|

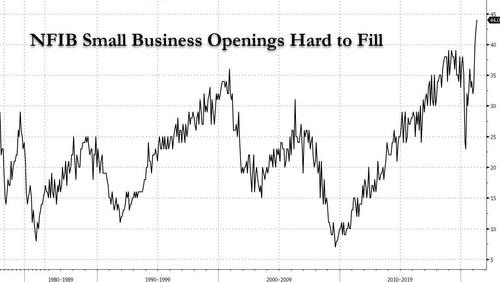

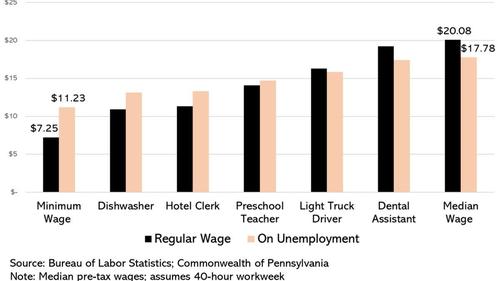

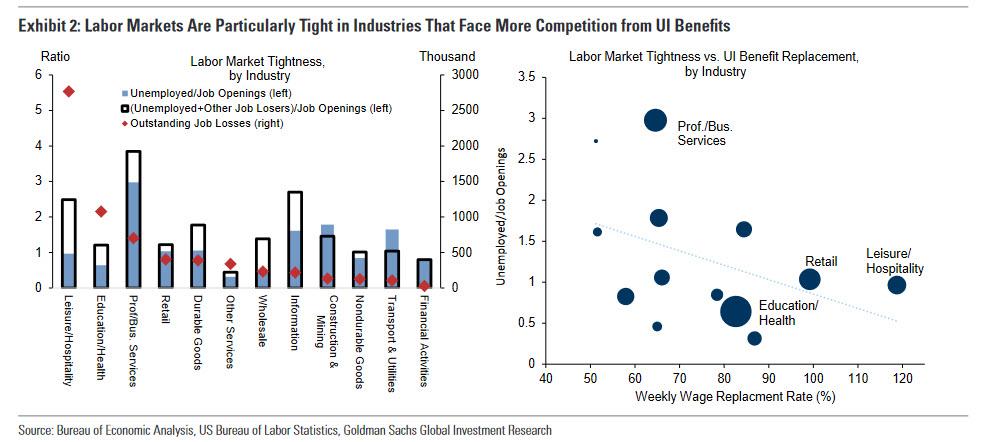

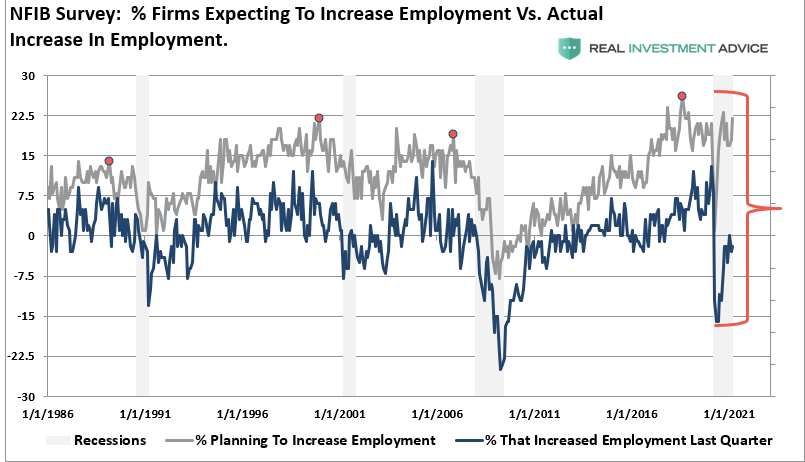

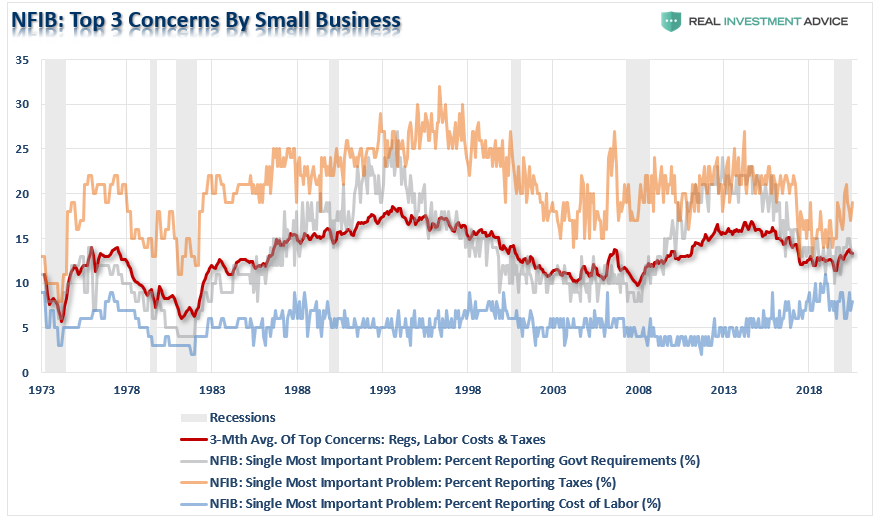

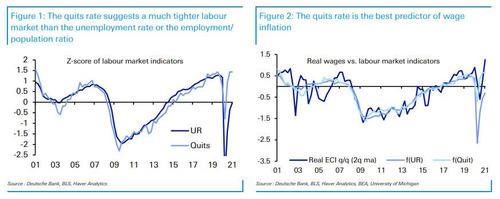

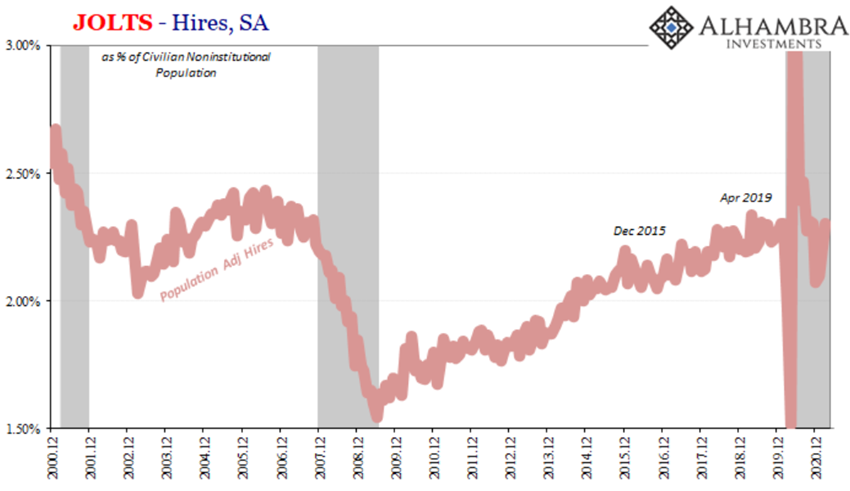

Resuming our recurring subject about the economic recovery (or, more appropriately, the lack of one; such as this or that), the latest NFIB report should not have surprised anyone who has been looking at the data objectively and ignored the mainstream economists and analysts. According to the National Federation of Independent Business, in April, an unprecedented 44% of small businesses struggled to expand their payrolls. which is clearly a great sign, right? That is what the government and the spin doctors want you to believe.  For the bulls, this conspicuous recovery (for some a supercycle) is grounded on those multiple "stimmy checks" handed out by Trump and Biden, as well as governments all around the world, and the unparalleled scale of monetary "accommodation" released by central banks. On paper and if you do not think much about it, it seems like a good plan. However, the consequences are disastrous. Despite this attack (on economic soundness) being two-pronged, impacting demand and supply in distinct ways, the end result is equally bad. As you can easily discern, consumption of goods (not services since the plandemic annihilated them) skyrocketed as a result of these handouts. Unsurprisingly, because businesses were seeing their inventories dwindling, manufacturers began to receive more orders, leading them to increase production. To do this, they have had to expand their staff. Thus, a widespread scramble for workers, initially gave the appearance of a rapid, V-like recovery, coming out of the hole in record-breaking time. However, those hopes turned out to have been completely wrong. In spite of the continual implementation of useless lockdowns and other moronic measures, to "flatten the curve" or something of this sort, definitely leaving a dent on the economy and its prospects for recovery, there has been an extremely detrimental factor for the experienced lethargy. If you have not surmise it by now, the next chart will show you the answer. Quite simply, companies have found enormous difficulty in getting workers due to the government making joblessness so damn desirable. Wouldn't you put off looking for a job if you were making more money laying on the couch, in front of the tv and sleeping all day than you were at your previous crappy job. Considering all that plus the stress and cost associated with the daily commute, even those earning a median wage may have been better off unemployed.  On a positive note, though, there is still a smidge of common sense in the Republican party. In the last month, realising the harm these federal policies are doing to their economies, most Republican-led states have ended, or passed laws to soon terminate these unemployment benefit schemes. As Iowa Governor, Kim Reynolds, affirmed: "Federal pandemic-related unemployment benefit programs initially provided displaced Iowans with crucial assistance when the pandemic began. But now that our businesses and schools have reopened, these payments are discouraging people from returning to work." Backing this assertion, Goldman Sachs has made the same findings. On the left, what one takes from it is that the sectors which had the largest job losses tend to have fewer people applying for a job in those very same sectors. On this account, Goldman's economists, just like every mainstream one, assume that this is an indication of severe tightness in the labour market, especially in the lower-wage industries as the graph on the right demonstrates.  Be that as it may, is the labour market really suffocatingly tight? Although there are those that point at overwhelming tightness, there are other indicators that indicate otherwise. Regarding the following couple of charts, these two, which come from the same survey, nevertheless send mixed signals. The top one, depicts a great struggle to arrange suitable workers. While the other one shows that labour costs have not become more concerning since this covid hoax started. In spite of arousing demand, the "stimmies" effect is short-lived. They merely pull demand forward. After the stimuli do their thing, the demand reverts back to its potential, i.e. whichever level/trend the productive structure is able to generate, which we are yet to discover what it is in this "New Normal" paradigm - maybe Klaus Schwab and Bill Gates already know. In view of the fact that wages are the biggest cost for any business, in order to increment hiring activity, companies have to feel rather confident about the economic prospects. Notwithstanding, the economic potential is tremendously constrained due to the increasing regulatory and taxing strangleholds across the globe, creating all kinds of frictions and raising costs in production, consumption, investment and trade in the whole world economy.   All the same, the Keynesians believe this is all conducive to an inflationary environment. Why? They just rely on spurious correlations between labour data and the CPI or the PCE deflator. For instance, the next couple of charts show that real wages have decoupled from the unemployment rate (UR). Hence, so as to continue rationalising the economy is on the path to recovery, the economists at Deutsche Bank simply ditch the UR and employ (pun unintended) the Quits figure from the BLS' JOLTS survey.  Alternatively, what I think is more likely to explain this high Quits rate is the misleading analysis from these economists and then reporting by the media, which entices disgruntled workers, particularly of those industries bashed by the insanely destructive covid mandates like Leisure & Hospitality, to pursue a higher-paying or more fulfilling career. Obviously, there is nothing inherently wrong about ambitioning a better lifestyle. Yet, they are being deceived about the true state of the economy and its outlook. Sadly, they are going to find out the hard way. Furthermore, another interesting data point from the JOLTS survey is the Hires one. Naturally, if we were in a truly inflationary boom, the amount of hires would have looked more like the reopening months of May and June of last year. Taking into account the freezing cold in Texas and other places in February that froze the labour market too, the March number for Hires should have been much higher. Certainly not on the same level as December 2019, which was a time, mind you, already on the brink of recession with several indicators hinting at that.

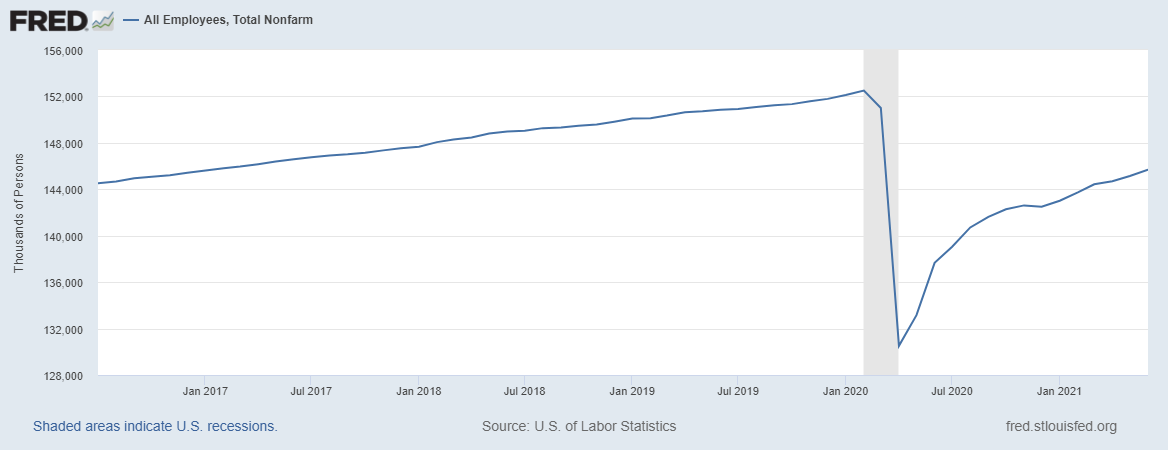

Moreover, to corroborate my point, the total nonfarm payroll is still horribly far from reaching the pre-covid level, not to mention that it is light-years away from what is should have been at had the plandemic never happened and the economy kept on growing at trend. To add insult to injury, the rate of change of labour growth (second derivative) is apparently falling. If it continues like this, which I think it will, then the recovery is not going to occur, similarly to the aftermath of the Global Financial Crisis (the Silent Depression, as Emil Kalinowski dubbed it).  To conclude, seeing that the multiple rounds and various types of subsidies fomented a false sense of economic resilience and vivacity, during a period where the deck is actually stacked against a booming expansion or renaissance - remember there were people truly believing we were entering a new edition of the Roaring 20's; is actually sad how Keynesians fool themselves -, soon the economy is going to fold in epic proportions.

To make matters worse, if the never-ending public health tyranny refuses to cease its devastation, the cost of commodities, labour and transportation is going to continue to rise, taking its toll on the (global) economy, smashing our living standards. Perversely, this will probably lead to more "red-hot economy" and "tight labour market" indicators that will leave the experts scratching their stupid, empty heads. Hopefully, by then, both workers and prospective ones will have wised up to it.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed