|

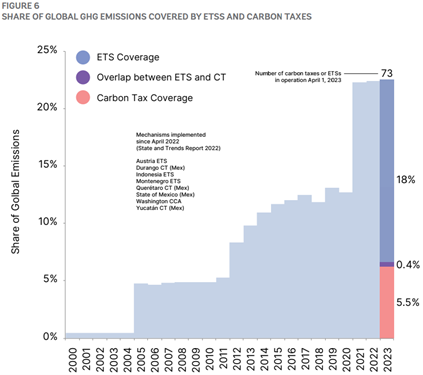

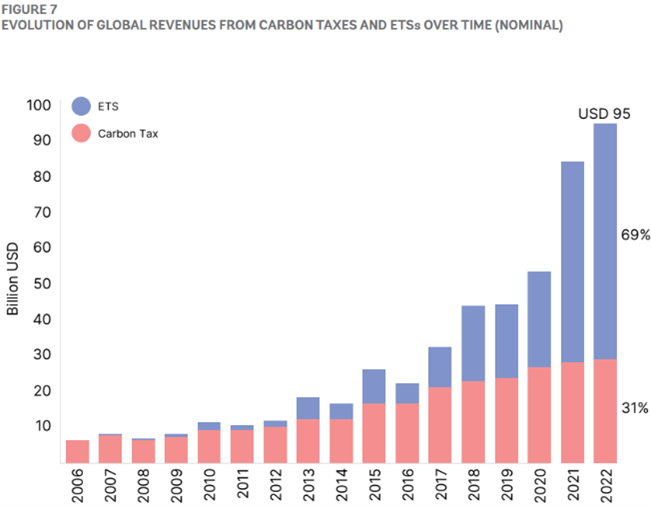

Having finished off the previous instalment by asserting that, after the Kyoto Protocol expired in 2012, voluntary carbon markets were on the cards to replace or supplement the mandatory emissions trading schemes (ETS) that were in place, let me now explore how this all progressed. Be attentive, please, because it may become convoluted. Tracing its origin to a 1966 paper by Thomas Crocker, The Structuring of Atmospheric Pollution Control Systems, the concept of cap-and-trade has haunted us in the last few decades. Ironically, this fellow has snubbed its own brainchild, preferring instead the use of carbon taxes to fight climate change. In addition, he is very sceptic about climate models, claiming that “they are numerical simulations, and as with any numerical simulation, a great deal depends upon what values you attach to unknown parameters.” As elucidated, there was a countless number of projects and stratagems conducted by the familiar environmental organisations and corporations allied with the ‘oiligarchy’ and banking clique to further the fathering of ETSs across the world. Whether regional, national or global, and whether mandatory or voluntary, a myriad of cap-and-trade initiatives began to be devised and implemented. On the one hand, there were those who defended that a global ETS must be erected, eventually. Yet, to arrive at that point, policymakers had to devise them at the regional or national level by decree. Then, a system would be created to allow access between the different geographical carbon trading mechanisms, forging a global cap-and-trade scheme. On the other hand, there were those who argued that, although a worldwide carbon trading system is going to be established sooner or later, this had to be done mostly through non-compulsory means. Likewise, regional and national markets would crop up at first, leading to an inescapable global ETS. Representing the mandatory faction, there was Jonathan Pershing, for instance. Acting as the Director of the World Resources Institute (WRI)’s Climate, Energy and Pollution Program, he contended that the three regional emissions trading programme that were on the pipeline in the US – the Northeast Regional Greenhouse Gas Initiative (RGGI), the Western Climate Initiative (WCI) and the Midwest Governor’s Initiative – could “increase pressure on Washington” to set up a national cap-and-trade system. Discernibly, WRI was a member of the USCAP, the notorious business and NGO coalition pushing this carbon offsets ploy. Sitting on the board of WRI as a Director was also Al Gore, joined by other luminaries, such as Theodore Roosevelt IV and William D. Ruckelhaus, the first US Environmental Protection Agency (EPA) Administrator. While Pershing was at WRI, he was concurrently a facilitator for the RGGI and serving on the California Market Advisory Committee. In turn, this committee was assembled by Governor Schwarzenegger’s Secretary of Environmental Protection, Linda S. Adams, in October 2006, “to develop a multi-sector, market-based compliance system that could permit trading between the European Union Trading System and the Northeast Regional Greenhouse Gas Initiative and others.” Denoting the voluntary camp, one could call upon the several financiers and their institutions, including Al Gore. To wit, Theodore Roosevelt IV who chairs the environmental think tank C2ES, which was a member of the USCAP and has been a chief supporter of various green endeavours, was Chairman of Lehman Brothers’ Council on Climate Change starting from February 2007 up to its collapse. Speaking of the devil, Lehman Bros was a founding member of USCAP, when it was instituted in January 2007. Other examples were delineated on the last episode, such as Goldman’s David Blood and Richard Sandor from CBOE and ICE. Carbon markets have gone through various phases, like many markets, and it has gone through a very fast startup; it reached €100 bn a year very, very quickly and very early on. [T]hen, it got stuck a little bit in neutral by difficult economic times and regulatory uncertainty. What I observe around me right now is a lot of people that have not been engaged in this for a while, or have quietly been engaged, they seem to be back, and they seem to be [in] a mood of optimism and the mood of, I think, we’re back guys, we can take off again.” At any rate, the most predominant organisation to promote ETS at the global scale, either mandatory or voluntary, has been the International Emissions Trading Association (IETA). Presently headed by former Bill Clinton’s climate advisor Dirk Forrister, it not only advocates a global market for carbon dioxide emissions, but also does it for the other purported greenhouse gases (GHGs). To get an idea of how dominant the IETA has been, it was the largest non-government delegation at the 2009 COP15 conference in Copenhagen. Following the adoption of the Kyoto Protocol in December 1997, the IETA was then established in October 1998, with the sponsorship of UNCTAD and the Earth Council, which was chaired by Maurice Strong, to become the successor to the Greenhouse Gas Emissions Trading Policy Forum. Its objectives are to “assist with the development of international standards, protocols and guidelines for, among other things, accreditation, measuring and monitoring of emissions, verification and certification of projects and emission reductions, auditing, and trading of emission allowances and reduction credits.” In IETA’s inaugural meeting, participants included the usual oil companies, UN agencies, financial institutions, environmental organisations, etc., like BP, Shell, NYMEX, IPE, Sandor’s Environmental Financial Products, the WBCSD, and so on. Obviously, as it would continue to happen, its declared mission to create “a plurilateral greenhouse gas emissions market by the year 2000” failed miserably. This endless series of bungle has been impossible to overcome and, thus, forced these swindlers to regroup. Addressing the hinderances they had met up to that point, Andrei Marcu, the founder and first president and CEO of the IETA – now simply an honorary board member –, in a quick interview to Responding to Climate Change (RTCC) – part of the Climate Home News network – admitted that, in spite of progress having stalled, there was “a mood of optimism” and these schemes could “take off again.” This exchange occurred at the 2015 Carbon Expo, from May 26 to 28, as a preparation for the COP 21, in Paris, later in that year. With its first edition in 2009, this colloquium has been organised by the World Bank and the IETA, of course. Frankly speaking, though, we cannot really put it in terms of opposing camps – mandatory versus voluntary. The reality is that these corporations, NGOs and their associates back and finance multiple projects, even if they often seem counterproductive and contradictory amongst each other. Seeing that these groups are not cohesive, with each constituent seeking their own self-interest, they seek a variety of alliances and shift resources to wherever they feel is more advantageous. With that in mind, some USCAP affiliates were also members of the two precursors of the American Coalition for Clean Coal Electricity (ACCCE), the Center for Energy and Economic Development (CEED) and the Americans for Balanced Energy Choices (ABEC). Interestingly, launched on April 17, 2008, ACCCE was “a partnership of the industries involved in producing electricity from coal.” Be that as it may, it vowed to support “the development and deployment of advanced technologies to further reduce the environmental footprint of coal-fueled electricity generation – including advanced technologies to capture and safely store CO2 gases.” As a result of these attempts to cartelise and consolidate the economy, a struggle for power emerged among the differing pressure groups. Due to being aware of the machinations in course which would entail a technocratic revolution, where the corporate overlords and state apparatchiks would take the reins of every market, the weaker and less well-connected had to assemble to try to counter this offensive by the ‘oiligarchical’ and financial elites. Besides coal producers, in those lobbying organisations were utilities, railroads, manufacturers of all sorts and every kind of party in the supply chain that benefited from having that cheap and reliable fuel to boot. Therefore, these smaller players, albeit borrowing some corporatist approaches to get a piece of that glorious globalist action, ended up delaying, as well as complicating, the technocratic plan. Notwithstanding, “in order to save the planet” the globalists would still need to impel “the industrialized civilizations [to] collapse”, as the then co-chairman of the Council of the WEF, among other things, Maurice Strong, so elegantly and eccentrically pictured more than three decades ago, when he and his partners in crime were pushing the still nascent global warming deception and conjuring up the feudalistic Agenda 21. What if a small group of world leaders were to conclude that the principal risk to the Earth comes from the actions of the rich countries? And if the world is to survive, those rich countries would have to sign an agreement reducing their impact on the environment. Will they do it? The group’s conclusion is ‘no’. The rich countries won’t do it. They won’t change. So, in order to save the planet, the group decides: Isn’t the only hope for the planet that the industrialized civilizations collapse? Isn’t it our responsibility to bring that about? Manifestly, the WEF has played that role of megalomaniac syndicate that Strong dreamed up. Once you delve deeply into its history, you will discover that globalist lackeys like Strong propped up the WEF to carry out the tradition set by Cecil Rhodes. If you recall, I showed you that the Anglo-American Establishment was fundamentally the originator of the WEF, through their three stooges: Henry Kissinger, Herman Khan and John Kenneth Galbraith. Nevertheless, it turns out that Maurice Strong was highly influential in this process too, with Klaus Schwab even calling him a mentor on his obituary. All the same, this idea never went away. As a matter of fact, voluntary carbon markets soon became all the rage again. Once the woes that devastated the present-day IMFS, through challenging the prevailing assumptions and models on which the global economic structure laid (especially the developed markets), were eased, though not fixed, those same tricksters jumped back on the climate change bandwagon. Despite that, they have never had to build the green economy from scratch. On account of the infrastructure and beliefs never being completely dismantled, this cadre has always managed to advance this agenda, building upon their previous attempts. Experiencing its ups and downs, the climate change swindle has nonetheless been relentlessly revived and shoved down our throats. Whether you consider California’s case, where a target of 1990 emissions level by 2020 was implemented in September 2006, though the first allowance auction was only carried out on November 2012, or the more recent, ambitious and socialist attempt at the federal level with the Green New Deal, which interestingly coincides with the rise of that annoying little brat Greta Thunberg, this sort of programmes and policies has always stuck around. The next five to 10 years is the most critical time to accelerate the transition to a low-carbon economy. We think capitalism is in danger of falling apart. As a result, the business, which has been fairly reticent in the past about the mechanics of investing sustainably, is planning to increase its visibility. We need to go all in. We are going to be more aggressive because we have to.” After convening for the first time in London, at the IPE’s place, IETA made a habit of arranging annual meetings with carbon market participants – funny that they are now hiding their own history. Initially, these exhibitions were named Carbon Expo, partnered with the World Bank, as we already know. Nowadays, IETA organises Innovate4Climate, Carbon Expo’s sequel, along with regional Carbon Forums in association with the UNFCCC, other UN bodies and international and regional development banks. Recognising the necessity of assuring that the carbon offsets are genuinely produced by actual emissions reduction projects, it was now time to put together industry standards and verifications processes so as to guarantee high-integrity ETS, particularly for voluntary carbon markets (VCM). Naturally, the same old entities were already standing by with those tools to close this putative quality control gap. Basically, there are four main carbon crediting institutions, among a legion of them, that serve both the compliance and the voluntary markets worldwide. For the former they are labelled as Certified Emissions Reductions (CERs), while for the latter they are called Verified Emissions Reductions (VERs). Still, it seems that new initiatives are being set up all the time, as I am going to testify later on. Firstly, the trailblazer has its origins in 1996 and goes by the name American Carbon Registry (ACR). With the assistance of the Environmental Defense Fund (EDF), which sponsored the California Global Warming Solutions Act of 2006 (i.e., Assembly Bill 32) along with the Natural Resources Defense Council – both members of the USCAP –, the Environmental Resources Trust (ETR), a Washington, DC-based nonprofit organisation, was established. Right then, ACR, the first private voluntary GHG registry in the world, was instituted. Undeniably, ACR is a Rockefeller-spawned entity. After all, ETR is a wholly-owned subsidiary of Winrock International. Perhaps you are out of the loop, unable to connect the dots. In short, Winrock is the amalgamation of the words Winthrop Rockefeller, the fourth-born son of John D Rockefeller II. As a result of an incestuous three-way merger between Winrock International Livestock Research and Training Center, his older brother JDR3’s Agricultural Development Council and the Rockefeller Foundation’s International Agricultural Development Service, Winrock International was formed in 1985. Secondly, there is the Climate Action Reserve (CAR). This organisation started in 2001 as the California Climate Action Registry (CCAR), which was developed by the State of California to promote and protect businesses’ early actions to report, manage and reduce their GHG emissions. Only upon the inauguration of California cap-and-trade programme, in 2012, did the CAR crop up and, in conjunction with The Climate Registry (TCR), replace the CCAR. Whereas TCR inherited the task of “providing best-in-class programs and services for measuring and reducing carbon emissions” to governments, businesses, academia and NGOs, the CCAR’s role of a carbon offset registry was passed down to the CAR. Besides California, with the support of its stakeholders, the Climate Action Reserve devises carbon credits for the Washington and international compliance markets, as well as the VCM. Thirdly, launched in 2003, the Gold Standard Foundation modified its methodology, which was originally constructed to adhere to the Kyoto Protocol’s CDM program and its CERs, to then suit the VCMs and their VERs from 2006 onwards. Essentially, the Gold Standard (GS) was forged chiefly by the World Wide Fund for Nature (WWF), which remains a sponsor and a partner of it. For your information, the WWF was constituted by eugenics fanboy Julian Huxley, Prince Bernhard of the Netherlands, founder of the Bilderberg Group and former employee of the IG Farben conglomerate, leading misanthropist Prince Philip of Greece and Denmark, Duke of Edinburgh, and Godfrey A. Rockefeller, great-grandson of William Rockefeller Jr., brother and business associate of John D Rockefeller. Even though its history is a bit murky and intricate, with some more characters worthy of mention, these are the most relevant chaps for our story. Finally, there is the Verified Carbon Standard (VCS), the world’s most widely used GHG crediting programme. Being administered by tax-exempt organisation Verra, at its outset, in 2007, it was known as the Voluntary Carbon Standard until 2018. Furthermore, VCS was concocted by the IETA, the WEF, the WBCSD and the Climate Group too. About the one that is likely totally unfamiliar to you, the Climate Group, suffices to say (for now) that this is a lobbying and networking group where paying members engage with governments, businesses and other institutions to shape the market frameworks that can help stakeholders achieve the Paris Agreement targets. Undoubtedly, this organisation boasts a quintessential stance, getting its funding – for the financial year 2021-2022 – mostly from the typical foundations (45%), corporations (27%) and progressive governments (25%), and being intricately connected to other green, globalist initiatives. All the same, these four premier standards form part of an industry association, dubbed International Carbon Reduction and Offset Alliance (ICROA), which not only accredits entities that offer carbon crediting and emissions reduction services, but also endorses those very same standards. Serving as a testament to the consanguineous nature of this phenomenon, the ICROA is managed by an “independent” secretariat operated within the IETA. In spite of originating in 2008, through the efforts of seven carbon offset providers from Britain, the US and Australia, it only partnered with IETA in 2011. Again, this conflict of interests is staggering. At bottom, these providers were just aiming at cartelising these new-fangled voluntary-ish markets. Similarly, the standard setters and the environmental groups that backed and hatched them later joined this endeavour by creating the Code of Best Practice for the industry. Evidently, this was done in order to consolidate their position and erect barriers to the entry of new standards and offsetting services providers. On this account, they can corral the market and make sure all business flows through this cabal. On page 20, figures 12 and 13, of that report by Ecosystem Marketplace and Bloomberg New Energy Finance, one can clearly detect the dwindling of activity in the VCMs during the 2008-09 GFC. However, as I have expounded before, this has been an ongoing cycle. Catching them by surprise, reality shuttered the lucrative hopes of these guileful, green financiers. As consultancy firm ICF International predicted, the global VCM would grow from 10 mn tons of CO2 in 2005 to 400 mn tons annually by 2010. What actually materialised was a complete debacle, with CCX – “the world’s first and North America’s only active voluntary, legally binding integrated trading system to reduce emissions of all six major greenhouse gases, with offset projects worldwide” –, seeing its trading volumes drying up by 2010. Rather amusingly, Richard Sandor blamed the US Senate inaction on not passing the climate change bills specified in the last episode, such as the Waxman-Markey, for the standstill in the voluntary-ish markets. In any event, as Table 3 of that report referenced above demonstrates, while transaction volumes and values tumbled from 2008 to 2009, declining respectively by 26% and 47%, those statistics experienced the inverse trend for the regulated (i.e., mandatory) markets, up 83% for volume and 7% for value. Indubitably, the Great Recession was vital to annihilate this and other malinvestments that were (voluntarily) generated during the era of the expanding eurodollar system. For nearly a decade there had been a lull in the ETS activity, especially in the VCM segment. At any rate, interest in carbon markets has been facing a resurgence, more emphatically since 2020. Unquestionably, this coincided with the surge of credit, both public and private, that was occasioned during the Covid ‘scamdemic’. Regardless of that respite in the post-GFC voluntary markets, the upward trajectory of the revenues from the whole ETS realm, dominated by the compliance programmes, has been unflagging, as the chart below on the right illustrates. Likewise, that figure shows that the impact of government-enforced carbon taxes on their revenues has too been indefatigable, though at a gentler pace. Because of this push by governments and the globalist supranational institutions, the percentage of GHG emissions that are covered by some kind of mandatory cap-and-trade scheme or carbon tax has reached the noteworthy mark of 23% (i.e., 11.66 GtCO2e), as the graph on the left demonstrates. Still, notice how this progress came in waves, not linearly. All in all, as of March 31, 2023, there were 73 carbon pricing initiatives, meaning ETSs and carbon taxes, already implemented, scheduled for implementation or under consideration across the globe. Comparing to previous years, the development has been remarkable. In 2004, the year before the EU ETS was launched, GHG emissions coverage was only 0.47%., surging to near the 5% level the following year up to 2011. Then, in 2012, when Japan enforced its carbon tax, that statistic jumped to 8.41%. Even though the rest of the decade saw a myriad of direct carbon pricing programmes being implemented, progress was very meagre, with coverage hovering around 12%. That is until China introduced its ETS in 2021, leading to the current figure of 23%.

According to the most recent World Bank’s State and Trends of Carbon Pricing report, published during the 2023 Innovate4Climate event in Bilbao, Spain, revenues from carbon taxes and ETSs swelled $10 bn in 2022, reaching almost $95 bn globally. As you can see, the share of revenues yielded from cap-and-trade initiatives has been ballooning impressively, reaching 69% in 2022, with the remainder 31% coming from carbon taxes. Moreover, 44.2% of these global direct carbon pricing revenues, $42 bn, came solely from the EU ETS.

Understandably, China’s ETS boasts the triple of the coverage that the EU ETS offers. Peculiarly, seeing that it adopts 100% free allocation (through technology-specific, emissions-intensity baselines), in effect, the Chinese government collects almost no revenues from it. To all intents and purposes, the eco-financial clique of Sandor, Gore, Marcu and alike has witnessed the materialisation of their artful ruse. Nevertheless, some tweaks had to be done to their action plans. Learning from past mistakes, efforts have been made to guarantee a high level of quality and integrity of carbon credits and their providers, as well as market mechanisms that are credible and pursue the highest standards. In other words, make sure that carbon providers produce projects that truly reduce or remove GHGs. In case you are still bewildered, carbon credits/offsets can represent emission reductions achieved through either avoidance, for instance by capturing methane from landfills, or removal from the atmosphere, such as sequestering carbon through afforestation or directly capturing CO2 from the air and storing it. Specifically, reduction does not necessarily mean an absolute decrease of GHG emissions, but a curtailment of emissions in relation to the business-as-usual scenario. As I have elaborated on before, the 1997 Kyoto Protocol instituted three flexibility mechanisms: the Clean Development Mechanism (CDM), the Joint Implementation (JI) and emissions trading, whether via exchanges or bilateral agreements. In view of coming up short of expectations in both quantitative and qualitative terms, if they wanted to erect a global carbon market, they had to raise their game. Plainly, for a carbon credit to be firmly regarded as an instrument for “effective climate action” (i.e., of high integrity), its claims of emissions reduction or removal must be real, additional, verifiable, and permanent. This means that the emissions cutback achieved (real) would not have happened in the absence of the mechanism (additional), will have been removed or avoided in perpetuity (permanent), and can be traced back to a specific project (verifiable). That being said, surveying the evidence to verify if CDM offsets comply with those requirements, we find out that the results show a grim picture of this programme. Owing to being relatively insignificant in size, the JI mechanism does not justify a review, though we can surmise it has suffered at least the same shortcomings as CDM. Undoubtedly, the most prominent problem to resolve is that of additionality. Despite early-stage research on their lack of stringency provoked some improvements to be made on CDM additionality rules, a 2016 study by the European Commission still found that 85% of CDM projects, generating 73% of the potential 2013-2020 CER supply, had a low likelihood of occasioning carbon credits which are additional and not over-estimated. Believe it or not, this suggests that the implementation of CDM has, in fact, increased GHG emissions. Astonishingly, in the EU alone, emissions increased by over 650 million tonnes of GHG due to the use of spurious CDM credits in the EU ETS – that represents 15.55% (=650/4180 MtCO2e) of total EU’s GHG emissions in 2016. To keep this light, as I always try to do, this episode will be divided into three parts. Having reached the end of the first one, hopefully you have acquired a somewhat comprehensive grasp of the making and evolution of carbon pricing schemes and of the main characters and institutions enriching this story. On the following part, I am going to explore in more detail the series of events, proceedings and perspectives that have effected and affected the carbon markets and the involving regulatory framework that we now have to deal with, particularly the history of the ESG concept. Lastly, I will finish off demonstrating how and explaining why everyone and their mother is jumping on the sustainability and green economy bandwagon, relating all of this to the prospects of this episode’s matter, emissions trading systems.

0 Comments

|

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed