|

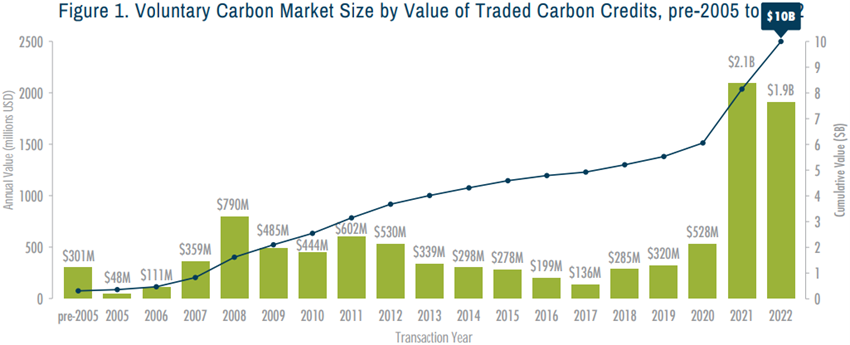

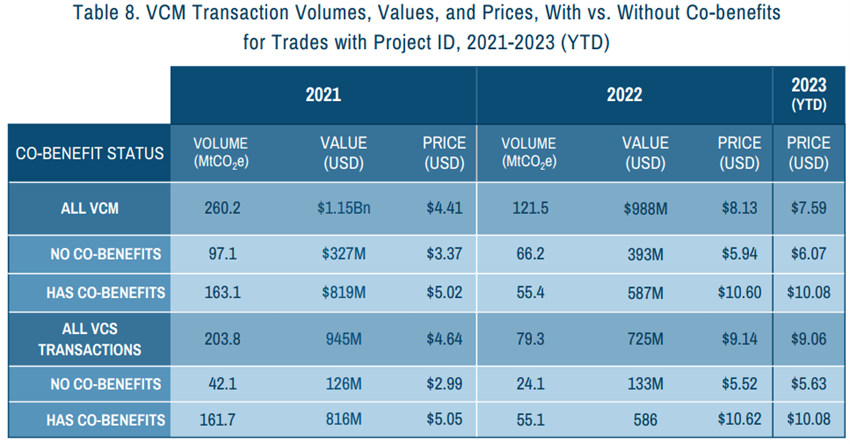

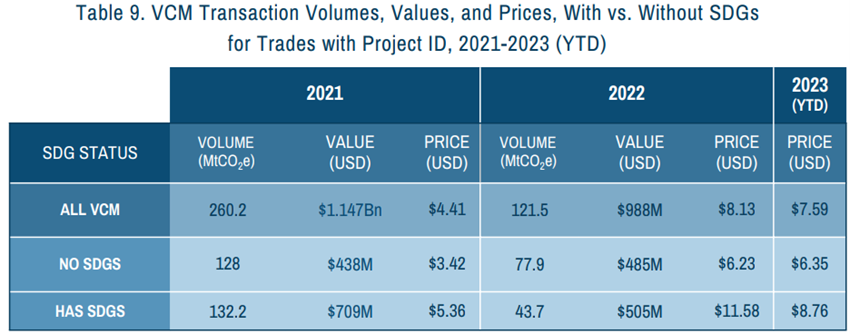

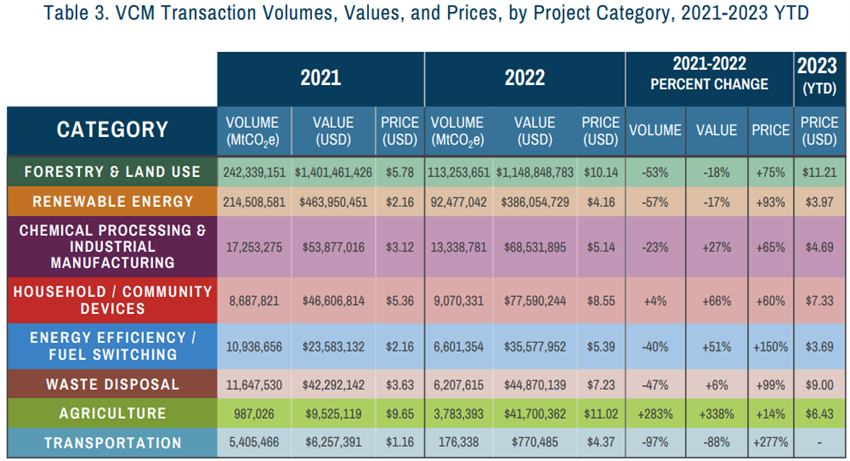

Recalling last episode’s revelations, Sandor’s CCX was effectively shut down in 2010 for having the bad luck of the cap-and-trade bills not passing the US Congress. Discernibly, on account of the Great Recession, the Climategate and, to some extent, the Tea Party movement, the timing was simply terrible and unfortunate. However, time is a great healer, after all. Thus, when all those issues became water under the bridge, the racketeering resumed once again. As I have already hinted at, by 2015 and the COP21 in Paris, the enthusiasm perfusing the minds at these globalist gatherings were able to lift the banksters’ and their puppet environmentalists’ spirits. Yet, this time they were going to make sure their attempts at fulfilling the Agenda 21 would not come to naught. Basically, the swindlers had to multiply their efforts and open new fronts in this ongoing insidious and subversive information war.  Simply put, the carbon market gravy train just could and will not stop in its tracks, come hell or high water. To prevent a repeat of that failure, all manner of propaganda and manipulation has been thrown at the masses. Furthermore, more organisations and pledges supported by the usual ‘oiligarchs’, financiers and the stooges that pervade their foundations have been developed. Drawing upon their recognisable tactics, the employment of the Hegelian dialectic and of useful idiots as controlled opposition would not have caught anyone off guard. In any event, what the globalists pulled out of the hat is quite unbelievable, even for their standards, not to mention dumbfoundingly insane. Seeing that this story is shrouded in an intricate plot, a whole instalment of this saga is going to be dedicated solely to this theme. All the same, carrying on with today’s exposition, the Paris Agreement aimed at solving these reliability problems around carbon crediting. As part of this accord, an item that stands out is Article 6, which relates to the “cooperative approaches” that governments can engage in to achieve their national carbon reduction and removal targets. To do this, there are mainly two mechanisms inscribed in this article. As covered by Article 6.2, bilateral agreements for the international transfer of carbon credits between countries are encouraged to curtail GHG emissions, whereas Article 6.4 creates a new multilateral mechanism to replace the old CDM. In spite of being approved in 2015 at COP21, like many of the components of the Paris Agreements, negotiations have taken a long time to be finalised, being concluded only at the 2021 COP26, in Glasgow. To wit, the parties to the UNFCCC (COP) and the Paris Agreement (CMA) devised the following articles: CMA 12a, CMA 12b, and CMA 12c. These new rules cover both government-to-government and government-to-private sector markets. Some early signals suggest these new rules will guide the practices of VCM activities. Be that as it may, this whole infrastructure envisioned by Article 6 is going to take some time to be assembled and in operation. According to a report by the Asian Development Bank, it could take until 2026 – 11 years from the approval of the Paris Agreement – for all the requisite measures to be put in place. This forecast takes into consideration the time span (11 years) between the establishment of the Kyoto Protocol, in 1997, and the start of its first commitment period, in 2008. Up to the most recent conference, COP28 in Dubai, held on December 2023, since the COP26 in Glasgow no further rules and decisions were implemented regarding Article 6. Owing to its coercive nature, compliance markets appear to steer the VCM indirectly. Broadly, mandatory cap-and-trade programmes seem to act as primary markets for allowances, credits or offsets auctioned or freely allocated, while VCMs are resembling secondary markets, even more so with pronounced flourishing of the publicly-traded exchanges. Nevertheless, the size of the entire VCM space pales in comparison with the mandatory schemes’. While the ETSs imposed by governments brought in about $65.6 bn (=69%*$95 bn) in revenue, in 2022, the market value of the global VCM totalled $1.9 bn. Obviously, this is at odds with all the financial markets where the secondary markets are much larger than the primary ones. In any event, this may change with time, as the VCM and the compliance markets keep on fusing with each other into a ‘forcefully voluntary’ apparatus, on a global scale. Sensibly, even this last hyperlinked report, made by Forest Trend’s Ecosystem Marketplace, which provides an updated description of the global VCM and its various aspects, acknowledges that “pre-compliance” was the major factor that propelled the CCX a decade and a half ago. Unmistakably, the profiteers were hoping that a national cap-and-trade programme would be erected and, consequently, the buyers of carbon credits were already on the market to get a sort of early bird discount before prices would inevitably skyrocket once it became mandatory for companies to keep a check on their GHG emissions.  Regardless of this obvious motive, the cadre of analysts surveyed by Ecosystem Marketplace (EM) posits that prices, and thereby volume, nowadays are “driven by profoundly different factors” than they were back then. Notwithstanding, the reasons given for their expectation of sustained expansion of VCM activity are all related to following and complying with the climate change hoax and the Paris Agreement, in tandem with the ecological disaster narrative and the SDGs. Stupefyingly, these imbeciles cannot put two and two together and discern that coercion, extortion and chicanery have always been the profound factors. Insofar as international covenants and backstage globalist dealings have dictated this technocracy-esque economic model on businesses, the value of the worldwide VCM is bound to keep on mushrooming. As displayed on the graph above, this growth will continue to encounter some (much needed) obstacles.  Due to variances in the trade reporting frequencies of the EM Respondents, as well as this report being concluded well before the end of the year, the data for 2023 is incomplete and goes only till the 21st of November; ergo, only the average prices, during this period, are shown. Moreover, I am going to present the reasons for the slowdown in VCM activity later on. Following suit on recommendations made by the Paris Agreement, in which the decisions on paragraphs 6.2 and 6.4 showed consensus for the need for transactions to address sustainable development, and environmental and social safeguards, both the compliance and the voluntary markets have been adjusting to this goal. Per EM’s study, carbon credits derived from projects that, supposedly, provide environmental and social benefits, the so-called co-benefits, in addition to cutting emissions, carry a premium that is reflected in higher prices when compared to the credits without co-benefits.  Similarly, the same thing happens with credits that adhere or not to the SDGs, as indicated by the table above. In view of market participants, on both sides of the trade, wising up to the necessity of investing in high-integrity projects which deliver reliable carbon offsets and assent to the SDGs, it is no wonder the demand for these types of credits is higher than the plain-vanilla ones, so to speak. Bearing this in mind, the variation in volume, value and price that exists among the different project categories signals this preference for high-quality offsets (meaning actual emissions reduction or removal) and adherence to the environmental and social targets, as the previous tables exemplify. This explains the lower price for credits from technology-based projects, such as Transportation or Renewable Energy, since nature-based projects, like those inserted in the Forestry & Land Use or the Household/Community Devices categories, more prevalently produce co-benefits. Pertinently, projects that remove GHGs, whether through natural sequestration from plants or through carbon capture, enjoy a premium over projects which simply claim to avoid emissions. Unquestionably, credits that are real, additional, verifiable and permanent are strongly requested on account of these high-integrity features that the globalist institutions are clamouring for.  Needless to say, this development of the VCM concept has been managed by the familiar characters of this story. Having already introduced this topic on the sixth episode of this series, you are aware that the Task Force on Climate-related Financial Disclosures (TCFD) was instituted amid the 2015 COP21 proceedings in Paris by the Forrest Gump of the financial realm, Mark Carney, with Michael Bloomberg being selected as the helmsman. What you may not know is that this was a stepping stone to another initiative which embraces those neglected environmental and social aspects: the Taskforce on Nature-related Financial Disclosures (TNFD). With the momentous COP26, in Glasgow, approaching, the eco-banksters began making their preparations to steer the discussions and negotiations their way. So as to do this, they announced on July 2020 the TNFD was being created, at first having a preparatory phase running from September 2020 until June 2021. Only then was TNFD formally established, commencing its work on October 2021, just before that contemptible climate-related UN summit. After a long-drawn-out design and development process, with several pilot tests and consultations, the TNFD released its recommendations on September 2023. If somehow you have a sneaking suspicion that the TNFD is the same damn thing as the TCFD, plus a few more fearmongering-induced malarkey, you are absolutely correct. According to that review about their recommendations and guidance, the TNFD builds on the work of the TCFD, as well as the ISSB, the GRI and other standard-setting bodies. Once again from the sixth episode of this saga, the ISSB was spawned from the IFRS Foundation, with the support from the WEF’s International Business Council which just so happened to be the entity that hatched the Stakeholder Capitalism Metrics that has impelled the ESG agenda. Whereas, the GRI was founded by Ceres and is credited with devising standards “for corporate reporting on environmental, social and economic performance.” Throughout that origination process of TNFD’s recommendations, a series of developments were concurrently taking place, which inescapably affected the final result. One of these I have already mentioned on the last instalment, which was the announcement made by GRI and the IFRS that they would collaborate to align the ISSB's investor-focused Sustainability Disclosures Standards for the capital markets with the GRI's multi-stakeholder focused sustainability reporting standards. At any rate, there have been many other relevant circumstances. To begin with, on the 9th of June, 2021, the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board (SASB) officially merged to form the Value Reporting Foundation (VRF), concluding a process that was initiated at the end of November of the previous year. By exploiting the principles-based guidance for reporting structure and content that the IIRC’s Integrated Reporting Framework prescribes, on the one hand, and the SASB Standards’ specific metrics to help stakeholders understand non-financial risks and opportunities in greater detail, on the other hand, this is a match made in heaven. In short, while the former stipulates the how, the latter provides the what. Because of the multitude of frameworks and standards for sustainability disclosure (also called ESG disclosure or non-financial reporting), including climate-related reporting, there has been an effort to consolidate and simplify the corporate reporting system. Sticking to this plan, GRI Chairman Eric Hespenheide affirmed, commenting on the formation of the VRF and the future partnership between these two entities, that the “GRI looks forward to working closely with the Value Reporting Foundation to continue progress towards the vision of a single, coherent system of corporate disclosure.” In turn, this partnership was made public on July 12, 2020, the same month the TNFD began to take form. Nonetheless, more was yet to come, for this ambitious effort gained momentum quite quickly. As a result of their Statement of Intent to Work Together Towards Comprehensive Corporate Reporting, a common standardised reporting framework was now seriously in the making, enabling the overhaul of the economy and the IMFS and, hence, ultimately fulfil Klaus Schwab and his cronies’ utopic dreams. Naturally, one of the facilitators of these discussions was the WEF. In truth, this paper, published on September 2020, almost simultaneously to the launch of the WEF’s Stakeholder Capitalism Metrics, sets out a vision of the elements necessary for an exhaustive corporate reporting procedure which includes both financial accounting and sustainability disclosure, connected via integrated reporting. Perhaps most importantly, this is the first time that the five major players in sustainability disclosure have aligned on a definitive shared vision. Taken together, CDP, CDSB, GRI, IIRC and SASB guide most quantitative and qualitative sustainability disclosures and provide the framework that connects sustainability disclosure to reporting on financial and other capitals – yes, “other capitals”, such as human or natural. Before we move on, allow me to explore those framework- and standard-setting institutions a bit more deeply. Piggybacking on GRI’s concept of environmental disclosure, Paul Dickinson established the Carbon Disclosure Project, now simply styled CDP, in 2000 and has to this day remained its head. CDP works with corporations, cities, states, and regions to help develop carbon emissions reductions strategies and manage their environmental impacts. The decision to change the name to CDP, in 2013, was considered to address the necessity of understanding wider environmental scares beyond the climate change swindle. Even though this organisation manages to finance its operations, in part, through its own services to businesses and the public sector, this only represents a third, more or less, of the total funding; most of it comes from philanthropy, while a bit comes from government grants and from sponsorships. As an offshoot of CDP, the Climate Disclosure Standards Board (CDSB) had been manufacturing a framework for climate risk reporting by corporations, gradually evolving to incorporate disclosures about environmental and social information and technical guidance on climate, water and biodiversity, since its inception at the 2007 WEF’s Annual Meeting in Davos. Seeing that it “was an international consortium of business and environmental NGOs committed to advancing and aligning the global mainstream corporate reporting model to equate natural and social capital with financial capital”, it is hardly surprising to discover that the “CDSB Framework formed the basis for the TCFD recommendations” that prompted this ESG corporate compulsion. Carrying through the IFRS Foundation Trustees’ announcement made at the COP26 in Glasgow that both the CDSB and the VRF were going to be absorbed into the IFRS Foundation by June 2022, the process of taking over CDSB was finalised almost five months earlier, on the 31st of January. This marked the completion of the first part of the undertaking made by these leading investor-focused sustainability disclosure organisations to consolidate into the IFRS Foundation, which actually only culminated on August 1. Creating long-term value requires both a focus on financial and sustainability performance. This means we need tools for measuring sustainability performance just as we have for financial performance. The World Economic Forum and its private sector coalition made a contribution on this front, proposing a core set of ‘Stakeholder Capitalism Metrics’. We are pleased that this effort will provide a basis for the technical work of the ISSB. We look forward to continuing our partnership with the IFRS Foundation in support of the ISSB, during its establishment and as it delivers on its historical mandate.” In view of this amalgamation providing staff and resources to the now expanded IFRS Foundation, the recently conceived board, the ISSB, could have a shot at realising its mission of becoming the global standard-setter for sustainability disclosures for the financial markets. To this point, it was intended that the technical standards and frameworks of the CDSB and the VRF, in conjunction with those of the TCFD and the WEF’s Stakeholder Capitalism Metrics, would bestow the grounds for the technical work of the new board. To facilitate this, by providing recommendations to the ISSB, the Trustees set up the Technical Readiness Working Group (TRWG), which comprised representatives from the CDSB, TCFD, IASB, VRF and the WEF. Until it rolls out its ESG disclosure standards, the ISSB urges businesses and investors to use and support CDSB’s framework and technical guidance on climate, water and biodiversity reporting. In addition, the IFRS, during this period, promotes the utilisation by market participants of the SASB Standards and the continued adoption of the Integrated Reporting Framework to boot. Therefore, the incestuous trait of this state of affairs is plain to see. However, a few more details about these entities’ history ought to be brought up in order to make this point crystal clear. In the midst of the proceedings of The Prince’s Accounting for Sustainability Forum of 2009, the idea of what would become the IIRC a year later was introduced. “The Prince” refers to the now King Charles III of the UK, of course, who established the Accounting for Sustainability (A4S) in 2004. This organisation aims to drive action by finance leaders to fundamentally shift towards “sustainable” business models and a green economy. Inasmuch as the Davos’ crowd and their dystopic vision of society that the stakeholder capitalism paradigm entails are merely the maturation and unfolding of the New World Order envisaged by the Anglo-American Establishment, it is par for the course that the brits are the tip of the spear in the advancement of the globalist agenda. Indeed, Cecil Rhodes would be proud. Owing to the sudden need to restructure the methodology of business administration, compelling companies to abide by the sustainability and inclusivity ideals, the A4S has set out to be at the vanguard of developing practical approaches to accounting. By resorting to research undertaken by the personnel at the Centre for Research into Sustainability (CRIS) – a multidisciplinary, international group of researchers and educators at Royal Holloway, University of London, UK –, A4S would help devise policies and practices to force companies to embed ESG considerations into decision-making at all levels of management. Corroborating this deduction was the A4S’ Executive Chairwoman Jessica Fries, who has led this group since 2008. Essentially, the findings from the research carried out by the CRIS’ faculty, particularly the 2011 case study into the supermarket chain Sainsbury’s by Spence and Rinaldi, shaped “A4S's work to establish the International Integrated Reporting Council (IIRC) and develop an international integrated reporting framework.” In fact, Fries had been a member of the IIRC Governance and Nominations Committee, representing the A4S, till the VRF was absorbed by the IFRS Foundation. Conspicuously, the Sainsbury’s affair has had legs. Prior to being a trustee of the A4S, from 2004 until 2011, Judith Batchelar was “Director of Sainsbury’s Brand with responsibility for all aspects of its product offer, including policy formation on ethical and sustainable sourcing, corporate responsibility and public affairs.” This implies that she has unknowingly been, when all is said and done, a major architect of the stakeholder capitalism model. Other trustees that are worthy of mention are the Special Advisor to the TCFD, Russel Picot, and the former CEO of the IIRC, from 2011 up to 2016, Paul Druckman. Besides this role, Druckman was subsequently a member of the SASB Board and previously had been President of the Institute of Chartered Accountants in England & Wales (ICAEW). Undeniably, accountants have been tremendously pestered by the environmentalists and their masters for their strategic usefulness in pushing this sustainability disclosure agenda. By the same token, the CFOs, who are responsible for overseeing and managing their respective companies’ finances, have also been harassed by these rapscallions. Having said that, the A4S has partnered with some UN bodies and other clubbable organisations to compose the CFO Coalition for the SDGs. Flourishing from the CFO Taskforce for the SDGs, which was launched on December 17, 2019, at the Borsa Italiana, in Milan, the purpose of this initiative was to coordinate the sustainability agenda of CFOs. To accomplish this mission, a set of CFO Principles on Integrated SDG Investments and Finance, and KPIs to set targets and evaluate the implementation of those principles were concocted. Succeeding this taskforce, the CFO Coalition was inaugurated on March 29, 2022, at the UN Global Compact’s Annual Local Network Forum in Dubai. Presently, it boasts 71 members, representing an aggregate $1.5 trn in market cap, and its co-chairs are two executives from Enel, which at the end of 2018 was the second largest power company in the world by revenue, and from the sixth largest asset manager in the world by assets under management – $1,740 bn –, PIMCO (officially, Pacific Investment Management Company LLC). Moreover, as members of the Coalition, the CFOs are committed to implement the CFO Principles inside their respective organisations and to share their experience and learnings with peer CFOs in the broader community of UN Global Compact companies. In turn the Principles were formulated with the collaboration of, among other entities, the UN’s Principles for Responsible Investment (PRI) and the UNEP Finance Initiative (UNEP-FI), which are key partners of the UN Global Compact (UNGC) as well. In all likelihood, you are completely in the dark about the significance of this unholy alliance. Instead of just giving away the ending, let me guide you down this rabbit hole to unveil the origins of the ESG contrivance. Considering the UNGC, this initiative acts as a setting for corporations and their CEOs to assemble and discuss, with the guidance from the UN and intervention from academics, public sector entities and NGOs, how to embrace and pursue the sustainability tenets and goals that the UN has urged since its effective onset on August 12, 2005. Notwithstanding, this ball started rolling all the way back to 1999, when UN Secretary-General Kofi Annan addressed the audience at the WEF’s annual summit in Davos, Switzerland. Because there were elements of the international community that believed in erecting barriers to trade and the open market to protect and favour certain interests of a particular set of well-positioned groups, the global free market that the UN and its affiliated organisations had ostensibly defended was in jeopardy of breaking down. By the way, this conviction in protectionism and central planning has patently remained till this day, which the globalists have laughably claimed to oppose. Visibly, those hurdles are sold to the citizenry of each respective nation with a veil of compassion and solidarity to attain the common good. Far from protecting and trying to fulfil selfish aspirations of some privileged classes, they are merely defending and acting in accordance with the putative universal values pronounced in the Universal Declaration of Human Rights, the International Labour Organization's Declaration on fundamental principles and rights at work, and the Rio Declaration of the United Nations Conference on Environment and Development in 1992 (commonly known as Agenda 21). Ergo, there has been no dispute in regard to the ultimate social, economic and environmental goals. Au contraire, statists and globalists, and C-suite and activists alike have all declared to support the sustainability agenda, albeit the means to pursue it have diverged. Being aware of this situation, the Secretary-General Annan challenged corporate executives to take matters into their own hands. In order to accelerate the materialisation of those objectives, businesses should lobby their governments “to give us [i.e., the UN], the multilateral institutions of which they are all members, the resources and the authority we need to do our job.” Alternatively, they “can uphold human rights and decent labour and environmental standards directly, by [their] own conduct of [their] own business. Admittingly, Annan affirmed that, seeing that “neither side of it can succeed without the other”, this initiative, the UNGC, is vital to sustain the “universal values” so that the “open global market” manages to endure. Whether he was being disingenuous or a simple coincidence, notice the terminology used. In lieu of employing the term free market, he went with open market. Indubitably, the collectivists that dwell in the multilateral institutions and the policy-making bodies at the national and local levels are all in the same page when it comes to the ideology entrenched in their economic and trade policies. Succinctly, the market is only open for those shrewd scoundrels and gutless cowards who consent to the sustainable development deception, consolidating the wealth and dominance of these cronies – 24,243 to be precise, as of February 19, 2024, and counting. Thus, to remain true to their principles and purpose, the C, in UNGC, should really stand for Cartel instead. Despite that, the plot is just getting interesting. In the run up to the June 1992 United Nations Conference on Environment and Development, popularly referred to as the Earth Summit, the UNEP Statement by Banks on the Environment and Sustainable Development was launched on May 1992, in New York, originating the Banking Initiative. Through operating under the auspices of the UNEP, “a broad range of financial institutions, including commercial banks, investment banks, venture capitalists, asset managers, and multi-lateral development banks and agencies” were cast to encourage “the integration of environmental considerations into all aspects of the financial sector’s operations and services.” Afterwards, it was time to beguile the insurance and reinsurance companies. In 1995, the UNEP teamed up with some leading firms from this industry and established the UNEP Statement of Environmental Commitment by the Insurance Industry, with the help from pension funds too. As usual, signatory companies committed “to achieve a balance of economic development, the welfare of people and a sound environment.” Then, these two groups began to cooperate ever more closely from 1999 onwards, until they merged in 2003, founding the UNEP-FI. Even though this initiative has been instrumental in pushing the sustainable development concept on financial institutions as a whole, engendering the Principles for Sustainable Insurance, in 2012, and the Principles for Responsible Banking, in 2019, its most significant project has been the one forged in its early years: the Principles for Responsible Investment. One element of the law governing investment decision-making that is common to all the jurisdictions is the requirement that decision-makers follow the correct process in reaching their decisions. In the common law jurisdictions, this requirement flows from the fiduciary duties of prudence and in the civil law jurisdictions, the duty to seek profitability and otherwise manage investments conscientiously in the interests of beneficiaries. Conforming with the correct process requires decision-makers to have regard to all considerations relevant to the decision, including those that impact upon value. In our view, decision-makers are required to have regard (at some level) to ESG considerations in every decision they make. This is because there is a body of credible evidence demonstrating that such considerations often have a role to play in the proper analysis of investment value.” During the time that the UNGC was constituting its governance framework, in 2005, it partnered with the UNEP-FI to manufacture “the world’s leading proponent of responsible investment.” In other words, the PRI was founded by the world’s largest institutional investors, acting at the Secretary-General Annan’s bidding, with the objective of forcing investors, both asset owners and managers, to go along with the ESG plan.

When this scheme was put in motion, the concept hitherto most similar to ESG was something dubbed “socially responsible investment”. In spite of sounding and looking the same outwardly, the foundations of each movement are different, though not entirely unrelated. Basically, the socially responsible investment kind is grounded on ethical motives, whereas the ESG gambit is promoted as a lucrative proposition. Evoking the words of his boss Kofi Annan, at the occasion of launching the UNGC, the former head of the UNEP-FI Paul Clements-Hunt argued that due to a healthy environment and stable world contributing to a more prosperous economy, the UN’s declared priorities were thereby aligned with the ambitions of investors. All the same, financial institutions were not being easily convinced by the merits of gauging companies’ performance on social and environmental themes. In particular, pension funds were afraid that their fiduciary duties prohibit them from considering “non-financial” factors in their investment decisions. As a result of two pivotal research papers, commissioned by the Asset Management Working Group (AMWG) of the UNEP-FI, released in the beginning of this century, the fund managers were about to come on board. The first one, published in June 2004 at the UN Global Compact Leaders Summit, which is the year after the AMWG was born, was made by this twelve-member group, consisting of mainstream asset management firms and brokerage houses. Albeit long and quite dull, the title of this report, The Materiality of Social, Environmental and Corporate Governance Issues to Equity Pricing, is thought to be the first instance these commonplace words were used together in an official UN publication. In summary, owing to increasing pressure for institutional investors to address these issues, this research was conducted, revealing that the environmental, social and corporate governance aspects were an integral part of successful management, consequently insisting on these being taken into account in financial analysis and in investment management. To address that pesky fiduciary duty ordeal, Freshfields Bruckhaus Deringer LLP, a leading institutional law firm from the UK, produced a report, issued in October 2005, that reasoned that “integrating ESG considerations into an investment analysis so as to more reliably predict financial performance is clearly permissible and is arguably required in all jurisdictions.” Whether we are contemplating common law or civil law jurisdictions, both have rules in some form requiring decision makers to act in the interests of the ultimate beneficiaries. On that account, this assessment argues for examining ESG criteria, not merely to determine the material impact on financial performance, but when it is reasonably believed to be the subject of a clear consensus amongst beneficiaries or when the ESG considerations provide any points of differentiation between equally attractive alternatives. All in all, in their rather simplistic minds, the sustainability-linked notion of responsible investment is more than inoffensive or noble, it is simply good business. In the end, the AMWG, together with some colossal pension funds and other investment firms, established the PRI in 2006, mustering 63 signatories which represented more than $6.5 trn in assets under management (AUM). Needless to say, these figures have skyrocketed since then. As of the end of 2023, the PRI boasted 5,372 signatories, of which 740 were asset owners – i.e., pension funds, insurance companies, foundations, endowments, sovereign wealth funds, development finance institutions, family offices, and some others –, amounting to an AUM total, in round numbers, of $120 trn. Comparing with the other initiatives spawned by the UNEP-FI, one clearly sees that the PRI is the preeminent one. The latest count for the Principles for Sustainable Insurance informs us that it has 159 signatories, including the largest insurance firms in the globe. Although this organisation does not compute the combined asset value of its members, we can infer that it is close to the global grand total of $35.73 trn. Even more impressive, the Principles for Responsible Banking possesses 342 affiliates, constituting $98.7 trn of total assets, which represents approximately 54% of global banking assets. Since we are at it, those $120 trn, as of March 30, 2021, in PRI’s aggregate signatory AUM, when you think about it, is really staggering. Looking at the evolution of the global AUM data, on the surface, the numbers do not appear to be on the money – pun intended! In view of the global AUM figures for 2021 and 2022 being, respectively, $108.6 bn and $98.3 bn, how can the sum total of the AUM of PRI’s members be that much higher? The answer is very straightforward. Those $120 trn reported by the PRI also includes the 740 asset owners mentioned above. For example, in the ranks of the PRI, the fourth largest public pension fund, Caisse des dépôts et consignation, has $1,12 trn in total assets, the podium of the insurance business, Ping An, Allianz and AXA, possess a combined $3.57 trn, the number one sovereign wealth fund, Norway’s Government Pension Fund Global, has accrued $1.55 trn, and even the fifth largest central bank, le Banque de France, carries $2.31 trn in its balance sheet. Right here, these 6 institutions represent $8.5 trn, or thereabouts, in assets. Adding that to the global AUM number for 2021, we get, give or take, $117 trn. Therefore, acknowledging this near overlap, one must conclude that looking for a bank, insurer or investment firm that is not affiliated, in any way, with these supranational entities, is like searching for a needle in a haystack. With the development of principles for the insurance and banking industries, in addition to the PRI, sustainability blueprints now exist for every branch of the financial sector. But it did not stop there. To fast-track financial institutions’ action on decarbonising the global economy, the UNEP-FI has convened several actors from across the financial sector. Starting in 2019, the UN-summoned Net-Zero Asset Owner Alliance was formed in partnership with the PRI; in April 2021, UNEP-FI engendered the Net-Zero Banking Alliance, and the Net-Zero Insurance Alliance was erected in July 2021. All of these member-led alliances unite financial institutions who have committed to achieving net-zero GHG emissions in their portfolios by 2050, in line with the Paris Agreement. Apparently, the globalists have covered all the bases. Every sector of the financial system and the corporate sector have all been captured by the stakeholder capitalists. Now, it is time to go back to the topic of sustainability disclosure, and appreciate how it relates with the carbon trading systems and the technocracy-esque green economy template championed by the banksters and ‘oiligarchs’.

0 Comments

|

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed