|

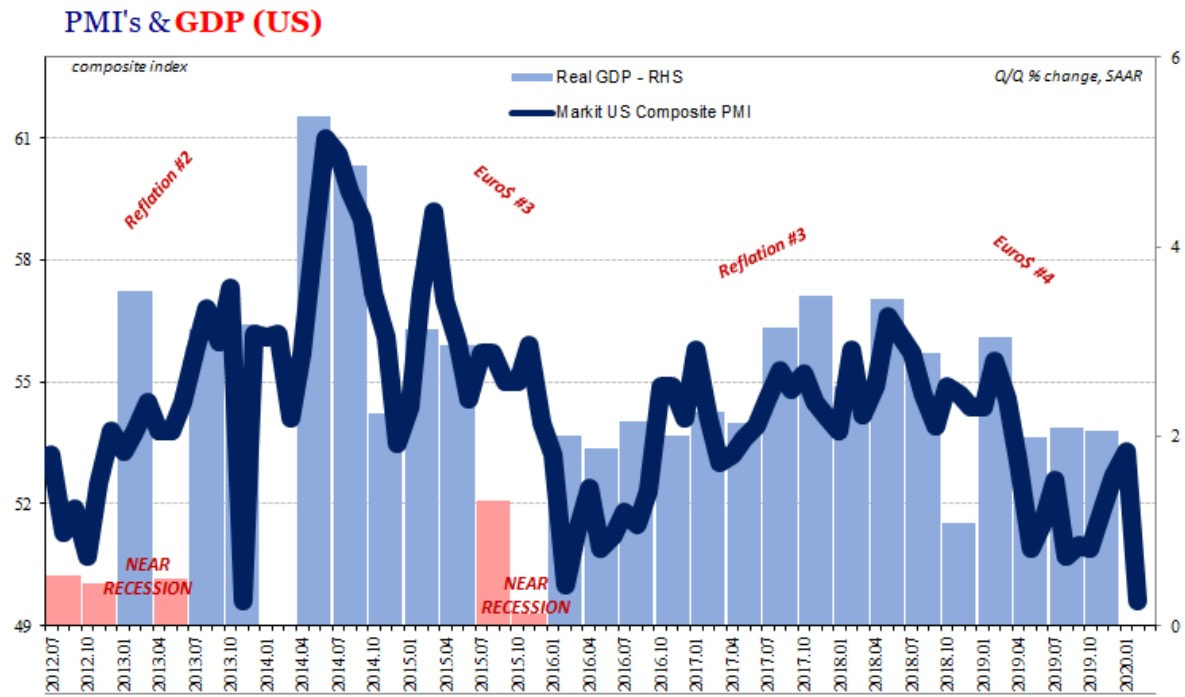

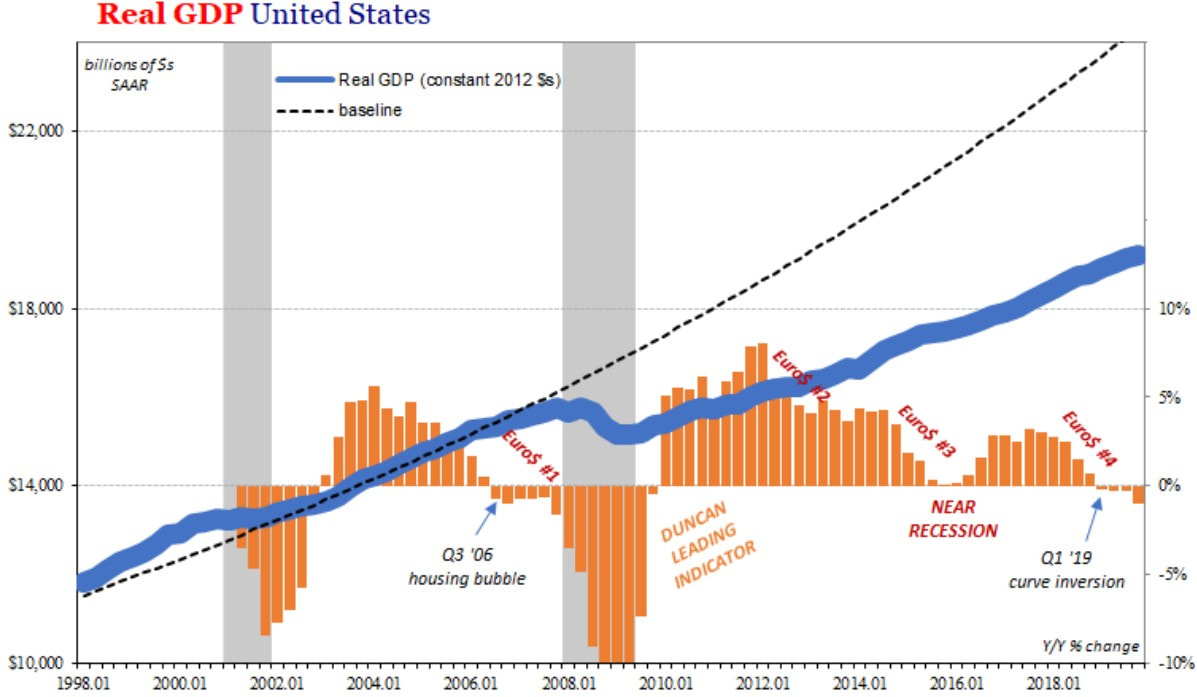

Picking up on the analogy presented on the second part's introduction, the Eurodollar system's liver has been severely impaired ever since the GFC. With the current financial meltdown that is bound to be of greater magnitude than the 2008 crisis, the liver will collapse at last. If a transplant does not follow, then the patient will die. In this last part of the series, I am going to delve into the various aspects surrounding the crash, why it should have surprised nobody, and whether it is over or just beginning. As I explained on part two, starting on early 2018, some signals of rising financial tightening were appearing, like soaring repo rates above the EFF rate and the dollar appreciating. Those signals began to materialise very soon on the GDP figures. Looking at the graph on the left, the PMI had been dwindling since the second quarter of 2018. The GDP, historically, has been following the PMI. Therefore, the PMI is a good indicator of the economic performance, depicting the health of the economy before the GDP statistics finally come out. An even better prognosticator of near-term economic activity is the Duncan Leading Indicator (DLI). As the name suggests, this indicator is a harbinger of future economic performance, signaling a contraction or recession for several quarters in advance. The DLI is the ratio of consumer durables spending plus residential and business fixed investment to final sales, with all data adjusted for inflation. Final sales are defined as the gross national product less the change in business inventories. As a result, the indicator is the ratio of the cyclical components of expenditure to GDP, except that the change in business inventories has been subtracted from both the numerator and denominator.

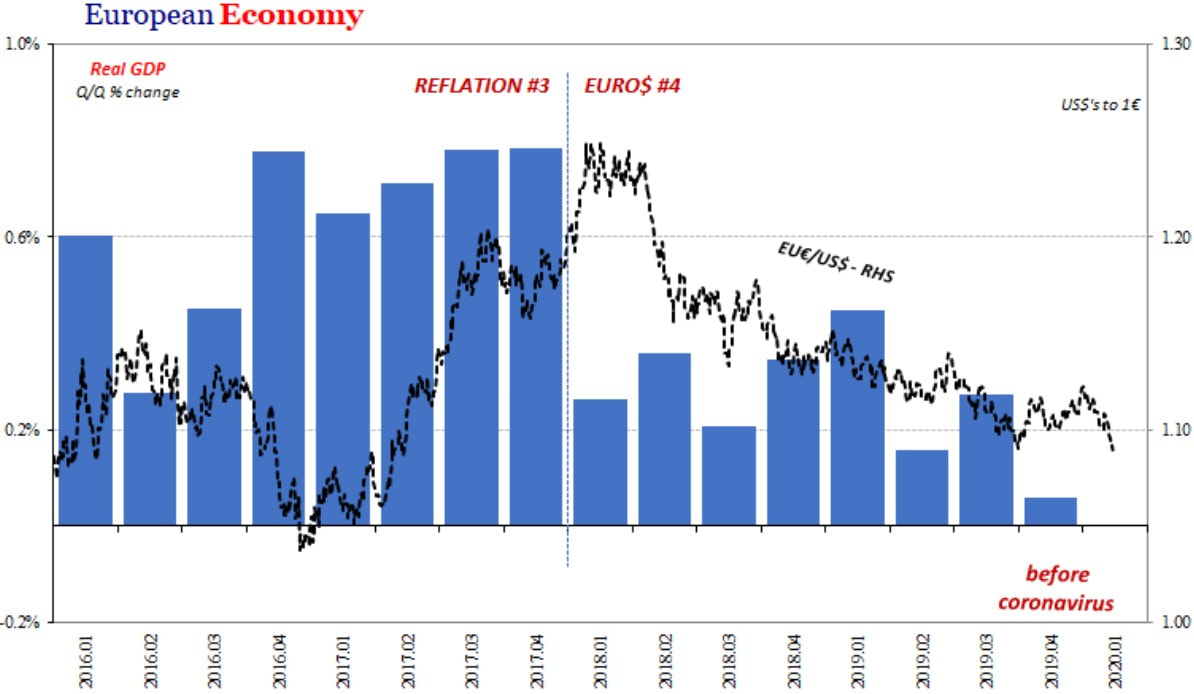

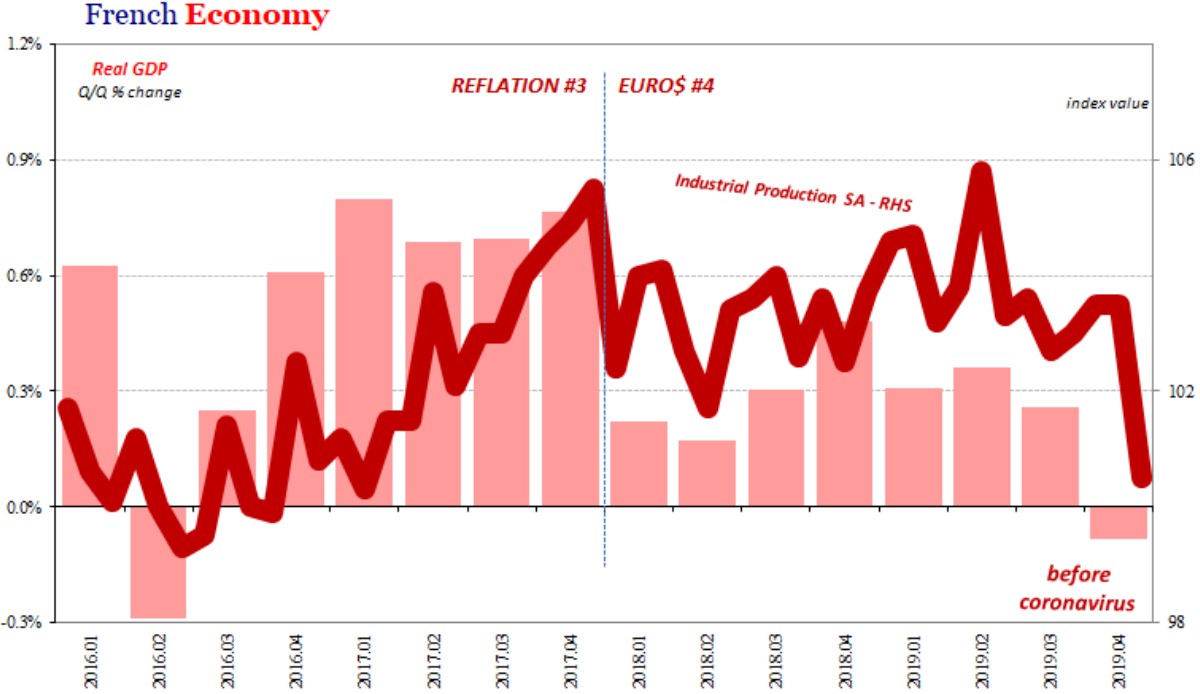

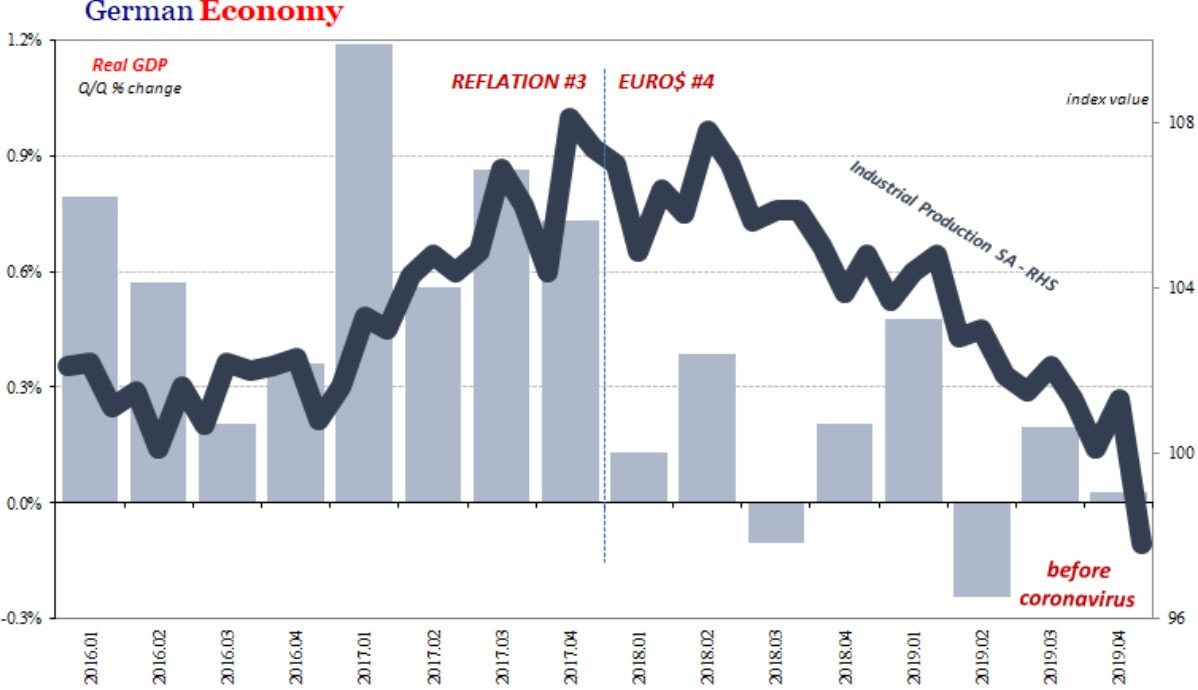

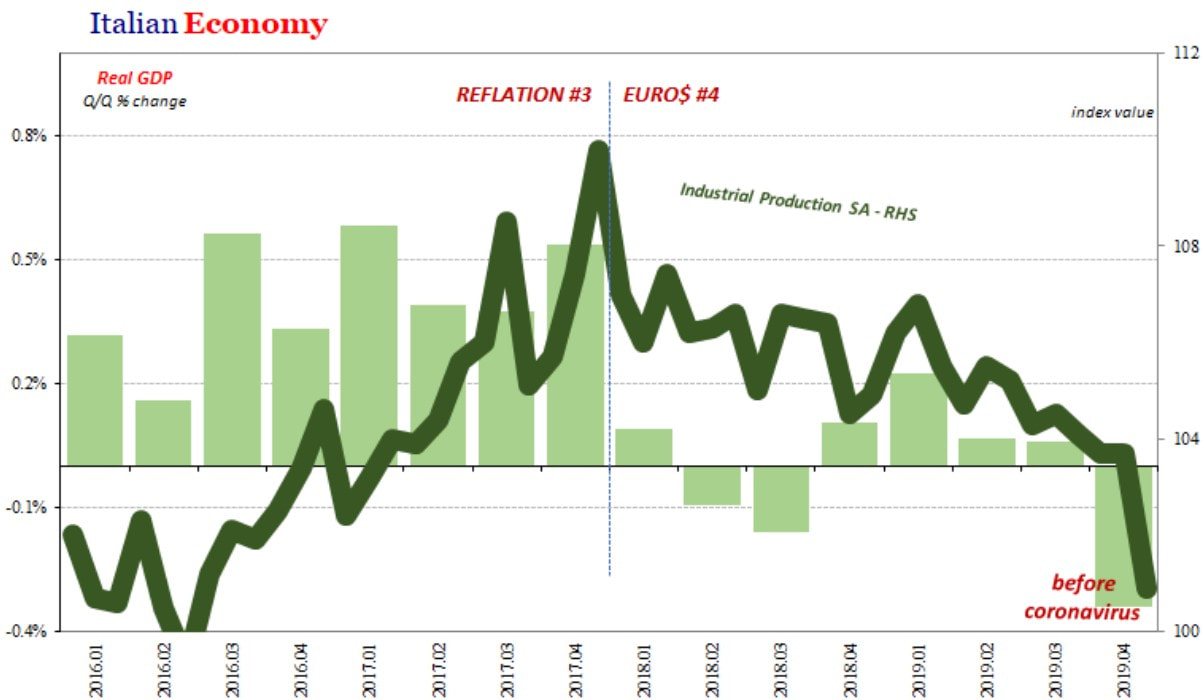

Hence, the US economy's check engine light had been flashing for more than a year, which means it could have broke down in the middle of the road at any given time. Instead, it got hit by an eighteen-wheeler truck. The evidence of a slowdown was far greater in Western Europe. From 2018 onward, the three biggest economies have struggled to increase industrial production. Although, Germany and Italy had shown no signs of a rebound throughout this time frame, France had presented some promising figures up to Q2 2019, joining the rest of the pack thereafter, having posted a negative value for the final quarter of last year, just like Italy.

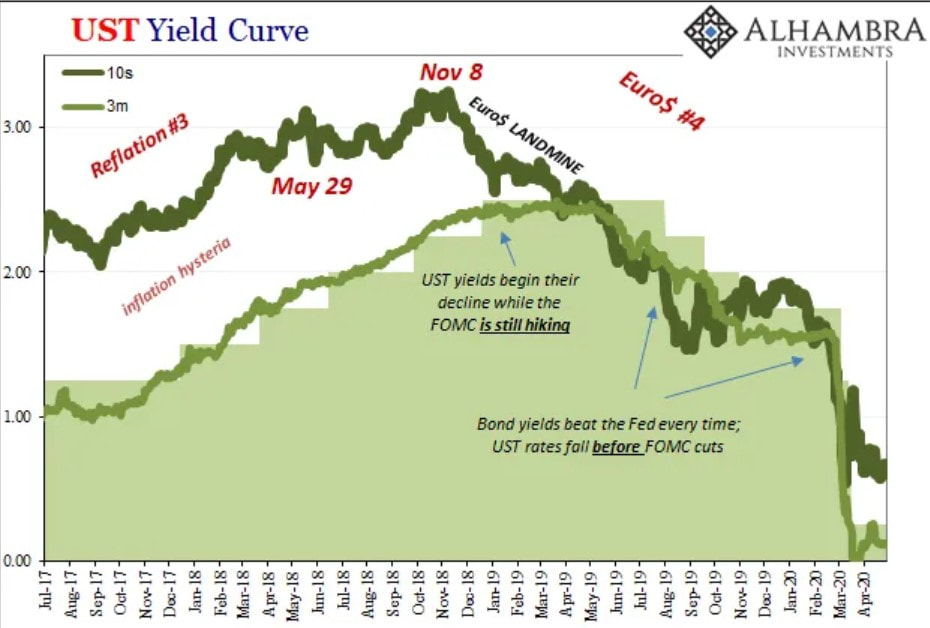

Furthermore, since late 2018, the yields of the US Treasuries had been transmitting, to those paying attention, that the financial state was decaying, which precipitated the central bankers all around the world to ease their monetary policies. Let's not forget this occurred long before the word coronavirus being bombarded on every news and social media outlet. Hence, the developed economies were set for a recession sooner or later - again, it would have broken down in the middle of the road -, dragging the emerging markets with them. For some reason, almost everybody was gobsmacked by the financial debacle that took place in March. However, the financial markets, as I said, were shouting that financial conditions were deteriorating and that commerce was going to wane down, more than a year ago.

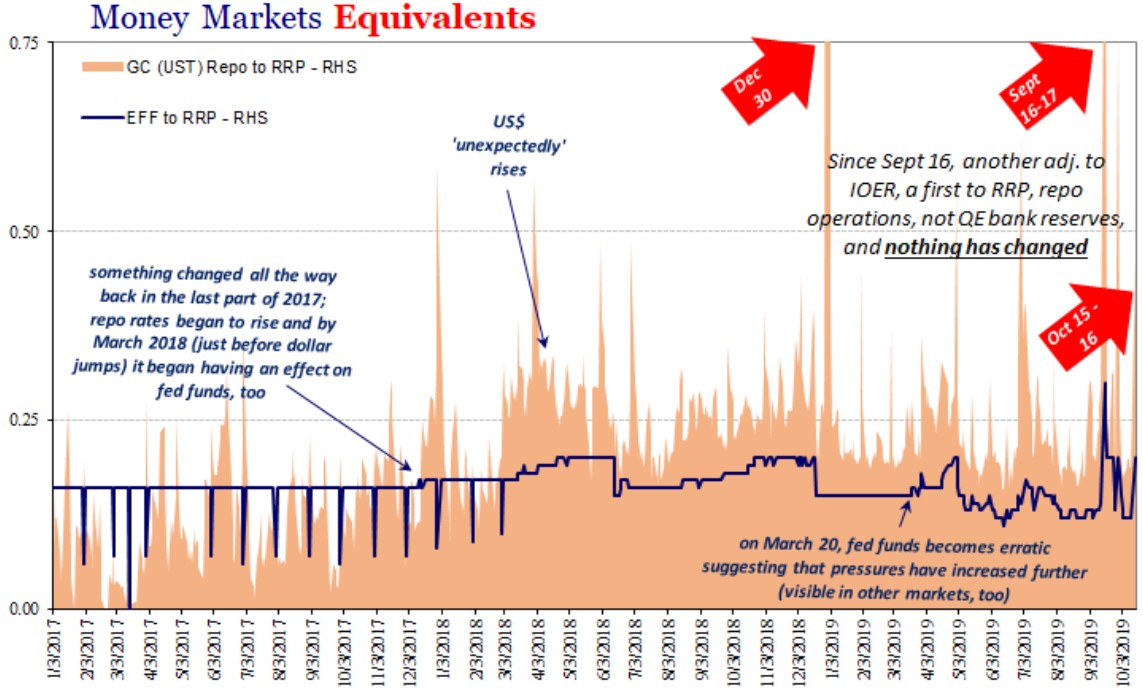

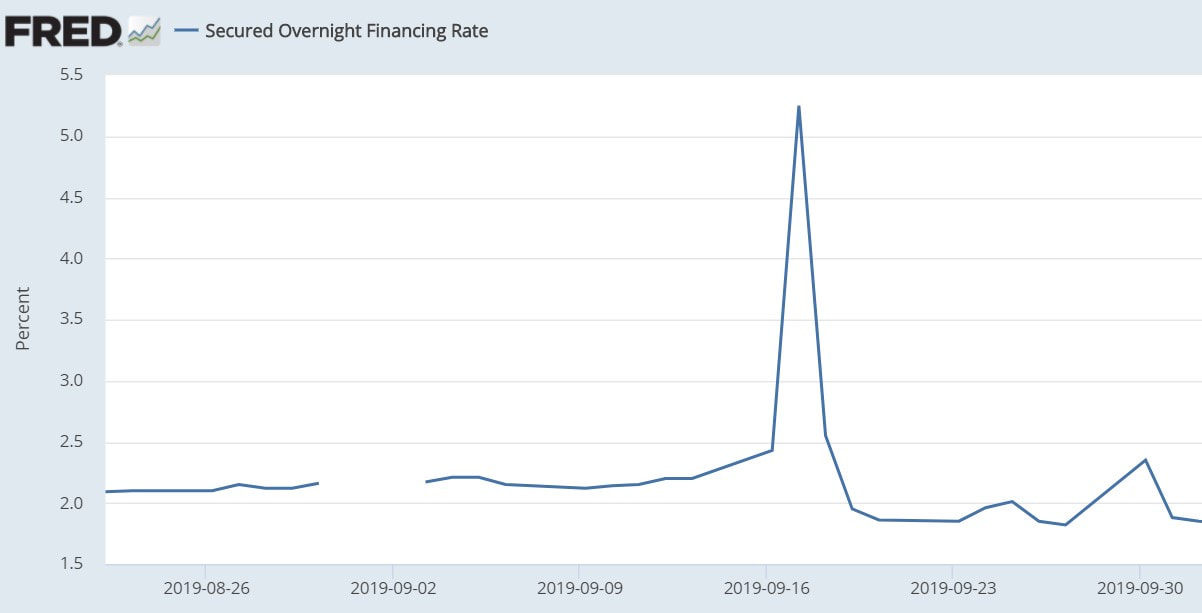

Moving on to last summer, on July 31, the Fed cut interest rates targets (for the EFF) for the first time since December 2008. As the graph above on the left demonstrates, the FOMC was forced to reverse their hiking course and embark on easing efforts, due to declining Treasuries yields. The 10-year tenor hit its dip in September, which happened to be when the "repo-calypse" began. Accordingly, the already erratic EFF rate jumped, and the GC repo rate and the Secured Overnight Financing Rate (SOFR) - broad measure of the cost of borrowing cash overnight collateralised by Treasury securities - spiked tremendously. These fluctuations of rates only calmed down when the Fed interjected. So they want us to believe. In reality, the actions undertaken by the Fed were only smoke and mirrors. The adjustments on the interest rate on excess reserves (IOER) and the reverse repurchase agreement rate (RRP), the "temporary" repo operations and the comeback of the beloved quantitative easing, though Jay Powell and his pack emphatically stated it was not QE, were simply a sleight of hand. The truth is that the markets soothed themselves (only slightly and for awhile).

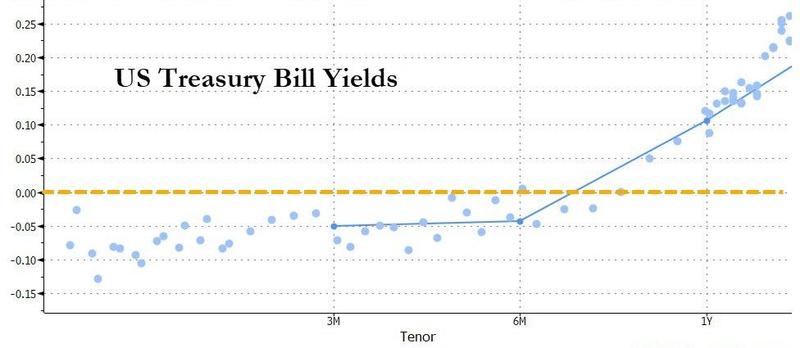

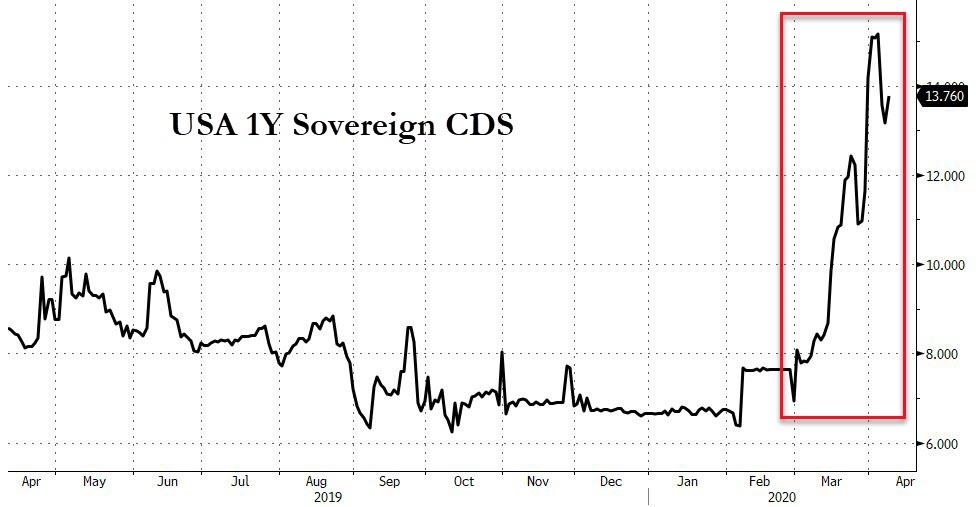

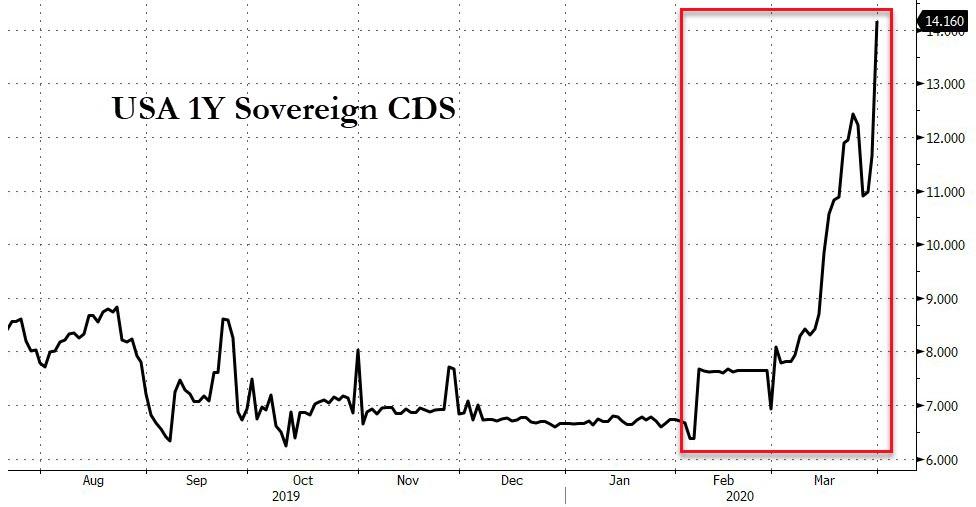

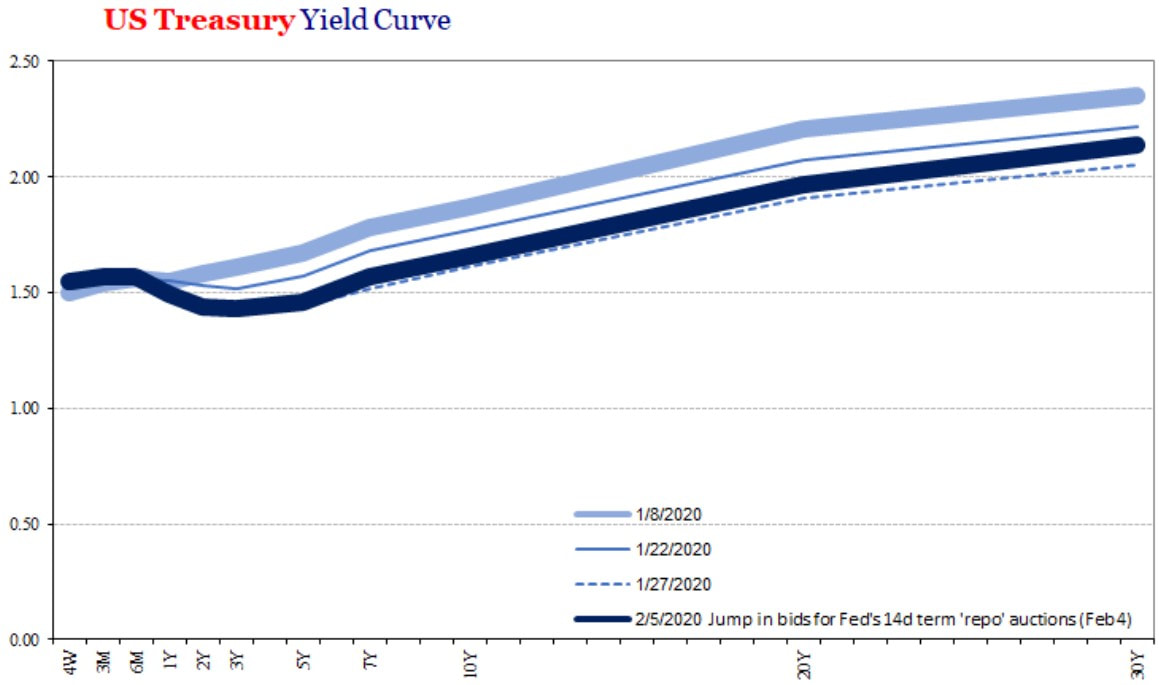

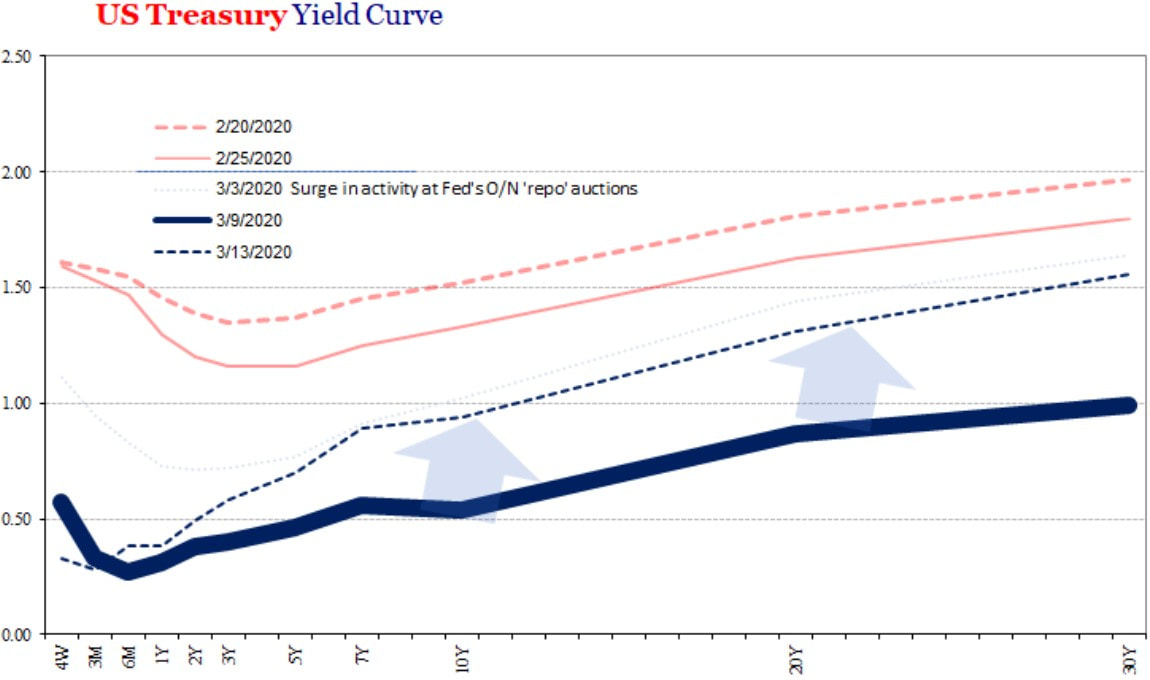

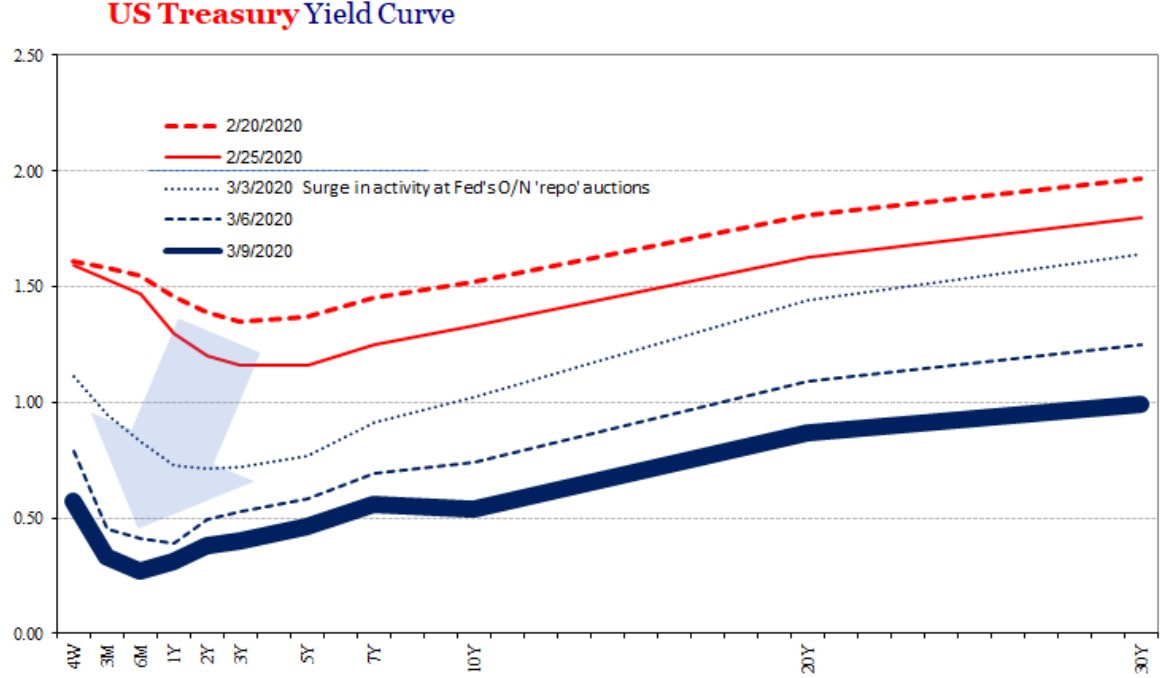

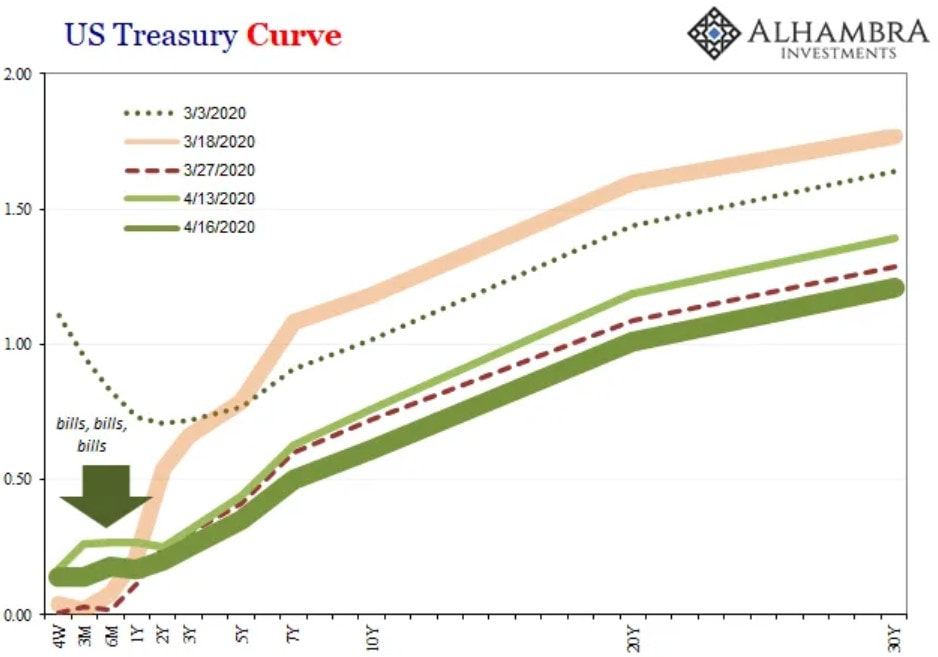

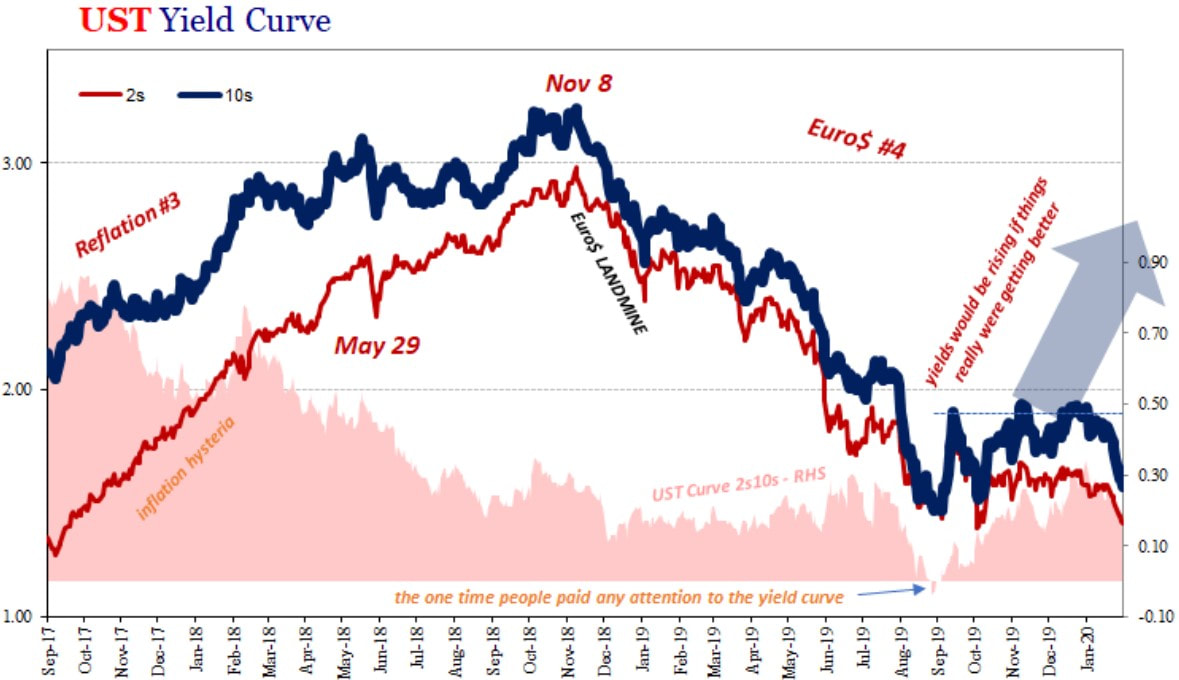

With COVID-19 entering the picture, the already frightful scenario got much worse very quickly. The yield curve was inverted once again by the end of January, when the kung-flu was only a Chinese affair. Then, from February through early March, the whole curve gradually subsided, indicating, as you know, a slipping economy and, consequently, the falling apart of the financial conditions. Subsequently, during the worst part of the financial turmoil, in mid-March, the T-bills' yields (maturities of a year at most) remained close to the zero bound, while the other yields, of the notes and bonds, climbed till the end of the markets' sell-off in March 23, steepening the curve substantially. Afterwards, the short-end increased a little bit and the long-end dropped close to early March rates and so it remains to this day.

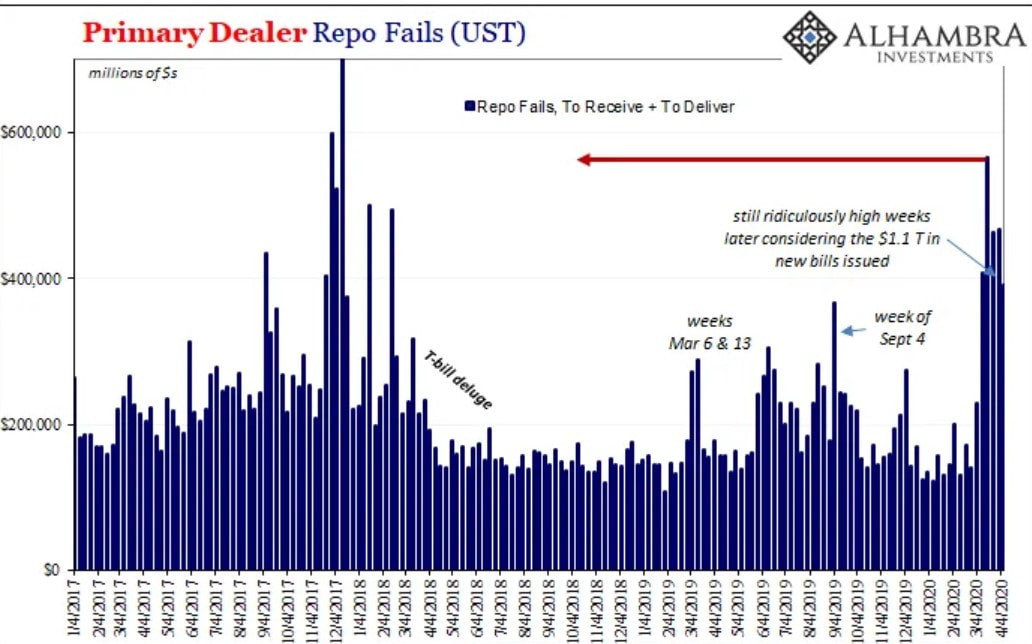

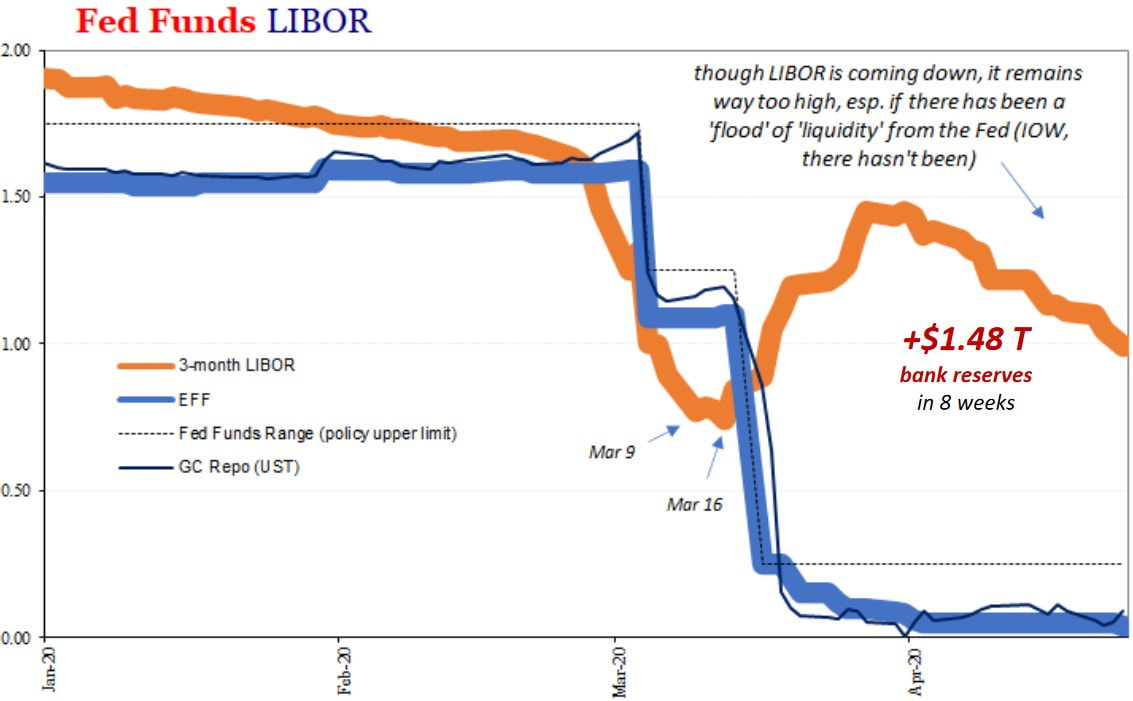

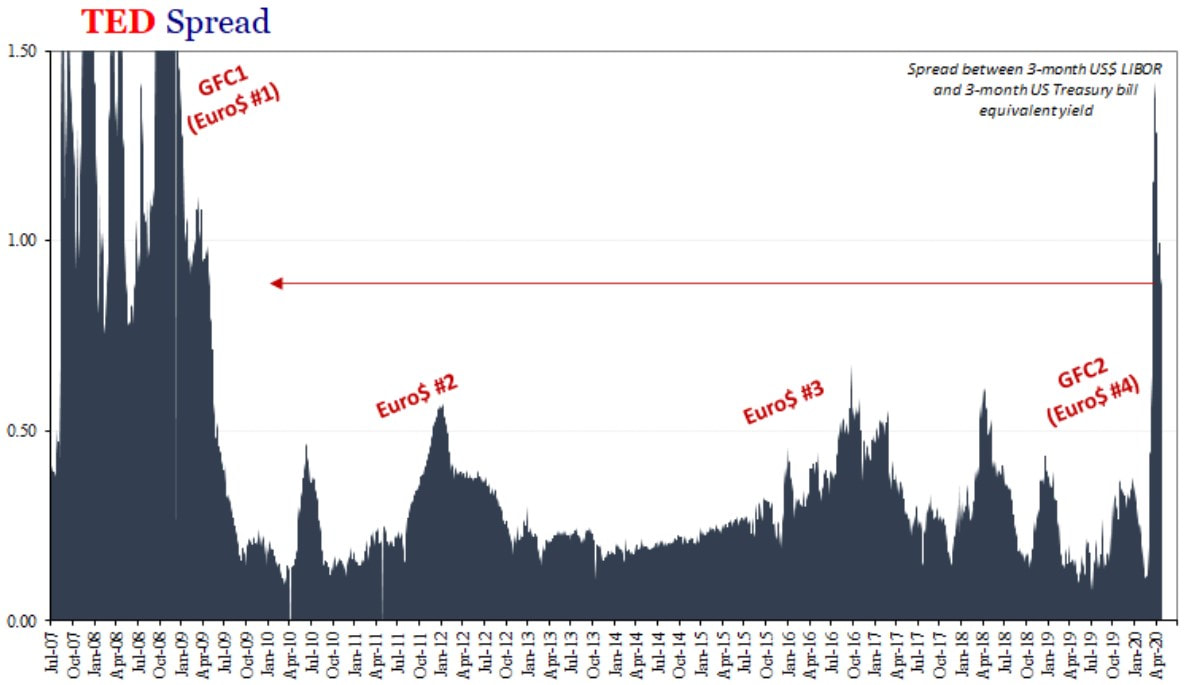

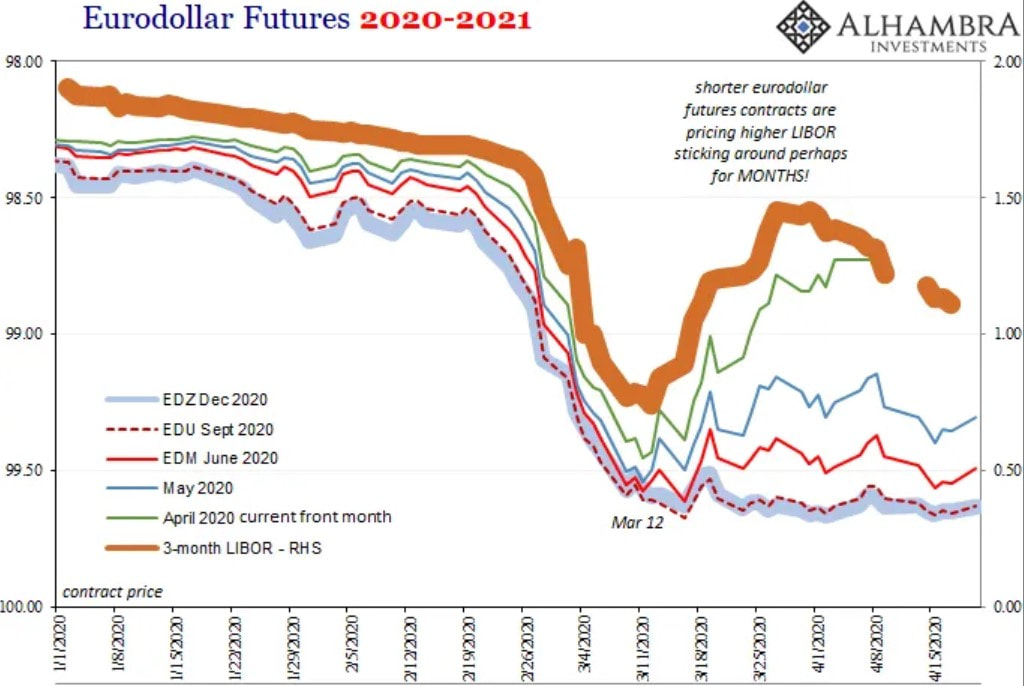

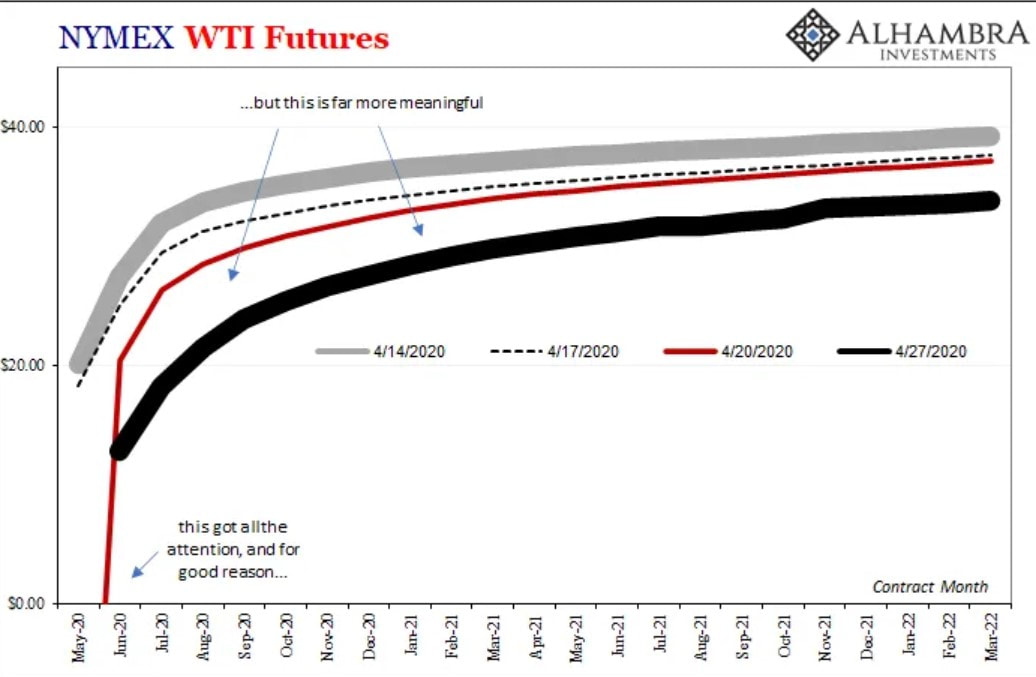

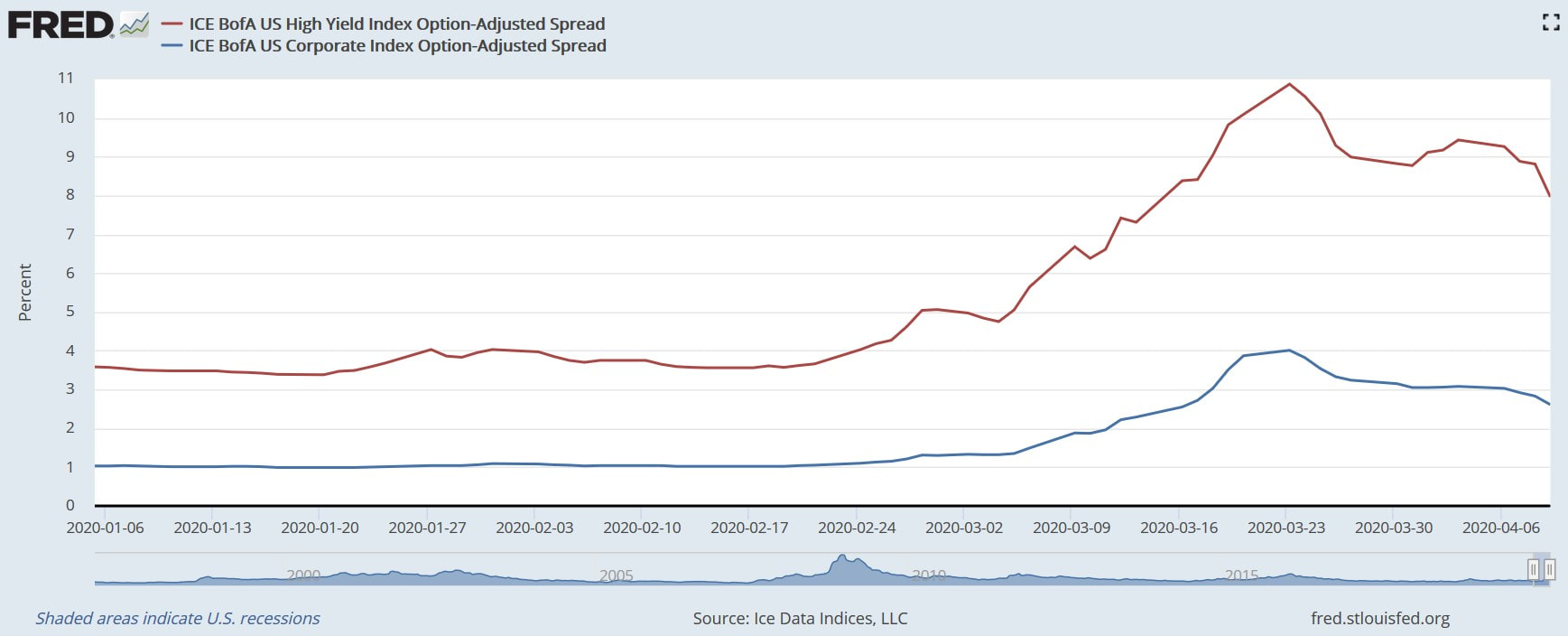

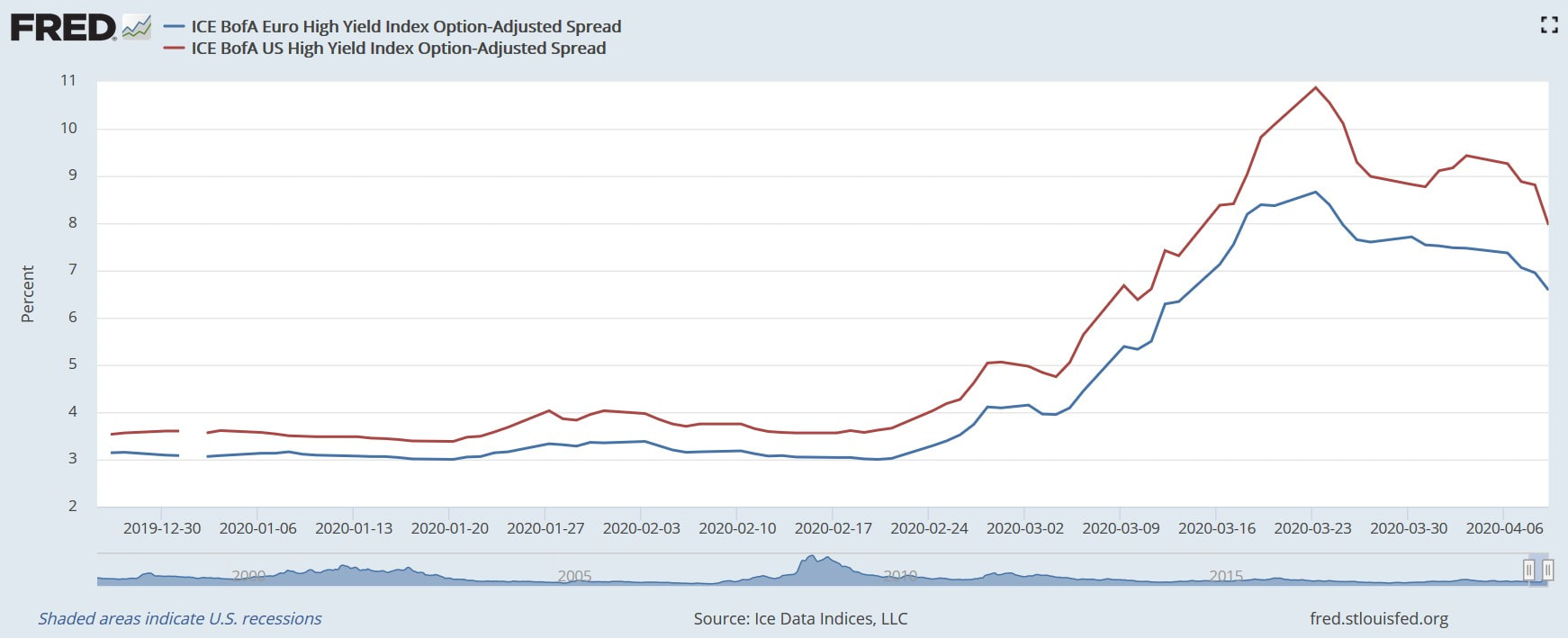

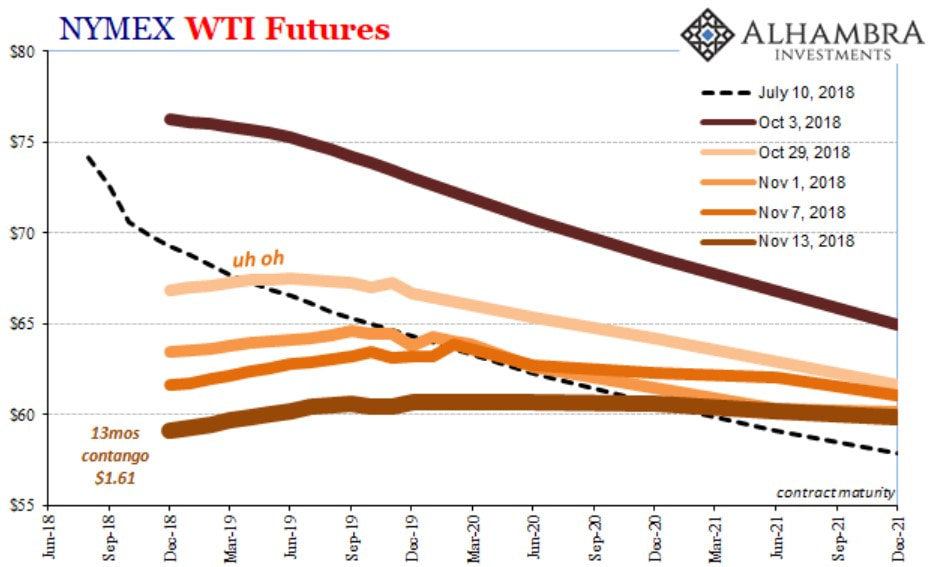

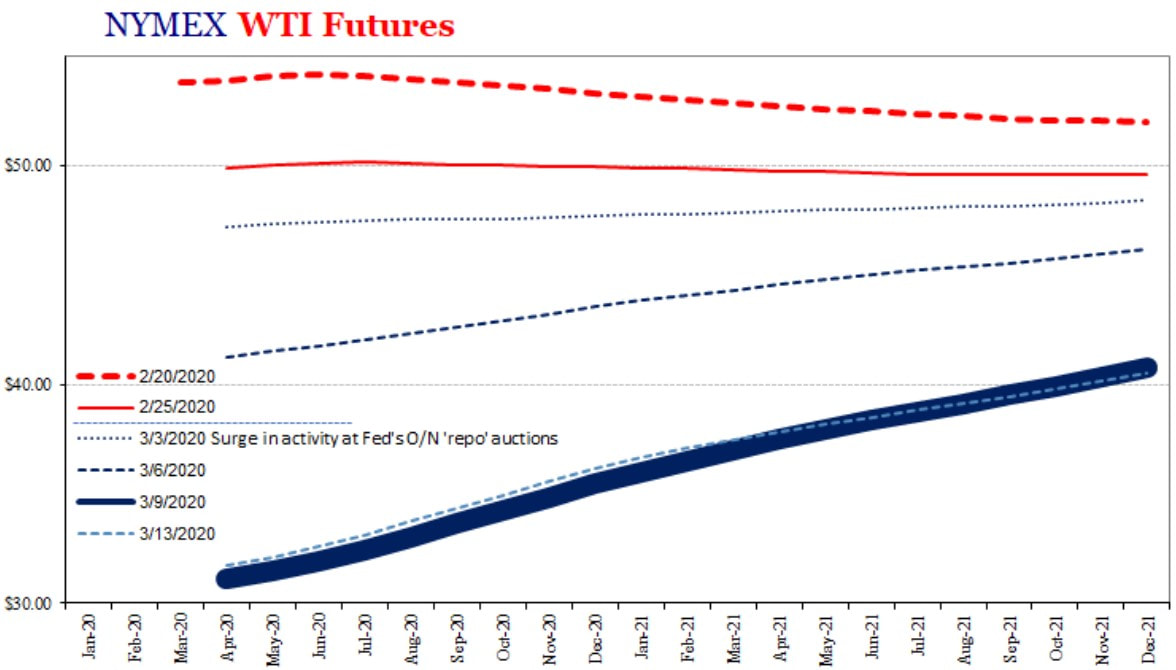

Similar to the GFC, which I exposed in part one, during this financial panic, there is a run on "cash". Despite the cash lenders having funds available and the financial institutions with funding needs having collateral to exchange for liquidity, the lenders became extremely picky on the eligible collateral. Previously accepted assets, such as CLO and other ABS, corporate bonds including HY, and even equities, were blacklisted by the lenders. These became so cautious that they were only taking collateral of the most "pristine" kind. Consequently, everybody tried to get the crème de la crème collateral, the T-bills. This makes their prices to surge and, therefore, their yields to plummet. Throughout the worst period of the meltdown, these yields turned negative, as the next graph portrays.  Likewise, the amount of repo fails, which are the repurchase agreements that do not come to pass, skyrocketed in the middle of March and have remained in high levels ever since.  Inasmuch as the variety of eligible collateral was immensely reduced, market participants had to get liquidity selling assets, specifically the ones denominated in US dollar, to meet their obligations, whether it was debt servicing, margin calls, payroll expenses or any other routine expenses. No asset class escaped the fire sale liquidations, except the T-bills. Paradoxically, gold, which is viewed as a safe-haven in episodes of financial trouble and, consequently, was expected to have soared, it joined the others and plunged too. Yet, since the crash climax on March 23, gold prices have recouped its ascending trajectory.  Additionally, another peculiar situation unfolded at that time that hardly went away. Whereas the EFF rate and the GC repo rate were dropping, the US dollar LIBOR went its own way, moving upward. On the one hand, the EFF rate decreased and has stayed low owing to the fact that primary dealers are tremendously well supplied with reserves and if there are depository institutions looking for funding but are deemed unreliable, the others refuse to provide them with the funds at any interest rate. As a result, because those risky institutions are left out from this market, the EFF rate does not express the financial health of its participants. Seeing that this rate is low, everybody thinks that the banking system is operating smoothly, when in fact the complete opposite applies. Similarly, the repo rate has been in very diminished levels, it even got lower than the EFF for awhile, which in normal times denotes a perfectly functional and liquid financial system. Obviously this is not the case. The reason is there was such a scarcity of eligible collateral that only the ones holding these (T-bills) could participate in the repo market. On one side, there are banking institutions with plenty of funds to lend, ergo there is a glut of supply. On the other side, a few institutions holding T-bills make up the demand. Therefore, the repo rate fell to near the zero bound. On the other hand, although the Fed has injected almost $1.5 trillion reserves in the primary dealers' balance sheets in eight weeks, the LIBOR, which depicts the willingness to lend and the perceived risk of shadow bankers operating in the London Eurodollar markets, shot up. Indeed, the participants of the Eurodollar system felt there was a lot of credit/counterparty risk in the system, regardless of the interventions pursued by the Fed.  In spite of the LIBOR having abated somewhat, it is still at a higher level since the end of the GFC. Looking at that crisis, the LIBOR lessened for long periods, with each spike upward being shorter than the previous one, making everybody believe that the worst had passed due to the efforts made by Ben Bernanke and fellow technocrats. Little did they know that the most horrible part was yet to come. So, you may be wondering if March was just the amuse-bouche and that the main course is yet to be served.  One way those doubts could be cleared is by checking out the Eurodollar futures curve. In a nutshell, these curves are indicating that the financial constraints will remain for awhile. In more detail, Eurodollar futures get settled in three-month LIBOR. Hence, it has an enormous potential to describe what participants are thinking about where the LIBOR will be at certain points in the future. Thus, the back-end of the curve expresses the participants' expectations of the liquidity conditions for next year and beyond. For that matter, it conveys their presumptions on the Fed's monetary policy to be enacted then and on the LIBOR as well.  Taking the oil market's signals into account, one could assume the Eurodollar participants are being overly sanguine, meaning that the main course is still being prepared. The relentless decline in the oil prices points to reduced demand, which reflects the anemic global economy that we are experiencing. One may think that this is because of the corona-induced economic shutdown and once the lockdowns are lifted the economy will return to its prior level in a jiffy. Although it is true that the present weak demand for oil was indirectly caused by the COVID-19, the oil futures are alerting to a continuously subdued demand (compared to the pre-virus paradigm) until at least March of 2022. This is not just about oil, this concerns the economic activity as a whole. Inasmuch as oil is by far the most used commodity in the world, for all kinds of industries, investors are speculating that the worldwide economy will not bounce back before for the following two years, at least.

Consequently, if these signals coming from the oil market do in fact transpire, even if just partly, the current financial woe will not have an end in sight. The market participants that comprise the Eurodollar system, whether they are governments, financial institutions, companies or individuals, with debt obligations (denominated in US dollar of course) will continue to struggle to come up with the needed greenbacks. Unsurprisingly, several countries in the emerging world will likely go through sovereign debt crises, once their reserves of US dollars reach a certain threshold. Some people au courant with these matters say that a Plaza Accord 2.0 will have to take place to prevent that massive crisis from hitting a big chunk of the world. Albeit this matter is a topic for another post(s), I take the view that the dollar shortage crisis in the emerging market realm may prompt the end of the dollar hegemony, giving rise to a new era where a neutral means of exchange will be the global reserve. One day, everybody, especially at the emerging bloc, is going to realise this system has, since 2008, benefited nobody because economic and, ergo, financial conditions have been severely hindered. Therefore, they will unite and demand for a new monetary system based on a neutral, fair and solid grounds. The outbreak of the current crisis and its spillover in the world have confronted us with a long-existing but still unanswered question, i.e., what kind of international reserve currency do we need to secure global financial stability and facilitate world economic growth, which was one of the purposes for establishing the IMF? In conclusion, the resentment felt by the emerging countries, and to some extent the developed ones too, towards the dollar privilege will lead in its collapse.

Moreover, the United States acting like a spoiled brat, as it has been - and it seems to get worse by the day - since their currency gained the global reserve status, it only helps speeding up the process of abandoning the dollar. During this crisis, the US government is embarking on a spending spree to rescue businesses and individuals and to keep markets afloat. As a result, the national debt is shooting to the moon, while the output growth becomes negative and anemic in the foreseeable future. To pay for all of this, the Fed simply introduces QE infinity, ZIRP and a myriad of alphabet soup programmes. Accordingly, when the whole world stops considering the US dollars as a global reserve currency, there will be nobody to absorb that flood of US dollars, except the American people. As a final remark, this does not augur well for America.

0 Comments

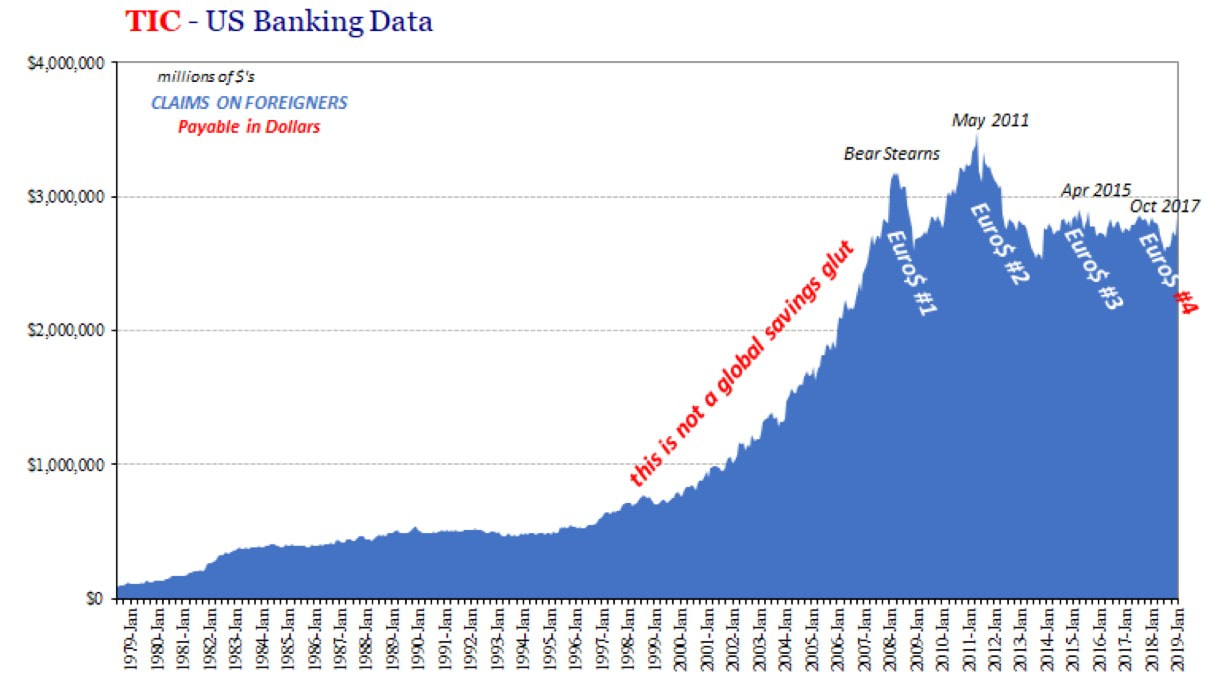

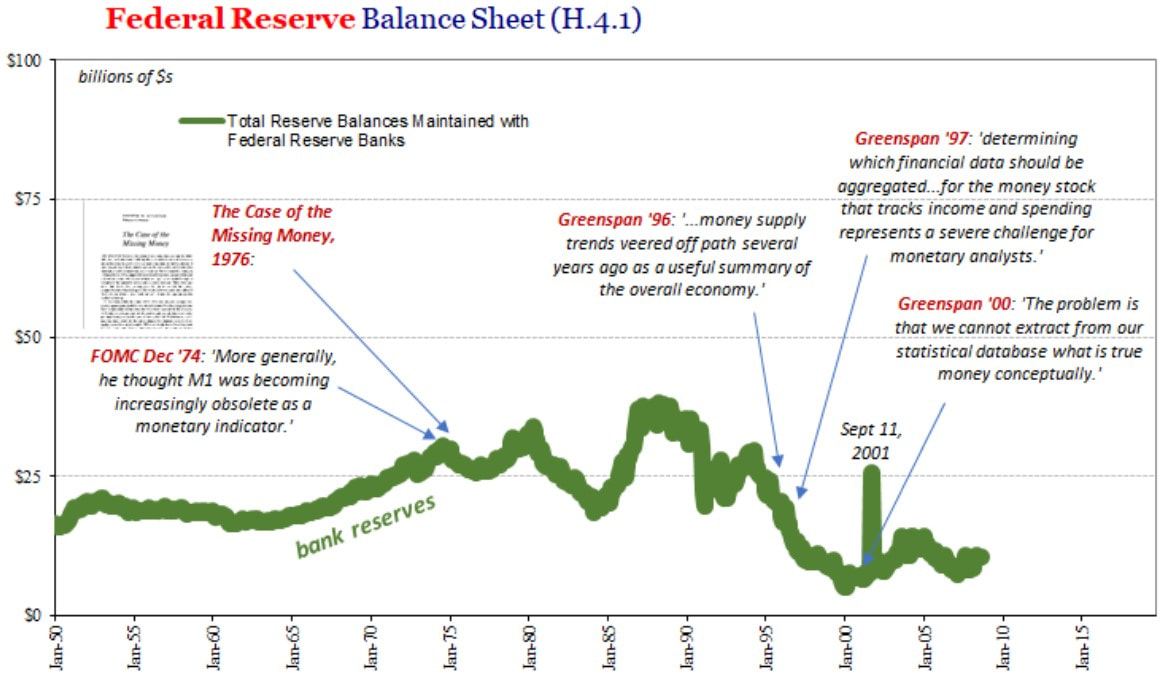

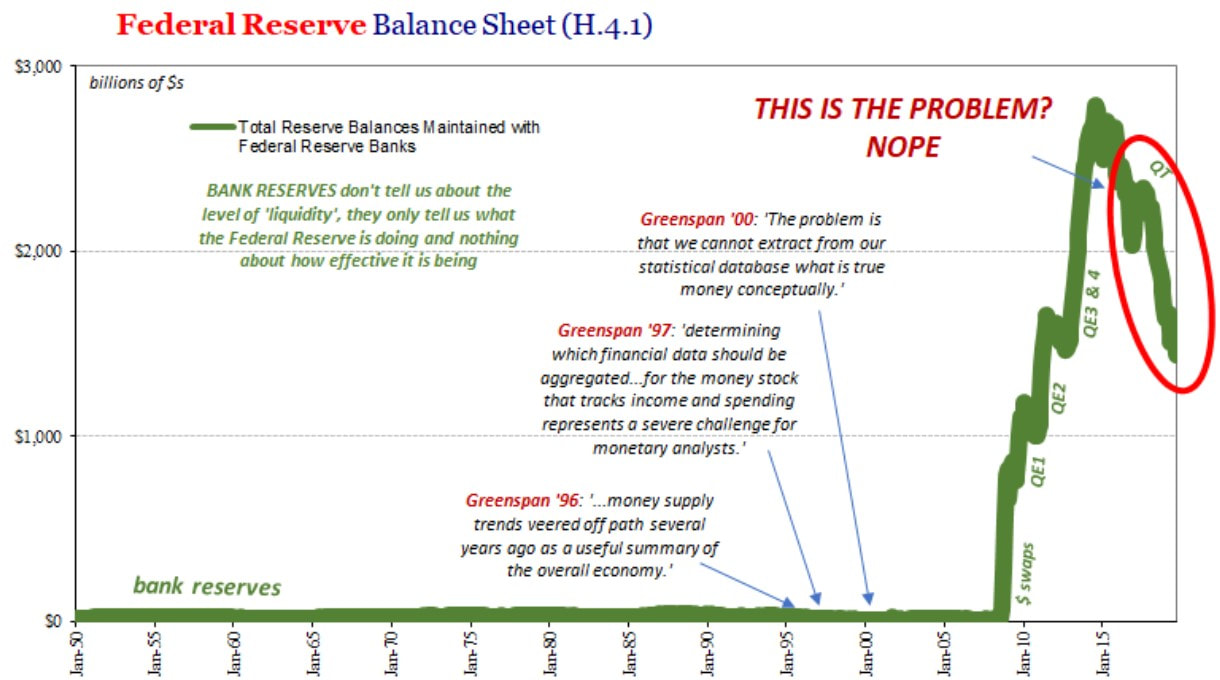

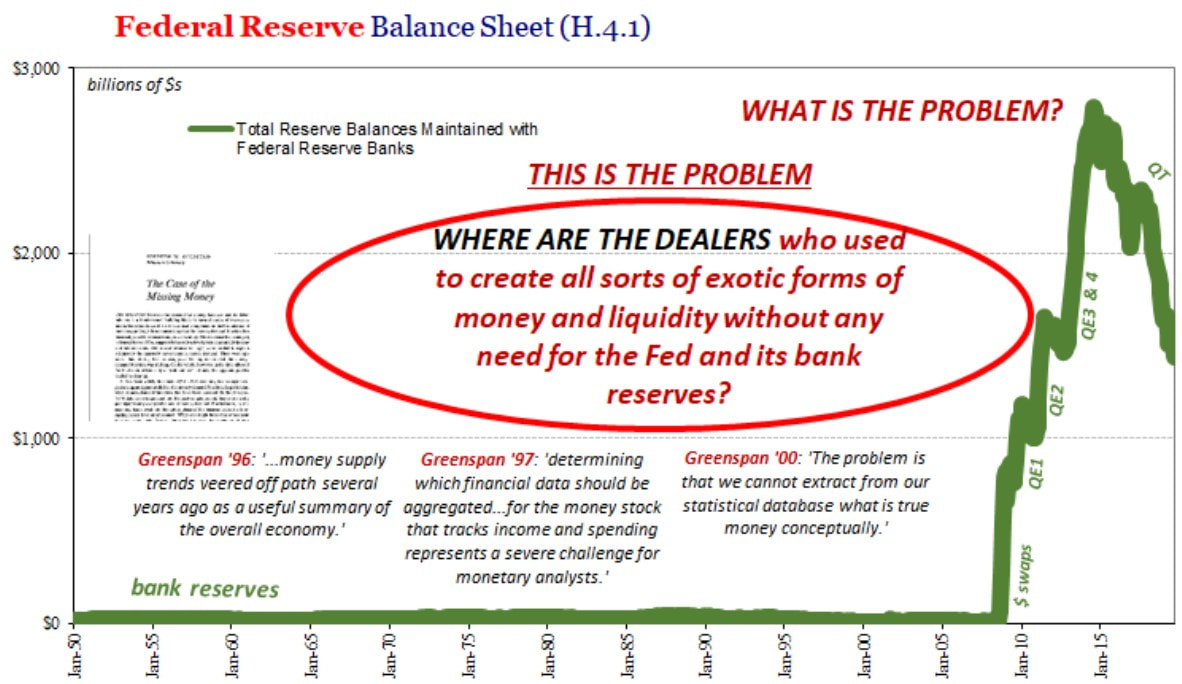

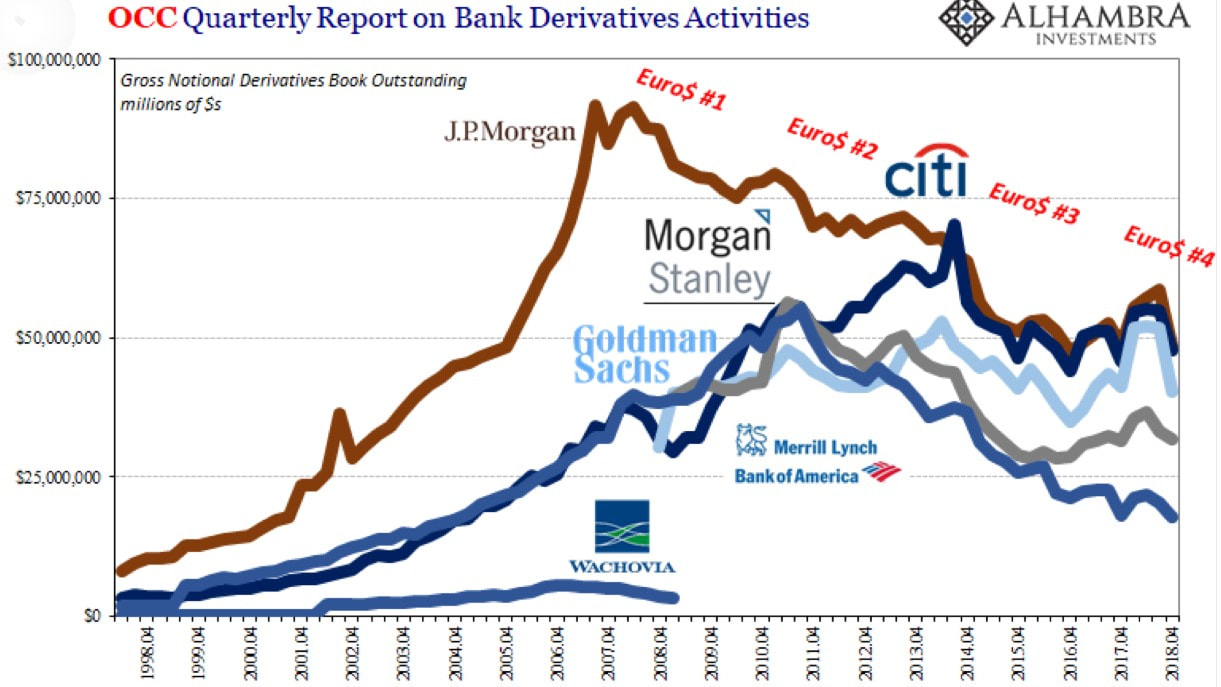

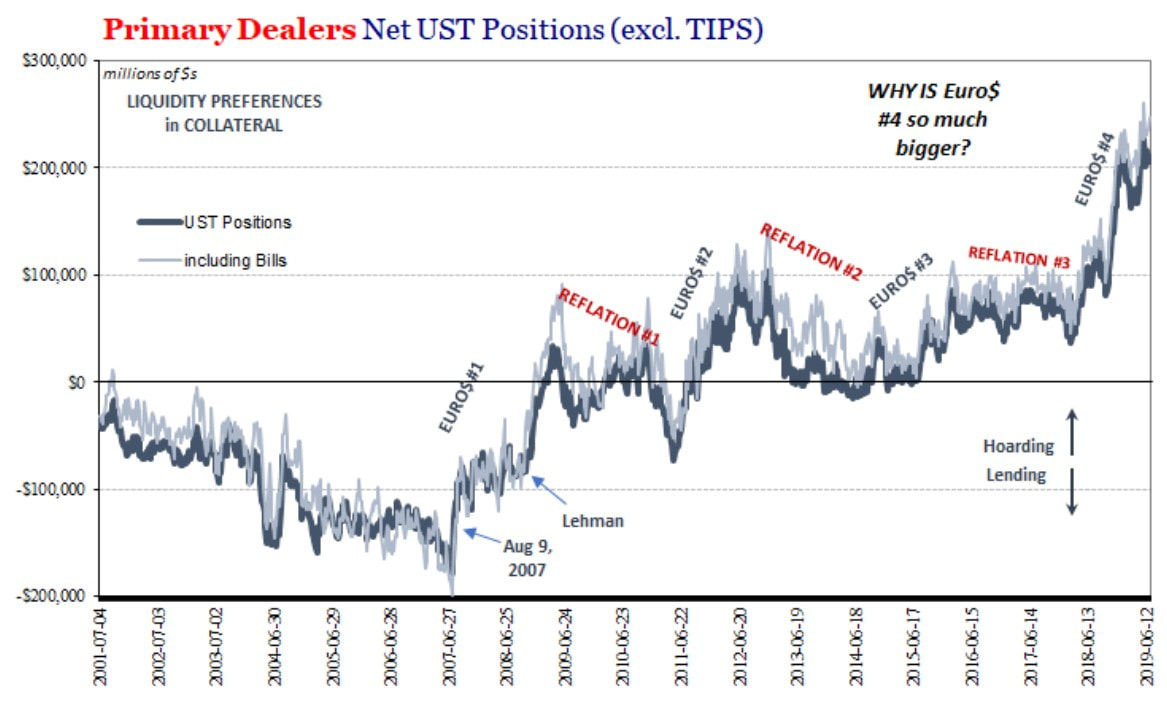

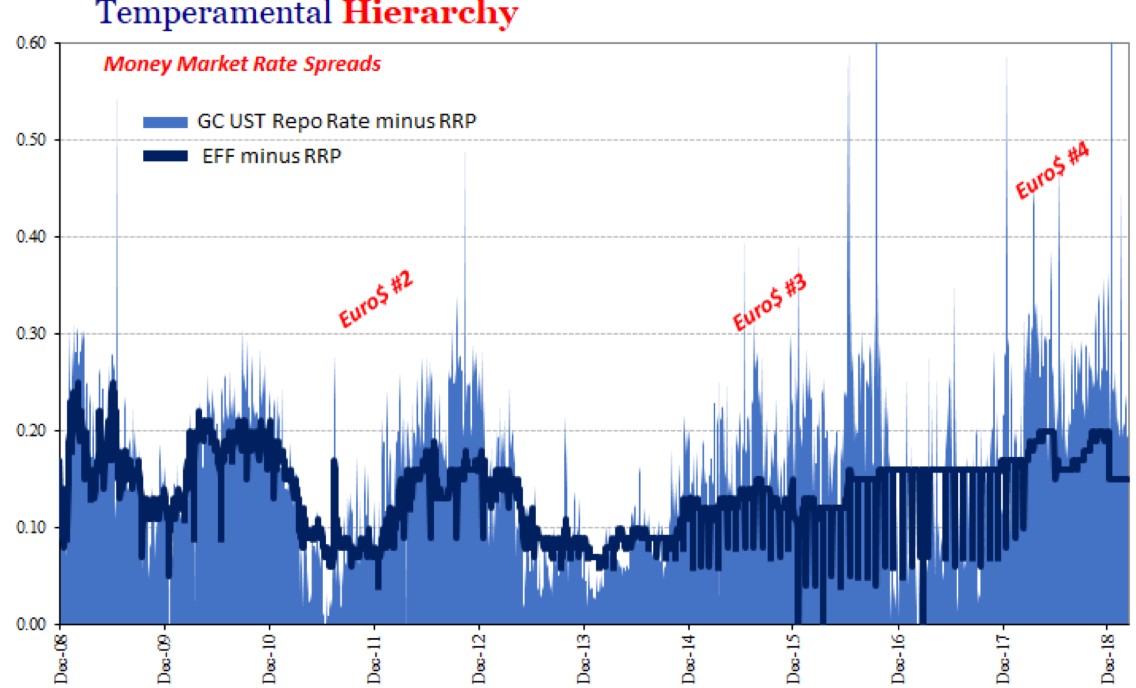

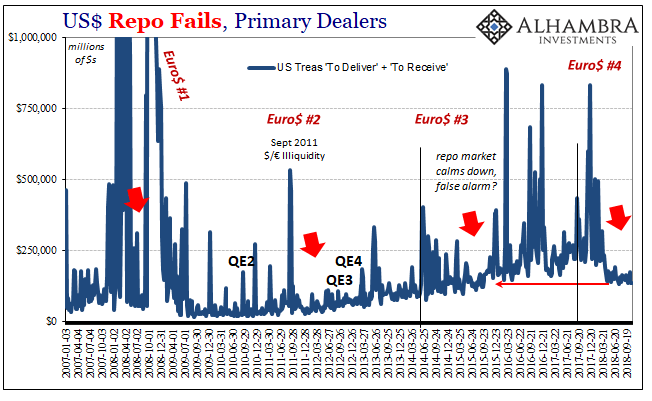

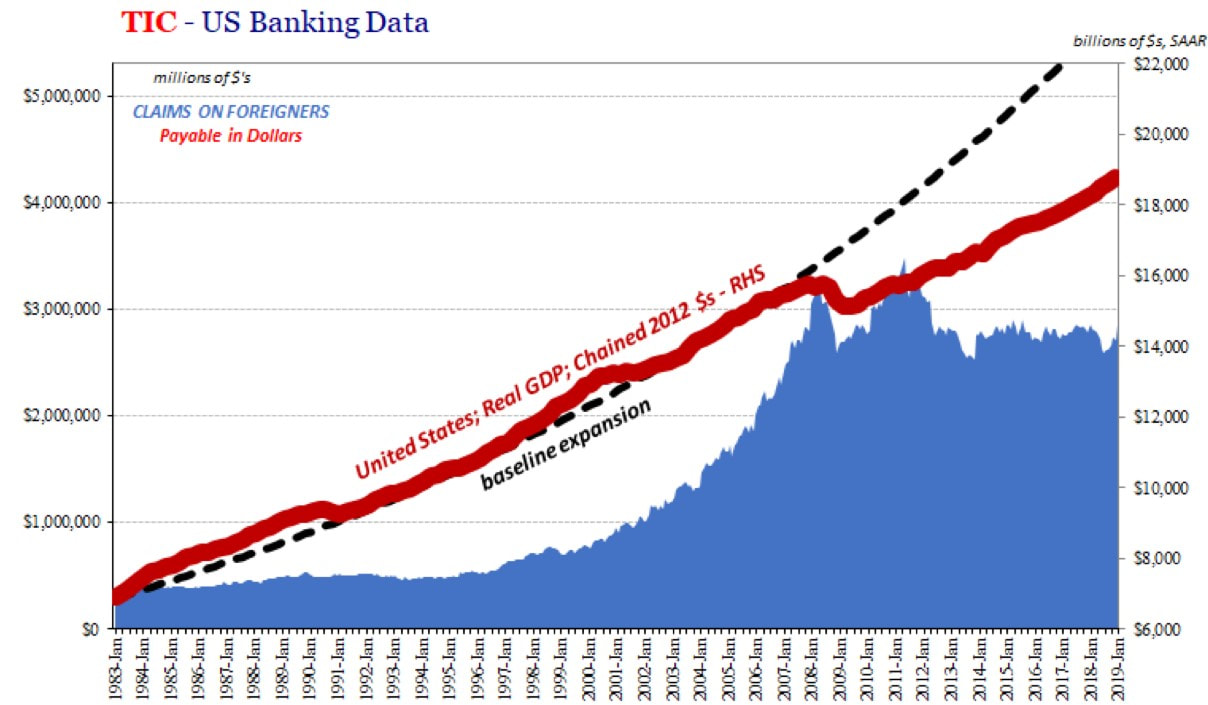

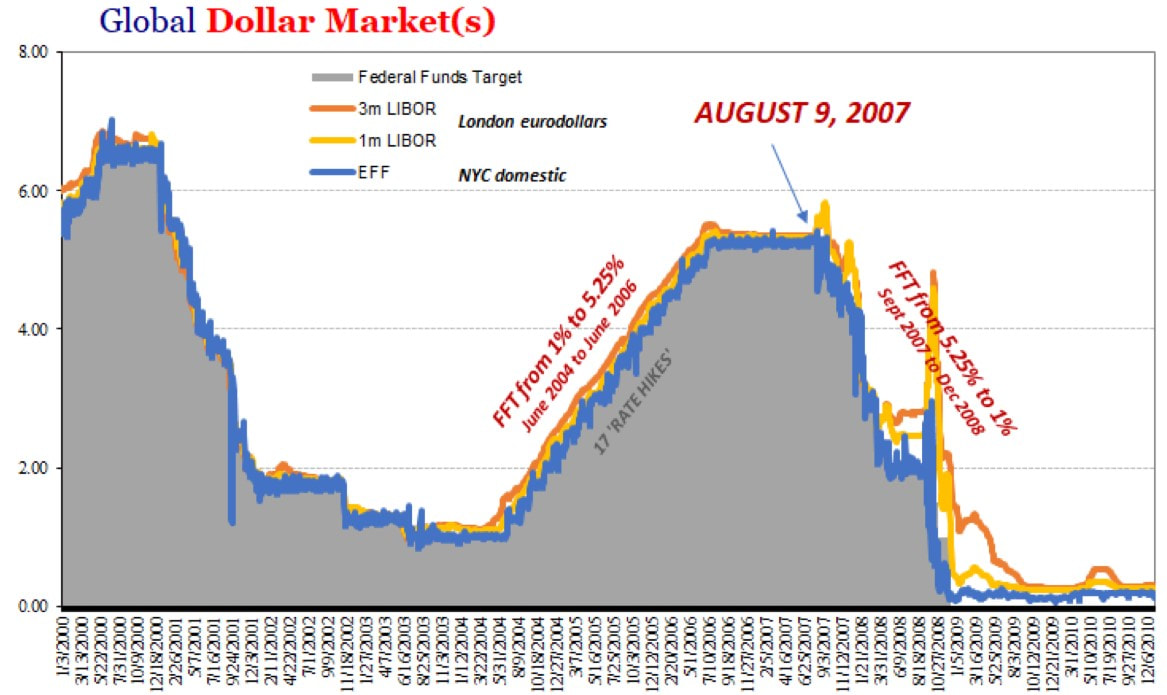

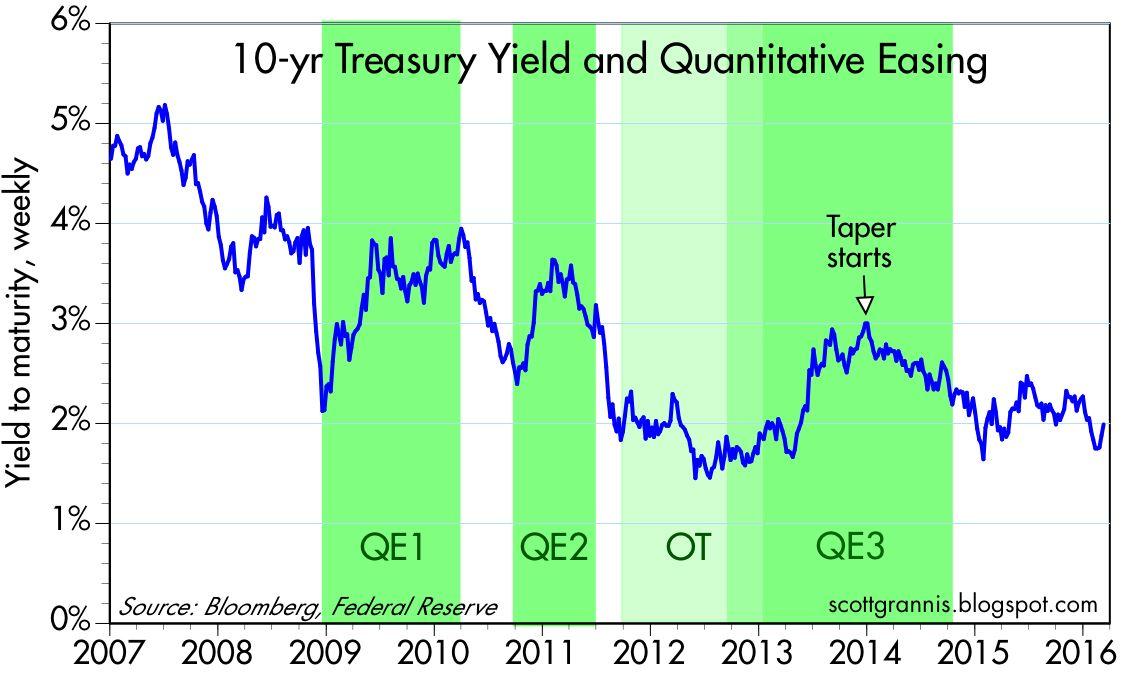

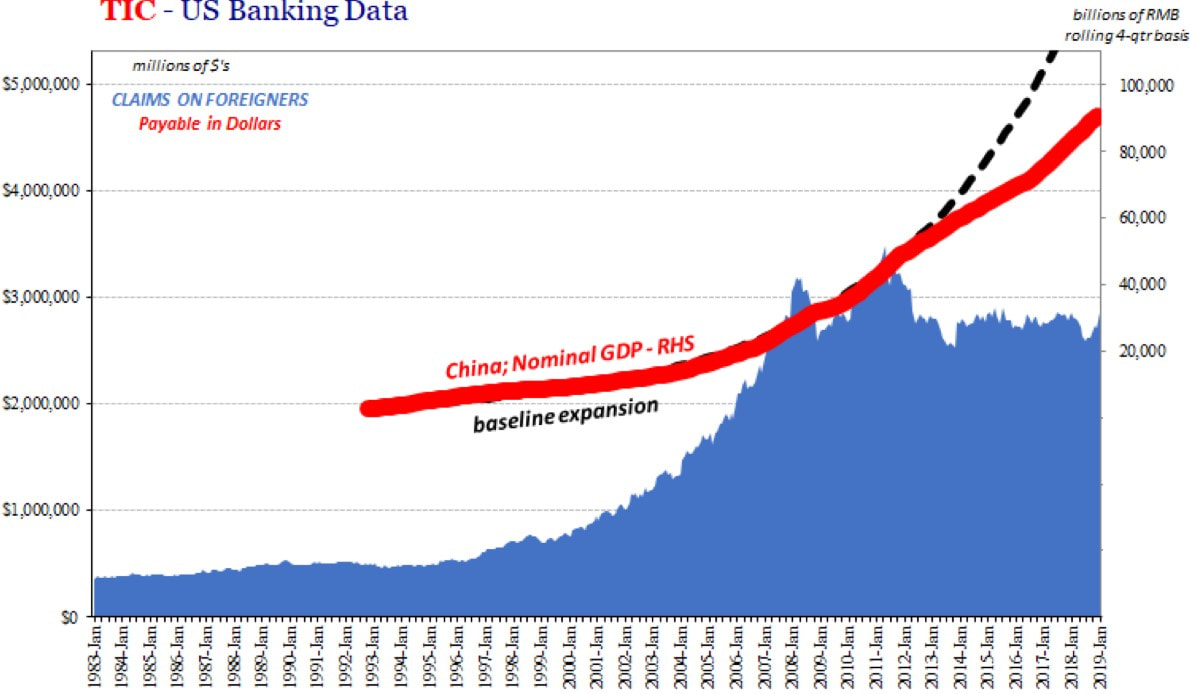

On July 18, 2008, George W. Bush commented at a private political fundraiser in Houston, Texas that "Wall Street got drunk" and that "now it's got a hangover". Although that may had been the case, it seems the financial markets, to this day, have not been able to bounce back. Apparently, the binge drinking practiced mainly since the 1990's made some irreparable damage to the financial system's liver. Despite the central bankers all throughout the world proclaiming to have the cure, the fact is that the hair of the dog provided by their "accommodative" monetary policies has done nothing to put the system back on the growing track. In all seriousness, for some reason the Eurodollar system broke on August 9, 2007 and none of the tools in the central banks' shed managed to fix it. To make matters worse, there are bases to believe the Fed and others are utterly powerless to handle the halt in offshore activity, with their stimulus programmes jacking up nothing more than expectations. On this part 2 of this three-part series, I am going to give explanations for the development of the Eurodollar system being stalled, in addition to its implications on the real economy. Below, the graph presents statistics about US banks and their various cross-border dollar operations. Therefore, that is a proxy for what they might be doing in concert with the unseen foreign counterparties related to this Eurodollar shadow backing activity. As the chart shows, after the GFC, further episodes pertaining to the dollar shortages or funding gap have taken place periodically, apparently every two years or so. Using the designations of Jeff Snider from Alhambra Investment Partners, there have been four Eurodollar events of turmoil. The first one was the Global Financial Crisis, which was also the greatest one (so far). A couple years later, in 2011, another one emerged, resulting in the European sovereign debt crisis, having waned by the end of 2012. Then, in late 2014, the third event ensued, hitting the Emerging markets specially hard, with China in particular slowing down, leading to speculations that it would take a "hard landing", which, were it to occur, it would send massive shock waves through the rest of the world. After this one terminating in the middle of 2016, in the second quarter of 2018, the fourth and most recent episode of Eurodollar woe kicked off. As you will see later on, this last one never faded, meaning that we are still trying to shrug it off.  Following part one's discussion, because of the evolution of the Eurodollar system, the complexity of overall financing started growing and defining what money was became an increasingly dubious task. In the early 70's, economists began noticing that, even though transactions denominated in US dollars, in both the financial and the real economy, were rising, the quantity of money was not changing accordingly. In fact, as the next graph depicts, traditional forms of money were becoming obsolete, with bank reserves actually contracting. until 2008. During the 90's, Alan Greenspan often complained that the Fed's aggregates for money supply were getting ever more useless to conduct monetary policy. In his famous December 1996 lecture, known for the "irrational exuberance" remarks, he was not denouncing the soaring stock market, which became the dot-com bubble. He was unburdening about his incapability to understand the trends in the financial markets, since his orthodox convictions on the definition of money made him and his fellow colleagues unable to assess whether their policies were supporting sustainable growth or stock and credit bubbles.  During the GFC, even with the innovative policies undertaken by the Fed, such as TALF, dollar swaps with other central banks and the mix of facilities (like it is being implemented today) to support the markets, and the rising uncertainty, the reserves on banks remained constant. Only when Lehman Brothers filled for bankruptcy, in September 15 of 2008, did the banks begin to accumulate reserves. Noticing the banks were hoarding cash in their balance sheets instead of loaning it out or conveying it to the economy via some other means, Ben Bernanke and his posse interpreted this as there was not enough supply of money to meet the demand. For central bankers and keynesians in general, the Fed has the power to steer the markets to where it wants to go. By expanding the monetary base, through open market operations, the banks, a.k.a. primary dealers, have more funding capability and, thus, they can provide loans for investment and consumption, stimulating economic growth. Undoubtedly, decreasing the monetary base has the contrary effect on growth. This is what ought to happen in theory. However, in reality this does not transpires, at least not since the Eurodollar inception.  The rationale behind quantitative easing was to be a temporary fix for a temporary trouble. The Fed would stand in until the financial system got back on its feet. To the technocrats surprise, the system never managed to go back to its pre-GFC glory days, no matter how many liquidity injections the banks would take. Likewise, removing liquidity through quantitative tightening (QT) is absolutely benign for the financial system in practical terms, though it is a different conversation for expectations and sentiment. Then, why did it not work? The banks and the other banking institutions that participate in this sketchy Eurodollar system lost their confidence in the system. Prior to the GFC, everybody thought there were no risks attached to their activities. After all, due to ingenious derivative products brought by the marvel of financial engineering, everyone was hedged against all kinds of risk. Adding some baseless faith in central banks to the mix, we ended up with markets where participants were fully convinced the system could grow incessantly. Accordingly, in 2008, reality set in and everybody learned that their convictions in this system were absurd. Unfortunately, most of them still believe the Fed and the other central banks have the faculty to get the financial markets and the real economy booming once again. Nevertheless, the system has not recovered on account of the halt or even decline in the "shadow money". Seeing that shadow bankers no longer trust each other, once they realised the system was brimming with risks, their activities became relatively more modest and aware of the dangers.  As a result, in each episode of financial distress, the banks grew more wary of the risks in the system. In spite of their derivative holdings being reduced after each event, by and large, the banks would eventually return expanding their derivative activities, indicating the shadow banking system was becoming more vivacious. However, this would only last for awhile. Like the graph below exposes, each peak in activity would be lower than the previous one, as well as each trough getting lower each time.  With the growing awareness of the perceived risk in the system, banks started positioning in an ever safer stance. When the GFC kicked off, the primary dealers reversed course and began accumulating US Treasury securities, especially after the Lehman insolvency. The short-term Treasuries, the T-bills, were particularly preferred for collateral purposes. As I explained in part one, the T-bills are the most pristine collateral. Because structured products that are used as collateral, like MBS, CLO and other ABS, are deemed riskier during periods of financial distress, banking institutions stop accepting them as collateral in the repo operations. This means that when times are bad, inasmuch as market participants have a fair amount of T-bills in their possession, they can use them to get liquidity without any difficulty.  Additionally, amidst these episodes, the EFF rate - which is the unsecured, weighted-average rate for all of the transactions of reserves among depository institutions at the Fed -, along with the rates on overnight repo transactions secured by Treasury securities, which the most used one is the General Collateral UST rate, climb up and in times of relative lull they go wane down. However, the typical hierarchy inverts in these periods. Despite the repos being a safer means to get funding, implying a lower rate than the EFF one, which is what happens in normal times, throughout the episodes of financial trouble, the repo rate jumps much higher, surpassing the the EFF rate. This occurs for interest rate are prices and, consequently, behave like such. The EFF rate cranks up due to increasing distrust in the system and higher counterparty risk, leading banks to be less willing to "supply" their funds, implying a greater price to get the funding. Similarly, the rush to ensure financial institutions are able to get financing makes the demand for the best quality collateral to balloon, spiking the repo rate. Since the repo rate shoots up more intensely than the EFF rate, this signifies the problem of the Eurodollar system lies in the collateral.  Accordingly, the repurchase agreements that do not materialise, which are known as repo fails, proliferates in these events, because the funds providers cease to accept the low quality collateral.  Moreover, another indicator the system never recovered and the Fed's efforts fell short of expectations is the performance of the long-term Treasuries. Looking at the chart on the right, one can see that during the events of distress, the demand for Treasuries strengthens, forcing yields to plunge. The reason is that market participants start speculating the financial conditions are, or close to, deteriorating and, as a result, they would begin switching to safe-haven positions. Considering the graph on the left, quantitative easing did in fact managed to ease the financial conditions. Yet, every time the Fed halted this asset purchase programme, the benchmark 10-year Treasury would reverse course and commence its decline, as well as another Eurodollar event would arise. Seeing that the financial activity would only reflate with the interventions from the Fed, this signals that the shadow banking could no longer return to its heyday on its own. Hence, the financial system became addicted to the Fed's easy money.

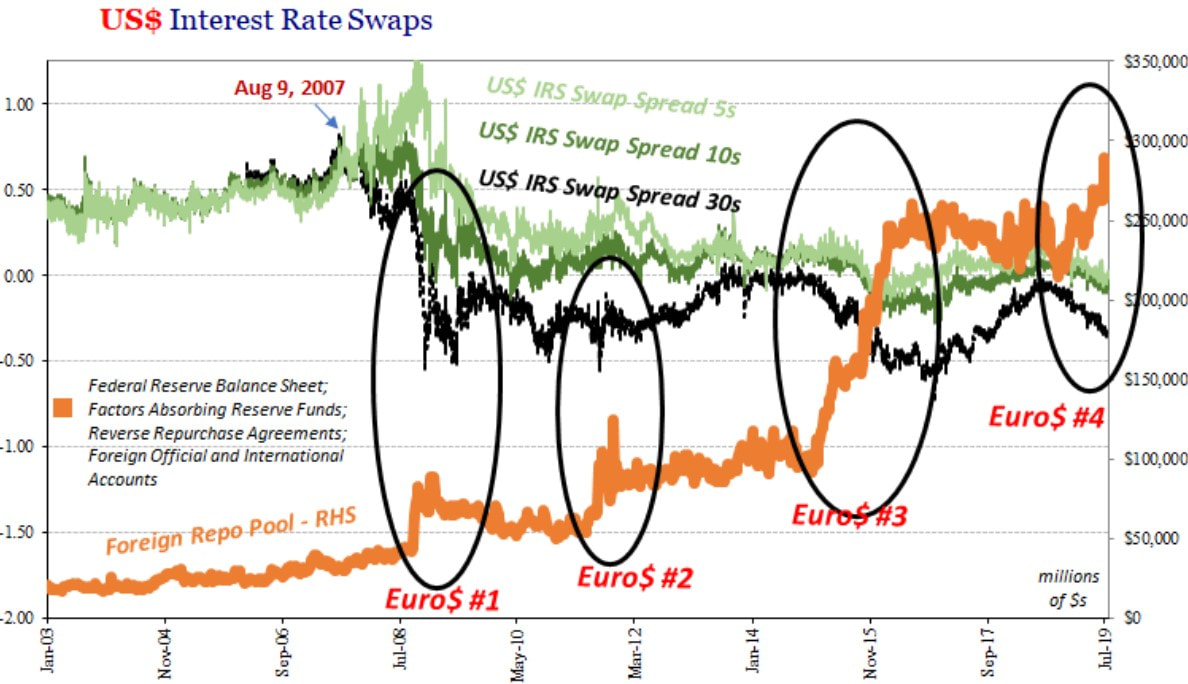

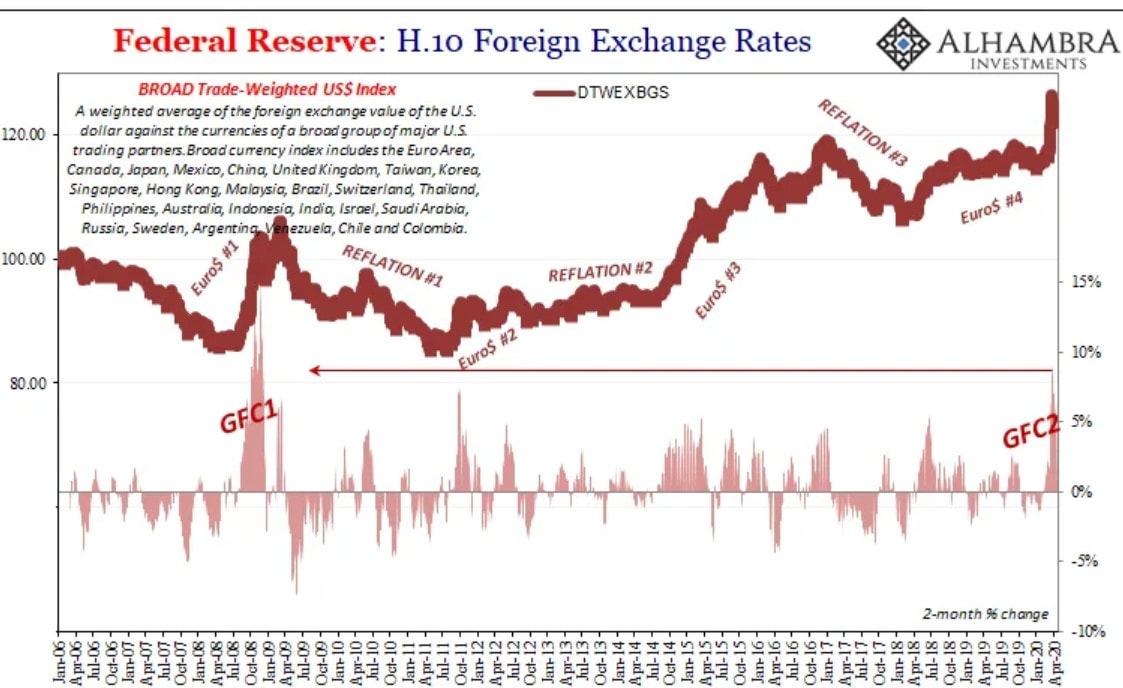

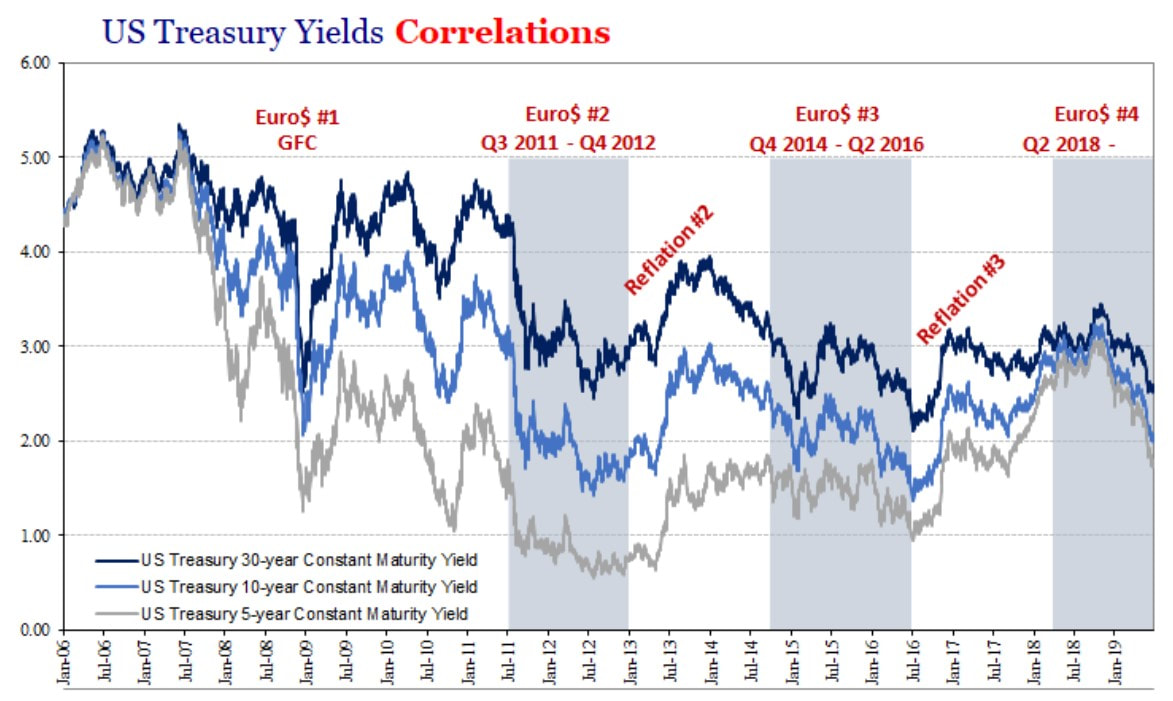

Moving on to interest rate swaps, these in tandem with the Treasuries yields make up another measure of the banks' balance sheet capacity: interest rate swap spread. Swap spreads are essentially an indicator of the desire to hedge risk, the cost of that hedge, and the overall liquidity of the market. The more people who want to swap out of their risk exposures, the more they must be willing to pay to induce others to accept that risk. Therefore, larger swap spreads means there is a higher general level of risk aversion in the marketplace. It is also a gauge of systemic risk. When there is a swell of desire to reduce risk, spreads widen tremendously. It is also a sign that liquidity is greatly reduced, as was the case during the financial crisis of 2008. Even tough this was the case up to the GFC, the interest rate swap spreads have since then behaved in a different fashion. After the GFC, these spreads have tighten gradually, even entering negative territory. On account of the loss of confidence in the system and the sudden realisation that the financial system actually carried risk, regardless of the breakthroughs in financial products, market participants stopped viewing these kind of instruments as incapable of hedging risks. Consequently, the players in the Eurodollar system had to find another source of liquidity to get the dollars to satisfy their US dollar-denominated liabilities, whenever the financial constraints cropped up. So, the financial institutions in this offshore dollar system turned to the central banks in their jurisdictions in order to get the funding needed. Inasmuch as the Federal Reserve is the only one capable of creating the greenback, the foreign central banks and other monetary authorities have to go to the Fed to get those dollars. One of the ways they can get the dollars, which is also the most used one, is through repurchase agreements. These foreign institutions temporarily sell some of their holdings in US Treasuries so as to get the dollars, which they then give to their financial institutions. In addition, as the next chart demonstrates, during the Eurodollar episodes, these foreign entities are extremely active in these repo operations with the Fed, in order to quench the offshore participants' thirst for dollars.  In these periods of financial stress, the Eurodollar players, in their quest to come up with dollars to meet their obligations, end up pushing the dollar higher. There is a common misconception that the strong dollar causes financial turmoil all around the globe, bringing about less economic growth for the world as a whole. Au contraire, the rising dollar is not the cause but the effect. For whatever reason - each episode has its own particularities -, the Eurodollar system periodically goes through woes, which, as I described, drives the dollar to greater magnitudes. Evidently, this appreciation of the greenback reinforces the financial distresses, impairing the real global economy even more. Therefore, whenever the USD is surging, it is a sign troubles in the financial system are emerging and will soon become apparent.  In this day and age, the soaring dollar accompanied three episodes of affliction when the Eurodollar system ventured on the brink of collapse. The fourth one commenced on the early part of 2018. The graph on the right portrays the onset of this last event, when the repo rate swelled and consistently stayed above the EFF rate, which in turn became more erratic. As a result, the dollar mounted up. Moving on to the graph on the left, the Treasuries yields began, on November 8, transmitting the message that troubles in the financial system were brewing. Then, on August 27 of last year, one of the most daunting indicators for market participants sprang up. The yields of the 2 and 10-year Treasuries inverted. Historically, this yield inversion has preceded every recession since the late 1970's. Once this occurs, it is almost certain an economic contraction is on the cards. Hence, the primary dealers and other depository institutions, interpreting the inversion as impending troubles, turned more reluctant to provide funds among each other. Furthermore, the search for liquidity became more difficult, which meant the repo rate surged due to increased demand for these operations. On part 3 of this series, I am going to expand more on the present Eurodollar event.

Moreover, you may have figured out by now that the Fed, despite its claim that it "provides the nation with a safe, flexible and stable monetary and financial system", the truth is that they are far from achieving that claim, because they do not know how to do it and, to add insult to injury, even if they did, they are powerless in their efforts to curb the Eurodollar caprices. The Fed's policies, as well as the myriad of facilities implemented in the midst of the GFC, do virtually nothing to solve the distresses of dollar shortages during financial panics. The only thing the Fed can do, with the help of the financial media and the keynesian technocrats spread worldwide, is try to persuade market participants that it is ubiquitous and able to support or rescue the financial system no matter what. The truth is that they can only follow the signals given by the markets and respond to them - rather late I should add - so as to create the illusion of backstopping the markets' woes and, thus, maintain the system afloat. In all fairness, the central bankers and the media have been successful in duping everybody that they do in fact have the control of the system's helm. Fortunately, the sham will be exposed very soon.

Finally, the system broke down in the summer of 2007 simply because there was, and still is, too much debt. As I have been discussing since part one, on account of diminishing good collateral and greater counterparty risk, the financialisation process of the global economy came out of the GFC severily hindered. Owing to the fact we live in a world where the tail wags the dog, meaning that the health of the financial system regulates the performance of the real economy, the near stall of the financialisation phenomenon prompted the economic development in taking its toll, especially in the developed economies, as the following graphs show. In a nutshell, the Eurodollar has been running on fumes.

To conclude, before the 2008 crisis, the shadow Eurodollar system grew exponentially, due to the ludicrous idea that financial engineering had managed to curb the risks taken by the market participants. After the GFC, that belief went out the window, turning everybody more cautious.

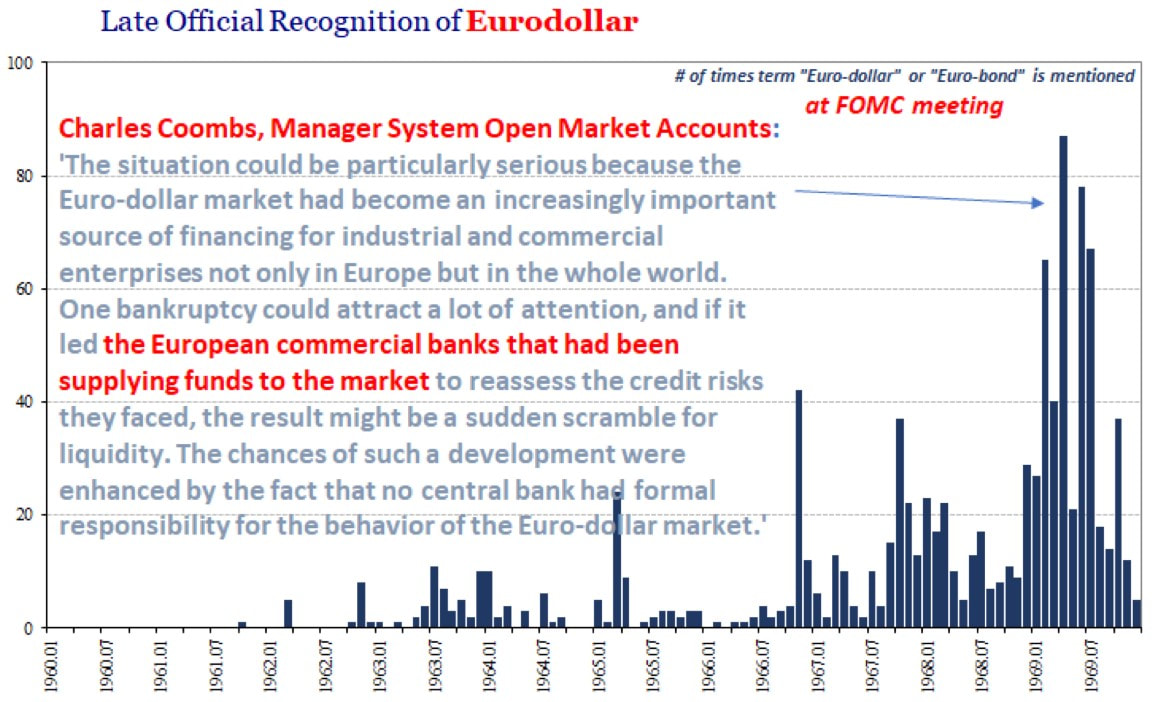

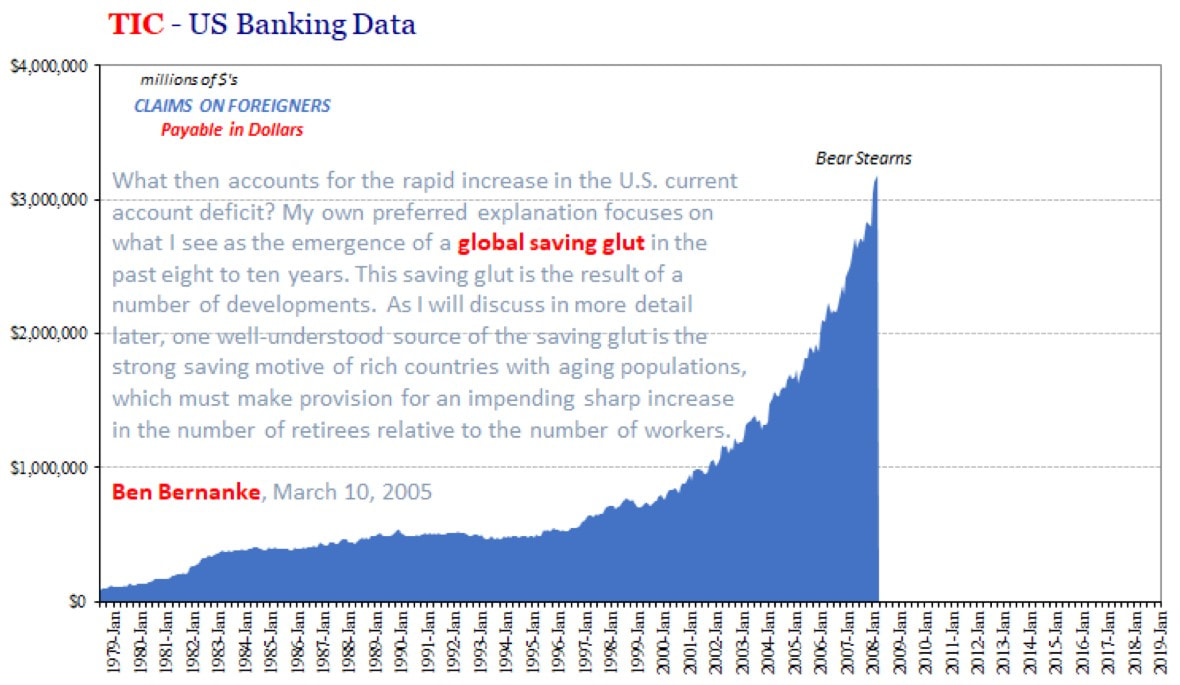

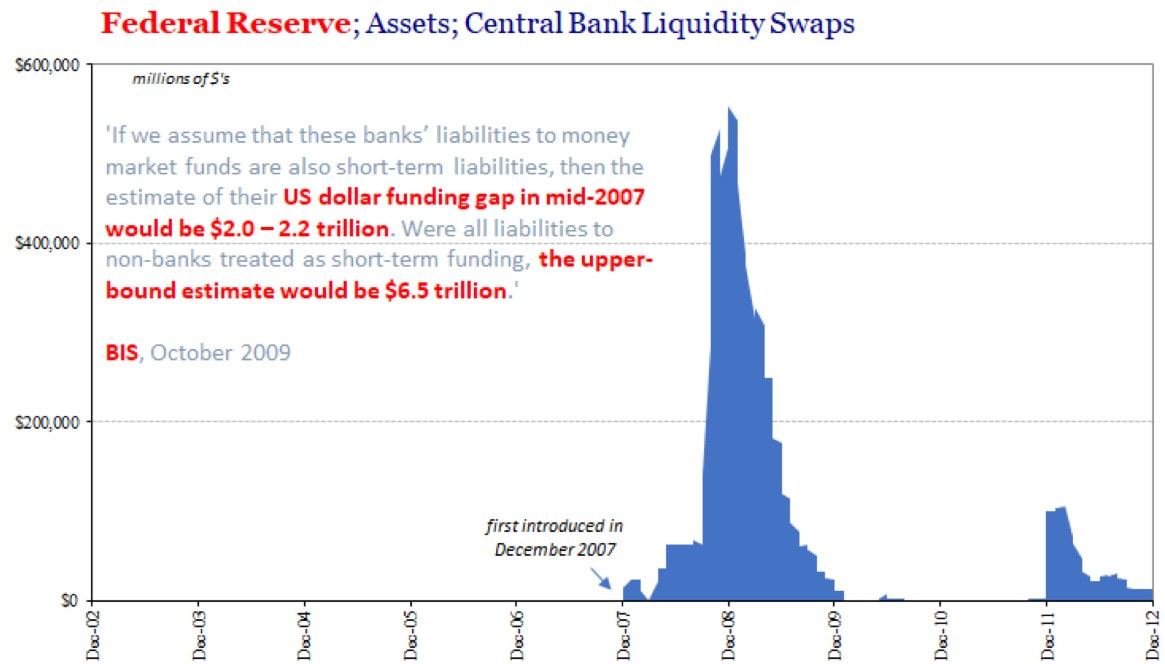

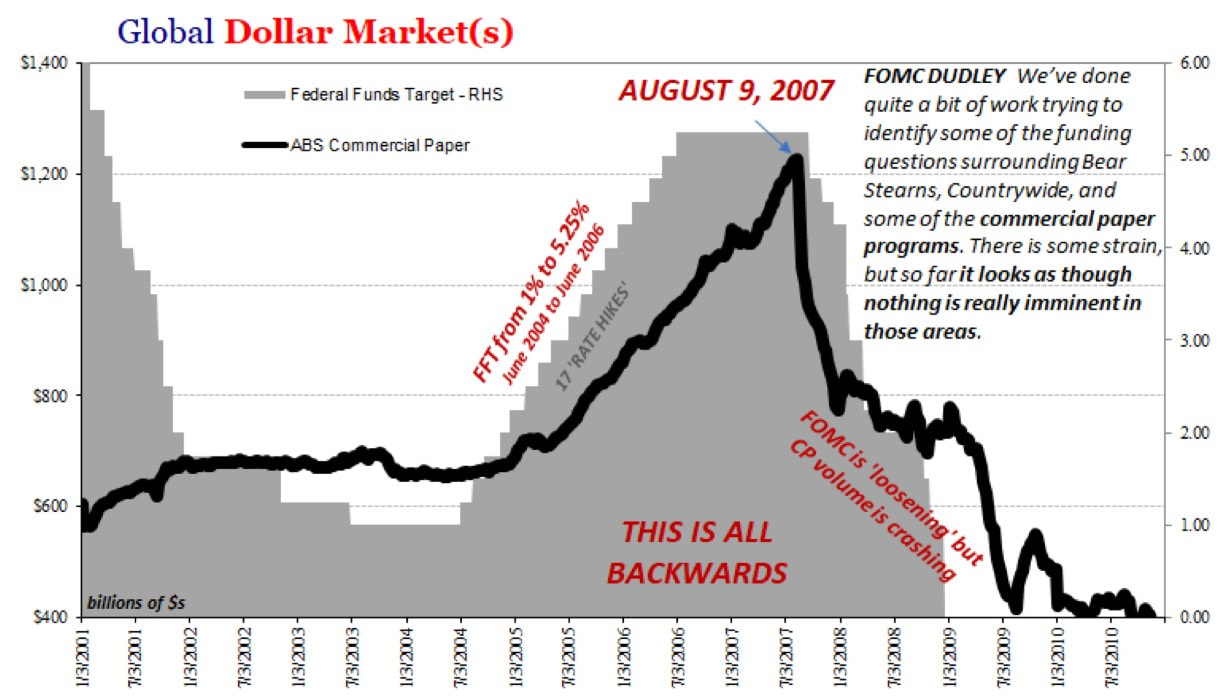

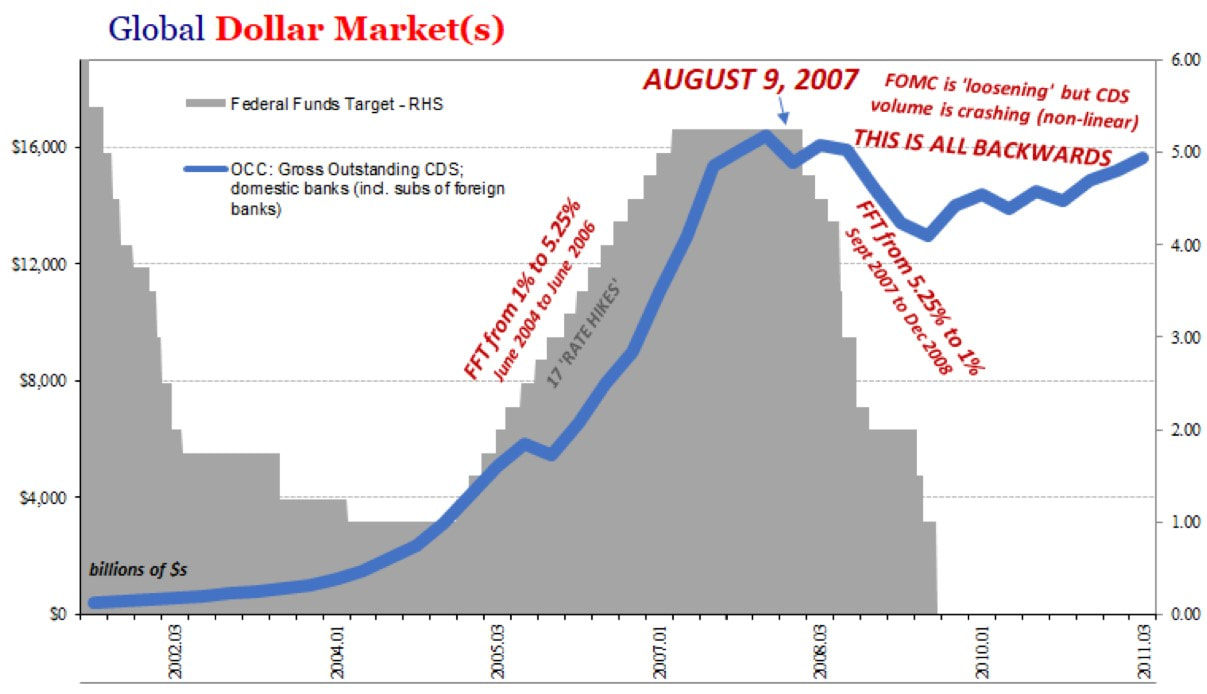

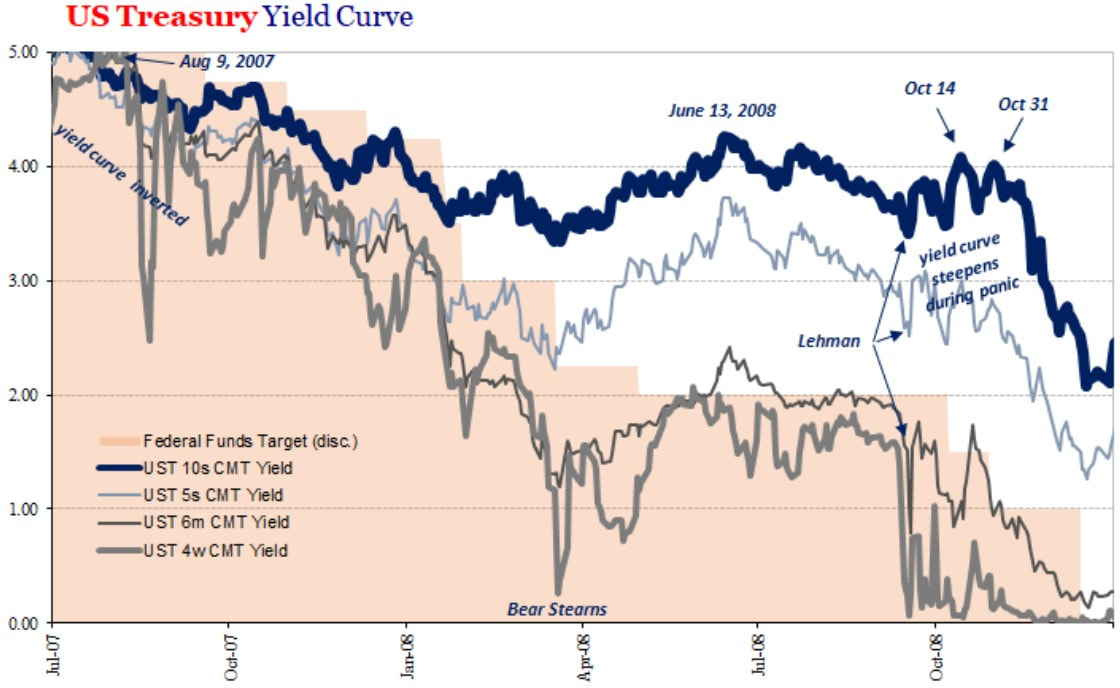

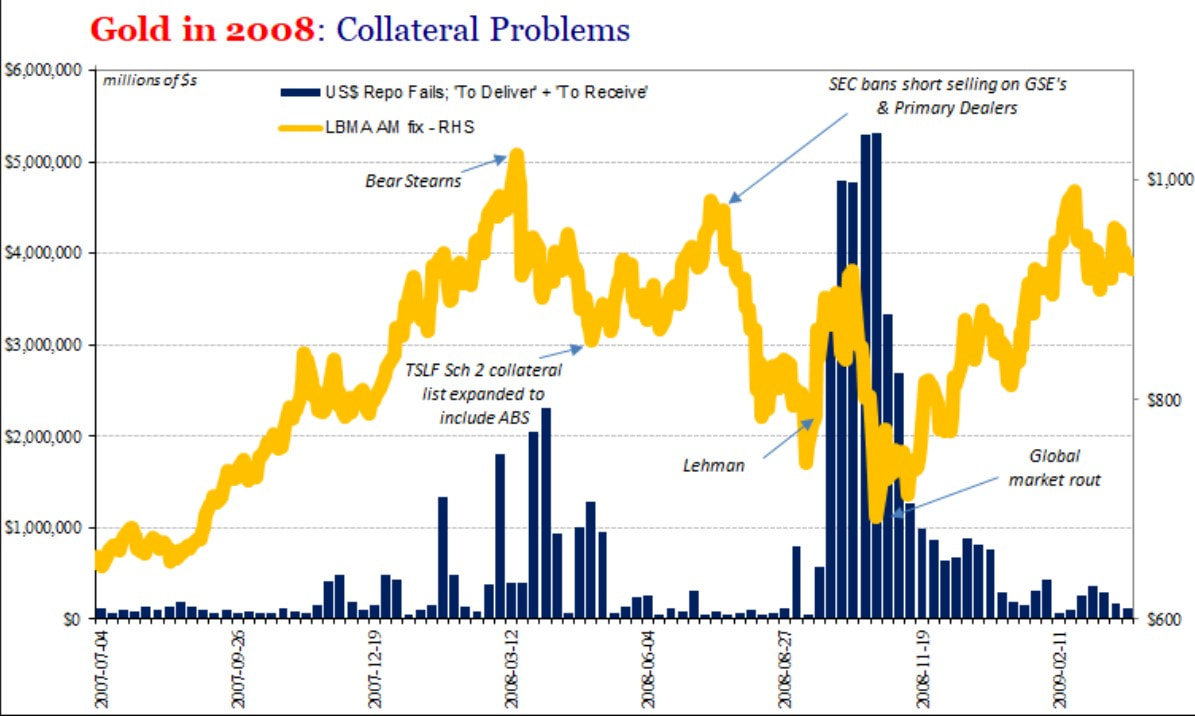

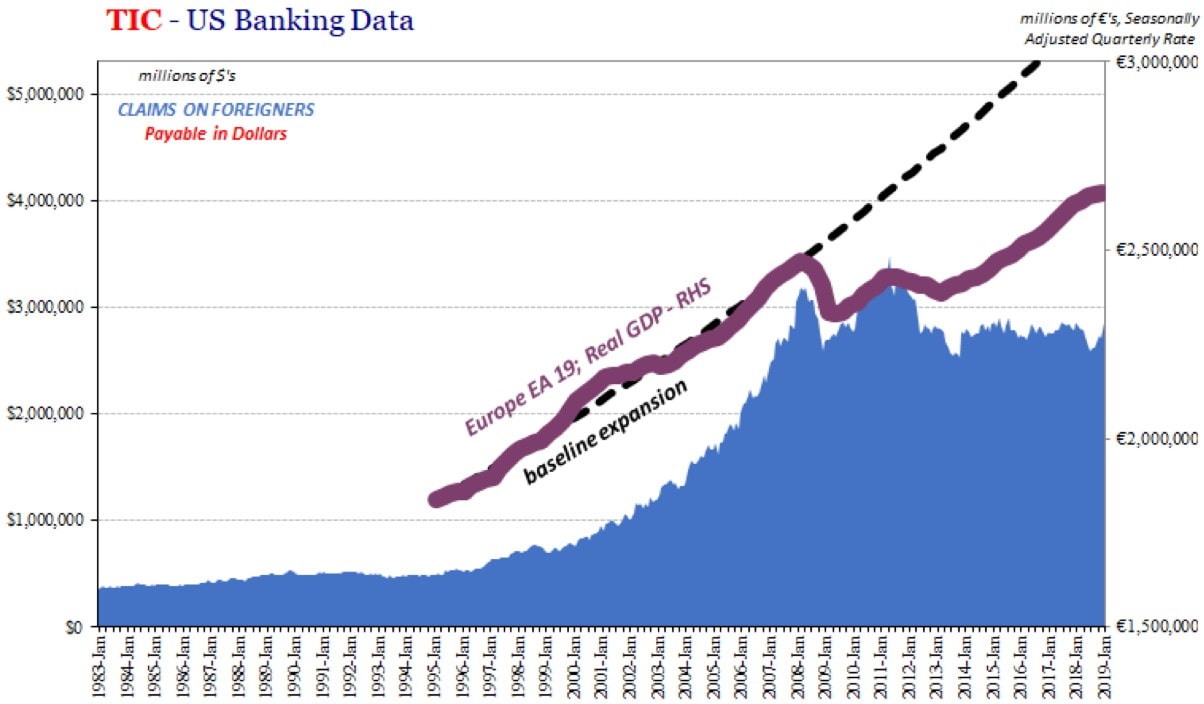

In spite of all the efforts made by the central bankers, the system never recouped its pre-GFC effervescent trajectory. However, the media has at least made everyone believe the Fed saved the financial system and the economy, even though everything points that conditions have actually got worse. On the last part of this three-part series, I am going to expound on the current financial panic. Specifically, on whether the crisis is close to its culmination or it is only beginning, and I am going to weigh in on the ability this system and the central bankers have to endure this blow. As I have been discussing, the current monetary regime is the dollar standard that substituted the gold exchange of the Bretton Woods system. In spite of the US dollar being the global reserve currency, taking the role that gold used to play, the Federal Reserve is for all intents and purposes powerless in managing their own currency. The offshore Eurodollar market has grown to such an extent that it determines where the world economy is headed. The evolution of this market is going to be analysed, and we are going to see how it influences the conditions in the financial markets and the economic growth. This is part 1 of a three part series. On this one, the development of this system until the Global Financial Crisis is going to be analysed. In addition, we are going to see why and how the 2008 financial debacle happened. The term “euro” long pre-dates the European common currency in our use here. And in front of the word “dollar” simply conveys the notion of offshore. And there are other markets. There is a eurocurrency market of, for example, offshore yen is called Euroyen. There is even something since the introduction of the European monetary union where there is offshore euro, which is called Euroeuro. A Eurodollar used to be just an account convertible into physical US dollars that were on deposit outside of the US. As time went by, the Eurodollar turned into a system of interbank liabilities that real economy participants were using, once they connected to it, in order to achieve real-world activities, as the Head of Global Research for Alhambra Investment Partners defines it. Additionally, it is a currency-like system based around the banks, scattered all throughout the world, which participate in it. Although it was William Clarke of the London Times who coined the term "Eurodollar" in 1960, Paul Einzig, who was known as "dean" of writers of international finance, was the first to write about the Eurodollar system in a widespread fashion. He stumbled across it accidentally in 1959 and he was emphatically told by some bankers not to report on that topic. At the onset, the Eurodollar market was largely an European affair, where merchant banks were using this market to achieve global trade settlements. Seeing that until the mid-1960's the players of this market were mainly European banks, US officials were not preoccupied by it. The chart below shows that there was little to no mention of the Eurodollar market by the Fed's Federal Open Market Committee (FOMC) in the early 60's, even though a 1964 paper by the Bank for International Settlements (BIS) - colloquially called the central bank of central banks - proposed that this market held "exceptional potential for expansion which may create a special problem for monetary authorities in the future".  The BIS turned out to be right and the Eurodollars managed to increasingly get under the Fed's radar. By the end of that decade, the Eurodollar market was a hot topic on FOMC meetings, because it had worked its way into everything. Moreover, on account of US banks borrowing tremendously from European banks in offshore dollars, distress in currency markets, especially the deutschmark, began to crop up. Thus, as US banks started to participate in it, the Eurodollar system embarked on replacing several traditional roles of global reserve currencies that had previously been performed by gold alone - the pre-WWI Gold Standard and the Interwar Gold Exchange Standard - and by gold and dollar in tandem - Bretton Woods (BW) system. As a result, the global monetary paradigm shifted, opening the door for different sources of funding through innovations in banking and money itself. In the late 70's still, the official doctrine written was that the Eurodollars must be treated exclusively as investments. Since, at the time, they were primarily using certificates of deposit, these Eurodollars were mostly functioning as a store of value and not acting as a medium of exchange. The authorities at the Fed and elsewhere had simply made a choice and decided that they were going to view this Eurodollar system as nothing more than an investment option for domestic banks. Yet, banks and their customers had come to create and utilise different monetary forms to accomplish real-world transactions. These liabilities and wholesale funding techniques did not fall under official definitions of money. So, there is no real Eurodollar. It is not a thing like there is a dollar bill. It is a system of financing and accomplishing monetary and financial ends that was just very different from how it had ever been done in the past. Monetary evolution that was unleashed during the 50's, 60's, and 70's kept evolving once it was let loose into its own ecosystem offshore. There was as much qualitative expansion as there was quantitative expansion. Accordingly, when I talk about Eurodollars, I am talking about US dollars, though what I am referring to is a system that operates in the shadows and creates supply of US dollars and creates all kinds of complex transactions in US dollars that the Federal Reserve does not really know about due to being outside of their regulatory purview, and it does not really understand exactly what is going on and how it really works, as well as what these bankers are up to. (...) the proliferation of products has been so extraordinary that the true underlying mix of money in our money and near money data is continuously changing. (...) a decision to base policy on measures of money presupposes that we can locate money. And that has become an increasingly dubious proposition." In its earliest form, this interbank offshore accounting system transformed what used to be deposit liabilities into interbank borrowing. Adding to that the communications technology revolution, you have financial innovations in the form of standardised derivative contracts in the 1980's – things like interest rate swaps and Eurodollar futures – and even the term "interbank borrowing" itself becomes exponentially more complex. Hence you have this flexible creative vacuum upon which globally connected financial institutions can, all on their own, choose how to participate and how to fill in what is the vitally important role of global reserve currency. Unlike the gold exchange system under BW, this Eurodollar system could supply what was needed, how it was needed. And it could do so largely without politics and official interference, or even public scrutiny. For the keynesians, the global exchange system under Bretton Woods lacked both liquidity and adjustment functions to maintain under the kind of demand that the lively swelling financialised world economy begged for. Consequently, it was not only the banks that wanted to do this, the official sector wanted them to do it because they did not want anything to do with figuring out how to replace the Bretton Woods system. On the one hand, gold was what gave confidence to the dollar in the BW regime, but even that was more and more challenged throughout the 60's on account of the Triffin Paradox, which consisted, at the time, on the depletion of gold reserves at the Fed because of the endless current account and budget deficits. On the other hand, the Eurodollar offered liquidity and adjustment to demand but, paired in denomination with US dollars, it also gave the confidence that this shadow money would easily supply financing for a globalising world. Effectively, the US dollar, despite being regulated by the Federal Reserve, it is only regulated by the Fed in the US. And a huge amount of this overall global US dollar system operates in the shadows, outside of anyone’s regulation, and it is all controlled by international bankers. By the first decade of this century, the Eurodollar system hit its zenith. Inasmuch as this is all shadow money, we have to be careful. Any kind of statistics or estimates that we have, they all come with caveats attached to them. These are, at best, rough estimates simply because, officials decided this Eurodollar system was just an odd investment choice rather than some reserve-less global currency design and, therefore, nobody kept track of what was really going on in these offshore places. However, in the aftermath of the 2008 GFC, some people were compelled to go back and look at this thing. Maybe we should start to piece some of these things together and match up some quantities for all of these offshore qualities that we’re observing throughout the period. During the noughties, banks, especially in Europe, had binged on the so-called international assets. From 2000 to the end of 2007, these assets had ballooned from $10 trillion to $34 trillion, according to the BIS estimates. So, how was all that offshore credit creation funded? Obviously, it was not Alan Greenspan and Ben Bernanke, because the Fed throughout this period had produced little to no bank reserves. The most Alan Greenspan or Ben Bernanke had done was move the Federal Fund target around a quarter point here or there, maybe 50 basis points, every once in a while. The answer is that the Eurodollar system created its own forms of liquidity, its own forms of reserves that were, again, these long chains of interbank liabilities that stretched all the way around the world and back. In that BIS study, researchers figured that the world was short of what they called a “funding gap” anywhere between $2 and $6.5 trillion on the eve of the panic. In this case, the dollar short means that there is a material mismatch between several credit dimensions, including maturity and geography as well, whereby some bank in Europe, for example, who has been using its holdings of structured US mortgage obligations or emerging market Eurobonds - bonds denominated in a currency of another country/region - in repurchase agreements (repos), suddenly has very limited monetary recourse when the global repo market suddenly rejects its collateral. In 2005, what Bernanke would propose was what he called a global savings glut (look at the chart below - US banks' claims on foreigners denominated in dollars, which are used as a proxy for the extent of the Eurodollar system). In other words, from his perspective, he saw that there was something happening in the world and it was distorting the US dollar system, including what seemed to be a perpetual bid for US government bonds, US Treasuries and also government-sponsored enterprises (GSE) agency bonds.  Because of his conviction, Bernanke believed this all had to be global savings with, for instance, foreign baby boomers seemingly getting ready for their retirement by increasing their savings and allocating their savings to US dollar assets for non-specified, unknown reasons. Bernanke and the other technocrats in the US were uncapable of seeing the actual extent of the Eurodollar for their orthodox keynesian convention blinded them. Their view was that since the US dollar is the currency of the United States, the big international capital flows in dollars must all originate in the US because that is where the system is headquartered. In reality, the bankers have figured out that if they originate major transactions in the US, they are under regulatory scrutiny over there. Instead, they have the ability to create these massive loans, structured products and swaps, and all kinds of elaborate derivatives in the shadows outside of the US banking system, where they are essentially unregulated and can get away with doing whatever they want. In fact, the Eurodollars expanded rapidly in the 90's till the GFC because what most people saw were only the benefits of globalisation, with growth in the worldwide economy, emerging market economic miracles, and global trade which seemed to be at the center of it, and these economic systems apparently were enhancing as they were becoming more closely tied together by this global monetary arrangement. Moving on to the 2008 GFC, the conventional explanation for the panic was that a bunch of greedy Wall Street bankers were taking on this allegedly secure instruments in the form of these subprime mortgages, which turned out to be ridiculously dicey. In reality, it was a bit more complicated. Firstly, even though the subprime mortgage market a threat that could somewhat imperil the financial system, it could not on its own knock down Lehman Brothers or Bear Stearns or AIG or any of the somehow nationalized banks that were scattered all throughout Europe and elsewhere. This panic is called Global Financial Crisis for a reason, it was not just an American failure. Because there were variations in financial systems all across the globe, some of which did not rely on securitisation and, thus, were not heavily exposed to US subprime mortgages at all. More than that, there were large, complex financial institutions that had failed or nearly failed in various countries around the world. The [majority's financial report] says the crisis was avoidable if only the United States had adopted across-the-board more restrictive regulations, in conjunction with more aggressive regulators and supervisors. This conclusion by the majority largely ignores the global nature of the crisis. For example: The global nature of the GFC explains the action of engaging in currency swaps taken by the Fed with other central banks. During 2008, the Fed’s balance sheet swelled not due to specific bailouts or domestic liquidity programmes. By far the most that was added was through these US dollar swaps with foreign central banks. The reason that led the Fed to hand out more than half a trillion dollars to foreign financial institutions (through the central banks), in the midst of the worst financial meltdown since the Great Depression, was because these foreign entities were demanding their central banks to rescue them, begging for funding in US dollar terms, in order to fill the funding gap as the BIS referred to. In more detail, the participants in the Eurodollar system were struggling to get access to US dollar financing owing to the fact that, as I am going to show you, a surge in counterparty risk and a diminishing pool of good collateral were in the making.  Secondly, most people pin the onset of the GFC on September 15, 2008, when Lehman Brothers filled for bankruptcy. While others may consider the Fed bailing out Bear Stearns in March 14 of that year the beginning. Once you look at the graph below, you realise the crisis kicked off on August 9, 2007. The GFC began to emerge in this day when the 1-month LIBOR - London Interbank Offered Rate is the average interest rate at which leading banks borrow funds of a sizeable amount from other banks in the London market; LIBOR is the most widely used benchmark or reference rate for short-term interest rates - jumped above the 3-month rate and, on the flip side, the Effective Federal Funds (EFF) rate - the EFF is the interest rate at which depository institutions trade federal funds (balances held at Federal Reserve Banks) with each other overnight; the federal funds rate is the central interest rate in the US financial market - took a tumble. This signaled that the counterparty risk in the Eurodollar system rose and, consequently, the financial institutions were more willing to park their funds at and transact through the US banking system.  In addition, the other parts of the Eurodollar system, this wholesale system, followed the same pattern, much the same way. Asset-Backed Commercial Paper (ABCP) was one of the primary innovations of the Eurodollar system and it was also one of the primary points of contagion as it spread across the globe. In the wake of August 9, it utterly collapsed. Nothing the Federal Reserve did, which included cutting the Federal Funds rate, there were Term Asset-Backed Securities Loan Facility (TALF) liquidity auctions, collateral swaps, those dollar swaps, and there was even a commercial paper funding program and a money market commercial paper funding program (just like today), would rescue these shadow markets.  Furthermore, the ABCP is a short-term money market security backed by collateral. This collateral may consist of collateralised debt obligations (CDO) and things of that sort, which are comprised of credit card debt, auto loans and student loans. Thus, the commercial paper is backed by the expected cash inflows from those receivables - various types of debt and loans. As the receivables are collected, the originators are expected to pass the funds to the conduit, which is responsible for disbursing the funds generated by the receivables to the ABCP investors, a.k.a. noteholders. Seeing that these receivables are a function of the general condition of the real economy, one would think that when the economic agents, particularly households, started to exhibit signs of financial constraint, these instruments became less appealing. Although that is a factor, the reality is more complex than that. The uptick in the LIBOR signaled soaring distress in the Eurodollar framework, on account of the collateral losing quality and surging counterparty risk surging. Likewise, the same thing occurred with the Credit Default Swaps (CDS). These intruments are credit derivative contracts that enable investors to swap credit risk on a company, country, or other entity with another counterparty. For instance, if a lender is worried that a borrower is going to default on a loan, the lender could use a CDS to offset or swap that risk. To swap the risk of default, the lender buys a CDS from another investor who agrees to reimburse the lender in the case the borrower defaults. The fact that the volume of transacted CDS stopped growing, and even went down slightly, indicates that investors were not very inclined to acquire such instruments, due to the borrowers' perceived probability of default becoming increasingly elevated.  By following the evolution of the yield curve while the GFC was unfolding, you see that each tenor behaved differently. As you can see, the yield curve inversion marked the inception of the panic too. After that, the yields fell until the Bear Stearns debacle, when the Treasury bills (short-term) plummeted while the notes and bonds started to climb. Then, with the Lehman Brothers bankruptcy, the same incident happened again. What went on during these periods of financial trouble is liquidity became very scarce. Banks turned very wary of lending out their funds. All of a sudden, banks were willing to lend only against the reputed "pristine" collateral. This collateral happens to be Treasury bills. As a result, investors and financial institutions went on a T-bill shopping spree. Alternatively, market participants could sell their holdings of US dollar-denominated assets so as to quench their thirst for greenback liquidity. The Treasury notes and bonds were included in this sell-off, pushing their yields higher, steepening the yield curve.  In these events of liquidity shortage, the dollar rummage was so intense that even the US Treasuries, which are (foolishly) considered to be the safest of safe-havens, were being liquidated. Like I exposed above, the funding gap of the Eurodollar institutions was colossal. Hence, these foreign entities got rid of any dollar-denominated asset with a bid. Before the GFC, those institutions were able to use as collateral in the repo market mortgage-backed securities (MBS) and other asset-backed securities (ABS), in addition to CDOs and structured products of that nature. In times of panic, the banks stopped accepting those less reliable securities as collateral. Therefore, as the next graph demonstrates, the amount of repo fails - which are simply the number of times repurchase agreements come to no avail - shot up during such episodes, resulting in the selling of US dollar-denominated assets. Since gold is also negotiated in dollars, the precious metal did not manage to escape the liquidation, driving its price lower.  To sum up, the Eurodollar system grew relentlessly up to the summer of 2007. At this time, finacial institutions, mainly banks, became worried with the level of counterparty risk and the quality of the securities that were being used as collateral. From this point on, panic ensued, leadind to a massive sell-off of dollar assets in order to fill the funding gap. That is why the financial crisis occurred and it was so all encompassing, geographically and in securities terms.

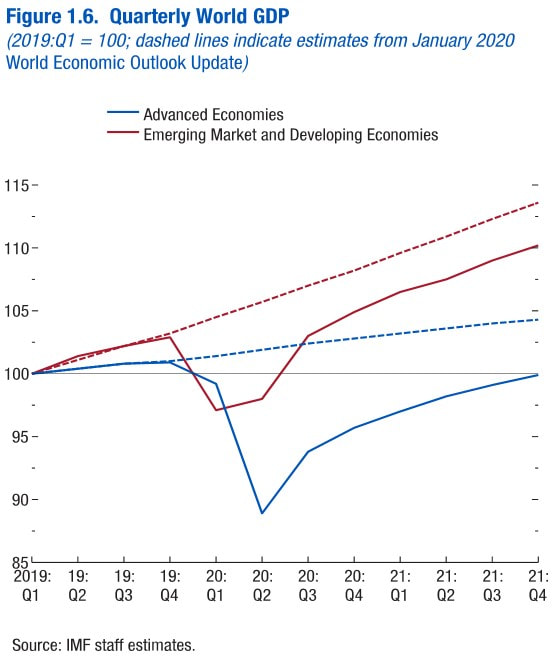

On the part 2, I am going to delve into the recovery of the Eurodollar system, or lack of it, until the emergence of the COVID-19 pandemic. On 1850, french economist Frédéric Bastiat presented the world with his magnum opus, Ce qu'on voit et ce. qu'on ne voit pas, which translated to english is "What is Seen and What is Unseen". In this essay, Bastiat introduced the concept of opportunity cost - he did not named it that, this term was coined later - through the parable of the broken window. In this day and age of coronavirus-induced turmoil, it is of paramount importance to revisit the lessons taught by that parable. The parable seeks to show how opportunity costs, as well as the law of unintended consequences, affect economic activity in ways that are unseen or ignored. The resources spent on one or a few sectors are resources that cannot be spent on other sectors. Thus, the stimulus felt in one sector of the economy comes at a direct – but hidden – cost to other sectors. In addition, the COVID-19 has led the governments to grind their economies to a halt. At a first instance, the interventions pursued by the governments to combat the spread of the kung-flu are causing a collapse of the economic activity. On that account, to tackle this issue, governments are again stepping in, which is set to bring about a whole series of negative outcomes that will leave the economies at an even worse shape. Firstly, shutting down the economy, in order to prevent the coronavirus from spreading, is proving to cause far more harm to society than the virus, with the unemployment soaring worldwide and the global economy entering a depression not experienced since the Great Depression. According to the IMF in its April 2020 World Economic Outlook, the World GDP is going to fall 3% this year, in relation to 2019. In more detail, the Advanced economies will plunge 6.5%, with -5.9% for the US, -7.5% for the Euro Area, -5.2% for the Japan and -6.5% for the UK; and the Emerging markets and Developing economies will decrease only by 1%, with 1.2% and 1.9% increases for China and India respectively, -5.5% for Russia, -5.3% for Brazil, -6.6% for Mexico, -3.3% for the Middle East and North Africa aggregate and -1.6% for Sub-Saharan Africa.  Despite the IMF being prone to contrive optimistic projections that fail to materialise, this time it provides alternative dreadful scenarios for the evolution of the pandemic. Yet, they seem to be too hopeful. Seeing that the base case for the pandemic will almost inevitably cause this debt-based economic system to fall apart, if any worse scenario for the coronavirus evolution occurs, the collapse of the dollar standard is in the bag, prolonging the depression even further.  Additionally, the social implications of the economic lockdown are extremely dire. Individuals are losing their jobs and, consequently, their incomes. By having a more diminished wealth, their standard of living is going to be severily reduced. Hence, expenses on both healthcare and nutritious food are bound to drop, leading to shorter average lifetimes and higher mortality rates. To make matters worse, the social fabric will deteriorate tremendously, causing suicides and crime-pushed fatalities to skyrocket. Therefore, far more people, especially young and middle-aged individuals, will die because of the economic downturn than from the COVID-19.

At least the politicians know the shutdown of economic activity gives rise to the freezing of the cash flows for businesses and the income streams for individuals, as well as the complete standstill of credit origination, which is the bloodlife of this monetary and financial system. Accordingly, governments and central banks are compelled to meddle in their economies, which takes us to the way the well-intentioned policy makers are hampering the economic recovery. Secondly, so as to counter the economic debacle, the keynesian technocrats, especially at the Fed and the US Treasury, have been coming up with a more preposterous programme or policy after another. However, the bailouts for corporations, Main Street businesses and households, and the ever increasing liquidity injections to the financial system are precluding the malinvestments done post-GFC from being corrected. Furthermore, governments' actions could discourage people from looking or going to work due to overly generous unemployment benefits and other policies, such as the Universal Basic Income. As a result, inasmuch as the pool of potential workers shrinks and businesses and individuals continue to be constrained by high levels of debt, the output will struggle to get back to where it was two months ago. If individuals and businesses were allowed to go on default and on bankruptcy, the debt would be wiped out and, thus, the economy would grow much quicker for there would be less debt weighting on it. To add insult to injury, the maintenance of the status quo pursued by the governments, central banks and supranational institutions is impeding the distortions on the production structure from being rectified. There is a myriad of businesses that are only alive because of extremely cheap and easy credit. The so-called "zombie" companies can only get enough cash flow to pay their operating expenses and service the debt, but are unable to pay off the debt principal. These companies, for being unprofitable, they do not create value. In fact, the "zombies" are just the tip of the iceberg. As you become aware by reading the Austrian Business Cycle Theory section, the boom is prompted by a subdued interest rate that results in an unsustainable production structure that will eventually crash. In a real capitalist regime, interest rates are not manipulated by central planners. Instead, they are a function of savings and the time preference (learn more here). Therefore, if the interest rates were allowed to adjust by the free market, it would not be just the "zombies" to die at last, but several businesses would vanish or would have to restructure in order to survive. Only then could the economy grow sustainably, reflecting the pursuit of each individual's best interests. In conclusion, in both instances - policies to restrict the COVID-19 spread and interventions to tackle the economic issues aroused by those policies - the governments and central banks come to the rescue, the economy and society come out, nevertheless, in an even worse shape. By looking at protests that are starting to occur, like the one in Michigan, it seems people are beginning to wake up and realise that the governments' cure is worse than the disease. In this week, stocks went higher, sovereign bond yields remained constant overall and spreads of the corporate bond yields became tighter, in both sides of the Antlantic. Foreigners continue to sell US Treasury securities, while the Fed's liquidity swap arrangements with other central banks have apparently plateaued. The Fed has also kept on collecting Treasuries and the dollar has been losing strength, though liquidity contraints seem to be disappearing. However, the real world carries on crumbling down. To begin with, on the US stock market, the S&P closed up 12.1% this week, for its best week since October 11, 1974 when the S&P gained 14.12%; it is 17.79% below its intraday all-time high of 3,393.52 from February 19; and it is 27.28% off its 52-week low of 2,191.86 on March 23. In addition, the Dow Jones closed up 12.67% this week, for its best week since March 23-27, when the Dow gained 12.84%, and the second best week since June 1938; it is 19.78% below its intraday all-time high of 29,568.57 from February 12; and it is 30.23% off its 52-week low of 18,213.65 on March 23.  In the midst of a global economic freeze, how can stocks be surging at one of the fastest paces ever? Answer: the Fed in tandem with the US Treasury coming up with innovative ways to intervene in the markets and prevent prices and rates from reflecting reality. Besides all the facilities and rate cuts the Fed has made or commited to make, on this Thursday, April 9, the Fed announced that it will provide as much as $2.3 trillion in additional loans during the coronavirus pandemic, including starting programmes to aid small and mid-sized businesses, as well as state and local governments. Moreover, these Fed's loans and facilities are based on the additional capital the Treasury has made available under the CARES Act. Of the total $454 billion that Congress appropriated to backstop Fed facilities, this morning’s announcement appears to commit $195 billion, leaving the majority of funds available for other purposes or to expand these programs if necessary - which they will. In a nutshell:

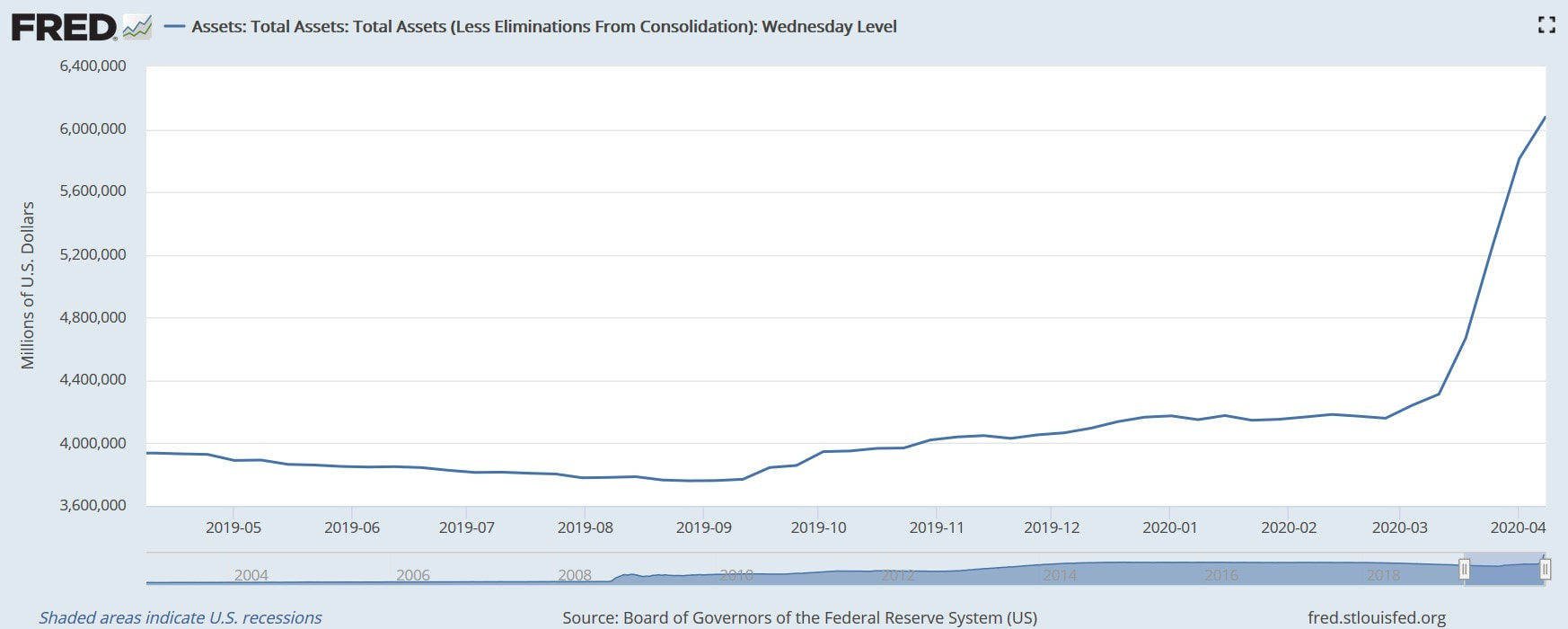

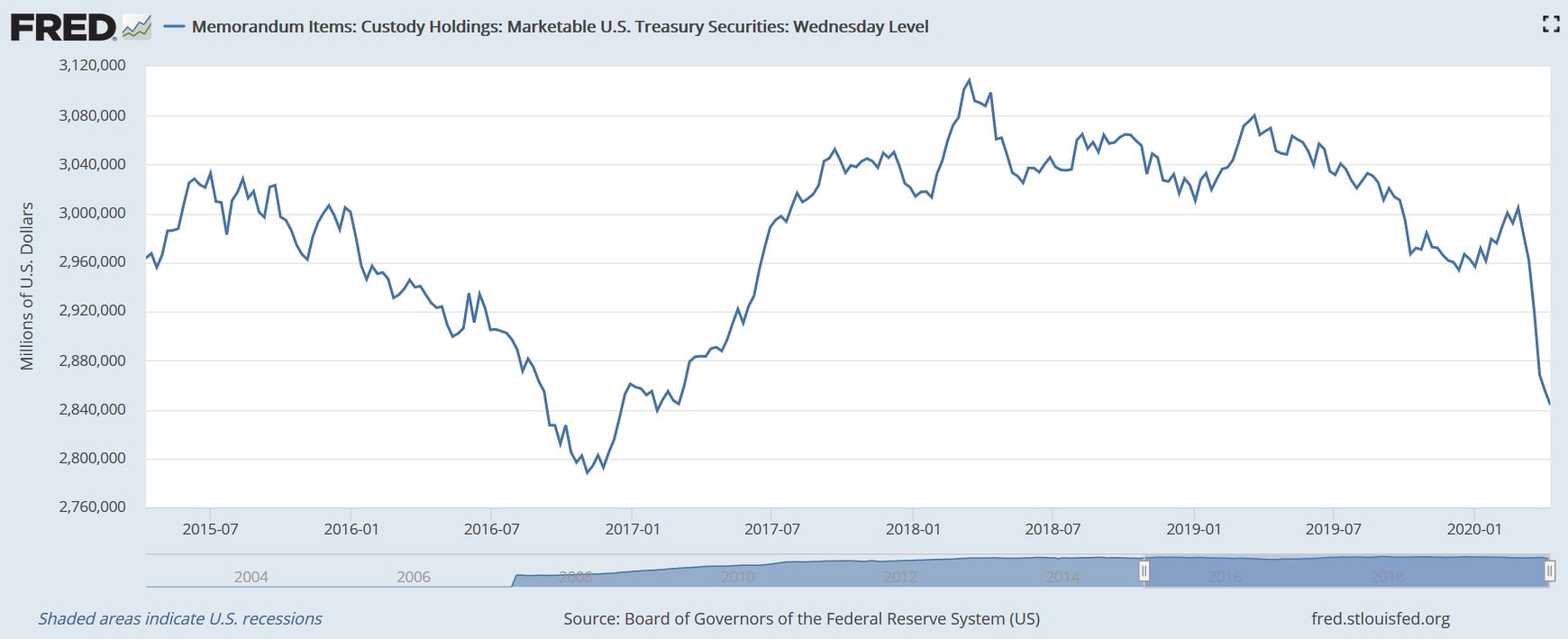

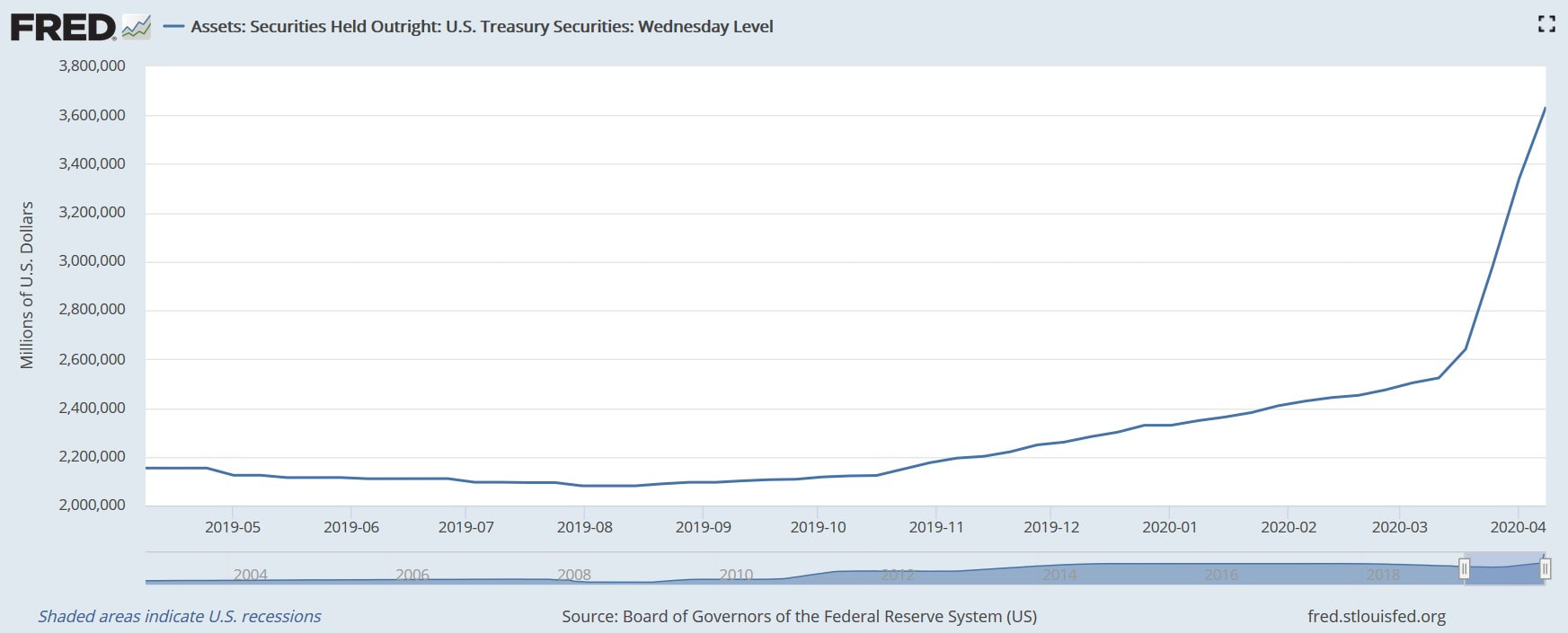

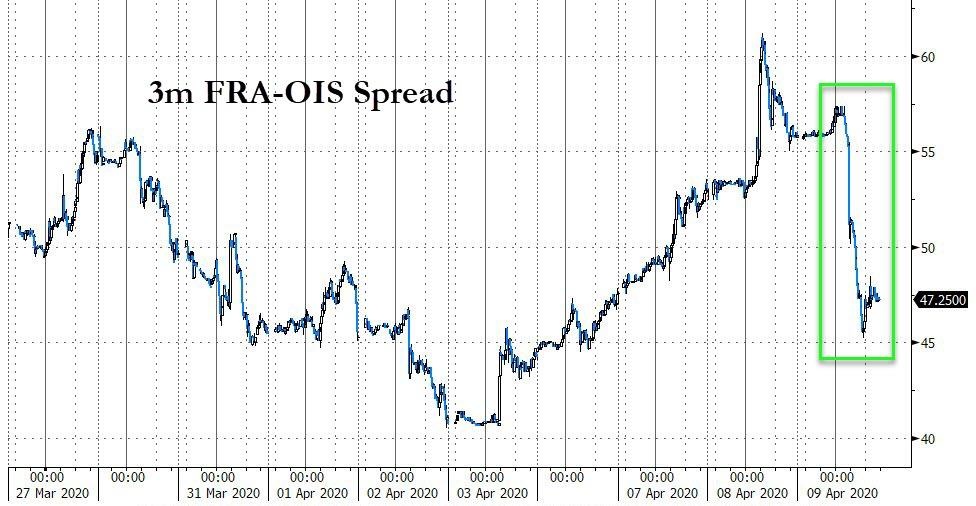

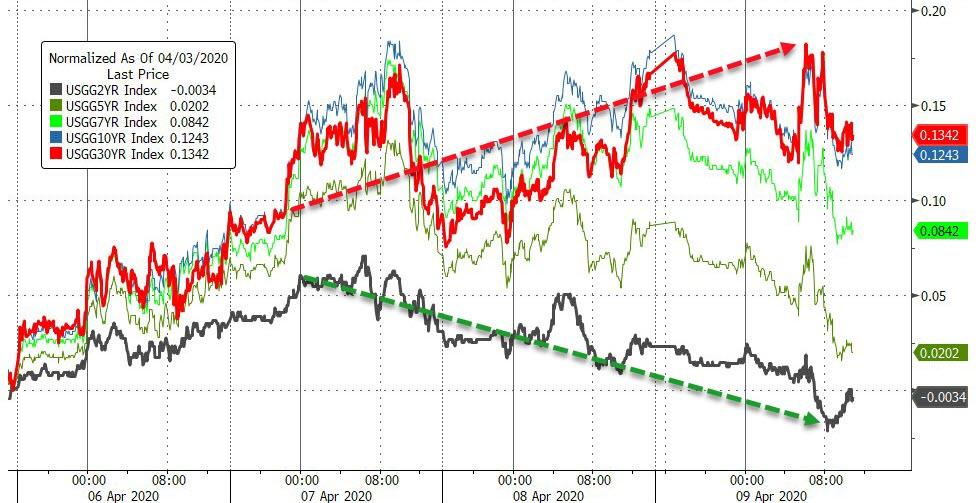

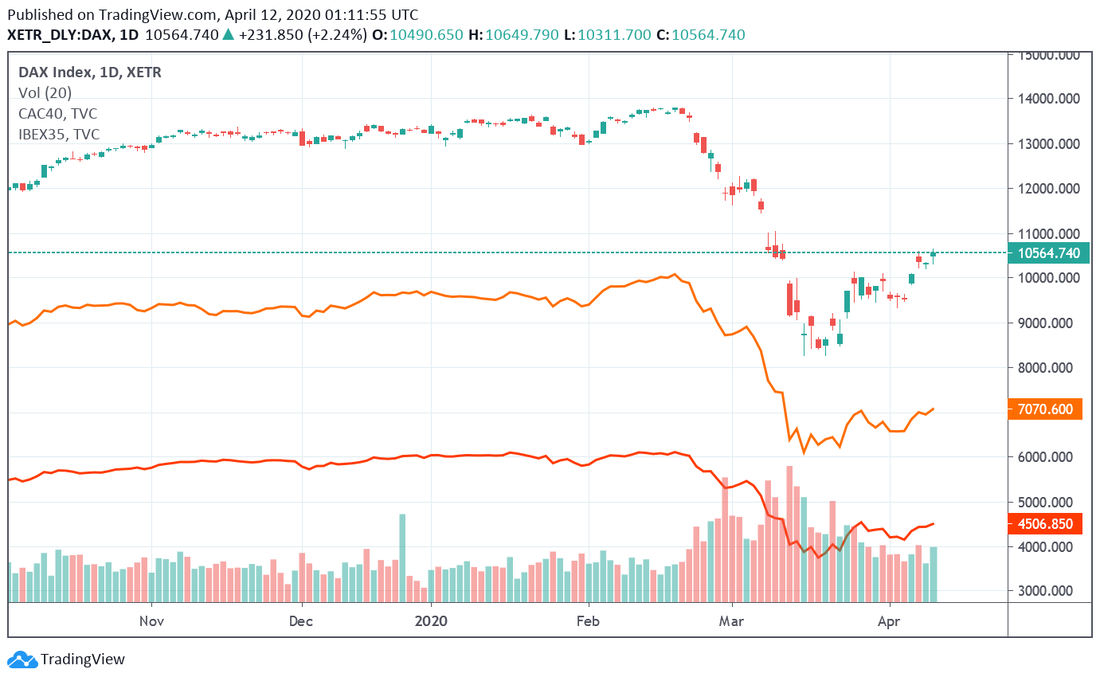

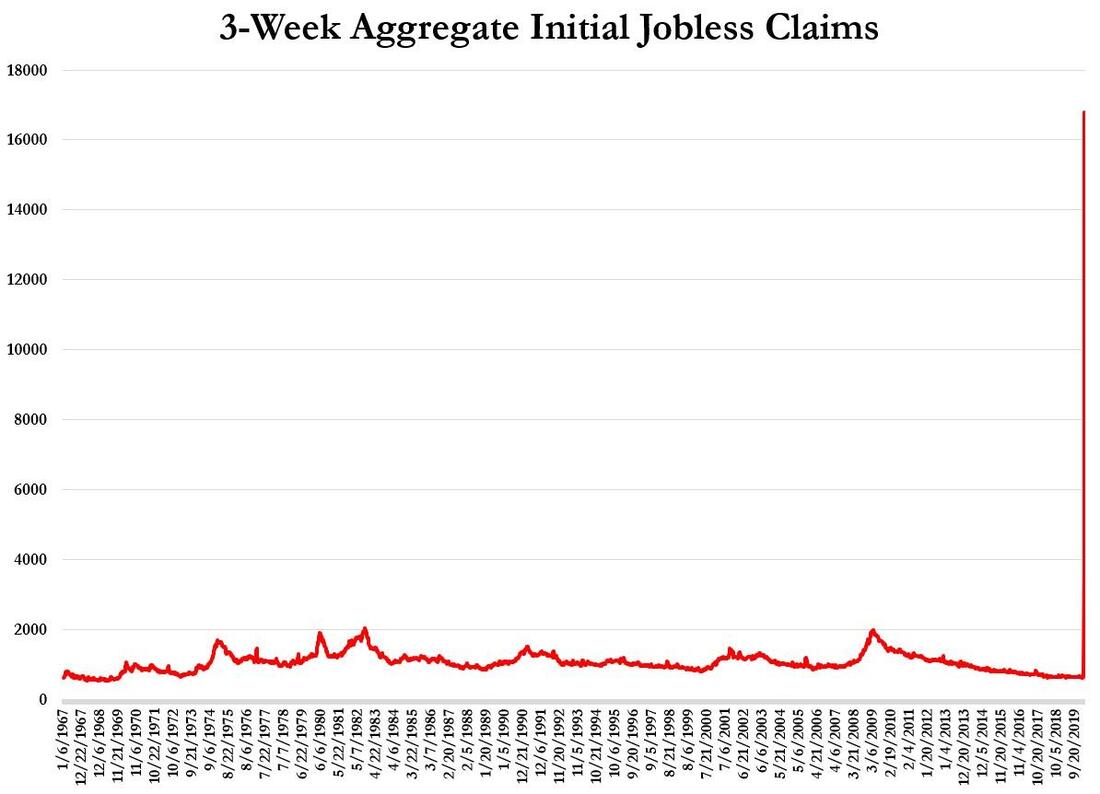

Likewise, the Fed's balance sheet has been soaring at ludicrous speed. Just in the week ending April 8, the total amont of assets in the Fed's possession was $6.083 trillion. Since March 11, total assets increased by about $1.771 trillion.  As I previously stated, the Fed expanded its central bank liquidity swap lines and established the FIMA repo operations to deter foreign monetary authorities from getting rid of their UST holdings and, consequently, to prevent the yields of the Treasuries from shooting up, so that these foreigners would get their much needed dollars from other sources. Hence, for the last weeks, the amount outstanding on those dollar swap lines have been increasing, though they remained at the same level this week compared to the previous one: on March 19, $162.49 billions; on March 26, $308.06 billions; on April 2, $395.86 billions; and on April 9, $396.65 billions. Additionally, the foreign holdings of US Treasuries held in custody at the Fed continues to plummet. On March 11, the amount in custody was $2,961.62 billions. That value diminished to $2,843.67 billions on April 8. Therefore, in the last 4 weeks, foreign officials and other international authorities with accounts at the Fed dumped, aproximately, $118 billions.  This decline may be explained by the FIMA repo operations. In such scheme, these foreign authorities are able to exchange Treasuries held in custody at the Fed for USDs. In spite of the alleged scrambling for dollars via the FIMA repos, the amount of Treasuries held by the Fed has gone up much more than what would be enough to absorb those repos. On March 11, the USTs held by the Fed added up to $2,523 billions. In the folowing four weeks, the amount increased by around $1.111 trillions to $3,634.39 billions, on April 8. This means the Fed now owns something like 15.1% of the federal government debt, which surpassed the $24 trillion mark this week.  By looking at the graph below, you can see the dollar liquidity became more stressed till Wednesday, April 8, having alliviated significantly on Thursday. Accordingly, only when those facilities mentioned above were announced, did liquidity concerns rest.  However, the dollar decreased nonstop all week. Although there had been liquidity uneasiness, there was no rush to cash. Usually, when this kind of stress arises, there are flights to safe havens, such as the greenback. Thus, seeing that the USD went down at the same time liquidity stresses were present, this could be a sign the faith in the dollar is being lost.  Moving on to Treasury yields, despite the Fed having accumulated more US notes and bonds in its possession, their yields rose, implying that the demand for them decreased.  Yet, the perceived sovereign credit risk has waned slightly. Since the US risk of insolvency went down while the yields of bonds plus the stock market climbed, investors must be thinking the global lockdown is about to end. Or is there another reason?  Furthermore, corporate bond yields are having their spreads tighten, specially the HY bonds which is not a surprise when you bear in mind the Fed is going to take as collateral (or purchase rather, to speak correctly) junk bonds.  Across the pond, sentiment has ostensibly started to turn around. Even though the daily number of cases and deaths due to COVID-19 refuses to subside, investors seem to take the view the worst has passed.  Although the Euro Area finance ministers failed to reach an agreement to aid the poor and fragile South in supporting their economies, the European stocks rallied this week. (CAC 40 in red and IBEX 35 in orange)  Inversely, in the actual world, the lockdowns persist and the economic indicators have begun to rear the economic halt's ugly head. This week's figure of the US jobless claims stands at 6.606 million. In the last three weeks ending on April 8, 16.78 million people have applied for unemployment benefits, as the chart below demonstrates.  Finally, considering that the economy is contracting at an unheard of pace to most of us, how come are the stock and corporate bond markets surging, the US sovereign credit risk lowering and the dollar liquidity constraints vanishing as well? The reason are the machinations of the central bankers and the keynesian technocrats. With the Fed commiting to intervene in every realm of the financial spectrum, the Fed has become the BUYER of everything. In addition, its interventions preclude the healthy and essential process of price discovery. Therefore, there is no asset price that is still brought about by market participants acting in their best interest, without the distorting influence of the Fed. Instead, everyone has become complacent in this Fed ruled paradigm, where everyone expects the Fed to come to the rescue once problems ensue, even if it means the Fed and the other central banks have to buy every asset of every market, in order to prevent losses for the participants. On that account, it is no wonder the price-to-earnings ratio (P/E) of the S&P 500 has just exceeded, by some estimates, the previous high of the Obama/Trump bull market, reaching a multiple of 19.4x.  To conclude, the pretext for what has been happening in the last few weeks with the utterly opposing trends in the financial markets and the real economy is the Cantillon effect - check out the Inflation section to find out more - on steroids. The US stock market has had one of its best 3-week performance, while the economy is halted almost completely and with the joblessness numbers skyrocketing to levels never seen before. Therefore, there is no shadow of doubt the markets have been moving, not by the fundamentals of the actual economy, but by the inflation whims of the Fed and the other central banks.  The COVID-19 is serving as an excuse for the eurocrats to further their federalistic agenda, approaching the outspoken objective of the power-grabbers of the likes of Jean-Claude Juncker to turn the European Union into the United States of Europe. The creation of the eurobonds presupposes the establishment of an institution like the ECB regarding fiscal and budgetary policy. Therefore, each member state would have to give up more sovereignty to a federal government. In a scenario where the harmonisation of rules and regulations carries on in this pan-european federation, all kinds of laws regulating businesses, labour or taxation, like a federal minimum wage law or federal income and corporate taxes, will in all likelihood be implemented, making the almost inexistent catching-up process an impossibility. Firstly, the harmonisation process in tandem with socialist and "green" policies in the peripheral european countries of the Euro Area (EA) have been hindering productivity growth and making them get under piles of debt. Since the formation of the European Monetary Union, the South, which consistes of Greece, Ireland, Italy, Spain and Portugal, has been lagging behind the North, i.e. Austria, Belgium, Finland, France, Germany and the Netherlands. In the South, the workers' unions have a lot of influence among policy makers and the public in general supports job security above labour market flexibility. In this societies, it even pervades the marxist belief that businesses only exist through the exploitation of the workers. All this foments an anti-business environment, deterring investments from being made and, thus, productivity struggles to thrive. As a result, the structure of production did not manage to flourish into a semblance of the northern manufacturing powerhouse. Moreover, the directives coming from the European Comission and other institutions of the EU promoting the harmonisation of policies hurt the South more than the North. The regulatory framework has imposed either more costs or limited production (quotas). The South had to start complying with the same regulations and practices as the North, jacking up the costs of production. For the South could only compete with the North by having lower compliance costs, besides lower labour costs - to compensate the lower productivity -, these measures have helped to foster current account (CA) imbalances.  To add insult to injury, some investments that were made harmed those economies as a whole, making these nations even more unfriendly to businesses. I am talking of course about the ironically unsustainable renewable energy projects. These are very expensive and are only "financially viable" through government subsidies, tax relief or curbing the competion from fossil fuels. Hence, energy costs shot up for households and businesses as well, holding off potential investors. Furthermore, there is a popular misconception that the culprit for the southern nations' debacle is the euro. Such a belief is like an alcoholic blaming a brewery or a whiskey distillery for his liver failure. The governments, businesses and households levered up because they wanted, not because they were forced. Obviously, easier access to credit was an objective the keynesians encouraged. As you know, debt is never a problem in their book. Accordingly, the economic agents of the South used that cheap and easy financing more to consume than to produce. Like I explained above, the southern members were not successful in attracting investment to develop their productive structure, due to half-witted policies. Secondly, with the introduction of the single currency, the member states are no longer able to devaluate their respective currencies to even out the CA balance. On account of the structural competitiveness differentials between North and South and persistent imbalances in CA and external lending between them, a divergence in speculative behaviours on financial markets between those two ensued. In more detail, current account surpluses commenced to build up in the North, leading to large capital flows sent to Southern nations by Northern banks. This capital was channeled primarily for consumption. Even though businesses were also the recipient of that capital, they did not manage to increase production - for reasons exposed above - sufficiently to generate trade balance surpluses. As a result, investment bubbles were fueled and consumption boomed too. However, this was not supported by an increased productivity. Commencing in 2011, doubt for the solvency of the Southern states due to persistent imbalances resulted in the sovereign debt crisis (SDC). Since the GFC, the imbalances of the CA began to correct, with deficits decreasing, eventually, turning into surpluses. The good times of easy credit were over and the economic agents had to start paying their dues. Demand plunged because of austerity and, hence, the imbalances reduced.  In order to prevent these imbalances from happening once again, it is necessary to have structural reforms. Although the paternalistic stance of the Southern governments was put on hold for a few years, which made them recoup part of the investors' and rating agencies' trust, recently these countries reversed course and started to go back to their old ways of pandering to the electorate and, specially, the trade unions. All these conditions that resulted in the SDC are still present today, though some of them are not at the levels they were prior to the GFC. Thirdly, enter the kung-flu into the picture. Governments of both the South and the North are implementing policies. to safeguard jobs and wages, cranking up unemployment and business subsidies, as well as loan guarantees or moratoriums. Thus, they will certainly increase these programs and come up with new ones, like Spain is, for example, doing, which is pondering some sort of Universal Basic Income, i.e. helicopter money, much like the US and Hong Kong are executing. Consequently, budget deficits and public debts are set to skyrocket. Seeing that the Southerners have extremely tight leeway to increase their debt without prompting the loss in their creditworthiness, they are adamantly advocating the establishment of the eurobonds. Eurobonds are government bonds associated with all EA members. In this way, the interest rate of these securities contemplates the risk of all member states, possibly consisting on an weighted-average of the interest rates of each country. Thereby, the issuance of these bonds is associated with different states, for which credibility varies. There are several reasons for and against this instrument. On the one hand, there are the pros:

Assuming that the Eurobonds are issued, the Southern members would gain leeway to increase public spending, not just during recessions, but during expansions too. As a result, the North would require the South to strictly follow some metrics to force them to keep their books in good financial health. Fortunately, these metrics already exist: the convergence criteria agreed in the 1991 Maastricht Treaty. Naturally, of the four Maastricht criteria, only the sound and sustainable public finances would be considered, as the other three are ceased to exist since the onset of the EA.