly possible scenario, the Fed could end up being the majority shareholder of several corporations by the time the reset of the monetary and financial system is set up. Thus, we may see the US become a full-blown marxist socialist country, with the government owning the means of production. In light of the rising acceptance of socialism in America, as the Democratic Party has demonstrated with the favourite candidates being those coming out with the most preposterous proposals and entitlements, I believe a lot of Americans would welcome and not many would vehemently oppose such a regime. Sadly, the same could be said about virtually every other developed nation, from Canada to New Zealand. All of them embarked on a race through the Road of Serfdom and all are only a few steps away from the destination. Now, we can only guess which ones can step on the brakes in time and which ones have their brakes slashed. On The dollar standard epic finale, I explained that the current downturn will give rise to increasing debt-to-GDP ratio, which ultimately will lead to a sovereign debt crisis. The US government's response will likely be to monetise the debt, resulting in a currency crisis. In today's post, I am expanding in more detail on the dynamics that may cause the dollar to collapse, taking every other fiat currency with it. To wit, I am taking a closer look at the money and the credit markets debacle that is happening before our very eyes. To begin with, let me shed some light on these markets. The money market involves the purchase and sale of large volumes of very short-term debt instruments, such as overnight reserves or commercial paper. Some of the types of instruments used are certificates of deposit, eurodollars, commercial paper and repurchase agreements (repos). Furthermore, the credit market refers to the market through which companies and governments issue debt, such as investment-grade and junk bonds, commercial paper, notes and securitized obligations, including collateralized debt obligations (CDOs), mortgage-backed securities, and credit default swaps (CDS). The repo market is an overnight lending money market, where financial institutions sell US Treasury securities, a.k.a. Treasuries or UST, and other securities deemed low risk to other institutions, with an agreement to purchase them at an agreed price and date. Moreover, the commercial paper market is for buying and selling unsecured loans for corporations in need of a short-term cash infusion. Only highly creditworthy companies participate, making it a low risk instrument. Moving on to the matters on the table. In September, inefficiencies in the repo market became apparent. The overnight repo rate, which is supposed to stay in line with the Fed funds rate, shoot up to around 7%, when the Fed funds rate was at the 2-2.25% interval. This episode became know as the Repo-calypse and it demanded the Fed to intervene in the repo market, for the first time since the 2008 Global Financial Crisis (GFC). According to the Fed, although this was expected to be temporary, it is still going and becoming worse by the day. This is being provoked by a lack of collateral and increased counterparty risk. The financial intitutions have been searching for liquidity, yet they are short of "good quality" UST. Thus, for one party to accept to take inferior collateral, the returns must be greater, hence, the higher repo rate. The ongoing repo operations by the Fed, besides indicating the lack of superior collateral, could be pointing out the increasing intability of the financial system and the rising insolvency risk of the banks, hedge funds and other intitutions. Likewise, these two aspects are contributing to the liquidation of everything, from equities and bonds to gold and silver, to cover expenses and margin calls. Over the last 4/5 weeks, problems have emerged in the credit market. Firstly, the spreads between corporate bonds, investment grade and high yield (look at the two graphs below), and Treasuries have been growing wider, leading to a spate of insolvencies in the corporate sector and investment funds, as well as losses on collateralised loan obligations (CLO) held by the banks on a systemically threatening scale. Secondly, the commercial paper market began to freeze . Investors started to demand a bigger return to lend to corporations, causing the rates to spike, which means it became more expensive for corporations to borrow through this instrument. Accordingly, corporations are using other means that are draining liquidity from the money market. On the one hand, corporations that have cash at their banks will draw it down, forcing the banks to go into the money market, either through the international interbank market or the repo market, to make up the balance, sell government bonds, or foreclose on borrowers. On the other hand, corporations that do not have cash will test their working capital facilities, likely to force their banks to cover increased lending in wholesale money markets. Where banks experience drawdowns on both sides of their balance sheets, outstanding bank credit contracts, sending the sort of signal that terrifies central bankers. The situation will be increasingly reflected by central banks having to backstop both liquidity and bank reserves through repos and new rounds of quantitative easing. In an interesting paper, Zoltan Pozsar of Credit Suisse describes the process that leads to what he terms deficit agents in supply chains (businesses experiencing payment failures) turning their banks into deficit agents as well. Pozsar demonstrates that a reluctant Fed will have to backstop not just soaring domestic dollar deficits but global ones as well, and he assumes for the purpose of clarity that foreign central banks will manage the payment crises in their own currencies.

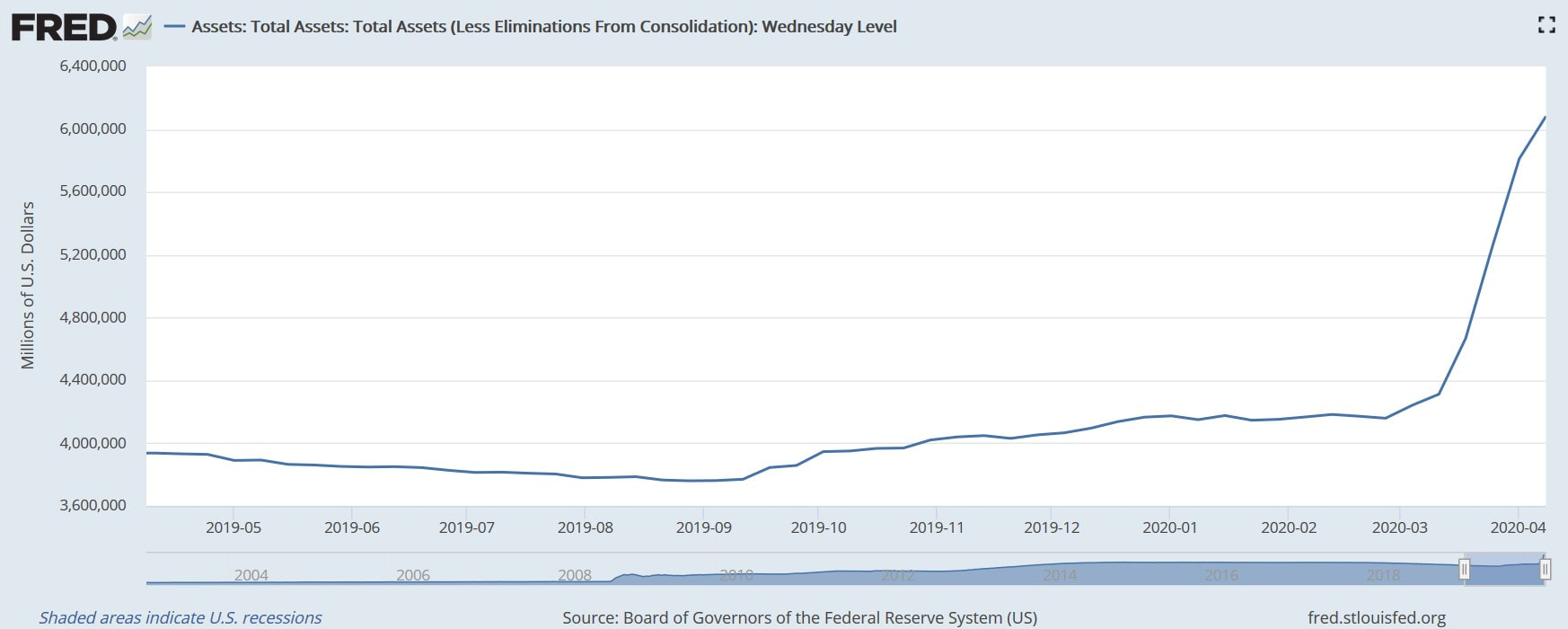

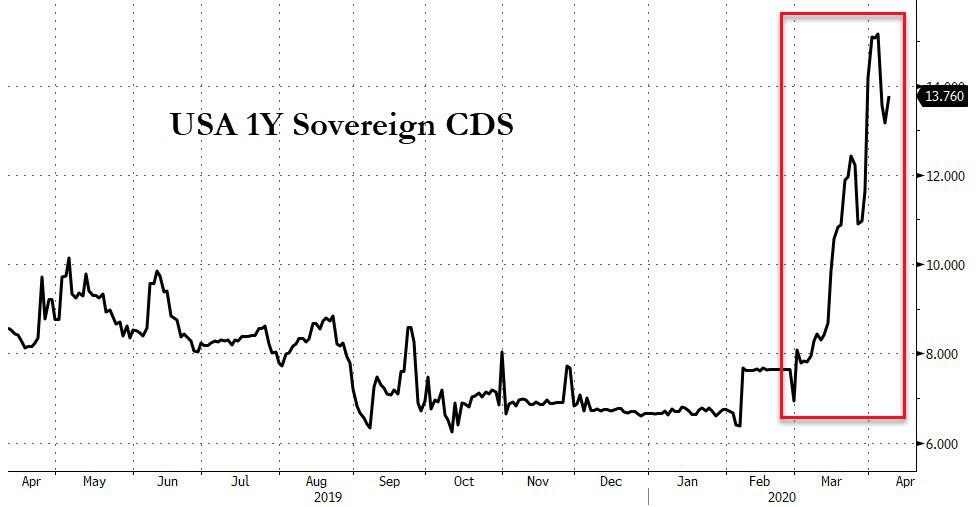

In addition, US hedge funds have ventured in enormous quantities of fx swaps to strip out interest rate differentials between euros and yen on one side, and the dollar on the other. Now that the Fed is closing down the rate differential by cutting its funds rate these arbitrages need to be unwound, leading to substantial liquidation of USTs and dollars to repay obligations in euros and yen. This will put significant downward pressure on the dollar. Furthermore, a reduction in outstanding derivatives will be the consequence of banks freeing up liquidity in desperation for their own balance sheets. The cost of hedging risk will increase significantly and in many instances become unavailable. Hedge funds and the like will be forced to restrict their activities, raising the possibility of widespread losses and potential failures in financial markets. Moreover, foreign governments will also be liquidating Treasuries to obtain dollars to satisfy their liquidity demands. As of now, Treasuries are still regarded as safe havens. However, when investors realise US insolvency risk is rising (look at the graph below), the safe haven status will fall. In any case, foreigners are getting the dollars they need via other means. One of those is the dollar liquidity swap lines between the Fed and foreign central banks. The Fed has had agreements in place since 2013 with 5 other central banks: ECB, Bank of England, Bank of Japan, Swiss National Bank and Bank of Canada. Yesterday, the Fed announced temporary dollar liquidity swap lines with 9 more central banks in Australia, Brazil, Denmark, Mexico, New Zeland, Norway, Singapore, South Korea and Sweden. It will not be long for them and others to lose faith in the Treasury creditworthiness. Additionally, foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. Nations with dollar-centric supply chains in their domains, such as China, South Korea or Taiwan, will probably have to unwind their long-dollar fx swap positions and sell Treasuries in order to release the necessary liquidity.  On top of that, US hedge funds and foreigners getting rid of dollars to get euros and yens, and to pay their dollar obligations, respectively, results in the reduction of the money supply, i.e. broad money. Specifically, it is the bank credit that contracts. Therefore, the Fed will have no alternative but to expand the base money to compensate the waning bank credit. The Fed will act this way because they have bought Irving Fisher's, Milton Friedman's and Ben Bernanke's description of how contracting bank credit led to the Great Depression. Up until a month ago or so, the 2020 budget deficit was estimated, by the CBO, to be around the 2019 figure of over a trillion dollars. This estimate seems ridiculously optimistic now. The Director of the National Economic Council, Larry Kudlow, is expecting to spend 2 trillion dollars in a stimulis package. With a stagnant or even declining (most likely!) economic activity, the fiscal revenue will not follow the growth in government expenditures. This means the budget deficit could reach $3 trillion and, consequently, the national debt may hit $26.5 trillion. For the sake of argument, the GDP for 2020 will remain the same as last year, $21.2 trillion, which renders the debt-to-GDP ratio at 125%. Thus, the Treasuries will not attract investors at the present low yields - the insolvency risk demands higher yields-, leading to Treasuries selloffs. In order to allow all that government spending, the Fed will have to absorb not only the newly issued debt but also the Treasuries sold by foreigners. By doing so, the Fed will end up ballooning its balance sheet by many trillions. As of now, the assets on the balance sheet amount to $4.3 trillion, aproximately, and by the end of the year it could be double that. Otherwise, if the Fed chooses to protect the value of the dollar, the debt is not monetised, wreaking havoc on the government's finances. In addition, it is not only the US banks which are in trouble. A glance at their share prices confirms that major European banks have long been at severe risk of failure, a fact which has been concealed by the ECB’s provision of liquidity. If nothing else, a new escalation of non-performing loans brought about by the coronavirus now threatens to collapse Italian, French, German, Spanish and other Euro Area members’ commercial banks, despite the ECB’s efforts. Hence, bailouts of Euro Area banks are on the cards. As a result, this will likely lead to widespread liquidation of euro commitments for speculation and arbitrage. Loans in the trillions have been taken out in euros as the counterpart in fx swaps to the dollar. As these positions are squared the euro will rise and the dollar will fall, transmitting a Euro Area banking crisis into liquidation of UST-bills and short-term US Government coupon debt by US hedge funds. A heightened risk of counterparty failure in fx swaps could spread to other derivative markets, requiring bailouts of non-banks, including major hedge funds. Furthermore, base money will be increased substantially to offset a contraction in bank credit and to give banks extra liquidity to compensate for becoming deficit agents as supply chains dislocate and retail sales of non-essentials goods and services collapse. On March 17, the Fed announced a Primary Dealer Credit Facility, with backing from Treasury. This facility will offer overnight and term funding with maturities up to 90 days. It became available for at least six months from March 20, at an interest rate equal to the discount rate, which was lowered to 0.25% on Sunday, as part of the central bank’s emergency action. This kind of measures are set to escalate. As a result, a coordinated G-20 global bank rescue scheme involving open-ended monetary expansion by central banks is likely to be instigated, in a widespread act of currency inflation. In respect to the fiscal stimuli, helicopter money is already being used in Hong Kong, where each citizen is receiving HK$10,000. Likewise, the US followed Hong Kong's lead and has commited to offering two tranches of $1,200 to every adult. There are also other expedients, such as deferral of tax payments and business rates to help provide liquidity, which will shift to governments some of the deficits building up in businesses. Mortgage payment holidays are offered in some countries. Helicopter money is already being provided to investors through share support operations, such as the Bank of Japan’s purchases of ETFs, which is likely to be expanded, and the ECB's €750 billion Pandemic Emergency Purchase Programme (PEPP) which commits to buy private and public sectors' securities. A few days from now, I am sure the Fed and US government is going to announce something along these lines, like buying corporate bonds, as has already been suggested by Ben Bernanke and Janet Yellen. Regarding the US, all of this stimulus is going to be financed through debt, which in turn will be monetised, diluting the dollar. A declining dollar will increase portfolio liquidation pressures on foreigners, leading to indiscriminate offerings of Treasuries, agency debt and equities (look at the graphs below). The Fed will have to take on not only the financing of an increasing budget deficit, but also absorb foreign sales of dollar-denominated securities (not just USTs), if it is to retain control of prices.   Accordingly, this is set to devastate the repo market. As you know, this market has become increasingly illiquid in part for lack of "good quality" collateral, USTs. As the public debt jacks up, the outstanding Treasuries carry on swelling because there are new ones being issued. In spite of the accruing "good quality" collateral, i.e. Treasuries, financial intitutions will continue to find difficulties in getting funding due to USTs losing quality. Therefore, the Fed will have to keep on backstopping this market through the repo operations, debasing the dollar even further. We have already seen daily repos by the Fed increasing from about $40 billions in recent weeks to between $130 to $200 billions currently.

In addition, so as to help keep credit flowing to corporations, the Fed came up with an emergency lending program on March 17. With the approval of the Treasury, the Commercial Paper Funding Facility was established. The Treasury will provide, through the Fed, $10 billion to a special-purpose vehicle that will purchase commercial paper from eligible companies, and purchases will last for one year, unless the Fed extends the program. As the title of this post claims, the Fed has painted itself into a corner. By providing an insanely cheap amount of liquidity, via zero interest rate and QE since the GFC of 2008, the financial system developed to a ridiculous size when compared to the economy as a whole. Because of the COVID-19 shock, the daisy chain of financial engineering is starting to come apart. Thus, the Fed and the US government have to support the financial system, intervening in each and every market. In doing so, the Fed has to ultimately devalue the dollar, putting the trust and faith in this debt-based monetary system, the dollar standard, at risk of collapse. At this stage it will become increasingly obvious to investors and domestic bank deposit holders as well that the dollar’s purchasing power is being destroyed by the Fed’s escalating asset support commitments. In effect, the Fed will be the only significant buyer of financial assets, paid for through quantitative easing on a far greater scale than what followed the GFC. Ergo, the dollar crash will bring the Treasuries and the entire financial system down with it. With the dollar as the world’s reserve currency and nearly all other fiat currencies having taken their cue from it since the Nixon shock in 1971, they also seem doomed to failure with the greenback. To conclude, this is the beginning of the end for the pervasive keynesian influence on the economic affairs of every realm, the monetary, the financial and the political ones, as well as at the individual and institutional levels. The preposterous fiat currency experiment is about to crumble. Obviously, the keynesians are not going to simply throw the towel. Being very sure and proud of themselves, they will stay the course. Accordingly, the central banks will either ramp up QE or implement negative rates, as discussed in the previous post. Only afterwards, will an economic system be erected on the pillars of a sound monetary system, based on gold. In this day and age, we are bombarded by articles about the various ways mankind is destroying this planet, through increasing pollution, emissions of carbon dioxide and urbanisation. In addition, a crescent view is growing that the widespread developments in artificial intelligence (AI) that have been happening, and are set to continue, will bring about mass unemployment, with the gap between the haves and have-nots spreading tremendously, causing the alienation of a majority of the population from the fruits of the technological progress. Moreover, some even believe the entire human species is in jeopardy of being totally wiped out.

The aim of this post is not to discredit these assumptions. Despite these themes being interesting premisses for Hollywood movies (like The Day After Tomorrow or Kingsman, on climate change, and 2001: Space Odissey or The Terminator franchise, on AI), in my opinion, they are unfounded. In any case, for those who believe that nonsense, they should be rejoicing over the fact that the developed nations in the world are on the verge of implementing negative interest rates. In spite of the Euro Area (deposit facility), Japan, Denmark and Switzerland being currently imposing the infamous Negative Interest Rate Policy (NIRP), plus Sweden having experimented with it for awhile, they will soon be joined by the other western countries as these are already at zero or very close to it. Taking a look at the interest rate, savings and time preference section, you know the interest rates are a function of savings and these, in turn, are derived from the time preference. Interest rates are positive because people have positive time preferences. This stems from their preference to satisfy their needs in the present rather than in the future, which leads people to demand a higher return on savings than the opportunity cost of savings (cost of foregoing present consumption). In lay terms, people only save if they assess that by doing so they can improve their lives and well being in the future. Hence, a positive time prefence is a requisite for civilisations to develop. Furthermore, a negative interest rate would only be materialised in a free market - without central bank manipulations -, if individuals had a negative time preference. This means they would not mind, and in fact want, the cost of savings to be higher than the return on savings. In other words, only present consumption matters, so much so that if they put money set aside the amount has to decline over time, so that they have less resources in the future, halting or even depleting the capital structure and, consequently, reverting prosperity. It goes without saying that people have positive time preferences. Despite all of those Chicken Littles who believe we are destroying ourselves, they still do not want to burn their hard-earned pay. Thus, this is only possible through central banking devilry. Additionally, were the interest rates on deposits to be negative, everybody would instead hold cash outside of the banking system. Accordingly, in order to force people to keep their currency in the banks, central banks are going to ban or hinder the use of paper money, i.e. cash. The move towards a cashless society has been gaining momentum, with institutions having been developing infrastructures for digital currencies. Besides cryptocurrencies, there are other initiatives in the pipeline. China has been developing its own digital yuan and in the future, as Jim Rickards proclaims, Russia and the rest of the "Axis of Gold" could have their joint digital currency backed by gold, the PutinCoin or XiCoin as he calls it. In the private sector there has been other projects referred to as stablecoins. The most prevalent ones are Facebook's Libra, JP Morgan's JPM Coin and Fnality International' Utility Settlement Coin (USC). Stablecoins are digital currencies pegged to a central bank currency, like the dollar, or a basket of currencies. Fnality International is a consortium comprised of some of the world's biggest banks. Its objective is to deliver a distributed ledger technology (DLT) based global payment system, one that can facilitate peer-to-peer markets. The crux of USC is that it has been sold to people as a model for a decentralised digital future. We are told that JPM Coin and other stablecoins will offer an alternative method for transacting through distributed ledger technology, one that moves away from the centralised ground of today – ground that is monopolised by central banks. Another objective of Fnality International is to connect decentralised market infrastructures to a corresponding central bank, which presumably would result in transactions being settled in central bank currency, through DLT ready payment systems. The USC and the other stablecoins will also have to conform to international anti-money laundering and know-your-customer regulations. Hardly an example of a decentralised utopia. More importantly, the IMF has been studying the most practical way to make NIRP possible. In an IMF working paper entitled Monetary Policy with Negative Interest Rates: Decoupling Cash from Electronic Money, the framework and rationale of (almost) banning cash is layed out. Its plan is to have a dual local currency system: cash and digital. The rationale is for central banks to be able to break on through the zero lower bound (ZLB). With such a system in place, a central bank would be able to use conventional monetary policy tools without the constraints of the ZLB to stabilize the economy. In a world of low neutral real interest rates - e.g. inflation rate of -5% would be matched with a -5% interest rate -, it would help reduce the length of business cycle downturns and, hence, the duration of low interest rate periods. Interestingly, cash would be maintained, for five reasons: cash is still widely used and banning it could lead to disruptions in retail; poorer and older people are less likely to use electronic payment methods; cash is preferred by those who put privacy above everything else; in case of malfunctions on the electronic means of payment, cash is the only option; and if cash is abolished the decision would be hard to revert. In terms of the design, the digital currency would pay the policy rate of interest, and cash would have an exchange rate, the conversion rate, against the digital. This conversion rate is key to the proposal. When setting a negative interest rate on the digital, the central bank would let the conversion rate of cash in terms of digital depreciate at the same rate as the negative interest rate on the digital. The value of cash would thereby fall in terms of the digital currency. In following this scheme, the banks would be able to pass on negative interest rates to their depositors, without causing a flight to cash. The funny (peculiar) aspect of this is the notion that the keynesians at the IMF believe that NIRP, in such a system, would effectivelly counter recessions, making the economy to expand again. However, as I explained above, only positive interest rates foment societal progress by reflecting individuals' desire to better their well being. In short, people save because they want something better in the future. Inversely, negative rates will incentivise individuals to spend their income now, precluding them from saving to improve their welfare. To conclude, although NIRP is aimed at being a tool to achieve the keynesians' wet dream of leveling the business cycle and having permanently booming economies, the outcome is the complete opposite. Individuals would stop thinking of ways to improve their future situation because they would be focus only on the present situation, freezing prosperity. After awhile, everyone would become aware of the failure of this policy, demanding for a reset of the monetary system, which I exposed in the previous post. For the time being, the move towards digital will keep on advancing, with stablecoins probably taking the lead and central banks following suit or adopting them. On some other day I will discuss the dynamics that the NIRP is going to produce in the economy, but as you can imagine the implications of this policy are dreadful. Before I delve into today's topic, I want to clear some doubts about the impending collapse.

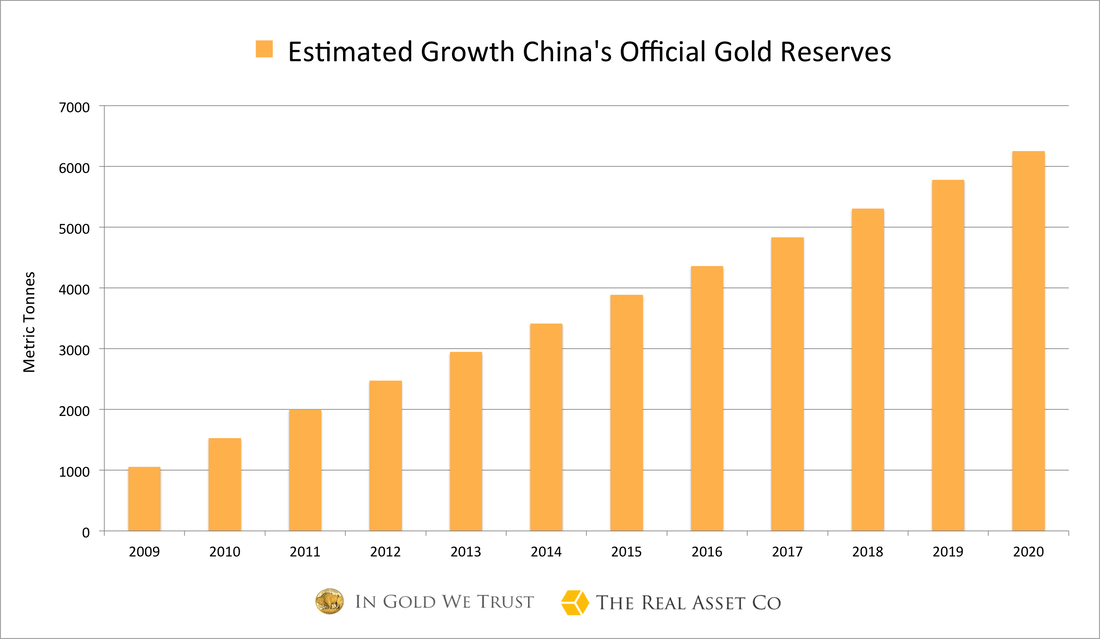

Anyways, let's get back to the agenda. As you know, the people and institutions in power are going to do anything they can to keep the fiat monetary system afloat. The end game for the dollar is its massive depreciation through inflation or even hyperinflation induced by the Fed. By reading this section of this website, you become aware today's currencies are not money for they are not a store of value. This is an essential requisite to be considered money. Since the dollar only loses a bit of its value every year (2% according to the CPI, though its been more than that in reality), individuals have the perception that it is stable, and the keynesians want you to believe it. During the next few years, due to tremendous debt monetisation and helicopter money, besides the "novel" Modern Monetary Theory rising in popularity, the dollar is going to devalue rapidly, breaking people from the keynesian stirred up daze, realising at last that the dollar is not a store of value. Seeing that the greenback is the world reserve currency, it is not only the american people that are going to lose confidence in it. Most of the dollars in existence actually circulate outside of the US (eurodollar and petrodollar systems). Therefore, foreign investors and governments/central banks are also going to dump the dollar and get rid of its supremacy. In addition, the dollar is not going to be the sole rejected currency. All around the world, the reliability on this fiat regime is going to evaporate, making people demand a proven, trustworthy form of money: gold. As emerging and developing countries continue to grow faster than the developed ones, specially the US, Europe and Japan, their weight in the world economy will become more prevalent. Hence, thet are going to get increasingly more influent on monetary, financial and political affairs at the world stage, with the balance of powers becoming progressively more even. Accordingly, they are going to make sure a resemblance of the Bretton Woods agreement is not on the table. On the Bretton Woods system, virtually all currencies in the world were pegged to dollar and the dollar was pegged to gold. This meant the dollar became the reserve currency of the world because it was viewed as good as gold. The US managed to struck this deal owing to the fact that after WWII, America rose as the greatest economy in the world, by far surpassing the wrecked post-war Europe. Thus, if the leaders of the world get together to discuss the next monetary system, the west will not have the upperhand and, consequently, it is going to recognise the most powerful emerging economies (BRICS) as equals. As a result, they are going to have to come up with a means of transaction that is created and managed by an independent entity. Luckily, such entity and means of transaction are already set up. I am refering to the Special Drawing Right (SDR) established by the International Monetary Fund (IMF). Currently, the SDR is calculated by an weighted-average of five currencies: the US dollar, the euro, the British pound, the Japanese yen and the Chinese renminbi. In the next system, the SDR will have to change the composition of the basket in order to reflect the new balance of powers. Despite having the structure established already, contries may reject this multilateral system, prefering instead to engage in bilateral settlements. Alternatively, the west may become resentful of the shift in powers and can refuse to submit to the desires of the chinese, the indian and so on. Therefore, it is likely the globe will be divided in two blocs: the west (the US and Europe) and the east (China, India, Russia, South Korea, etc). Each bloc could have its own intitutions to regulate trade and monetary and financial matters, with gold acting as the means of transaction. Moreover, China, Russia and other emerging countries have been moving in this direction. According to James Rickards, who has written several books about the imminent meltdown of the dollar and present monetary system, China, Russia, Iran and Turkey are forming what he calls the "Axis of Gold". All of them have been acquiring gold, as well as reducing their holdings of US Treasuries. Furthermore, others countries may join the Axis, such as India, considering that it has been active in a gold shopping spree.

Obviously, these scenarios are not going to unfold until at least five years from now. In the meantime, the keynesian technocrats are going to insist in following their impossible and fanciful doctrine of having permanently booming economies. To follow this fantasy, the Fed is going negative. Just a moment ago the Fed announced it was going to cut the Fed Funds rate by 100 basis points, from 1% to 0%. Hence, the US will join the Euro Area and Japan in the moronic NIRP experience. Tomorrow, I am going to expand more on the possibility of negative interest rates and their outcomes.

As I said in yesterday's post, on point number 5 (Banks), if banks were to be left bankrupt, this whole debt-based system would collapse, with all the distortions and malinvestments being quickly corrected. This would be extremely deflationary, benefiting, therefore, the savers and punishing the debtors, who would see their phony wealth being destroyed. In a nutshell, this would spark off agony among the reckless debtors and speculators and completely change the structure of the economy and society, with epoch-making shifts in industries and institutions. Although it does not seem like it right now, this would be the correct and least painful path the governments and central banks could follow. Unfortunely, they will most likely have a go at saving this system, embarking on bail-outs and producing inflation to reinflate this bubble economy. Unsurprisingly, at least to some, their endeavours will fail, resulting in more havoc and suffering to the whole society.

Let me expand on why that is the case. The governments, central banks and supranational intitutions, in addition to universities' economic departments and financial media, are all riddled with keynesians. The keynesian ideology is one of control and manipulation, as well as being the reason we are stuck with this debt-based system. Had you read the content of this website, you would have already know this. Hence, when the bubble pops at last and the economy starts to heal itself, all the keynesians are able to see is the contracting GDP and rising unemployment figures. This pseudoscience indoctrinats them into believing the economy has a general equilibrium and would it ever deviate from such then governments and central banks must intervene. Thus, the public debt piles up, because of fiscal stimuli, and the currency devalues, on account for expansionary monetary policy. Furthermore, from this framework stems corporativism, a.k.a. crony capitalism. Whenever the system is on the brink of collapse, like in 2008 and at this moment, the politicians, technocrats and central bankers come to the rescue of their cronies by paying for their reckless, immoral and even criminal endeavours. To recap, when economic activity diminishes, fiscal revenue declines and government expenditures shoot up. Consequently, the debt increases, leading to a higher debt-to-GDP ratio, provoking a higher interest rate. This in turn adds to the debt, stiring up a greater debt-to-GDP ratio. When a country cannot cover its debt servicing expenses through its fiscal revenue, a sovereign debt crisis ensues. Then it faces two options: default or monetise the debt which undoubtedly gives rise to a currency crisis. Taking a look at the most traded currencies in the world, the US dollar, the euro, the British pound, the Japanese yen, the Swiss franc and the Canadian dollar may very well be embroiled in their own personalised crises. Since the US, the UK, Japan, Switzerland and Canada are countries with their own central bank, when they reach that unsustainable level of debt, they will opt for monetising the debt. Inversely, the Euro Area is going to face a political crisis owing to the fact that the financially foolish members, i.e. southern Europe, will want the ECB to buy their debt, but the responsible northern Europe will put a stop their efforts. The inevitable desintegration of the EU and the end of the euro experience is to be discussed some other day. Today, it is the turn to write about the destiny of a country which I am certain it is going to be through such crises: the United States of America. The world reserve currency, the US dollar, is without question going to crash. Firstly, the US is going to increase its debt to such an extent it will become unsustainable. Arguably, it may have already passed that threshold, seeing that the debt-to-GDP has surged every year of this expansion, except in 2015 which incidently almost killed the bull. Regardless, the government can default and negotiate with the lenders/bondholders for i) a restructuring or a haircut, or ii) refuse to pay. Either one will bring the dollar standard era to an end. The foreign holdings of US Treasuries, both from the private sector and from governments/central banks, account for about 30% of the national debt (as of December 2019, 6.69 trillion dollars of a total 22.72 trillion dollars). If it chooses the former, the other countries, US rivals and partners alike, will make sure to get rid of the dollar hegemony and its "exorbitant privilege", as Valéry Giscard d'Estaing, who was at the time minister of the Economy and Finance for France, put it. If it picks the latter, the relationships that the US has with its trading partners, and international community as a whole, will severely deteriorate, hindering at least the in and outflows of goods, capital and people to and from the US, and at most bringing about unrestrained war. Alternatively, the Fed will monetise the debt, which it has already been doing since 2009 through various rounds of Quantitative Easing (QE), having started its latest round, QE5, this past week. By doing this, the Fed will be flooding the economy with dollars, though the demand for the greenbacks is going to start falling soon, because all this inflation erodes its value. Yet, more importantly, the investors will finally realise that the expanding Fed balance sheet, i.e. QE, is not a temporarily emergency measure that can be unwinded. Therefore, the world is going to learn any day that this monetary and financial system can only be sustained with ever growing amounts of debt and, ergo, dollars, which means its purchasing power keeps on wearing off. On account of Washington, DC being swamped with keynesians and Big Business lobbyists, they will get the government and the Fed to spend currency like drunken sailors, even if it renders the greenbacks as valuable as Monopoly money. I am betting on this one. In conclusion, whatever it happens next, the dollar will cease to be the reserve currency of the world. Now you may be wondering what will the next reserve currency be? Will it be gold? IMF's Special Drawing Rights? Chinese renminbi? That is what I will be trying to discover on the next post. The great peril facing humanity right now is not climate change, nor the trade war and the rise of nationalism, but the novel coronavirus, COVID-19. Despite having a fatality rate of 2.3%, it varies tremendously by age and whether one has some pre-existing illness or not. This data comes from a paper by the Chinese CCDC released on February 17.

In addition, this virus has an R0 (average number of new infections by an infected person) of 1.4 to 4.08. It seems that the experts have "settled" at around 2.2. Comparing to the common influenza (death rate of 0.1% and R0 of 1.28), this virus presents a much bigger threat. Accordingly, for the youthful and healthy there is not much to worry about. However, in order to save the lives of those more immunosupressed, everyone must make a sacrifice and temporarily change their behaviour, and cancel or postpone some activities. As I am writing this, the total infection cases is 134,684 and the fatalities amount to 4,973 in 127 countries. Obviously, the overwhelming majority of deaths have been among the people who have surpassed the average life expectancy or had critical pre-existing conditions, or both. Although all these deaths are a tragedy, there is a particular victim that only a few have noticed, and even fewer are aware of the repercussions such a tragedy will bring about. You may have guessed by reading the title: the bull market. This should have come to no surprise since this market had gone far past the average lifetime of an economic expansion, as well as having some critical pre-existing conditions - chronic liquidity disease and debt addiction. Like I said above, this virus is forcing people to delay or cancel their plans and companies to halt production due to disruptions on the supply chain and workers staying at home. Hence, economic activity, which was already waning since last year, is deteriorating rather rapidly. Consequently, several implications arise for the various economic agents.

Tomorrow I will develop on the options that the governments and central banks have to deal with the financial debacle. Moreover, how the option likely to be followed will impact the consumers, businesses and investors, both domestic and foreign, and finally what is the end game for the current monetary and financial system.

|

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed