|

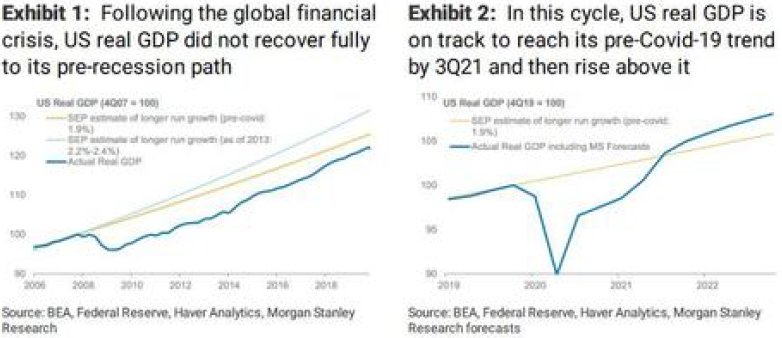

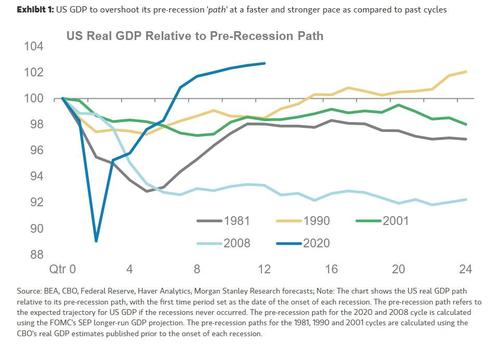

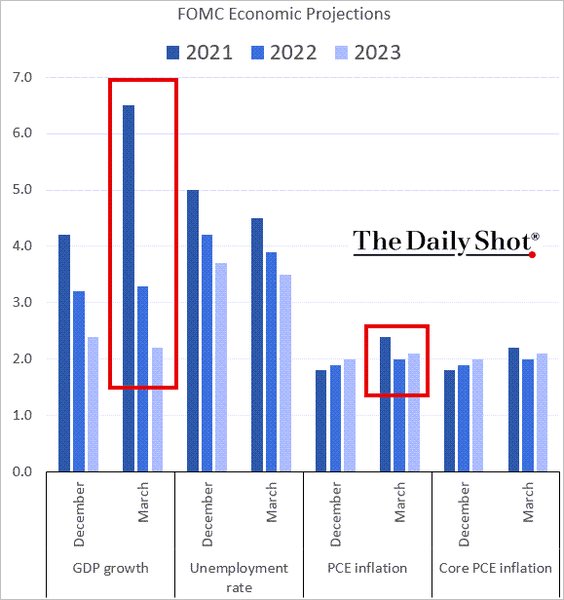

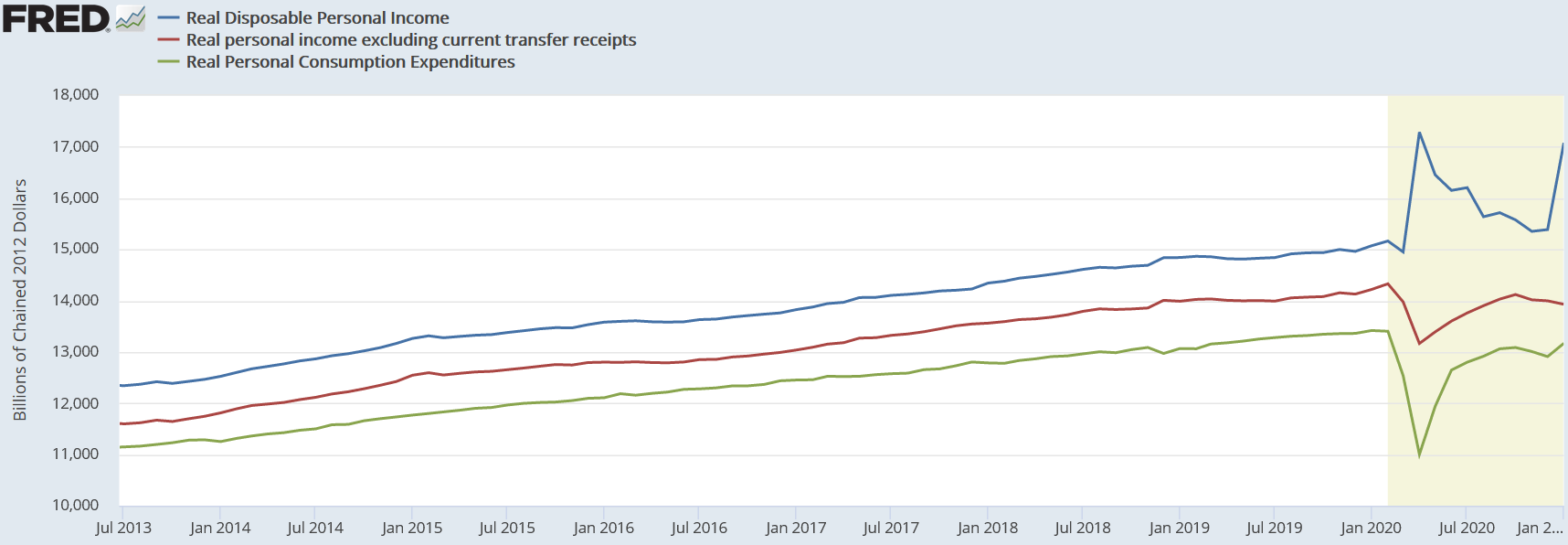

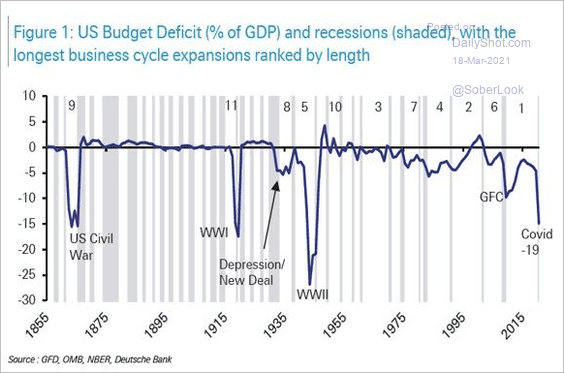

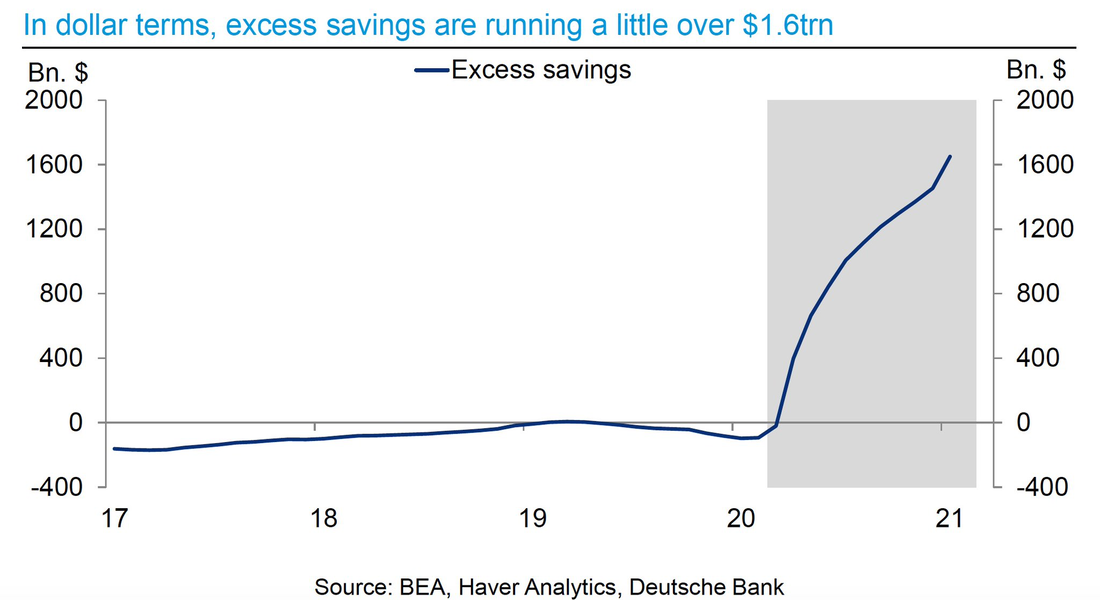

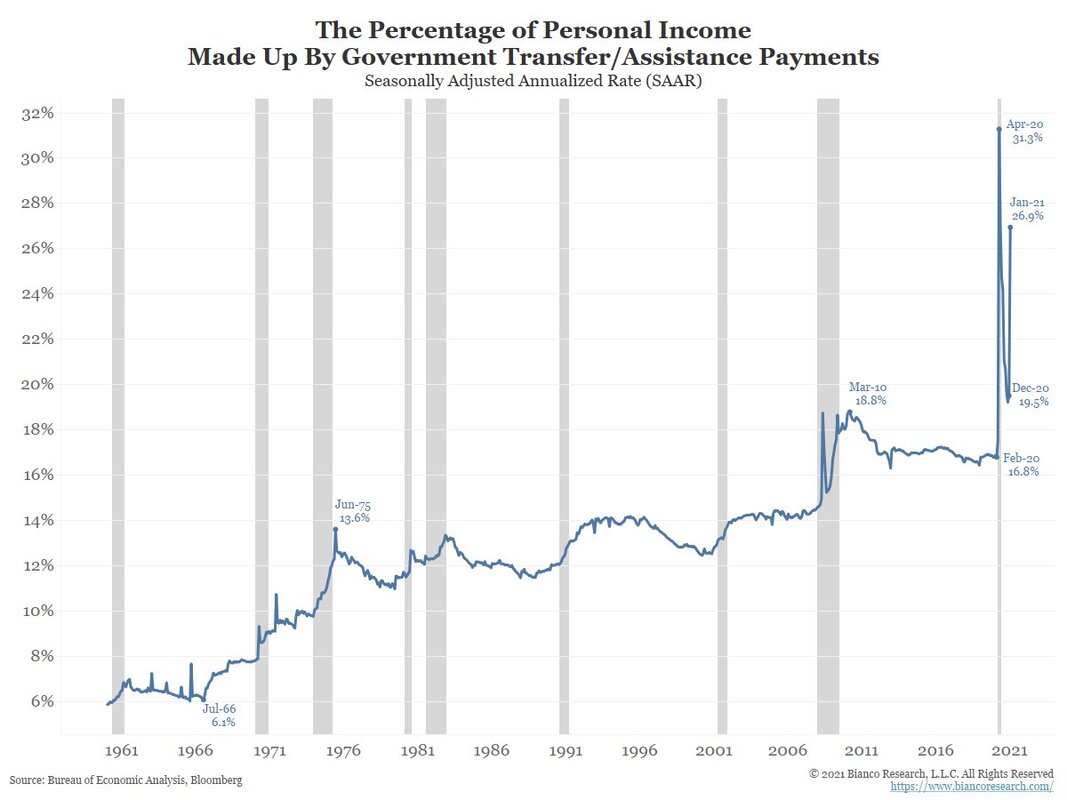

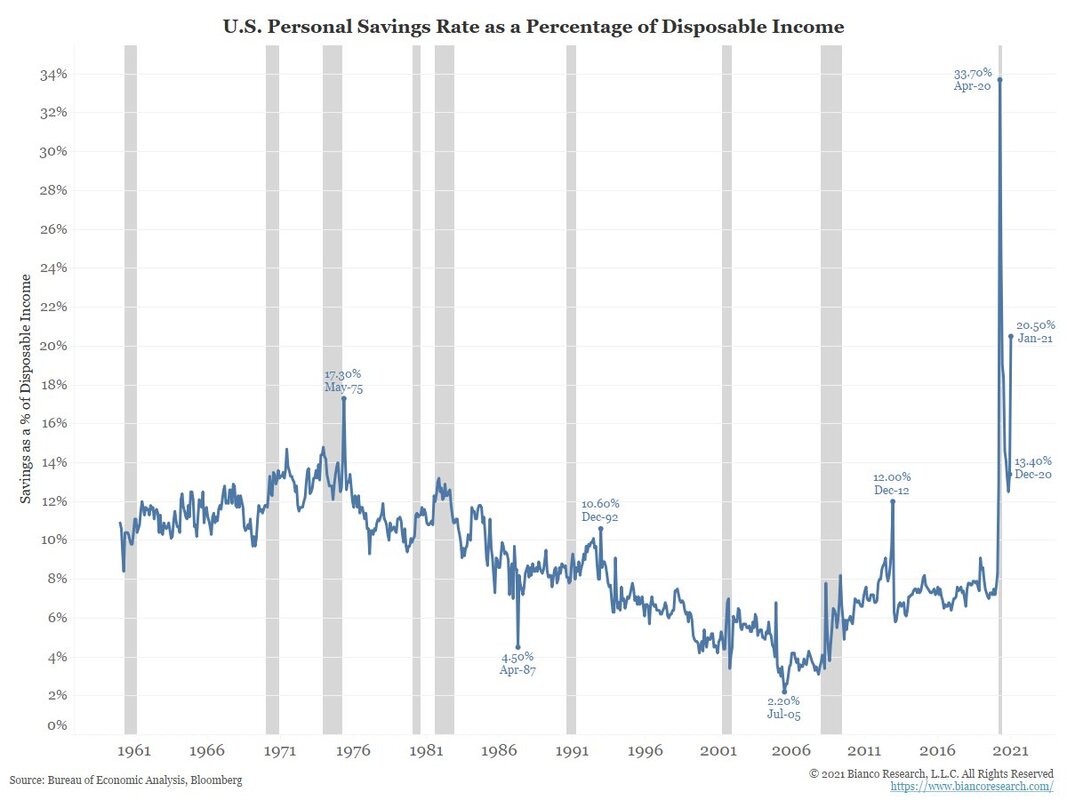

After uselessly engendering the greatest economic contraction and social calamity in the post-war era so as to curb the spread of the kung-flu, policy-makers have then started to desperately try to push the economy to the level of activity it was supposed to be at had none of this ever happened. In classic spoiler fashion, let me just go ahead and declare they have not and are not going to succeed. Nevertheless, those in the media and the economists who feed them this nonsense are always very keen on crying inflation every time the government steps up its deficit spending. For almost thirteen years now we all have been listening to this spiel and for all this period we have been patiently awainting for that technocratic-planned recovery which never arrived, prompting anguish and resentment for the average Joe and Jane. Be that as it may, bearing in mind the colossal amount of money the Democrats are injecting in the economy, $1.9 trn now plus another $3 trn or so later on to be invested in "green" projects, in infrastructure and so forth, the recovery has to be inescapable. If not to the pre-GFC1 (2007-2008) trend, then certainly to the pre-GFC2 (2020) one. Among those who believe the recovery is on the cards are the economists at Goldman Sachs and Morgan Stanley. In a letter written last month, the analysts in the latter bank claimed the fiscal and monetary "stimuli" are creating a "high-pressure economy" that will put the ten million people who have become unemployed back in their jobs (or some new one). For 2021, these economist projected, in February, US GDP to grow by 6.5% in 2021 (7.6% 4Q/4Q) and 5% in 2022 (2.9% 4Q/4Q). These estimates imply that US GDP will rise meaningfully above its pre-Covid-19 path after this year's Q3 and will allegedly be higher in 2022 than what we would have expected in the absence of the pandemic. That is a particularly remarkable outcome, especially when you consider that in the post-GFC period the US economy never really returned to its pre-recession path, as I affirmed above. In view of the regime shift in both monetary and fiscal policy, they assert this accelerating recovery is bound to take place. The shift they are refering to are i) the move to average inflation targeting, on the monetary front, by the Fed, and ii) on the fiscal front, the Biden administration have jacked up their efforts to address the "issue" of inequality by enacting large-scale government transfers to low- and middle-income households.   Furthermore, on their updated estimates, the US economy will reach pre-corona output levels by the current quarter. From the third quarter of this year onwards, US GDP is foreshadowed to overshoot the path it was projected to follow before the recession. The last time GDP rose above its pre-recession path was in the 1990's (above graph). Back then, it took fifteen quarters compared to seven quarters this time around, with these analysts expecting the US economy to reach 103% of its pre-recession path in twelve quarters (i.e., by December 2022) versus twenty seven quarters in the 1990's. In this March update, they are forecasting growth of 7.3% in 2021 (higher than the February forecast) and 4.7% in 2022 (lower than last month's), almost 2 percentage points above consensus this year and 1 percentage point next year. To justify this, they defend this historic fiscal policy, which is the most sizeable during a peacetime (next graph on the left), is doing much more than fill the output hole. Transfers to households have already exceeded the income lost in the recession, causing savings to mushroom (next chart on the right). As reopening gathers pace, the labour market is poised for a sharp rebound, entailing that consumption growth in 2021 will be supported by wage growth and transfers, with little reliance on excess savings. In fact, they think the excess saving stock (savings accumulated by households over and above the pre-kung-flu run rate) will still rise to a peak of $2.3 trn (roughly 10% of GDP) by the end of this summer. Even for 2022, they are building in only a modest drawdown of the excess saving to $2.14 trn (8.7% of GDP) by year-end. Evidently, a faster-than-expected drawdown will pose upside risk to growth. All the same, they see inflation, following a near-term surge in the spring, remaining elevated above 2% this year and the next.

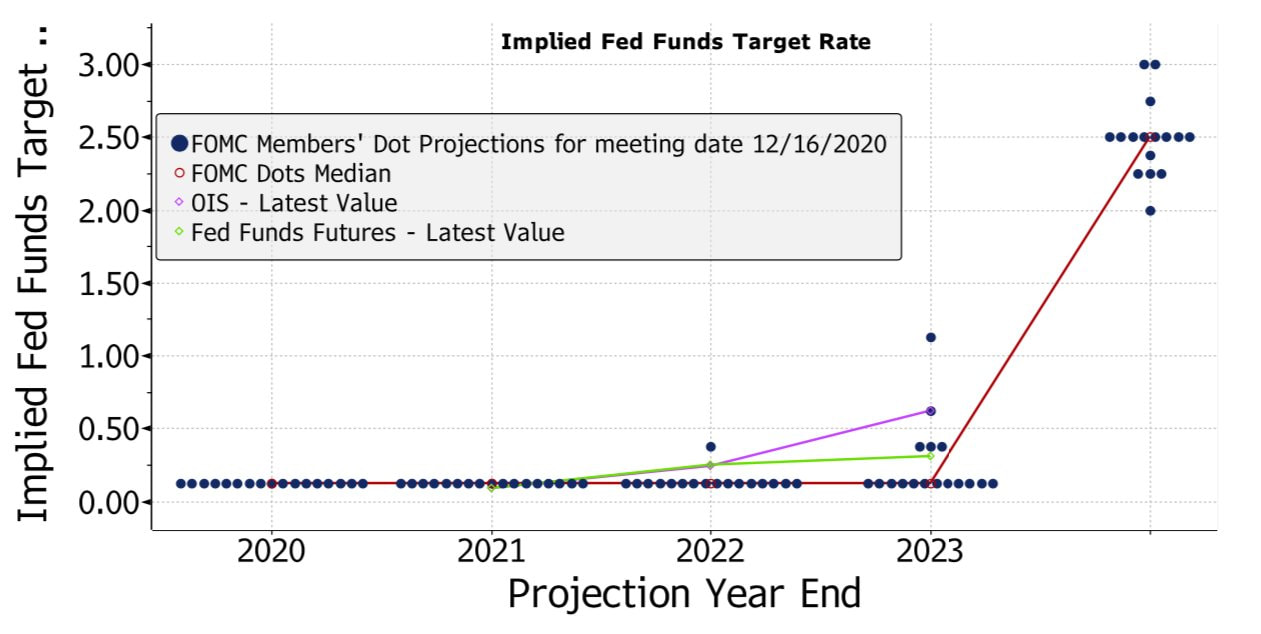

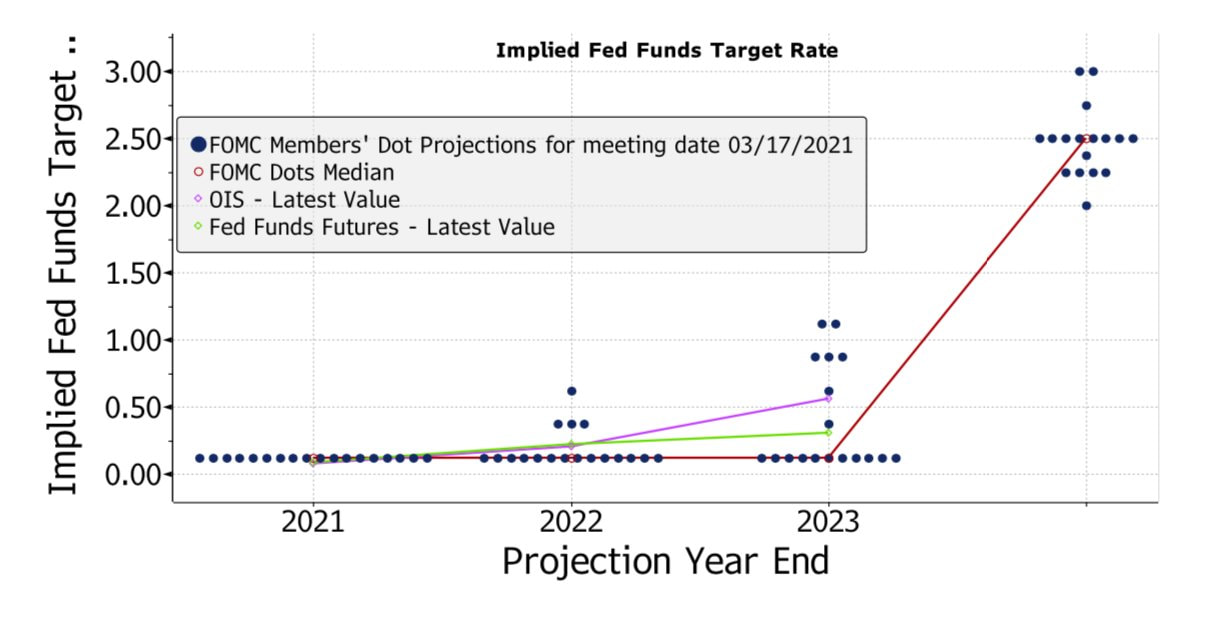

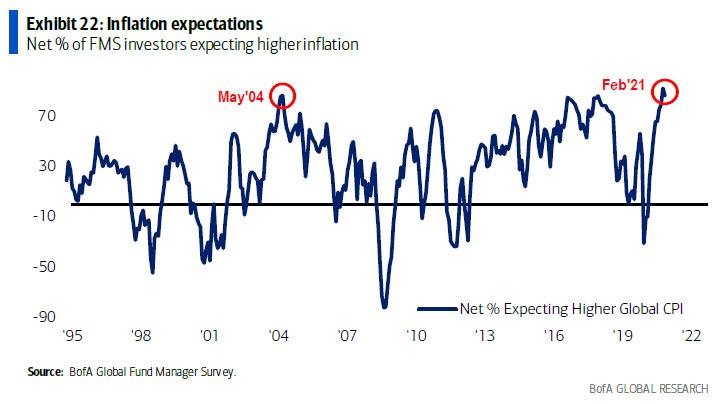

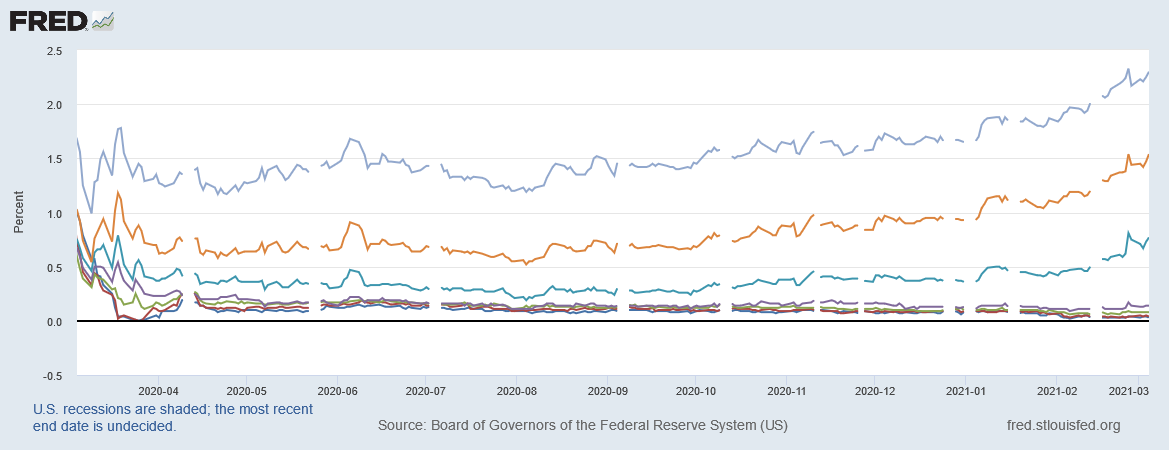

Having already stated the change in its objectives, the Fed is not concerned with the uptick in the "inflation" rate, maintaining this rise in prices to be transitory. Despite the economists' assessment of future inflation and economic performance, the markets are apparently contradicting them, siding with the Fed (top graphs) - or more correctly, the Fed siding with the markets. Even though since 2021 broke out the sentiment has improved substantially among financial and economic analysts, as well as in financial newsrooms and economics departments, the reality is that markets are indicating the immediate and near futures are still terrible. Therefore, federal funds futures and the overnight indexed swap (OIS) on the fed funds rate are telling us that financial conditions have remained tight and, more importantly, are expected to be so in the next couple of years.

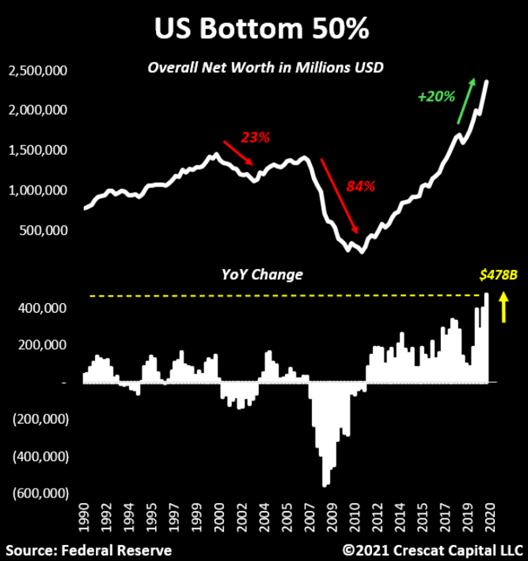

Perhaps the Fed is assuming prices to climb more than 2% transiently because they know the economy is still suffering from a deflationary/disinflationary landscape - definitely not; they are simply following the market signals. Like I said on the March 1 post, "it is not stimmy checks sent by Uncle Sam, or any other government for that matter, that are going to enkindle the much-anticipated inflationary conflagration. Because individuals sense, and rightly so, the government aid is temporary and inconstant, they are not spending money in proportion to what they are gaining in income". Although the surge is staggering, the "stimmies" are not going to cure the economic malaise and turn it into a proper boom. If you have been following my work, you are aware that I alluded to the cause of such malaise many times, albeit never really expounded on it. Once more, on account of that being a topic that requires thorough analysis, I will save it for another day. Regardless, I think you already know the culprit is the gargantuan weight governments worldwide have on the (global) economy. In addition, that whole notion that individuals are swimming in a sea of savings that would put Scrooge Mcduck to shame is absolutely false. A couple of months ago, Real Investment Advice's Lance Roberts perfectly exposed the truth behind those misleading statistics. In short, the accumulation of savings has occurred in the upper-class, while the lower-classes have been living paycheck to paycheck. As a result, were this skew in savings to keep on going this way, seeing that an increase in the savings of the wealthy individuals is not going to change their propensity to consume, the economy is definitely not going to boom. To be fair, the government handouts have been directed at the lower- and middle-classes, having the theoretical potential to boost consumer spending and, consequently, economic growth. Unsurprisingly, "theoretical" is the key word there. In the real world, these poor bastards have every reason to carry on being thrifty. Owing to not having a stable source of income and finding extremely difficult to get a nice job - due to government interventionism creating a lethargic economy and over-regulated labour market -, being dependent on the whims of politicians to get by, and, to add insult to injury, because credit moratoriums and eviction bans cannot last forever, the fact that their savings ballooned and their net worth curiously shot up, which of course never happened during a recession, is not going to change their economic outlook. Revisiting our friends from Morgan Stanley, they believe the impact of the pandemic is likely to fade, and they foresee a surge in demand as the economy reopens this spring. For being forced to accumulate excess saving as restrictions on mobility have limited their opportunities to go out and spend, with warmer temperatures coming and vaccinations set to cover a large part of the vulnerable population, these analysts are confident that the relaxation of restrictions, which has begun in some states, will pick up speed as spring approaches, resulting in the economy ultimately firing on all cylinders. No dice!

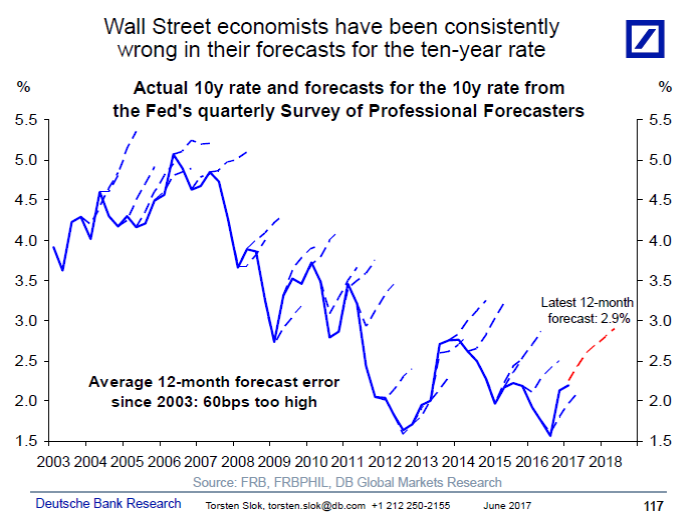

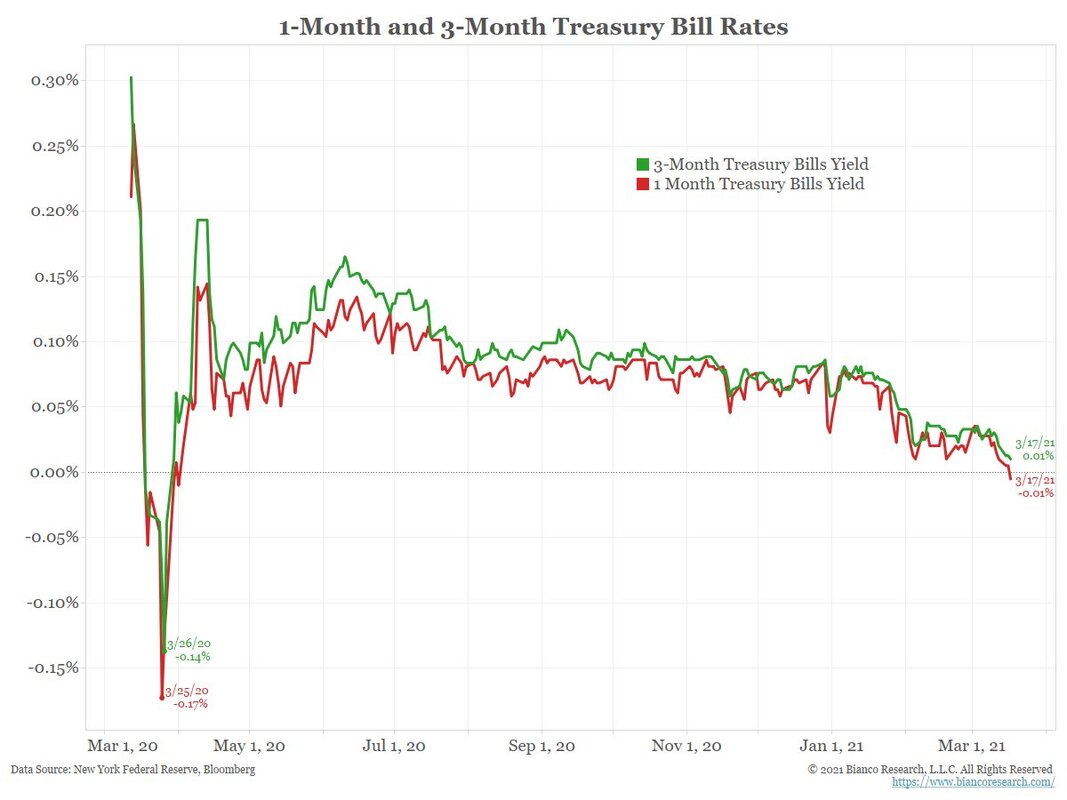

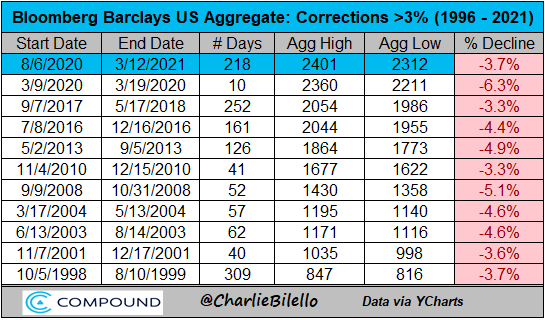

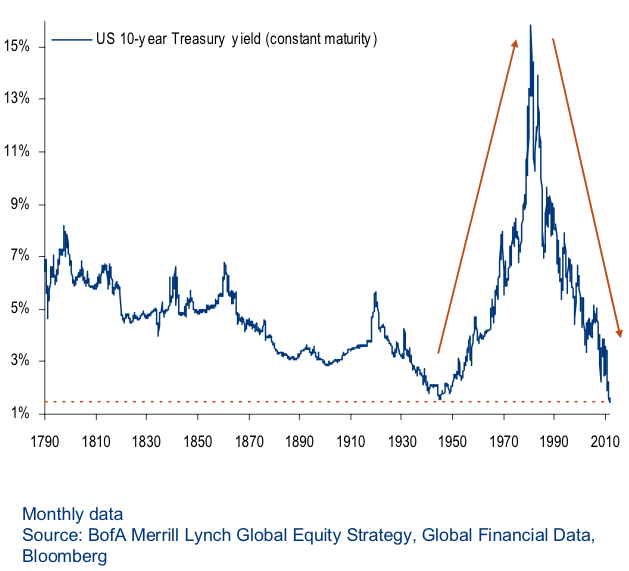

Notwithstanding, insofar as the econometric models suggest the much awaited inflationary recovery is set to materialise, economists take this view. Hence, watch out for the bond rout! As the top left graph demostrates, Wall Street economists might as well change careers to become tarot readers or public health officials. Seeing that they are always overly optimistic about economic prospects and the efficacy of the policies pursued by the government, why will it pan out differently this time around? Obviously, it will not and in spite of all the kerfuffle surrounding the current sell-off in the long-end of the UST market, this has actually been one of the weakest in the last quarter century, as shown in the top right table. Like I mentioned above, economic and financial conditions remain tight. Undoubtedly not as much as they were a year ago, but still enough to momentarily push T-bill rates to negative territory, which is depicted in the bottom left chart. Similar to the economic environment of the last thirteen years, the Great Depression of the 1930's also experienced all kinds of weird phenomenons that have transpired since the GFC. Albeit a topic for another day, as the bottom right graph indicates, the deflationary conditions of that period brought about an insatiate demand for those safe and liquid Treasury securities., despite the tremendous amount of government debt issued to finance the New Deal programmes.

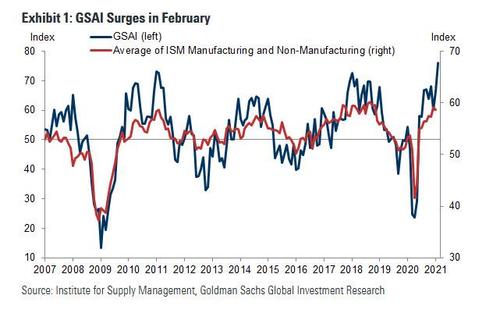

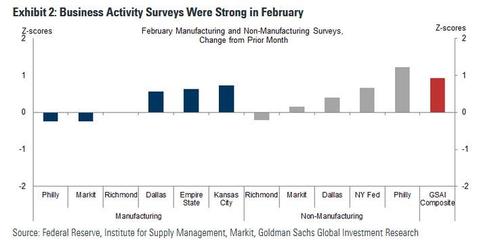

Moreover, the Goldman Sachs Analyst Index (GSAI), which provides a snapshot perspective on the US economy (and thus differs from the BEA's GDP measure which is an average look at output over a period of time), rose 9.4 points to an all-time high of 76.0 in February. The composition of the survey was strong, as the orders, shipments, and employment components all increased. Most regional business activity surveys were very strong in February with Goldman's manufacturing (+0.4pt to 58.2) and non-manufacturing (+1.7pt to 54.2) survey trackers both rising (bottom table).

To break the data down to its various items, one clearly realises the picture is not that rosy, as one may have initially expected. To wit, the sales and shipments component surged +19.0pt to an all-time high of 90.2. The orders component increased (+13.3pt to 76.2) by more than the inventories component (+3.2pt to 53.2), increasing the orders-less-inventories gap to 23.0. The employment component rose to its highest level since December 2018 (+0.9pt to 66.6), and the wages component rose to its highest level since May 2018 (+6.8pt to 81.8). To cap it all off, the output prices component decreased (-4.0pt to 77.3), while the materials prices component increased (+1.4pt to 80.0). Basically, the rebound from the massive depth of the Q2 2020 trough has entailed, without surprise, a surge in activity, along with the stimmy checks like the ones the Trump administration began to send out at the end of last year as a parting gift. What is most noteworthy is the dissonance between the apparent burgeoning demand and the declining output (i.e., consumer goods) prices. The explanation is something that I have discussed earlier this month. To make long story short, the distortions in the supply chains provoked by the paranoia-induced restrictions of all sorts have led to shortages of goods (e.g., computer chips, ship containers, etc) and services (more strikingly in transportation), among other unintended consequences. Ergo, because the transportation industry, chiefly shipping, is impeded to function smoothly, businesses have increased their orders to get as much supplies and as fast as they can get them, in order not to be forced to reduce or halt production outright. Naturally, this has caused even more disturbances in the supply chains, as the PMIs have also captured (below charts). Therefore, higher input prices, though lower output prices on account of lackluster demand.  To conclude, these circumstances are surely not propitious to a rapid adjustment of the productive structure, which is wholly necessary for the economy to fully recover. Besides everything I have presented here, since the supply squeeze is squeezing producers' margins of profit, how is this conducive for them to hire?

Eventually, due to shrinking margins, they will pass part of the cost on to retailers and these, in turn, will pass it to consumers afterwards. However, in view of the unreliable income source for most consumers, these are not going to totally spend their stimmy checks. Thus, retailers and producers and the rest of the supply chain participants are going to be the ones to absorb the costs entirely. Unsurprisingly, a lot of them are not going to manage this squeeze and will certainly be wiped out. On top of that, the government stipends are, on the one hand, lifting demand to higher levels it would otherwise be in a laissez-faire economy and, on the other hand, making it far more costly for businesses to fill their job openings due to the government being unconsciously competing with them by bidding for (potential) workers - these stipends make it much more appealing to stay unemployed and have pratically 100% of leisure time. Therefore, seeing that governments, especially Uncle Sam, are, in addition to hampering the normal functioning of the economy because of the corona-phobia, precluding the swift adjustment of the price and profit system, there is no way the economy is going to break from its deflationary shackles anytime soon. To make matters worse, the growing encroachment by eager politicians and clueless technocrats are sure to reduce the (global) economy's potential even further, depressing its trend henceforth.

0 Comments

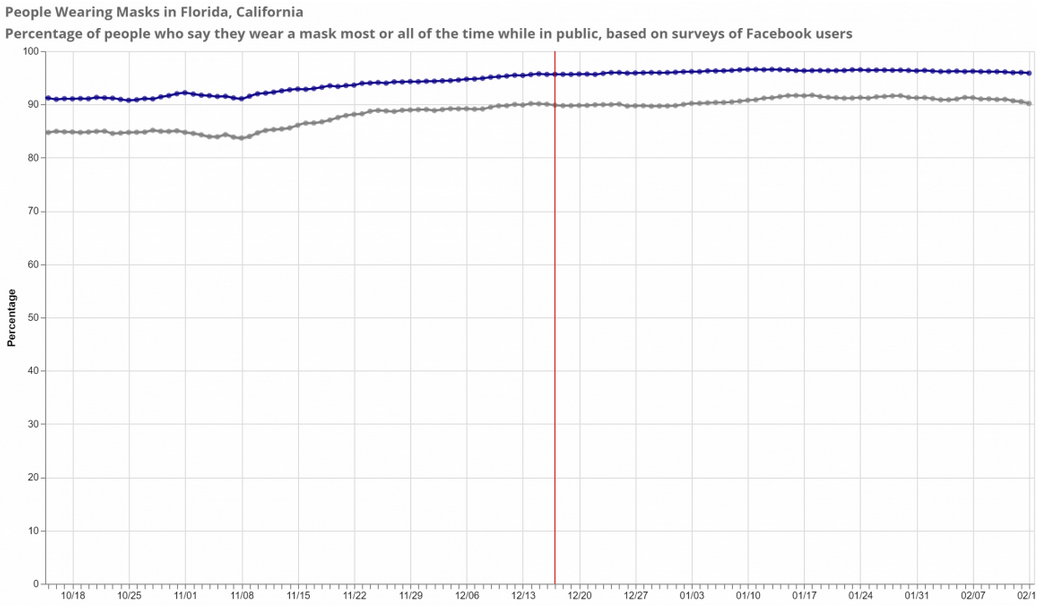

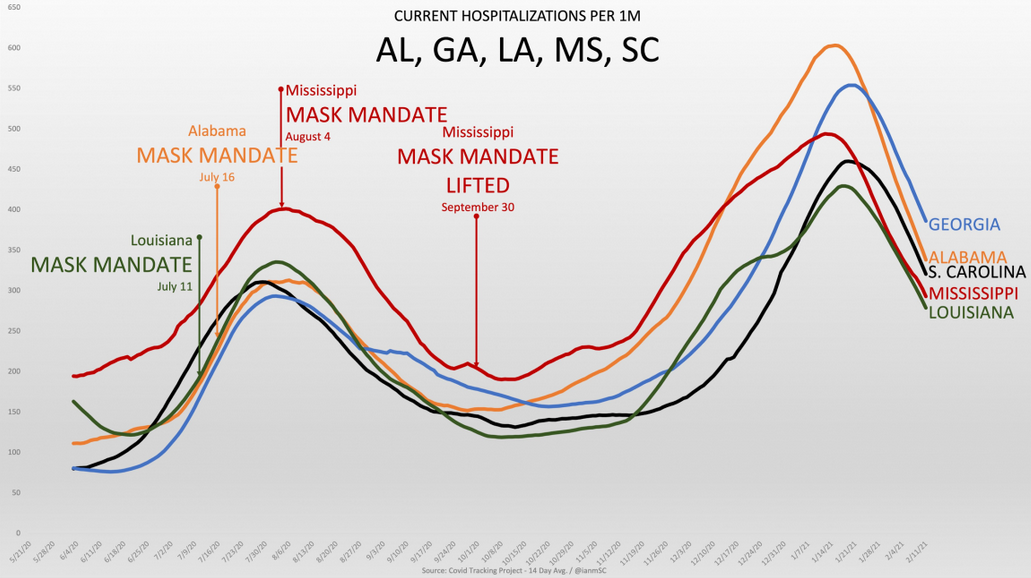

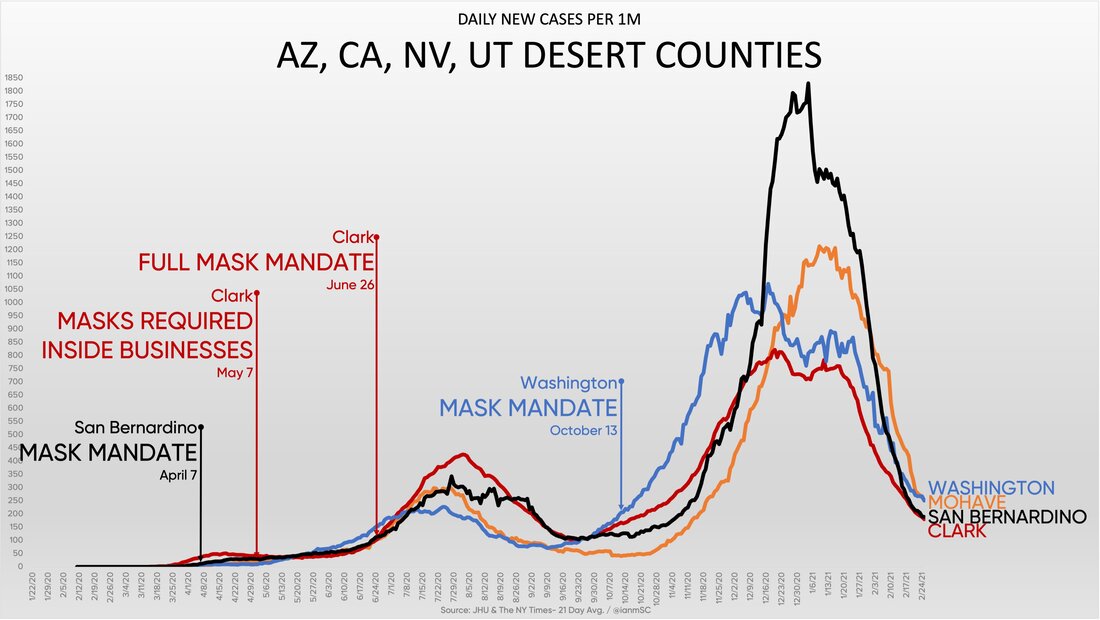

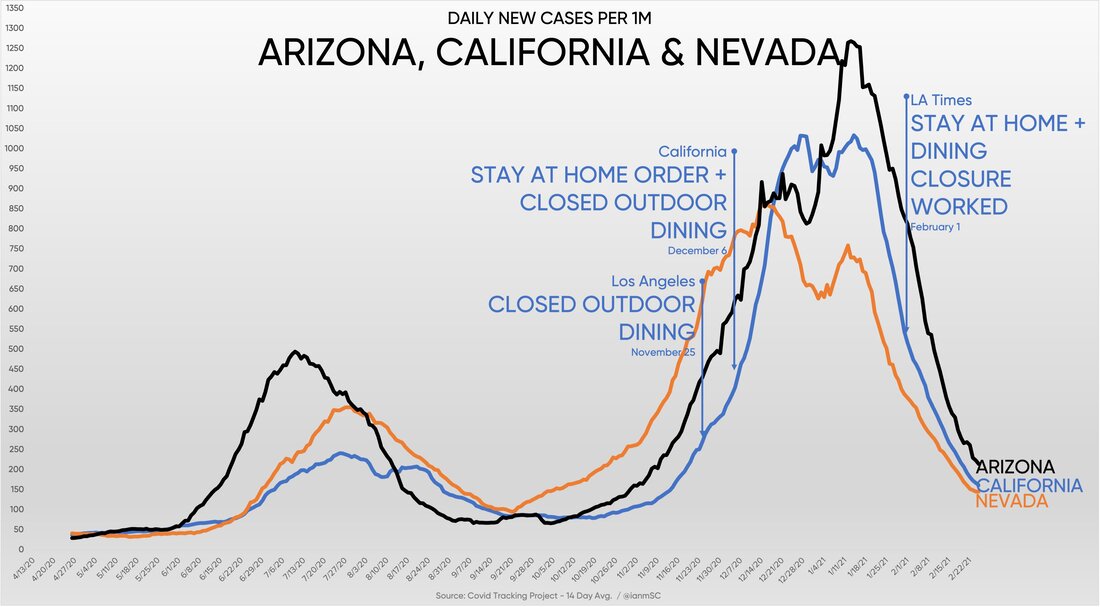

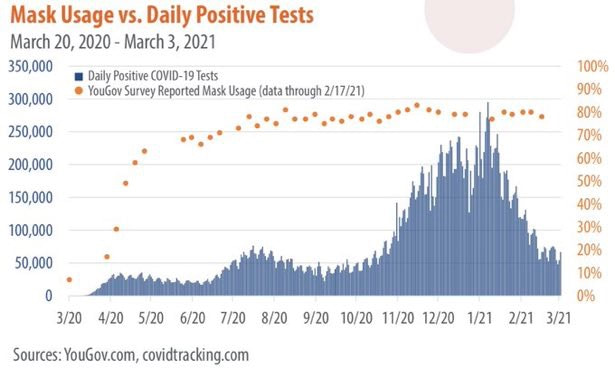

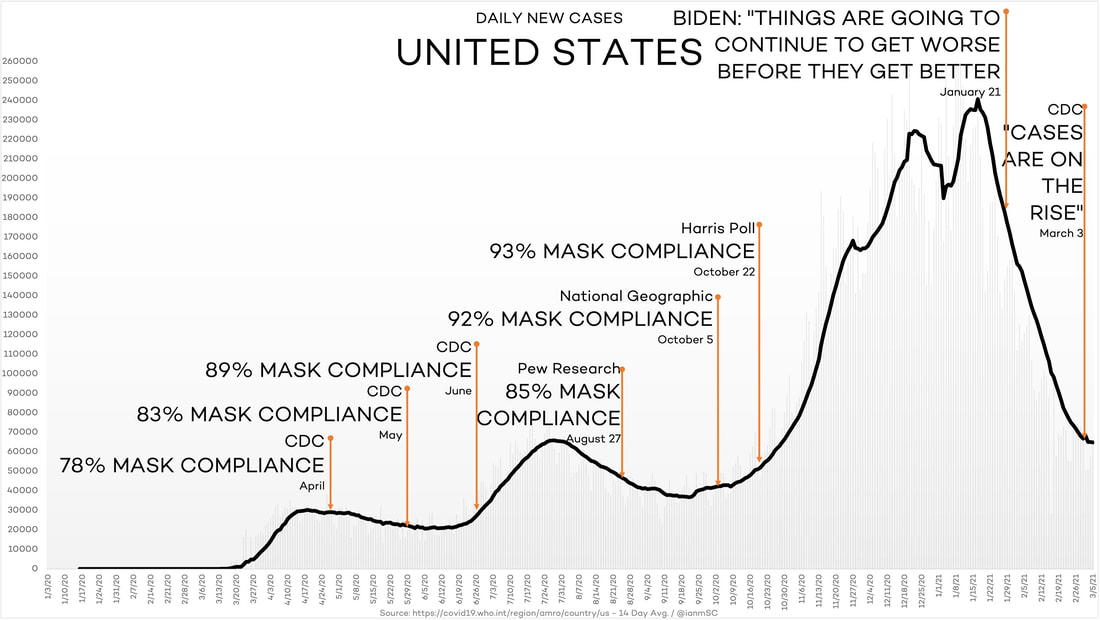

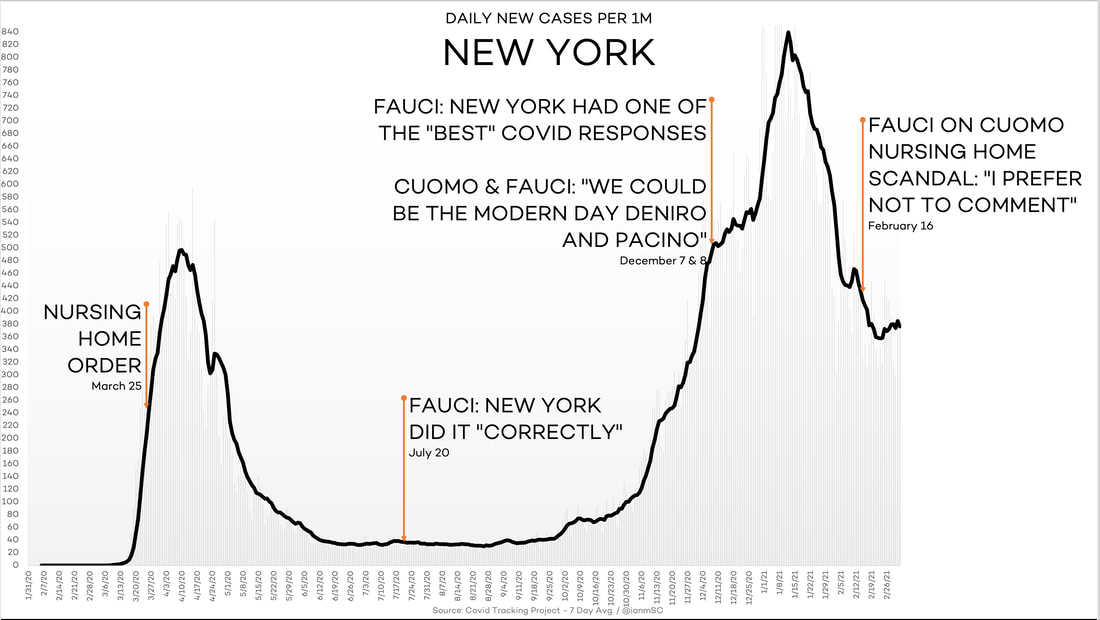

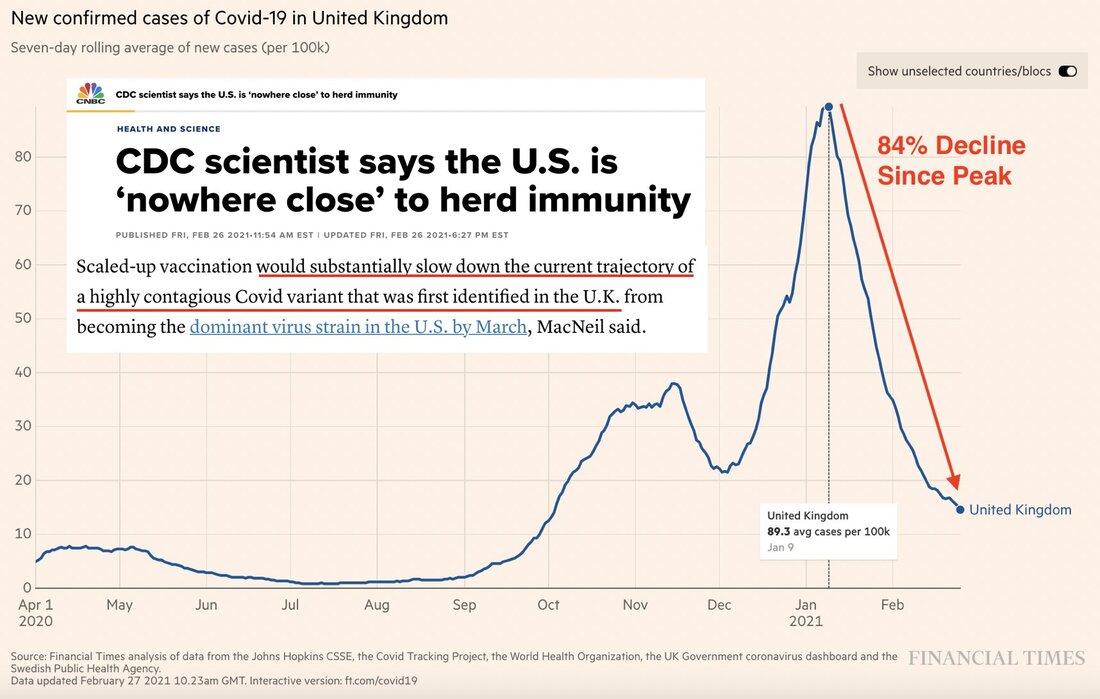

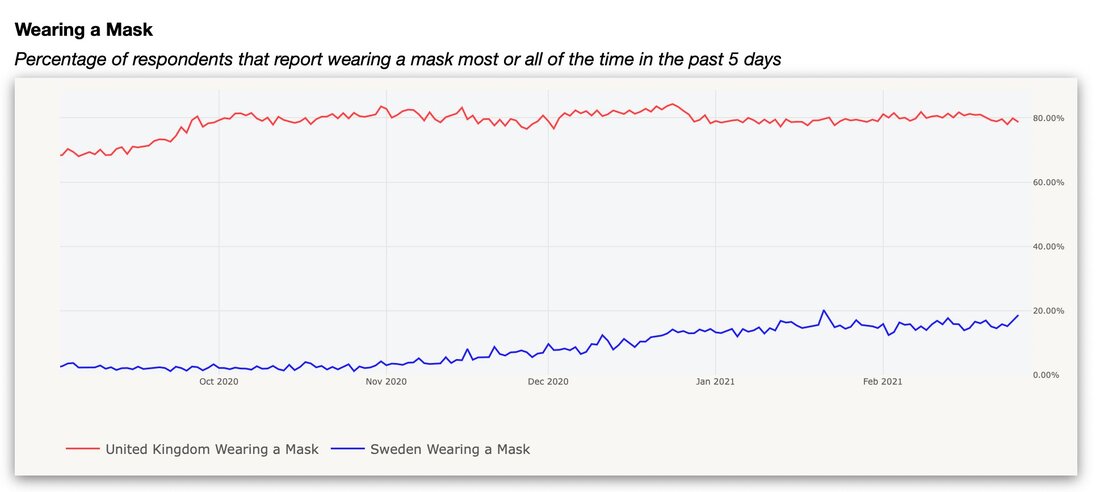

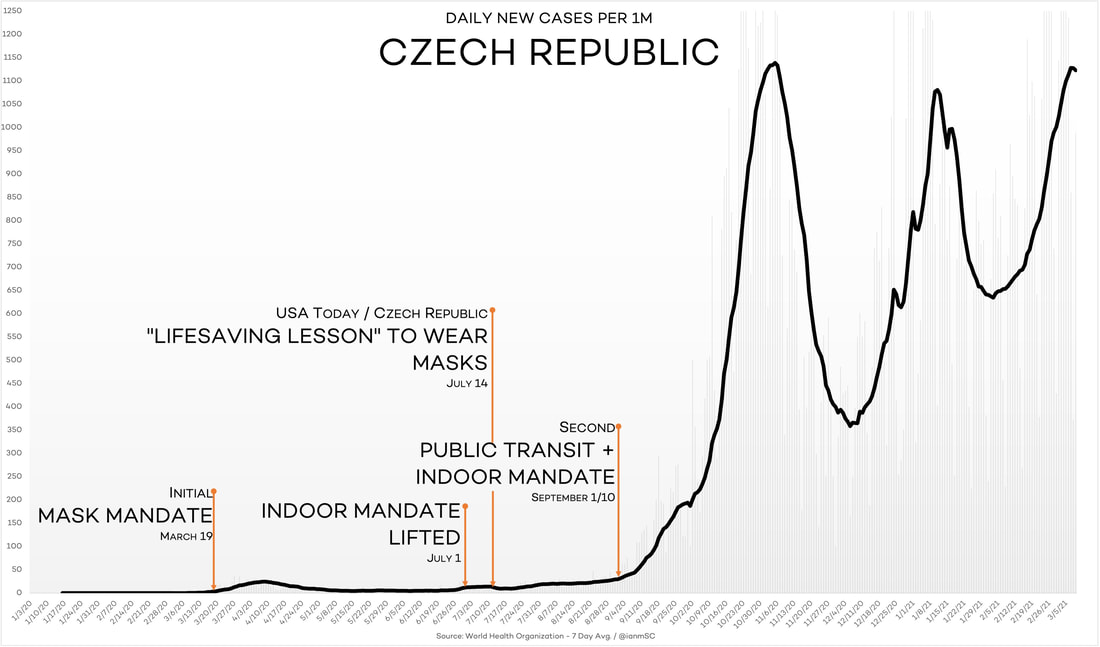

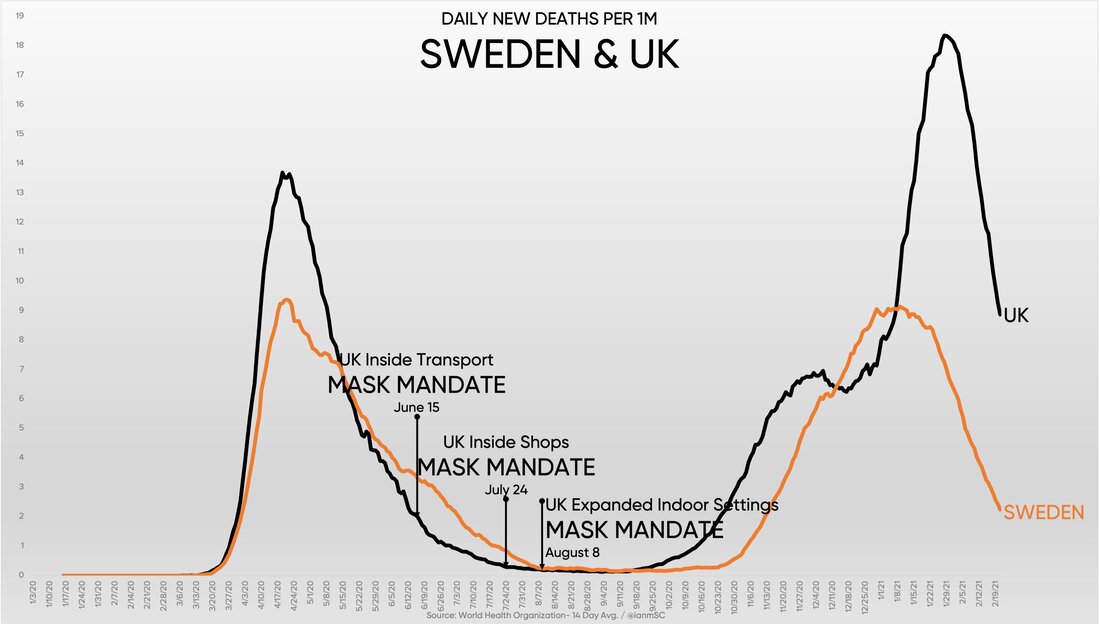

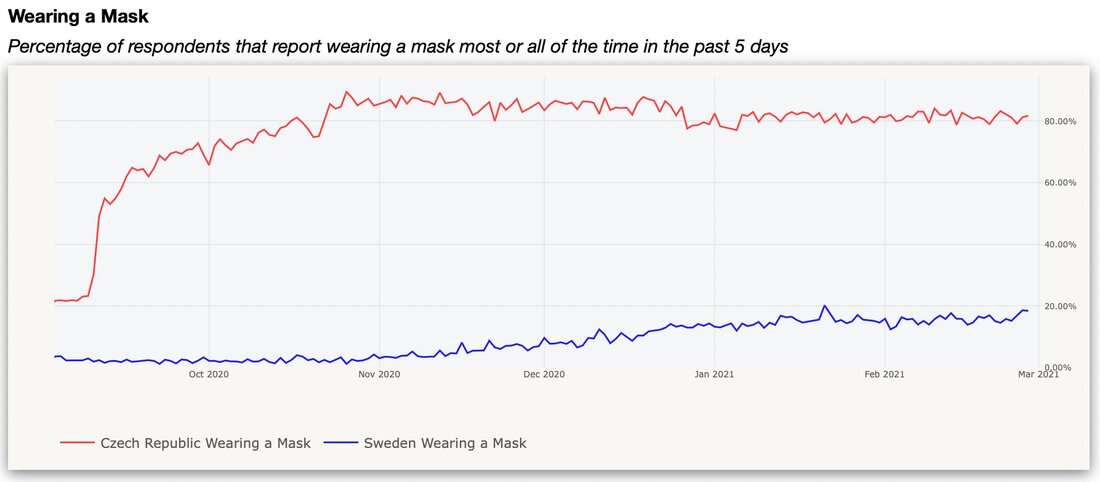

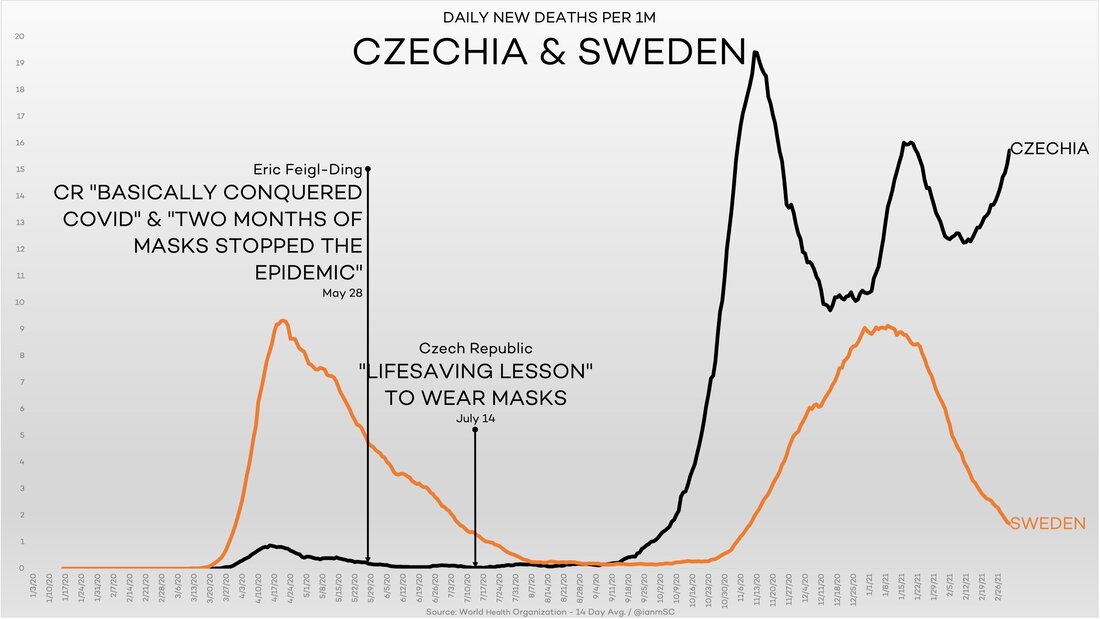

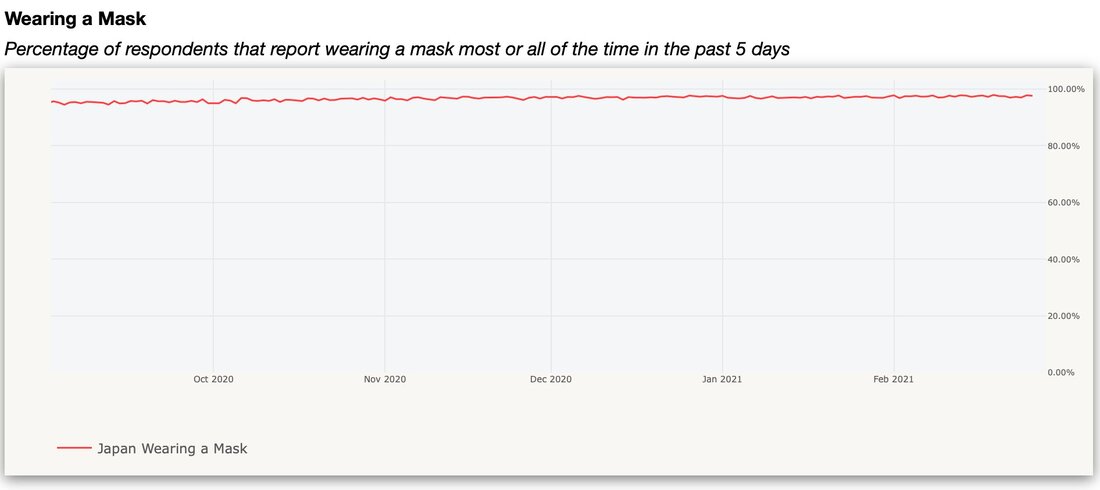

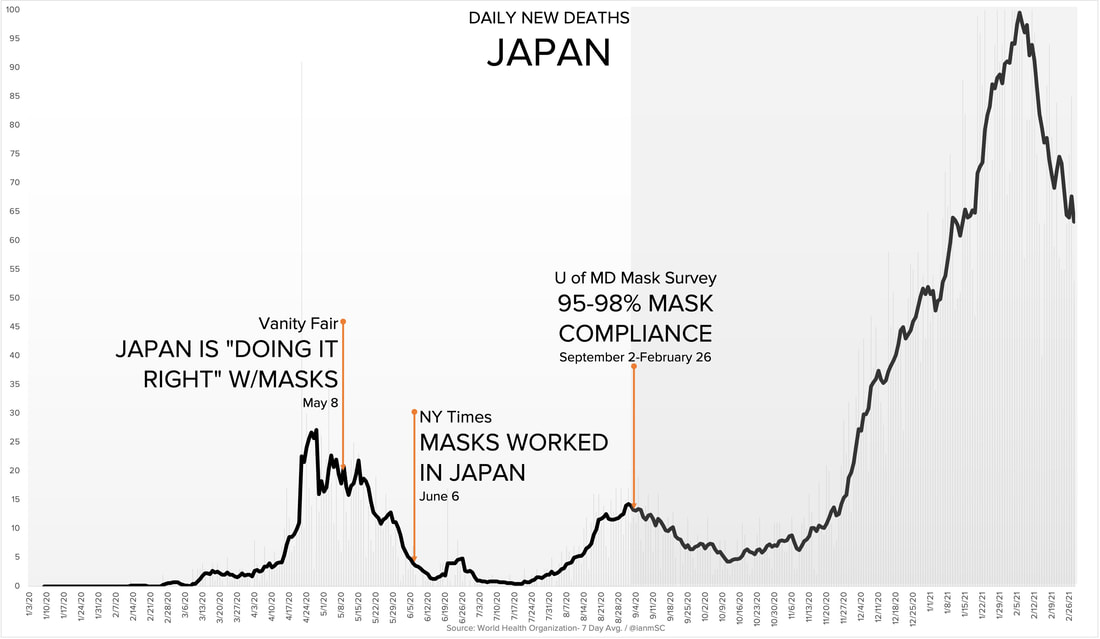

Throughout the History of mankind, there have been episodes of various kinds and degrees of calamity and hardship, which inevitably caused severe torment and provoked widespread panic. Regardless of what you hear on the news or in conversations with friends and family members, Covid-19, or the kung-flu as I prefer to call it, is not one of such episodes. Notwithstanding, there has curiously been plenty of severe torment and widespread panic around this virus. Insofar as the kung-flu constitutes nothing more than another influenza-like illness (ILI), the agony and anxiety the world has been experiencing must have a source, or more, other than the virus itself. Overall, the excess mortality caused by the kung-flu (direct or indirectly) is mainly linked to the obesity levels and the aging of the populations of each country. As you can check out here, 2020 was, by and large, an outlier in terms of the mortality rate in the advanced countries of the West (Europe, North America and Australia and New Zealand). Albeit a result of several factors, it is pretty clear the overriding one is geography. Undoubtedly, neighbouring countries have had similar outcomes, with the glorified non-pharmaceutical interventions (NPIs), such as masks and lockdowns, and other measures like contact tracing and large-scale testing turning out to be a complete flop in stopping the coronavirus' advances. By implementing these measures, policy-makers were just following the advice of the presumed experts on the fields of public health, virology, epidemiology, etc. If the scientists were stating the NPIs and the like were necessary to avoid a global rampage in the scale of the Spanish flu, who the hell are you to criticise them. For one, scientists do not all agree with each other. This idea of consensus has no place in any scientific endeavour. Just because the majority defends one position, it speaks nothing to its truthfulness. Moreover, with media outlets being profit-maximising entities (i.e. businesses), they always try to engage the most viewers possible to generate as much revenue as they can get. Thus, they have long ago realised the best strategy is to entertain, not to inform. Under this entertainment umbrella, besides spinning false narratives of collusion (Russian hoax) or insurrection (Capitol "invasion"), they also produce doomsday scenarios. While climate change and extreme weather events are usually these corporations' preferred themes, the flu season provides a nice change of pace. In fact, just lask week, Jason Kilar, who is the CEO of CNN's parent company, WarnerMedia, said "the pandemic and the way that [CNN] can help inform and contextualize the pandemic, it turns out it’s really good for ratings".  In addition, as I referred on just a few paragraphs ago, the settled view on any particular matter could be completely wrong, even though it passed the scientific method's scrutiny. For a moment, try to remember the times you read a headline stating some study which claimed that a cup of coffee a day was bad for you, having a couple of days before read another headline about another study asserting that a daily dose of coffee was actually beneficial. Therefore, seeing that these two were both peer-reviewed papers, published on scientific journals, how does one know, especially a layman, which one is right? You simply have to look at the data yourself and come up with your own judgement. Unfortunately, the vast majority of the people would rather save the trouble of doing the work to stay informed, bestowing their independent reasoning faculties to those in the seats of power. Whether this makes me cynical or not, the harsh reality is that politicians are only going to hear and do what makes them more popular so as to stay in power. As a result, in times like these, our rulers are going to put forward policies that, in lieu of being aimed at solving or mitigating the situation, it has the intent to lionise them as heroes. This is not to say that they never try to provide solutions to problems, it just means that making themselves look like heroes is the top priority. In plain and simple terms, they have to be seen as indispensable.  As all over the world we celebrate the one-year anniversary of fifteen days to flatten the curve, we have yet to acquire any data suggesting that the past year of life-destroying lockdowns and politicised behavioural mandates has done anything to keep us safe from the kung-flu. While lockdowns made a comeback in Europe and other regions, it is impossible to ignore the lockdowns' disproportionately deadly effects and the numerous studies demonstrating their futility. However, the media still retain their grip on the narrative that NPIs and other measures remain necessary to prevail in our fight against this virus. Government officials, in lockstep with big tech and nearly all major news outlets, have controlled the NPI narrative to such an extent that its proponents have simply sidestepped the burden of proof naturally arising from the introduction and continued support of novel virus mitigation strategies, happily pointing to the fact that their ideas enjoy unanimous support from the corporate media and government officials across the globe. Unsurprisingly, this seemingly impenetrable narrative rests on the critical assumption that NPIs, or behavioural instructions, have kept us protected against Covid-19. None other country than Sweden was the recipient of more rampant criticism on the response to the novel coronavirus. Since the middle of the summer, or even sooner, everybody started to acknowledge the Sweden response (or lack of one) had not been the disaster foreshadowed by the experts on television. Yet, the critics still claimed that they could have saved many more lives if the Swedish government followed the example of the other European nations, pointing out that its Scandinavean neighbours, Denmark, Finland and Norway, fared much better due to imposing those praised restrictions of people's liberties. Actually, contrary to what you have been led to believe, Sweden was, and still is, no less stringent than its neighbours. Be that as it may, a paper published in August outlines the factors which led to Sweden being in a worse position from the get-go, compared to its neighbours, as well as it defends the lockdowns and other procedures would be totally useless. By the time Sweden would hypothetically close its borders and encarcerate its citizens in their homes at the same time as their neighbours, the kung-flu had already been circulating freely, particularly in Stockholm, for about a fortnight, owing to "Sweden’s 'sport' break (sportlov), where families often go to Italy or Austria for skiing", Nevertheless, the two most important aspects they considered were the weight of the migrant population and the "dry tinder". About the former, it is pretty well established the people with darker skin, living in higher latitudes (outside of the tropics, where they are adapted to live), have a greater likelihood of dying from Covid-19 - this in mainly due to having darker skin that inhibits the production of vitamin D, which is extremely important to fortify the immune system. On the latter, the "dry tinder" aspect alludes to the fact that Sweden had previously had a couple of flu seasons milder than usual, unlike the other Scandinavian countries. Still, Sweden has endured far better than most of the other developed nations.  Across the pond, among the few US states that did not impose statewide restrictive measures, Florida has been the most mediatic, maybe because of its size and importance. In light of everything our officials have babbled about how this virus spreads, it defies reality that Florida, a fully open and popular travel destination with one of the oldest populations in the country, currently has lower hospitalisations and deaths per million than California, a state with much heavier restrictions and one of the youngest populations in the country. While it is true that, overall, California does slightly better than Florida in deaths per million, simply accounting for California's much younger population tips the scales in Florida's favour. More specifically, Florida has zero restrictions on bars, breweries, indoor dining, gyms, places of worship, gathering sizes, and almost all schools are offering in-person instruction. On the flip side, California retains heavy restrictions in each of these areas. At the very least, Florida's hospitalisations and deaths per million should be substantially worse than California's. Those who predicted death and destruction as a consequence of Florida's September reopening simply cannot see these results as anything other than utterly remarkable. Even White House Covid-19 advisor Andy Slavitt, much to the establishment’s embarrassment, had no explanation for Florida's success relative to California. Slavitt was reduced to parroting establishment talking points after admitting that Florida's surprisingly great numbers were "just a little beyond [their] explanation".  Still, do masks and lockdowns serve their stated purpose? As the graph above shows, they do not, considering only masks at least. All the same, to demonstrate that I am not cherry-picking, and in view of the fact a picture is worth a thousand words, here comes a barrage of charts - on the top left one, California is blue and Florida is grey.

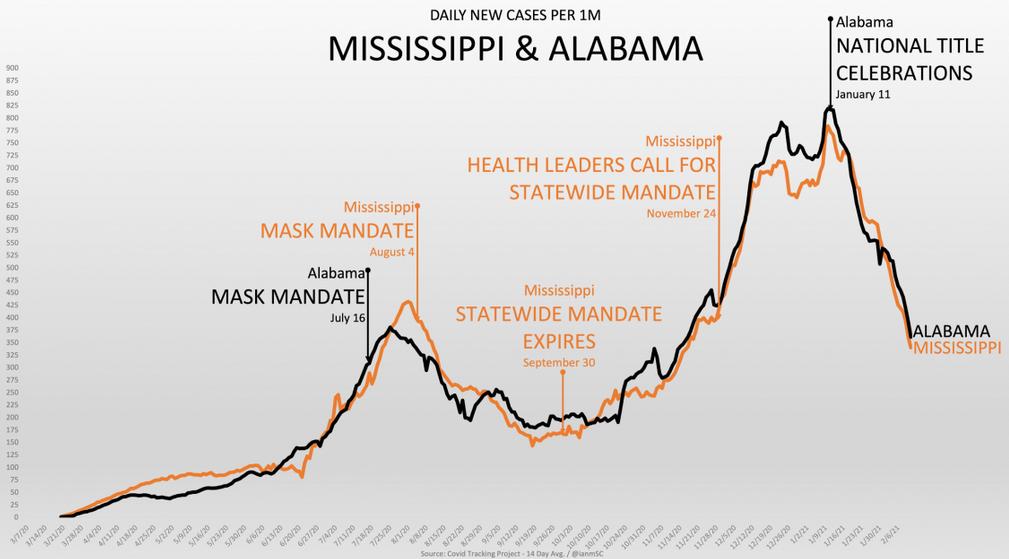

Daily new cases per 100k people; from John Hopkins Coronavirus Resource Center If it is not the NPIs that shape the course of the virus propagation, then what could possibly be? Seeing that similar patterns are formed among bordering and nearby countries and states, instead of legislative decree, case counts and mortality rates are strongly correlated with temperature and latitude, a concept known as "seasonality". Evidently, whereas varying degrees of behavioural mandates have had no noticeable impact on cases, thanks to seasonality, identical regions follow similar case growth patterns. For the firm believer in NPIs, these simultaneous and nearly identical fluctuations between cities within the same state and among states having similar climates are inexplicable. After accepting seasonality as one of the driving factors behind case fluctuations, we can start speaking of "Covid season" as pragmatically as we speak of "flu season" - this is after all the kung-flu. A helpful visual of what covid season might look like, based on the Hope-Simpson seasonality model for influenza, can be found here. As a bonus, Alabama recently came under heavy fire after thousands of maskless football fans took to the streets to celebrate their team winning the national college football title. FanSided, among others, was quick to label the large celebration as a "superspreader" event, and health officials were worried that the Alabama "superspreader" was going to result in a huge case spike. Here is what really happened.  Miraculously, cases immediately plummeted after Alabama’s "superspreader" event and continue to dwindle to this day. If that did not suffice, Mississippi, Alabama's next-door neighbour, followed a nearly indistinguishable case pattern, despite hosting no potential "superspreader" events.

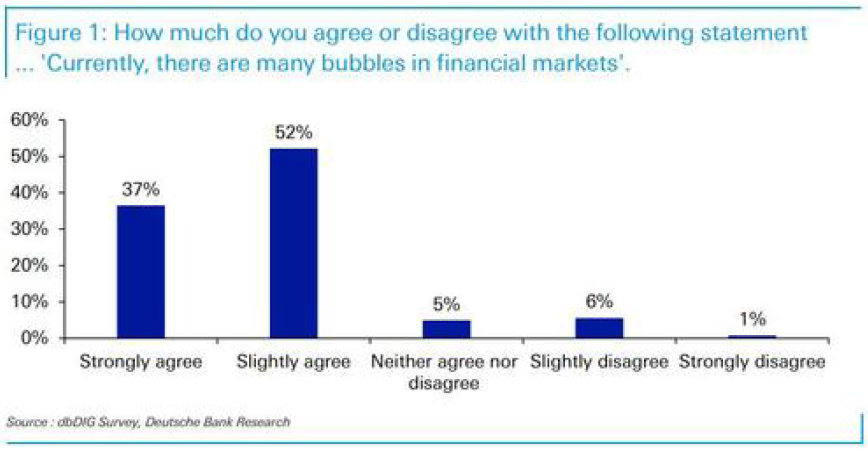

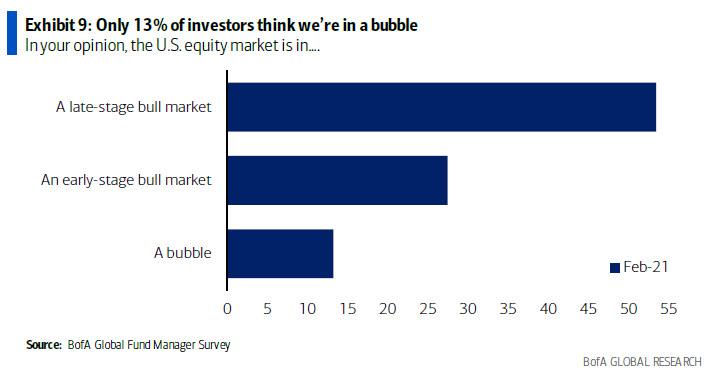

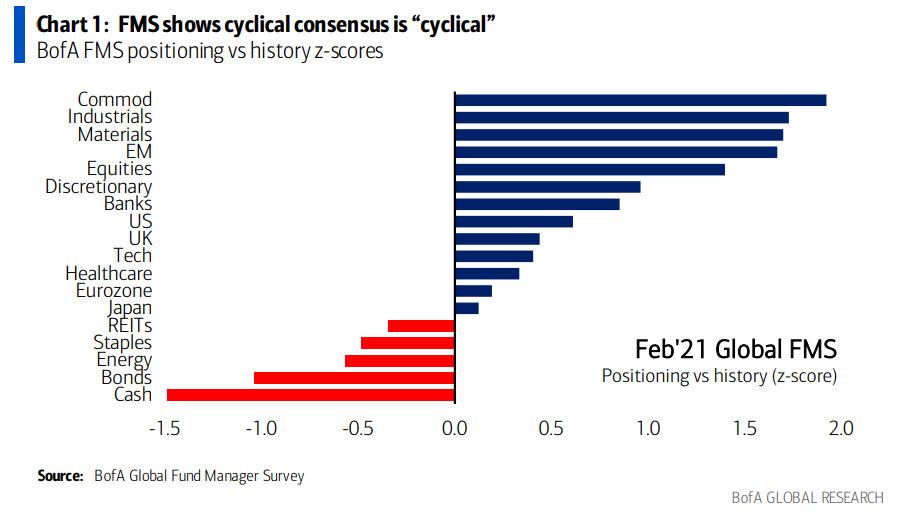

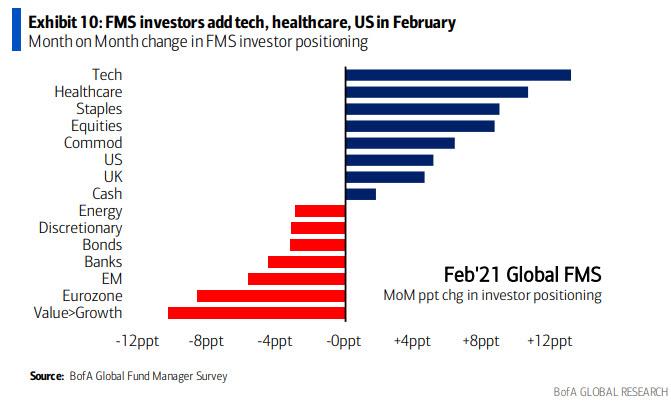

Moving on to the results begotten by those draconian policies, it is of paramount importance to note most of the excess deaths of last year were driven by our governments' measures. As Daniela Lamas, a critical care doctor at Brigham and Women’s Hospital, has written in a Washington Post article, "[t]hough we have always known that the cost of this pandemic would be greater than the number of the dead, we are only beginning to understand its true magnitude. In what might be a final wave of this pandemic, we find ourselves treating patients who have avoided the virus only to succumb to its many unintended consequences — addiction, untreated disease and despair". However, it was not the pandemic that caused this single-minded focus, where Covid-19 is the only harm to be taken into account. Instead, it was the government-imposed policies enacted in response to the pandemic. Without surprise, a pathogen alone with such a narrow demographic impact cannot cause such devastation in so many. In reality, it has been the NPIs that locked people out of their workplaces, schools, hospitals, and churches, wrecking life for billions of people worldwide. "The long shadow of this disease is everywhere," Ms Lamas writes. Although it is a long shadow all right, the shadow belongs to government interventionism mainly, and, partially, the public panic fueled by media hysteria that led people to acquiesce to massive violations of their rights and freedoms. Sadly, the refusal by the media to report objectively and soberly the facts about the kung-flu and - like the link between obesity and the risk of dying from Covid-19 -, especially, the calamity occasioned by overstepping technocrats is keeping the public in the dark to this day, believing these actions to be absolutely necessary to control the spread of the virus and, consequently, to keep deaths at a minimum. In conclusion, that is the problem with all this absurdity. Our rulers act on the grounds the virus can be controlled. Unsurprisingly, and as I exposed on those graphs above, the kung-flu, once it reaches a territory unchecked in the middle of the Covid/flu season, it is impossible to stop its advance, no matter how stringent populations become. To draw a parallel with ancient times, our rulers are stealing from the playbook of the shamans. These measures are nothing more than modern versions of the rituals and sacrifices our ancestors performed to please the gods. In those days, in order to make sure, or try to, the harvest would yield enough food for the population, they would do things like the rain dance or slaughtering thousands of individuals, particularly virgin girls, to make the gods happy and, in turn, allowing the crops to be fruitful. On the one hand, if the harvest turned out to be a bonanza of food, the people would link that outcome to those practices, with the priests and rulers being exolted for their good leadership and superior intellect and powers (for communicating with the gods and knowing what they want). On the other hand, if the harvest became a failure, then the shamans and leaders would simply declare the sacrifices were not enough or that the gods disliked the offerings - perhaps the virgin was a bleeder. In this case, they would double down, triple down, and so on, until a generous harvest season would arrive. Obviously, they had to do this so as to maintain the illusion of having dominion over nature and, therefore, keep the people (happily) under their rule. In the end of the day, that is what this all boils down to: superstition. Whether one carries a shamrock or horseshoe for good luck, or someone else consults a clairvoyant, they both do it to have a sense of control in the chaos that is life. Nevertheless, going back to the present, the public is increasingly being more doubtful about the true danger the kung-flu has posed, in particular the actual death toll caused by the virus and not being a mere coincidence. In other words, they are beginning to question what is the real amount of individuals that died from Covid and not with Covid. Around the globe, ever more swaths of people are realising that lockdowns were pointless, unnecessary, and destructive. Those who hold positions of authority in politics, belong to the media or others who have been spewing fearmongering spatter through our screens for the past twelve months are bound to face a reckoning. Will the modern day shamans lose control of the situation? Are the people finally discerning the technocrats powerlessness and irrelevance? Let us not jinx it, though I am keeping my fingers crossed and kissing my rabbit's foot. To cap it all off, if the technocracy loses its grip in this field, could this sceptical stance expand into other areas, say the monetary, the financial or the economic ones? Sure, if that is God's will. Having a financial crisis after experiencing a tremendous one just a year ago, is something few people are expecting. Regardless, one would be foolish to completely dismiss a crash right around the first anniversary of the last one. However, in spite of being very little reason to suggest a repeat of the 2020 Global Financial Crisis (GFC2), or anything close to it, is going to occur in the following weeks, some indications point for a new financial system meltdown not being as fanciful as the laws of probability would have you believe. Be that as it may, I still think the most plausible scenario is for some correction in the markets, particularly in the stocks' one, due to rising instability as the (winter) quarter-end bottleneck nears. Following the GFC2 and lifting of restrictions during last spring, every market, from stocks to high-yield bonds, has gradually been returning to pre-corona levels, having been driven by the assumption that the (global) economy was going to totally and immediately recover, like the flick of a switch. With all the monetary and fiscal "stimuli" injected in the economy and financial markets, the much hoped for "V-shaped" recovery was in the bag. Although the real economy not experiencing the putative recovery, the presidential election results, the vaccine discoveries, as well as the Blue Sweep in Congress, propelled markets, in general, to assume the economy is bond to roar, 1920's style. Without surprise, the stock markets have been the main adherents to this narrative. Albeit a worldwide phenomenon, let us just focus on the US financial markets. In view of going through such a monumental rally since early November, according to Deutsche Bank, by late January most of the respondents (89%) were seeing some bubbles in financial markets (left graph). Curiously, the Bank of America Global Fund Manager Survey (FMS) of February (right graph) reports that only 13% of the managers surveyed took the view that the US stock market was in a bubble. Notwithstanding, more than half of them felt the bull market was getting exhausted.

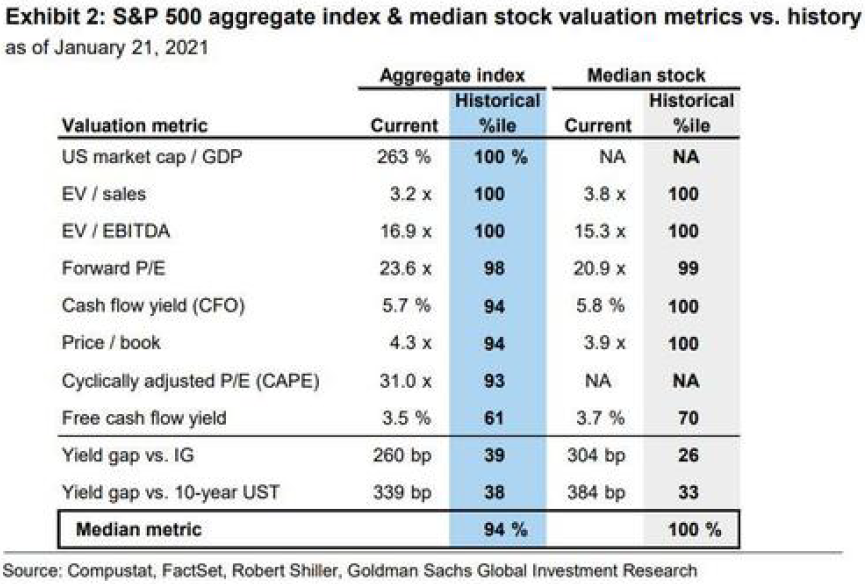

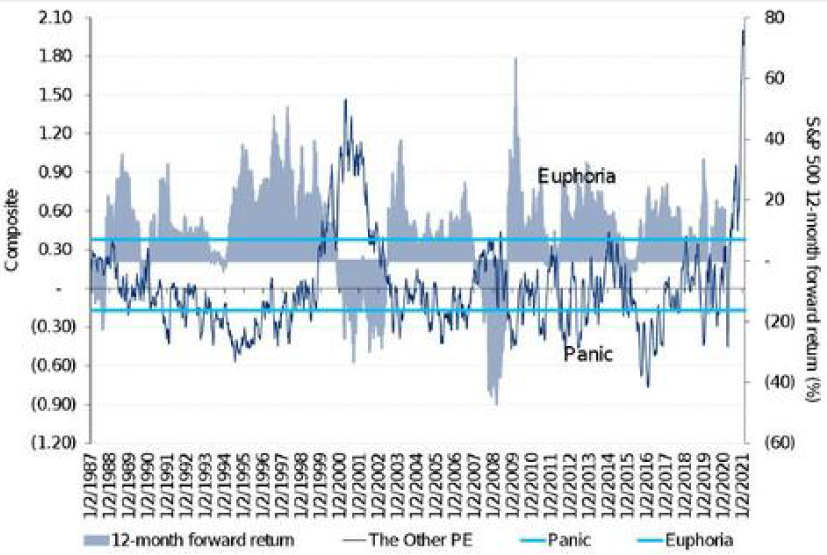

On account of this topic deserving a post (at least) for its own, the discussion about the stock market being at fair value or in a bubble, despite being interesting and important, it is rather irrelevant for today's subject. Surely, there are several of indicators that are, or have recently been, at and near all-time highs, though valuation metrics (left chart) do not tell the whole story. Nevertheless, there has certainly been bubble-like behaviour. Starting with the army of day-trading Robinhooders, receiving their investing tips in highly esteemed financial venues such as Instagram and TikTok, strolling to the relentless amount of IPOs and SPACs that only seems to end when everybody and their mother have one, in addition to the outperformance of stocks with negative earnings, and ending with the short squeeze fueled by r/wallstreetbets crusaders, there are definitely some resemblances to a bubble. As the chart on the right shows, which is Citi's Panic/Euphoria model, investors have never been this euphoric, auguring horribly for the 12-month forward return of the S&P 500.

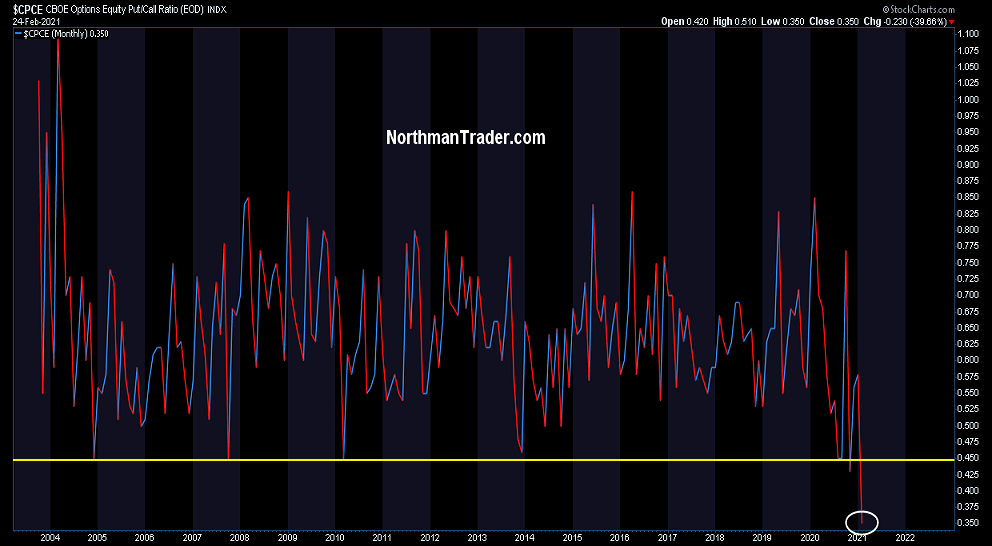

Moreover, the new round of stimulus checks, as part of another $1.9 trn package, which is set to be enacted very soon, "could unleash a $170 bn wave of fresh retail inflows to the stock market, according to Deutsche Bank AG strategists." Therefore, it is no wonder why the demand for puts has not accompanied the surge in call-buying - as demonstrated in the historical low on CBOE's put-call ratio (left chart) -, because ever since the March trough, short-sellers have been slaughtered, as the the graph on the right depicts.

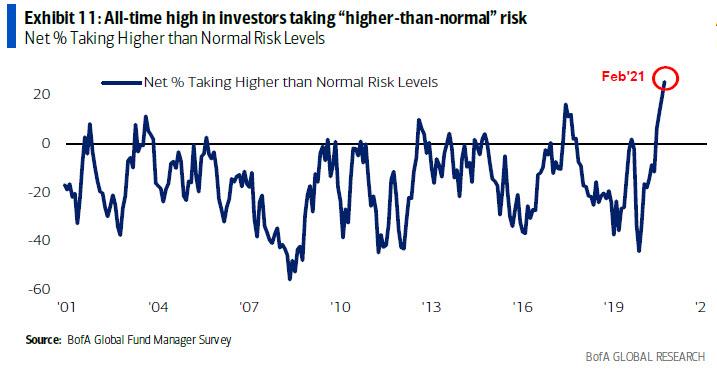

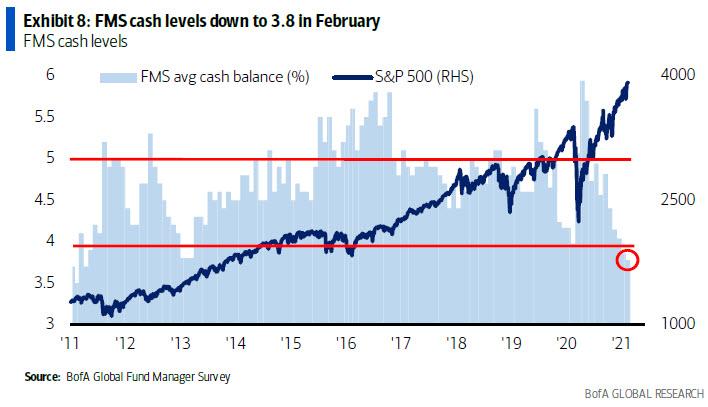

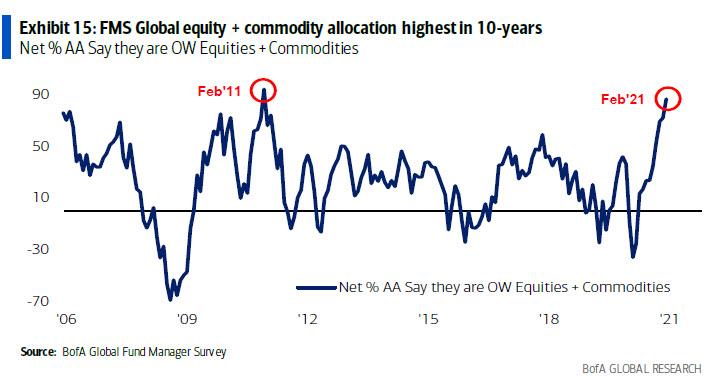

All the same, the reverence for the technocratic institutions responsible for all the record "stimuli" has prompted those in the financial services industry (as reported by the FMS) to take never-before-seen levels of risk. Hence, their cash balances has not been this low since 2011, which proved to be a bad decision by the middle of that year (Eurodollar #2). So, an eventual liquidity stress is far from the managers' minds. What could possibly go wrong?

Thus, investors are positioning themselves according to either the "roaring 20's" or the "commodities supercycle" narratives, or more likely both of them. Bearing in mind what I asserted on Monday, "[a]s soon as individuals start seeing their bank accounts ballooning through their own endeavours in the economic system, as opposed to handouts from the political system, consumption will pick up, although that is naturally taking a lot of time to ensue. Nevertheless, one thing is for certain, as long as society holds this collectivist mindset that is beholden to politicians and technocrats, an economic boom, worthy of this designation, will never happen and, thus, a commodity supercycle will have to be deferred".

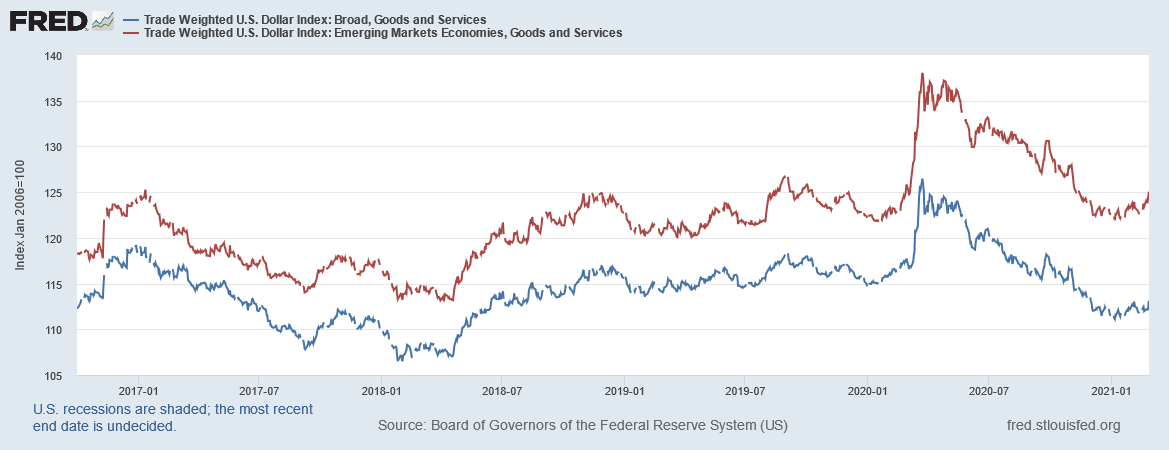

At least one bank is getting worried about the prospects for stocks. According to Bank of America’s Sell Side Indicator, which tracks average recommended stock allocation by Wall Street strategists, by rising to 59.2% it is signaling that bullishness is overextended and is now time to sell. Although that supports the view that equities are overdue for a correction, it does not insinuate that a financial crisis is on the horizon. For that, we have to look at other indicators and markets. Having said this, the T-bills (along with the 2-year; left chart) and the US dollar (right graph) have been implying since the beginning of this year that, as a reflection of the state of the economy, financial conditions have deteriorated. Obviously, this alone does not mean the markets are about to crash. However, it suggests that the financial system (Eurodollar) has been growing more wary of potential deflationary risks, and rightly so.

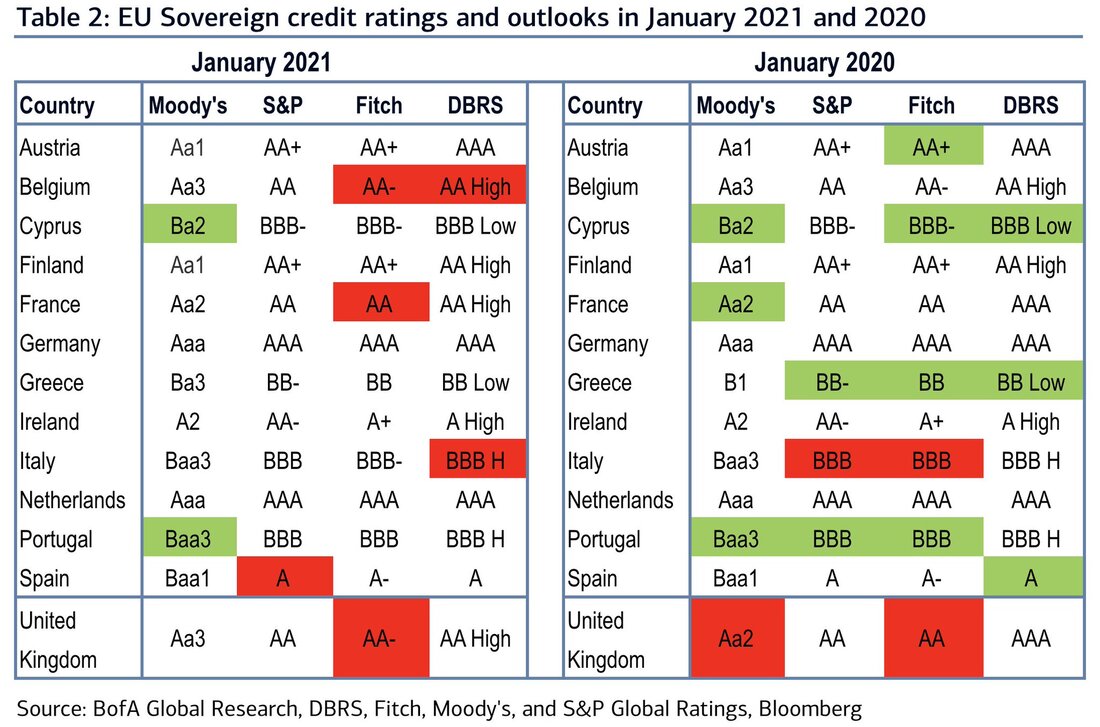

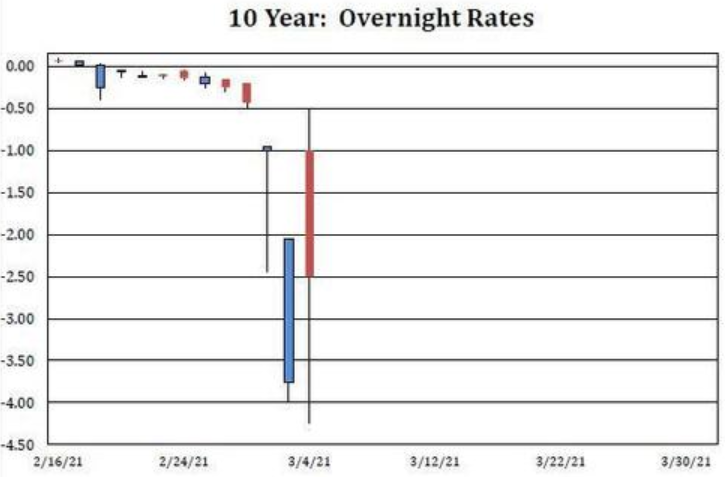

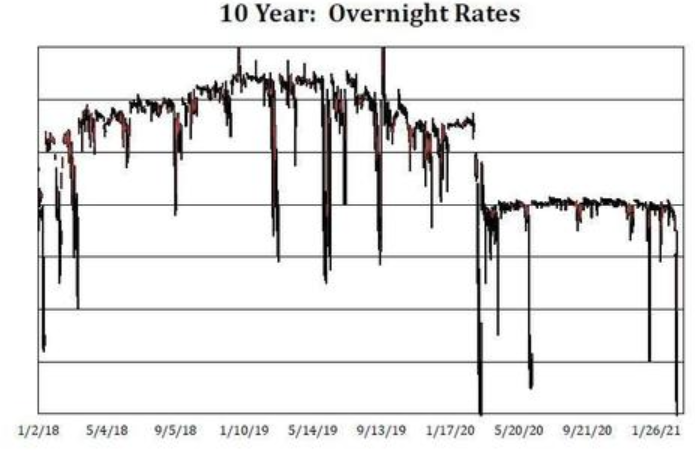

In case it is not clear in the graph above and you have not been paying attention, yields of the T-bills have curiously been dwindling since early November, being extremely close to the zero lower bound. Lately, the explanation for this has been something to do with the Treasury General Account (TGA). More specifically, the TGA is the account the US Treasury Department has at the Fed. Supposedly, due to the release of fiscal "stimulus" engendered by Uncle Sam on the economy, the TGA balance will decline from $1.6 trn to $500 bn by the end of June. Basically, this roughly $1 trn decline will occur either through waves of fiscal spending, which will expand deposits and reserves at large banks or, if spending is too slow to meet the $500 bn target, through bill paydowns. Furthermore, coupon (notes and bonds) issuance will be $1.4 trn over the first half of the year, which will be bought mostly by banks. However, an obstacle arises. The Supplementary Leverage Ratio (SLR), which, as the name implies, supplements the US leverage ratio by taking into account, besides on-balance sheet, certain off-balance sheet assets and exposures - learn more here; what consists exactly is not important, though -, is going to be fully implemented as the regulatory break (enacted during the GFC2) is set to expire on March 31. Unsurprisingly, this re-imposition is going to once again include US Treasury securities and deposits at the Fed (bank reserves) on the calculation of this rule. Allegedly, owing to the SLR, the commercial banks in the US, mainly the primary dealers, do not have the balance sheet at the bank operating subsidiary level to add $1 trn of deposits, reserves, and Treasuries. Unless we get an extension on the SLR relief, banks will have to turn away wealthy households’ and institutions’ deposits, which will then go to money market funds. Despite that, money market funds will face a constraint too. The marginal asset they will direct inflows into, the Fed's overnight reverse repurchase agreement (ON RRP) facility, is capped. Each money fund can place only $30 bn into this facility, which is just too little. In fact, banks’ balance sheet constraint becomes a collateral constraint for money market funds. Even though collateral supply from coupon issuance will absorb this cash over time, money markets react to what happens now, and with $1 trn of new cash, there may be many pockets of collateral scarcity as these flows play out in real time. So as to resolve this, the Fed has to intervene once more and allow intermediaries to park that extra trillion dollars in cash somewhere. Otherwise, if the Fed refuses to uncap the ON RRP facility, T-bills and repo could go negative. Going back a bit, what banks turning away depositors mean is that, in order to avoid complying with the cost of having "too many" deposits, the banks may impose a negative interest rate on those bigger deposit accounts. In addition, unless the Fed steps in aggressively and either grants banks SLR relief and/or the ON RRP facility is uncapped - so that banks have a place to park the "flood" of $1.1 trn in excess cash instead of turning it away - the US dollar Libor-OIS spreads are expected to reach zero by June, on account of foreign banks being the ones holding the bag, warehousing the rush of reserves. In part, I agree with this reasoning, particularly with the assessment the collateral scarcity will lead to lower yields. Yet, that whole point about banks running out of space for the safest and most liquid instruments (US Treasuries, bank reserves and cash) sounds ludicrous to me. As a matter of fact, since 2014, in spite of SLR being online, primary dealers kept on accumulating USTs and deposits without a problem. In my opinion, the plunge in T-bills' yields has been a result of, besides the diminishing supply being issued, rising concerns around the creditworthiness of individuals, businesses and governments as well, like the next table demonstrates. Being presented here the ratings of sovereigns, which are shown to have slipped, you can imagine what it has been like for companies and financial assets like corporate bonds and ABS.  Getting closer to the crux of today's matter, the overnight repo market has shown last week some irregular behaviour. As the chart on the left shows, the overnight repo for the 10-year Treasury traded deeply "special", which means the repo rate is negative, as a result of massive short-selling speculation. In a nutshell, so many investors are short the 10-year UST that there are not enough to go around. Ergo, the rate to borrow the 10-year in the repo market reached a low of -4% on Wednesday, March 3, and printed around -4.25% the following day (left chart). An investor lending out cash for the 10-year notes would end up having to pay, rather than getting paid. Oddly, that is below the -3% charge leveled on users who fail to deliver a security to a counterparty. Besides the colossal short base, the Fed has been taking supply out of the market through its large scale asset purchase programme, QE6. Evidently, this was the lowest print since the absolute record of -5.75% touched during the GFC2. Feeling the urge to act, "the Fed loaned $8.7 bn of its $10.9 bn holdings of US 10-year notes on Thursday, easing the debt squeeze", according to Scott Skyrm, executive vice president at broker-dealer Curvature Securities. By Friday, believe it or not, demand in the ON RRP facility peaked at $11.2 bn, apparently exceeding the Fed's holdings - seems too small an amount, though; perhaps $10.9 bn is what is alloted for this facility.

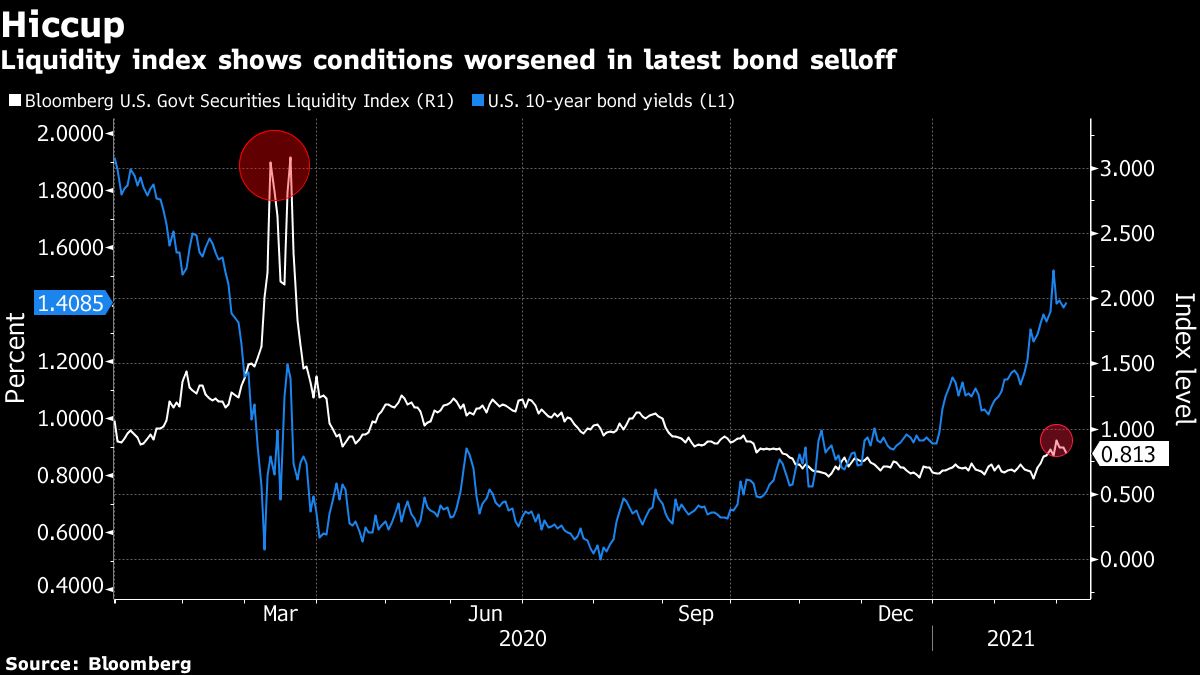

Moreover, because of the illiquidity/volatility that has impaired the smooth functioning of the financial system, it has not been just the Treasury market to feel the repercutions (right chart). What caused the small uptick in illiquidity was likely a mix of portfolio repositioning (reflation trade) and the "operational error" in FedWire, late last month, which triggered the latest correction in the stock market (left graph). Finally, in order to correct these key issues dealing with market functioning, a lot of people were awaiting for Powell or some at Fed to at least give the markets a hint that they were thinking about reviving Operation Twist, with the new one being the third instalment. In case you do not know, this programme consists of a simultaneous selling of front-end Treasuries (bills and shorter-term notes) and buying of longer-dated paper (bonds and longer-maturity notes). According to the advocates of such a policy, a Twist 3.0 will: i) pull up front-end rates; ii) stabilise back-end rates; and iii) it does so in a reserve neutral way that lessens bank SLR pressure to hold more capital. Hence, part of their solution entails taking from the market even more highly sought assets, even if they are wanted just to be shorted later on. Like I wrote a few paragraphs above, the SLR is no impediment for banks to hold more Treasury bonds and notes. Also, removing even more 10-year notes could precipitate more illiquidity due to shrinking supply of an instrument that is having tremendous demand. Notwithstanding, selling T-bills would surely help to satiate the impressive appetite for these assets, improving the health of the financial system.

Bringing it all together, as the squaring of the books take place in mid-March, and taking into account that illiquidity has been increasing, which has been indicated by t-bills and the US dollar (like was shown above) along with the peculiarities around longer-tenor Treasuries, it is reasonable to be concerned. Because of the ensuing collateral bottleneck that is to be expected, the safest and most liquid instrument, US Treasury securities, are going to be faced with a rush of demand. In view of the longer-dated Treasuries having an extremely big short base, a short squeeze will likely follow, not just pushing yields much lower, but provoking a huge liquidation in other asset classes, especially equities, to pay for the margin and collateral calls and to cover the short positions to boot.

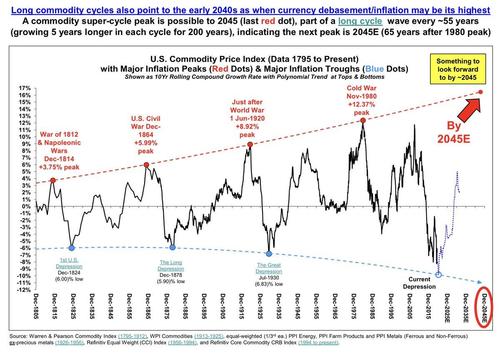

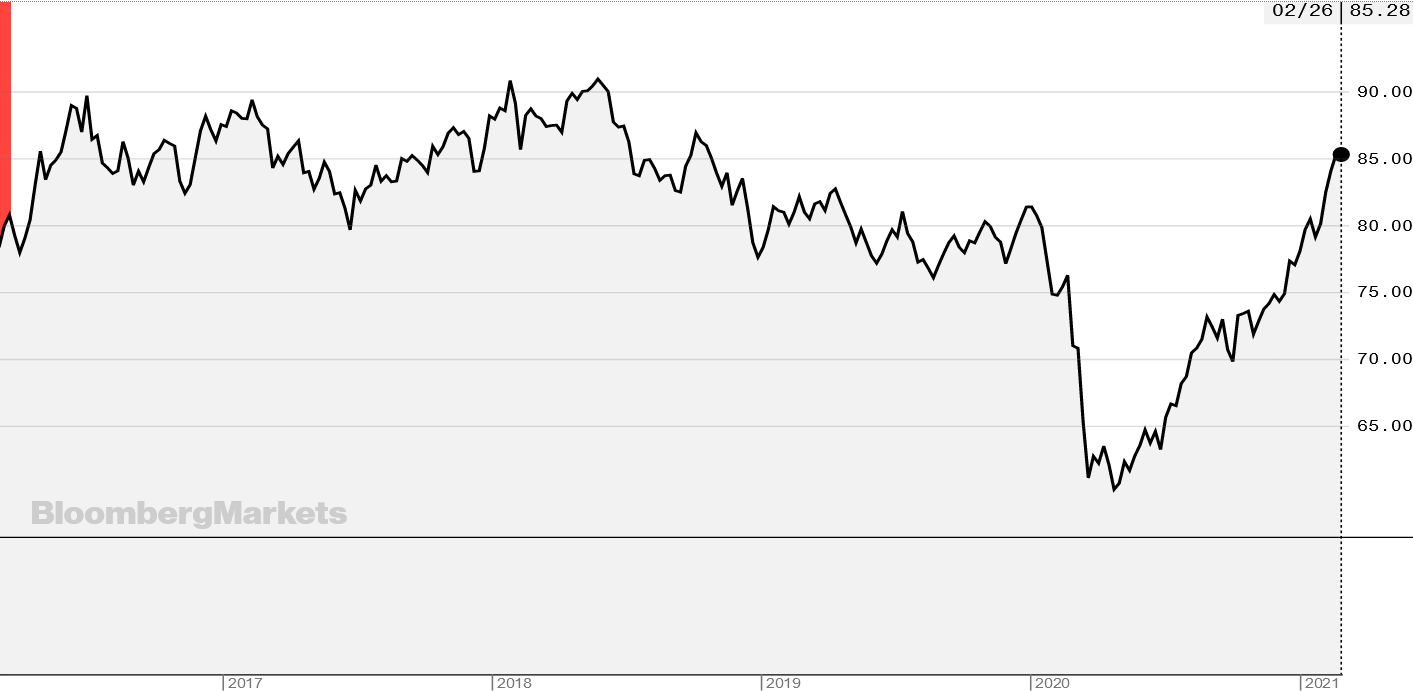

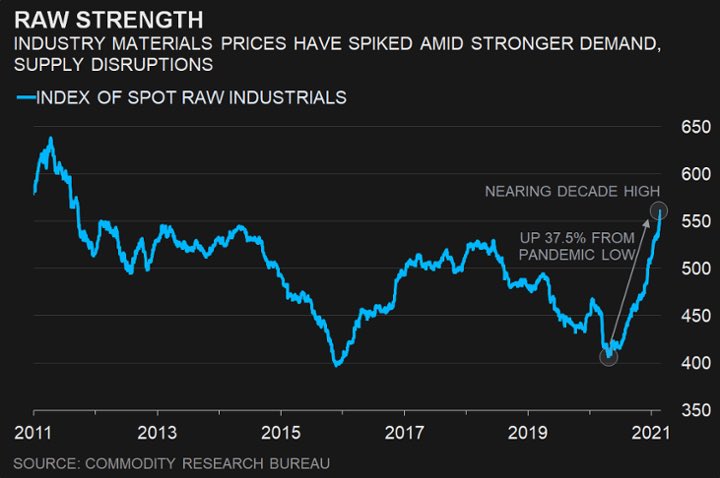

In relation to what was discussed before about the SLR and its implications for short-term rates/yields, there is a real and rather big chance that these will go negative (because of collateral shortage) and, more importantly, stay negative (on account of unrelenting demand for the most liquid instruments). Undoubtedly, such a background emerging is set to feed more vulnerability in the (global) financial system. To conclude, do not let yourself be surprised by a new crash in the following days. Seeing that there are all of these factors causing instability as we approach the notorious March bottleneck, the potential for some serious turmoil is certainly here. However, as I stated in the beginning, a correction rather than a financial crisis is what seems to be more likely to happen in the next few days. Considering that markets participants will gradually awake up to reality and realise the economy is not recovering, with households and businesses going through terrible financial distress, whether the next financial crisis crops up this month or not is immaterial. What is important to understand is that, in all likelihood, one is bound to befall on the world in the near future. For almost four months, since the honourable and ultra-charismatic orator Joe Biden rallied a record number of voters (that even raised the dead), to get fascism and white supremacy out of the White House, and the discoveries of vaccines for the kung-flu, sentiment on the part of pretty much everybody has improved. On the one hand, the vaccines "injected" a sense that life would return to normal, the "old" normal, and not stuck in this twisted and abhorrent "normal" we have been told to be necessary (to flatten the curve, not to kill granny, or something like this). On the other hand, as the medical community was on a crusade to find the vaccine, the stimulus and financial aid which were going to be put together by governments, especially the ones engendered by the Biden administration and the soon-to-be Democrate-controlled Congress, were aimed at supporting the economy so that the house of cards would not collapse in the meantime. As a result, and because of the public's reverence for technocrats to boot, (most) markets began to price in an economic recovery, or at least the initial steps of one, as businesses started to perceive a better economic outlook than previously surmised, albeit households do not appear to share the same view. To wit, some of the markets that have been hinting at recovery more strikingly are the commodities. Although that is what some analysts take from them, are commodities really suggesting an inflationary boom? Are the "Roaring 20's" staging a comeback? Among the financial institutions which take this view there are JP Morgan, Bank of America and Goldman Sachs. In their opinion, the commodities secular rally will be a story of post-corona-phobia economic recovery, as well as "ultra-loose monetary and fiscal policies". In addition, commodities may also jump as an unintended consequence of the fight against climate change, which threatens to constrain oil supplies while boosting demand for metals needed to build renewable energy infrastructure and manufacture batteries and electric vehicles, namely cobalt and lithium for example. Furthermore, commodities are typically viewed as a hedge against inflation, which has become more of a concern among investors. In the end, as if we are in some post-war period in which there is a large-scale effort to rebuild what was destroyed, owing to tremendous demand, prices of raw materials are going to skyrocket for the next quarter of a century, following the depiction below.  For now, commodities' prices have indeed surged since the lows of the March Meltdown, having even reached multi-year highs, as the next couple of charts show. In spite of the rally in the Bloomberg Commodity Index (top graph) seeming to be somewhat extraordinary, its performance pails in comparison to the one in the Index of Spot Raw Industrials (bottom chart). By taking a look at this, it makes you wonder if the inflation spigot has been tapped at last.   Notwithstanding, on Friday, February 28, "[t]he return on commodities as measured by the 23-member Bloomberg Commodity Index dropped the most since April as a strengthening dollar reduced the appeal for raw materials priced in the currency. Meanwhile, a surge earlier this week in US government bond yields has fed into increasing concerns that accelerating inflation could lead to easing monetary policy support", Bloomberg reported. To begin with, as I have explained in the Eurodollar system series (see part I, II, III and bonus), rising UST's yields are indicative of improving financial and economic conditions (i.e. money creation is easy), which always happens after an economic contraction or just deceleration reaches its trough. Similarly, the US dollar falls in relation to its peers, particularly those in the EM domain, when growth prospects are favourable. Thus, affirming the accelerating inflation has arisen on account of the "accommodative monetary approach [(translation: low yields)] that helped fuel the recent price gains", having just in the previous sentence alluded to the recent uptick in the dollar, it tells you something is amiss. By turning our attention to the next graph on the left, the yield of the 10-year Treasury (orange line), even though it has climbed quickly, meaning market participants are foreshadowing an improvement in the monetary landscape in the long-run, the copper-to-gold ratio implies much more pronounced growing expectations, albeit still short of pricing in the much-awaited recovery. On the flip side, seeing that the dollar, has not only stopped dwindling, but has, since this year broke out, gone up a bit, financial conditions have, according to the greenback, been getting uptight lately.

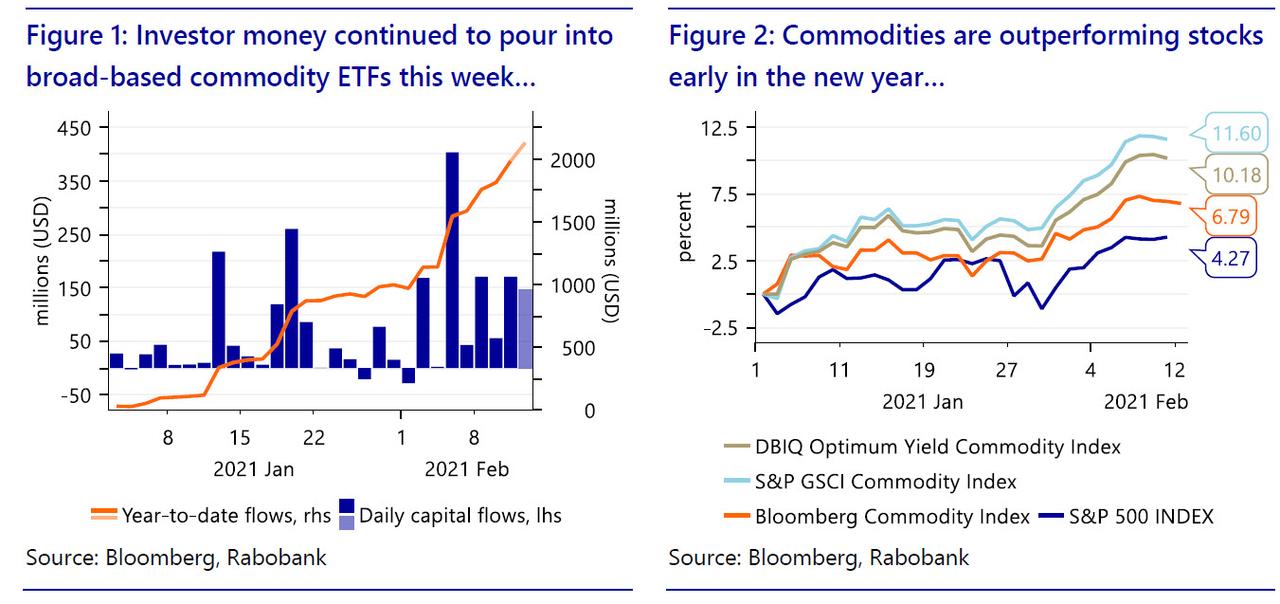

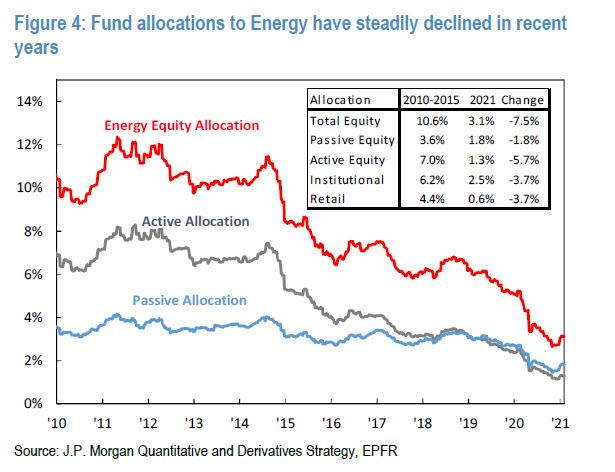

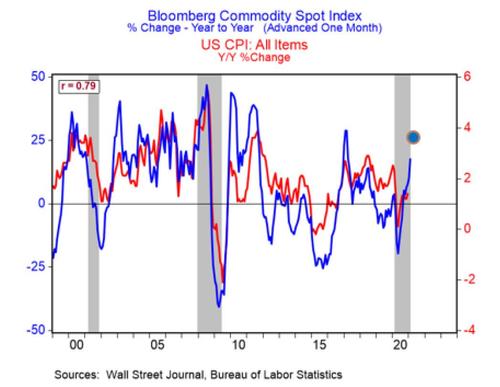

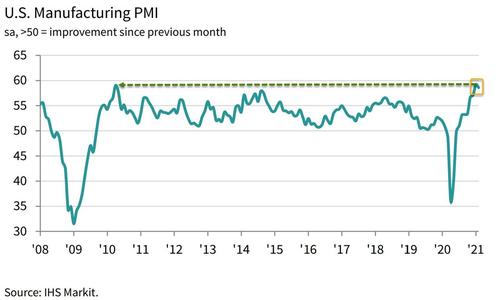

Hence, despite troubles in the present, a burgeoning economy awaits us in the (distant) future. As the saying goes, patience is a virtue. However, as they have demonstrated many times throughout the times, investors seem to lack several virtues, patience being one of them. Since the beginning of the year, investors have piled in the commodities realm (left chart), greatly contributing for the commodities' outperformance in relation to the stock market (right chart). Curiously, this current "mania" has, on the face of it, bucked the decade-long trend in energy fund allocations (bottom graph). If the supercycle in commodities is actually in the cards, then stocks like the energy sector are the bargain of a lifetime.   Moving on to the real economy, the soaring prices for raw materials have been taking their toll in the economy, probably causing more harm in the near-future. "Timber growers across the US South, where much of the nation's logs are harvested, have gained nothing from the run-up in prices for finished lumber. It is the region's sawmills (...) that are harvesting the profits", writes the Wall Street Journal. In fact, the glut of timber is so great "that mills are paying the lowest prices in decades for logs." Evidently, the corona-phobia, and the measures imposed because of it, has led sawmills to run "close to capacity", rendering them "unable to keep up with lumber demand." Moreover, according to Bloomberg, the corona-phobia "upended food supply chains, paralyzing shipping, sickening workers that keep the world fed and ultimately raising consumer grocery costs around the globe last year", leading to farmers, which for instance raise cattle, hogs and poultry, "getting squeezed by the highest corn and soybean prices in seven years (...) [lifting] the costs of feeding their herds by 30% or more." In the coming months, "higher price tags for beef, pork and chicken around the world" will be the consequence of producers seeing their profit margins being squeezed. The CPI is not going to reach YoY 4%, as commodities are suggesting on the next chart, in view of consumers lacking the purchasing power to sustain such an increase in prices. Because of mass unemployment, few jobs openings and poor wage growth, consumer demand is going to take some time to return to 2019 levels, which, by the way, was a terrifying year on account of being on the verge of recession. Therefore, retailers are only going to pass the higher costs to consumers when they can no longer squeeze their margins any further.  By the same token, the transportation segment of the supply chains have also been obstructed, mainly the shipping industry. The Shanghai Containerized Freight Index (SCFI), which represents weekly spot container freight rates (export) from the port of Shanghai, has a current reading which more than triple its levels in May of last year. Likewise, other freight indices tell a similar story. In a nutshell, the reasons are quite simple. For one, supply growth has shrunk considerably in recent years, with three major shipping alliances having become far more disciplined around capacity. Furthermore, recent supply chains disruptions from a lack of containers (boxes in the wrong place), the kung-flu (lack of staff), geopolitical tensions (China-Australia spat) and weather (US East Coast cold snap; and in Europe to some extent as well) have not helped matters either. Then, on the demand side, consumers have been propped up by government handouts and, more importantly, the vaccines coming online has, like I said above, led many to believe the pre-corona normality is returning in a jiffy. Therefore, due to being aware of these disturbances in the supply chains, companies have been preparing in advance, prompting them to acquire the supplies they need before these get jammed in traffic. Accordingly, the IHS Markit Manufacturing PMI figure, which came from 59.2 in January to the current 58.6, was wrongly buoyed by a substantial lengthening of supplier delivery times amid significant supply chain disruption. Ordinarily a signal of improving operating conditions, longer lead times for inputs reportedly stemmed from supplier shortages and transportation delays due to government-imposed restrictions. The extent to which wait times lengthened was the greatest since data collection began in May 2007. While orders remain nottably lagging, prices of inputs exploded to their highest since 2008 - when oil was trading at $140. As Chris Williamson, chief business economist at IHS Markit, stated, "shortages of raw materials have become a growing problem, with record supply chain delays reported in February, contributing to the steepest rise in material costs seen over the past decade", leading to prices "charged for a wide variety of goods coming out of factories [being] consequently rising, which will likely feed through to higher consumer inflation."

So, we now know why commodities have spiraled lately. Regardless, there is very little backing this trend. For being chiefly caused by government-imposed hindrances because of the corona-phobia, these higher costs will come down as restrictions are lifted. Longer-term trends point to a cooling down for some materials. For starters, the energy transition that heralds a bright new age for green metals such as copper would be built on the decline of oil. Even producers of iron ore, the biggest market of mined commodities, expect prices to weaken over time as Chinese demand starts to decline and new supply comes online. On the coal front, there is an even bleaker outlook with producers looking to exit the market altogether, as the world switches away from the heavy-polluting fuel. Being the major beneficiaries of China's industrial expansion that resulted in the last commodities supercycle, iron ore, coal and oil prospects augur horribly to this conjectured one. On the oil front, prices have recovered as demand rebounded more strongly than many had expected, after reaching the never-imagined $-42 per barrel. Early in 2021, the Organization of the Petroleum Exporting Countries (OPEC) and its allies were holding back crude equivalent to about 10% of current global supply. Long before that, market fundamentals have shifted, especially in the US with the emergence of shale oil. Ergo, haunting traditional producers is the prospect that a prolonged period of high prices would trigger a new flood of supply beyond OPEC’s control, pulling down prices. Despite copper being on a tear in early 2021 thanks to rapidly tightening physical markets as governments plow cash into electric-vehicle infrastructure and renewables, insofar as the iron ore, coal and oil markets dwarf copper in scale, the crank up of its usage along with other methals like lithium and cadmium are going to have an extremely limited impact on the broad commodity basket. To cap it all off, while agricultural commodities have their own particular dynamics, soybeans and corn have rallied to multiyear highs, driven by relentless buying from China as it rebuilds its hog herd following a devastating pig disease (African swine flu). Owing to being more dependent on global economic and population growth, rather than the decarbonization trend underpinning excitement in metal, agricultural commodities have very weak fundamentals to justify prices these high as the world moves forward from the kung-flu. Finally, it is not stimmy checks sent by Uncle Sam, or any other government for that matter, that are going to enkindle the much-anticipated inflationary conflagration. Because individuals sense, and rightly so, the government aid is temporary and inconstant, they are not spending money in proportion to what they are gaining in income, as the next graph shows. As soon as individuals start seeing their bank accounts balloning through their own endeavours in the economic system, as opposed to handouts from the political system, consumption will pick up, although that is naturally taking a lot of time to ensue. Nevertheless, one thing is for certain, as long as society holds this collectivist mindset that is beholden to politicians and technocrats, an economic boom, worthy of this designation, will never happen and, thus, a commodity supercycle will have to be deferred.  Hence, the question remains: what is super about this? As it is usually the case, investors' and analysts' short-sightedness, of course.

|

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed