|

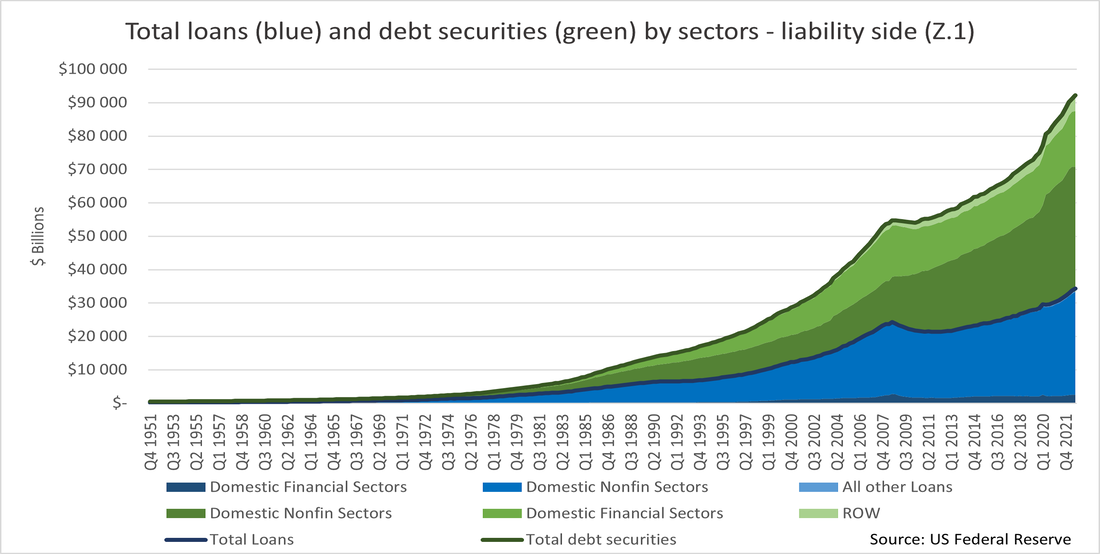

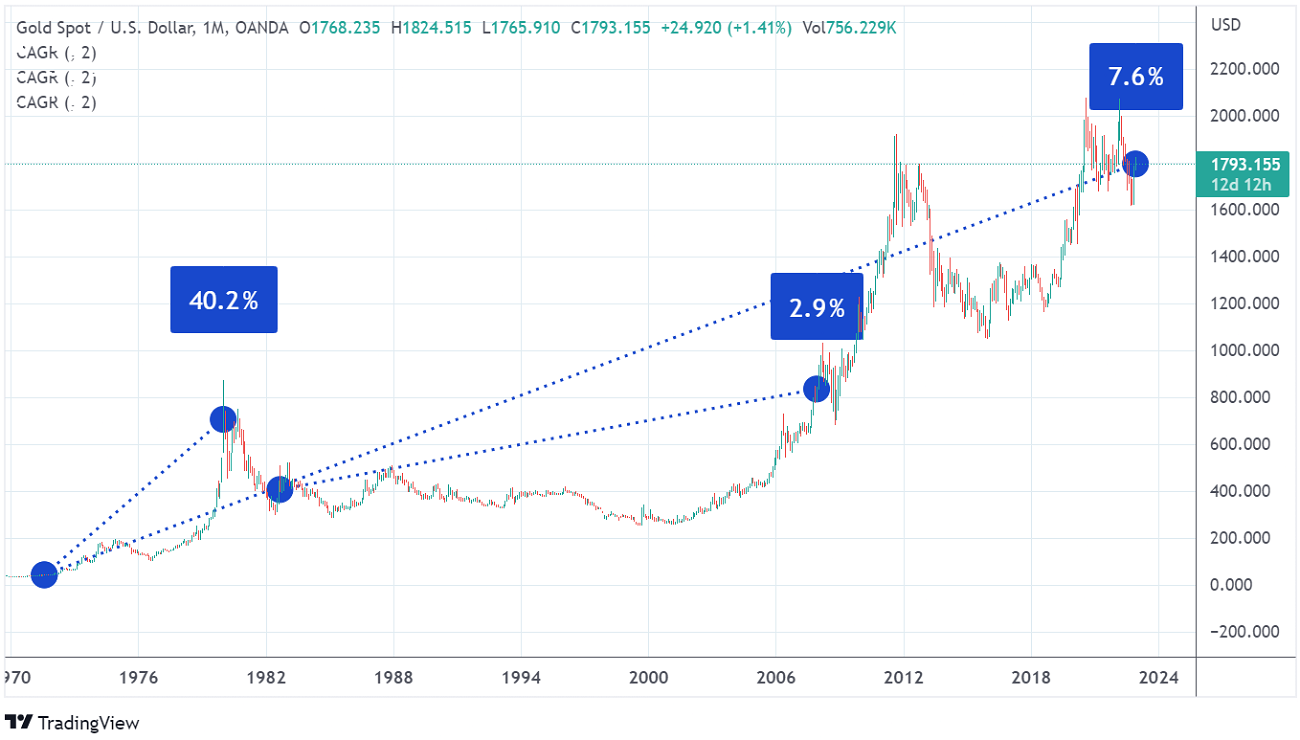

Continuing the perusal set off on the first episode of this second instalment of this three-part series, I am going to focus on the factors determining the price of gold in this post-BW eurodollar paradigm. After showing how the gold market is structured, in terms of the various venues, the different asset classes and the paper vs physical markets dichotomy, I am now going to demonstrate how exactly the Eurodollar beasts affect the gold price. As I mentioned at the end of Part I, the heart of the matter is the London Gold Lending Market, where bullion and central banks gather to carry out gold lending and gold swap activities. Due to these operations being very opaque and secretive, who is actually participating and how much true gold, in lieu of the paper “synthetic” kind, is being submitted in these trades are big unknowns. Be that as it may, that does not stop or prevent us from figuring out and inspecting the determinants governing the performance of gold throughout time. Having said this, there are three facets that, so as to become discernible, depend on the time interval. On that account, I take the view the analysis ought to be divided into the long, the medium and the short terms, with each stretch possessing a unique factor. Starting with the longest term, in the long run, inflation – the real one, without the quotation marks – has been the most obvious influence. Despite the common belief nowadays that the price of gold has failed to keep up with the rate of price surges because of the compelling credibility of central banks, with some even disregarding inflation altogether, the truth is that gold has played its role of inflation hedge pretty well since President Nixon put the final nail in the coffin of Bretton Woods.  Using the Fed’s Financial Accounts (Z.1) data as a proxy for the whole world, we can easily discern that gold has done its job. Albeit far from being a perfect method, it is better to just stick to the US. In fact, the global aggregate data of credit to the non-financial sector has only been collected by the Bank for International Settlements (BIS) since the fourth quarter of 2001; not to mention the debt securities figures which ignore the Emerging Market countries completely. Besides, the American economy may be viewed as a representative sample of the global economy, owing to being a mean, between the blossoming, jovial developing countries, and the stagnant, decrepit European and Japanese markets. Thus, from the moment the convertibility to gold was terminated, total credit of US origin (chart above) has had a compounded annual growth rate (CAGR) of about 8.25% (from Q3 1971 to Q3 2022). Comparing to gold’s performance, beginning in August 1971 and up to December 16, 2022, its CAGR amounts to 7.6% (next graph on the left). Hence, judging solely from these statistics, one can claim that gold is a tiny bit undervalued. Examining the following graphs further, clearly the price of gold does not track the expansion of debt, which has been smooth and relentless, though with an important inflection caused by the GFC. Ostensibly, it has its own boom and bust cycles.

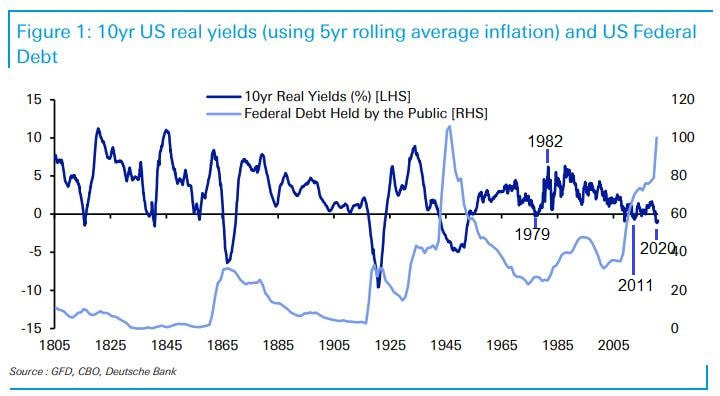

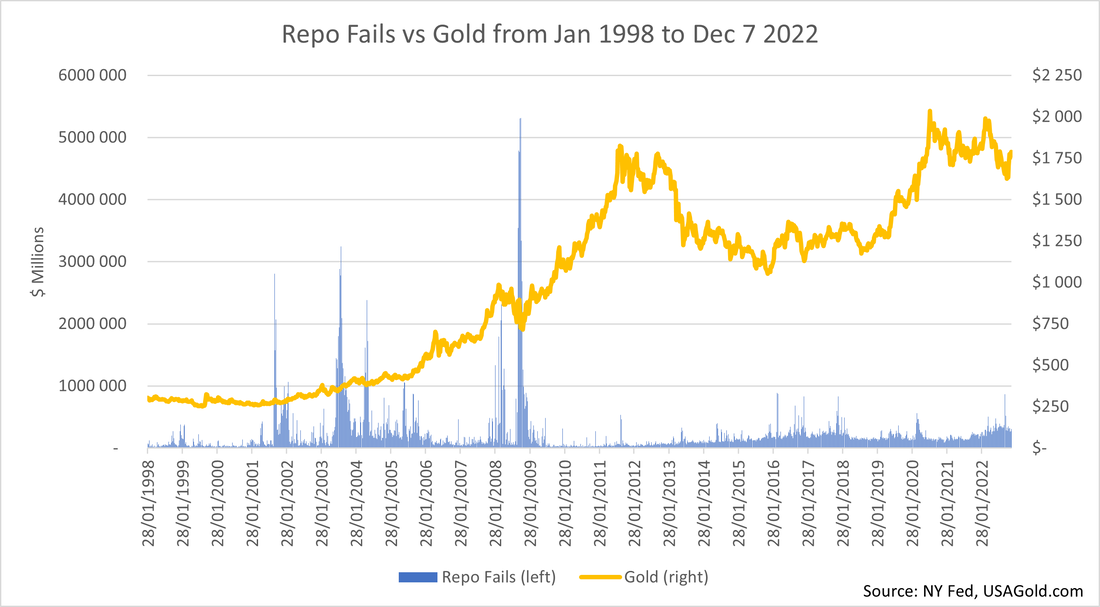

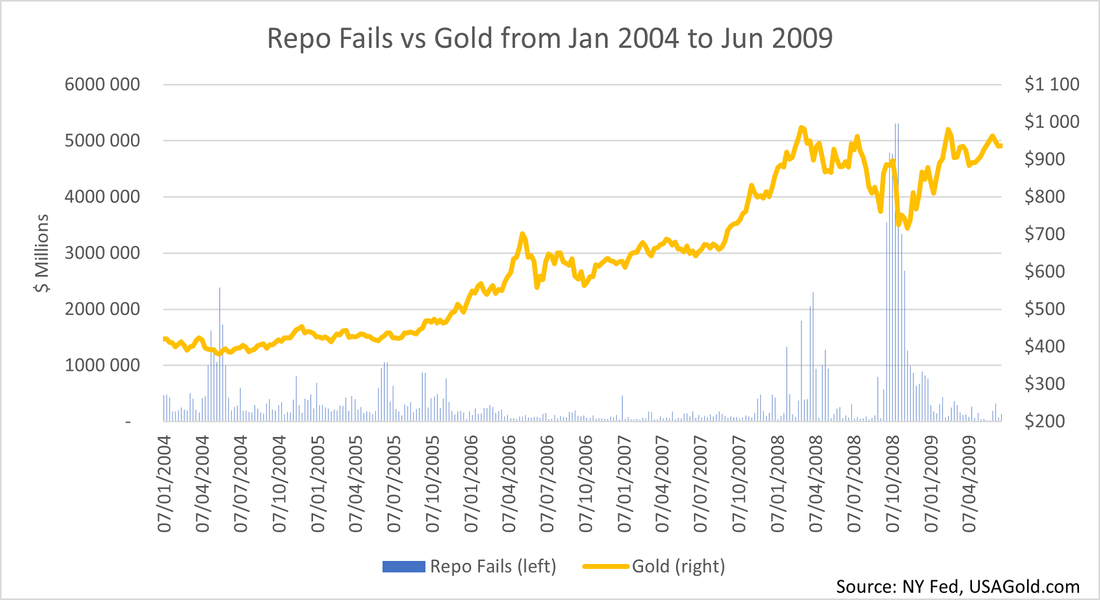

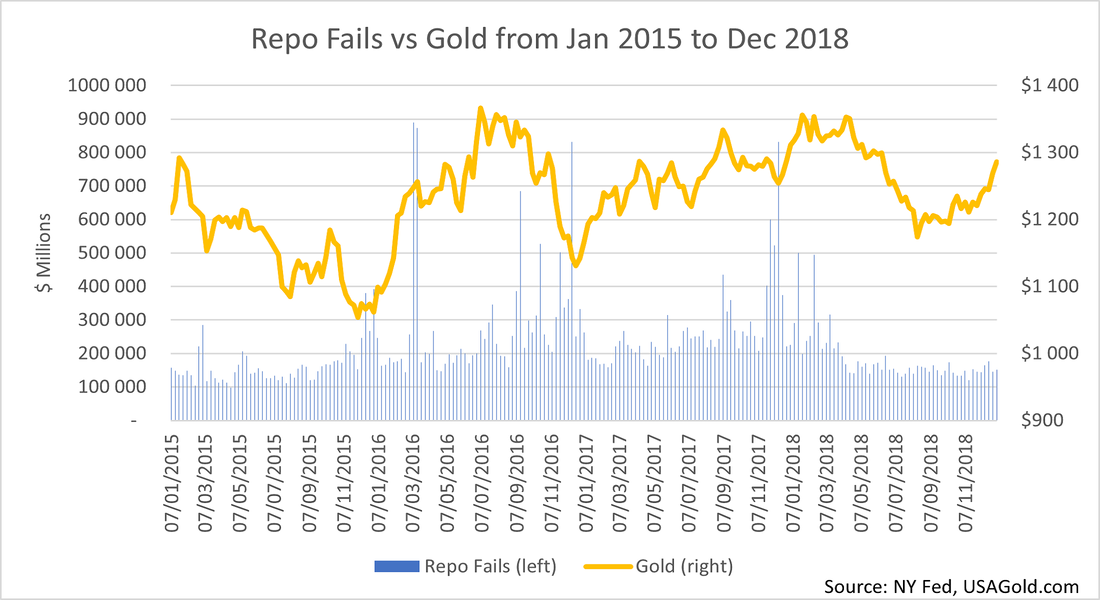

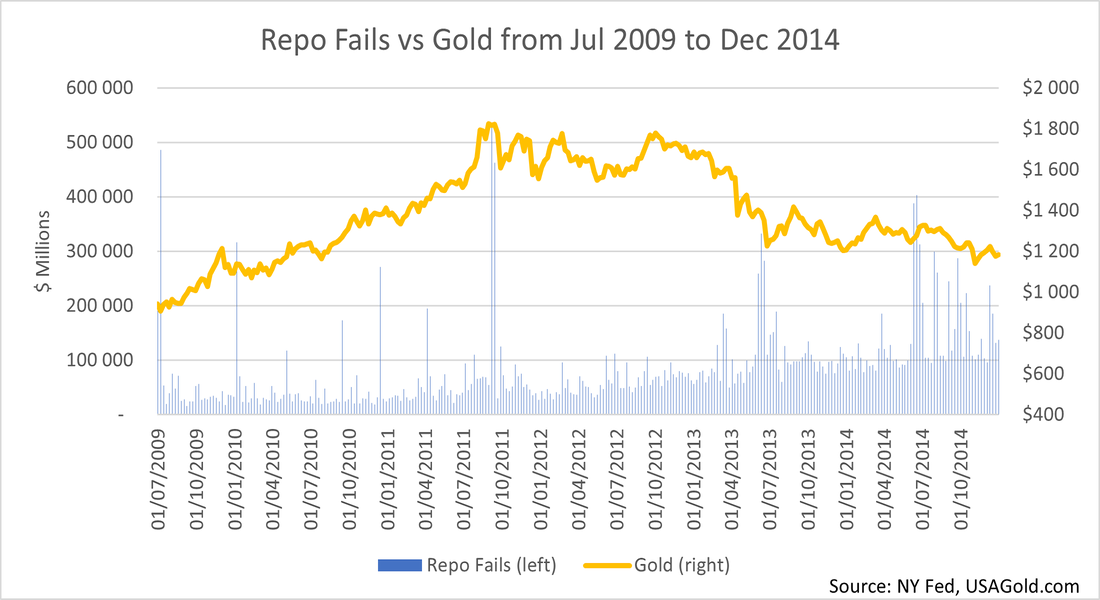

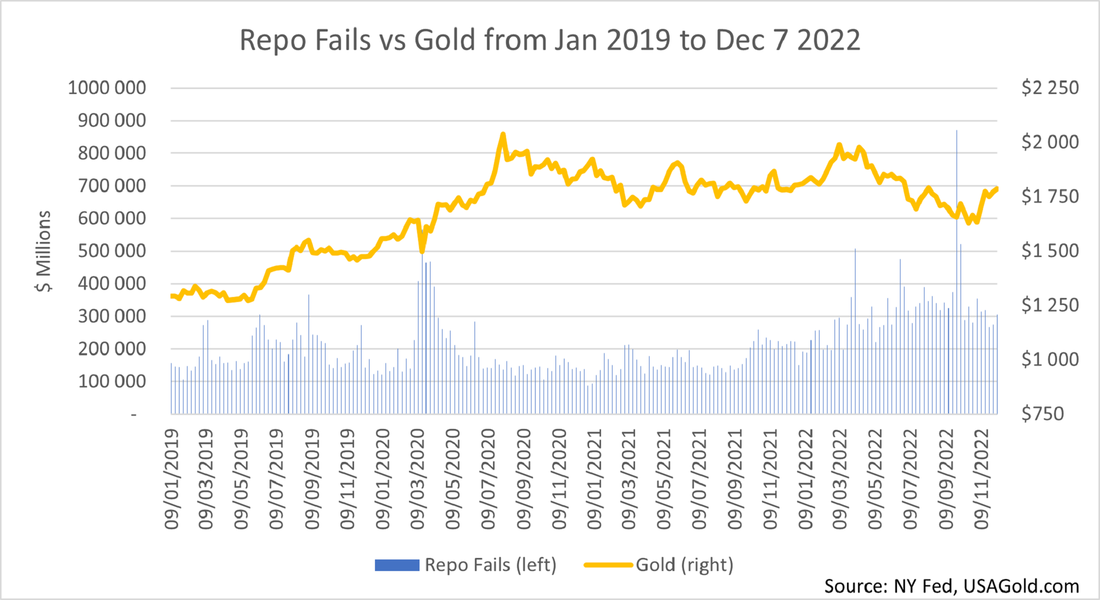

During the Great Inflation, gold’s CAGR was 40.2%. In turn, total credit (in the US) ballooned on average 11.79% annually. Then, at the time debt was increasing at an annual average of 9.20%, which became known as the Great Moderation – from Q1 1982 to Q4 2007 –, gold grew at a rate of just 2.9%. Moreover, at the aftermath of the GFC, starting in the winter of 2009 and ending in the summer of 2011, the yearly pace of credit expansion was merely 0.69%, while the corresponding figure for gold was a gigantic 31.4%. At last, keeping the Q1 2009 as the base, until Q3 2020, when gold reached its all-time high, its CAGR came to 7%, and until the recent local maximum reached in March of this year, this statistic added up to 5.9%. In comparison, respectively to those same intervals, debt accrued 3.54% and 3.94%. In the end, it is unquestionable that inflation does not explain by itself alone the ebbs and flows of the price of gold. Nevertheless, in the long run, the gold price ultimately catches up to the profligate behaviour of the economic agents. Therefore, this raises the question of what then has a more impactful sway on gold in a more direct fashion. By and large, the answer is the investors’ expectations for the average yield of the risk-free assets, adjusted for inflation of course, in the near, foreseeable future. Applying this to the actual world, the main determinant in the medium term is the real yield of the 10-year US Treasury note, which trades with the label TIPS (Treasury Inflation-Protected Securities). Unsurprisingly, this is no accident. Insofar as Treasuries are the most liquid assets in the world, they possess the most “pristine” characteristics in collateral terms, rendering them the safest financial instruments and, consequently, the risk-free asset class.  Even though the 5-year tenor could be used too, the 10-year maturity is the benchmark and, therefore, it carries the most liquidity of all the Treasury notes and bonds. As a result, the longer note presents the most precise depiction of current events and accurate representation of the market expectations. As the previous chart suggests, as speculation for weaker growth intensifies, gold becomes more attractive. In detail, the real interest rate is the average rate of return, adjusting for inflation, that investors are expecting to see in their investments in the predictable future. Typified by the yield of the 10-year TIPS exhibited above in blue, the lower the yield goes (notice that the left scale is inverted), the higher gold appreciates. Evidently, as I thoroughly demonstrated in a previous post, the investor viewpoint is not sufficient to justify the rates of interest. In reality, the Eurodollar beasts put the liquidity risk at the helm, commanding the direction of the yields of bonds and other securities, as well as the interest rates of loans. In addition, for having not even two decades worth of data, seeing that the TIPS have only been around since 2003, we have to resort to other kinds of figures. Accordingly, we can turn to the measured “inflation” rates, instead of the expected ones employed by the TIPS. Unfortunately, this is not the correct way of calculating the real interest rates. At any rate, due to being the only alternative, it will have to do the job. Looking at the chart below, which uses the 5-year rolling average “inflation” to compute the real yield of the 10-year US Treasury note since 1805 (dark blue line), the same tendency noted before remains true. Although this is a neat and interesting graph, with a lot of good information, for the sake of argument, we can pass over the light blue line representing the federal debt to GDP ratio and focus solely on the numbers after 1970. So, remembering the gold chart displayed before, one can straightforwardly observe that the lower the real yield falls, the more does the gold price soar, and vice versa.  However, this too is not enough to fully describe the movements of the price of gold. As we have seen, gold has these moments when it just soars quickly and vigorously, and other periods when it collapses intensely and unexpectedly. Ergo, there is a fierce factor influencing the gold market in the short run. In spite of being rather imperceptible, I am going to reveal the most important determinant of the price of gold in the short term is the liquidity conditions in the inner workings of the global financial system, also known as the eurodollar. As the next graph shows, the relationship seems to be spurious. To be fair, it is most of the time. Notwithstanding, this relation comes to light during periods of financial distress.  In order to explain this, I have to bring into service the gold lending and leasing and the gold swaps trading. As a matter of fact, these transactions, which I alluded to on Part I, in view of being mainly conducted with a great deal of secrecy by and assistance from the wizards in that fancy building on Threadneedle Street, in London, are without any doubt terribly misunderstood. Thus, allow me to shed some light into these shady operations. Firstly, a brief exploration of the gold swaps market. Although there had been some gold swaps that happened earlier in the 19th century, at least for the one in 1925 there is some detailed information about it. Upon reading the first chapter of this series, on the History of money, you will recognize the year 1925 for its significance. In this year, the UK went back to the gold standard after abandoning it in the beginning of the Great War. Wishing to reinstate the classic gold standard parity, Winston Churchill caused some severe strain in financial markets and in the economy. Failing to account for the wartime inflation, proved to be a horrible mistake for prompting a deflationary shock. Regardless of that, the Fed stood ready to aid its homologue across the pond, the BoE, in trying to defend the pre-war parity, despite all of those difficulties. Because there was not enough gold to support it, the attentive and sceptic market participants began to lose faith in the BoE’s ability to sustain the old parity. Ergo, so as to dupe the market, when the gold was being taken out of its vaults, the BoE had to tap into other sources of the “barbarous relic”. In this manner, one of the ways to accomplish this assignment was that gold swap, in 1925. Basically, what happened was the Federal Reserve Bank of New York, on behalf of the Federal Reserve system, made $200 mn of gold bullion available to the Bank of England for its disposal in whatever transactions it might take in defending sterling at that pre-war parity price. In accounting terms, this meant that the BoE took those $200 mn in gold then sell them in the market for sterling at the price that it wished to defend. Subsequently, they put the sterling currency into an account in London on behalf of the Federal Reserve Bank of New York. Hence, what really happened was gold disappeared from New York and ended up as cash in the UK denomination, in London. However, for accounting purposes, the New York Fed showed a “gold receivable” where gold used to be. Simply put, what is happening is the gold is coming off the US central bank’s possession, but not off its balance sheet. All the same, in the perspective of the monetary authorities, there are legitimate reasons for it. By taking the expression “as good as gold” literally, they deem a collateralized account on behalf of a counterparty central bank as good as having gold. Due to a default from a central bank being improbable, one could make the case for this indistinction. In other words, if the New York Fed have asked for its gold back, the BoE would not refuse. 15. Central bank officials indicated that they considered information on gold loans and swaps to be highly market-sensitive, in view of the limited number of participants in such transactions. Thus, they considered that the SDDS reserves template should not require the separate disclosure of such information but should instead treat all monetary gold assets, including gold on loan or subject to swap agreements, as a single data item." In the modern conventions, that is still the case. Reading the above ruling, which was proclaimed by the International Monetary Fund (IMF) in 1999, when this question was raised, the convention states that on official reports to the IMF, central banks and other government official agencies are not required to disclose how much gold they have, as distinct from gold swaps or gold receivables. For not having to differentiate the physical from the paper gold, they can just shove it all in the same line item. Thereby, these procedures leave the public in the dark about how much gold has been swapped and how much truly remains in custody. Despite spurring a lot of interesse, I am not going to address the justifications that central bankers give to withhold this information. Instead, I am saving it for the next instalment. Be that as it may, gold swaps are operations almost exclusively restricted to central banks. Furthermore, the BIS has been a big player in gold trading activities since its inception, in 1930, with disclosures provided since 2010 showing that it has taken tonnes of gold from commercial bullion banks via swaps. Yet, this has decreased considerably in recent months. With the advent of the eurodollar regime, and really the 1980’s forward, we started to see a lot of gold lending and gold leasing. As the title of this series hints at, the financial engineering created by the Eurodollar beasts brought about several innovative instruments. Undoubtedly, gold was not spared. Judging it to be a mutually beneficial transaction, central banks as one counterparty owning gold and gold producers as the ones that go out there into the world and actually dig up the commodity from the ground, come together to participate in this gold leasing market. Having to face the prospects of falling gold prices, the gold miners are going to be interested in hedging, to lock in the price where it is. Seeing that there is a significant time lag in the process of producing gold, the desire to hedge is understandable. To wit, after gold is prospected and extracted, which is very time consuming, it still needs to be assayed, measured and, lastly, refined and purified. Only then can it be marketable and sold to bullion investors, including central banks. In a gold lease arrangement, a miner or gold producer sells forward future production to lock in whatever price, akin to hedging. In order to sell forward, the producer has to borrow existing bullion from somewhere. For a long time, the only holders of such large inventories of gold have been central banks and bullion banks. So, an increase in gold leasing dislodges formerly dormant stores of physical gold from central banks, acting as an added supply of gold onto the markets. Naturally, central and bullion banks, acting as the intermediaries, were more than happy to make their gold stores yield them a nice cashflow. Similar to this leasing arrangement, the gold lending activity functions in the same fashion. Notwithstanding, it is a purely financial affair. In a gold lending relationship, the bank uses the unallocated gold as collateral for cash (in whichever currency is needed, which is one of the appeals of using bullion for collateral). Now, the gold is in the hands of an intermediary that, apart from any haircut set with the borrower, has to protect its position from associated risks. Consequently, the cash lending bank will either sell the gold outright, since it only has to replace metal at the end of the agreement, or hedge its collateral position (based on the cost of selling futures). Like the gold swap business, the accounting rules are such that the central bank continues to “hold” gold on its books, in spite of the lending and leasing operations that moved that metal into the marketplace. Thus, the market has actual gold, albeit mostly of the paper type, sold into it while central banks report no loss of supply, under the line “Gold and Gold Receivables”. Once again, these are opaque transactions, nobody really knows what has been leased or lent out and what remains in the coffers. All in all, the reason central banks want to engage in these procedures is because gold does not pay interest. By participating in these gold market arrangements, they manage to turn what is a non-interest-bearing asset into an interest-bearing asset. Although that is not a big deal for somebody like the US Federal Reserve. For some of the smaller central banks, there are needs and requirements that mandate them to earn money on their assets. Afterall, a central bank is still a bank. As a result, it has to earn some money if it wants to at least cover its own expenses. For the gold market, the end result is exactly the same whether swapping, lending or leasing gold. It acts as an agent to disgorge previously inactive supply into the physical or paper markets, or both. Gold that was until that time sitting idle in an unallocated account has now entered the market through physical (dumping by the cash lender/collateral holder) or, most likely, paper (hedging the collateral holdings) markets. Unsurprisingly, this leads to plenty of people in the goldbug community presuming that there is a secret conspiracy of central bankers, intentionally working with one another, conspiring to suppress the gold price. Even though this would require a deep inspection, the goldbugs make a really good point. Having said that, if that is not what is happening, an explanation on some of the apparently irrational moves in gold prices is needed. For some strange reason, right around 8 o’clock in the morning, New York time, it is very common to see what some people call gold pukes. Abruptly, somebody sells hundreds or thousands of contracts all at once in the futures market. As any competent futures trader knows, those transactions happening all at once rather than gradually is going to dramatically affect the price. Surveying for a more simple, prosaic interpretation, one only needs to look at the plumbing of the financial system and understand how it runs. Going back to the arrangement between gold lending and leasing between a central bank and a mining company, there is no risk for a central bank in price. In this prosaic line of thought, there is no legitimate reason for them to take an interest in price. By its very nature, the gold lending and leasing operations have negative effects on price, without having anything to do with monetary policy of any central bank around the world. Due to dislodging previously idle, stored gold onto the marketplace, when an uptick in lending and leasing ensues, for whatever reason, it is price negative. Therefore, it has nothing to do with manipulation. Plainly, it is just the natural supply and demand mechanics of the way this eurodollar system has been constructed. As the charts below show, represented by the repo fails volume, when stress in the interbank functioning (a.k.a. the “plumbing”) intensifies, gold is negatively impacted. Weirdly, this flies in the face of most investors and observers, since the precious metal is taken for a safe-haven during times of turmoil. Nevertheless, it still fulfils this role, though the beasts of the Eurodollar apparatus get the upper hand over goldbugs in moments of severe strain.

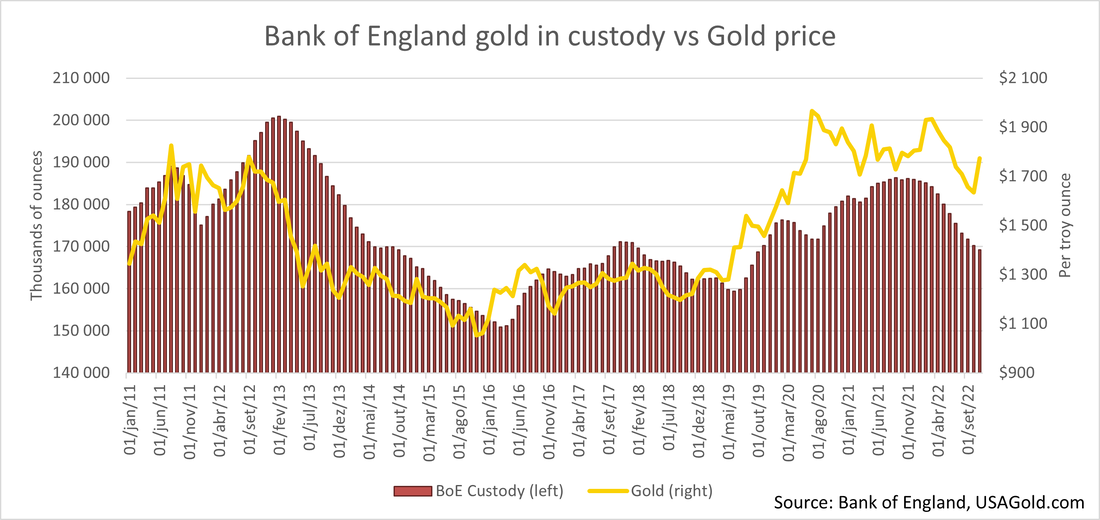

Unmistakably, one immediately grasps that these gold pukes line up rather well with repo market fails. As a reminder, these fails are nothing more than an indication of collateral problems inside the eurodollar system. If we think about gold as it pertains to these lending and leasing businesses, it is sort of a collateralised loan where somebody can borrow a financial asset – in this case, gold sitting idle at a central bank – and use it to help alleviate a collateral shortage system wide. To recall the inner workings of this financial system, the banks and other financial entities use the wholesale interbank markets, of which the repo is the main one of the secured type (from now on used as a pars pro toto for all the secured wholesale interbanking activities), to finance their operations. Since these operations, which include all kinds of asset-backed securities and OTC products, involve massive amounts of funding and smoothly liquid markets as well, they are very dependent on counterparties. In times of anxiety, fears of counterparties failing, something that is never supposed to happen, starts to happen. Ergo, delivery failures in the repo system create an absolute crisis for a bank, where they urgently need cash, no matter what. When a financial institution with funding capacity enters this affair of lending cash against gold to another entity with funding needs, it has no interest in holding that gold. Owing to storage fees and price downside risks, the cash lender will prefer to get rid of the gold, either via OTC or futures markets. Challenging common sense, if they have no interest in acquiring gold, why would they use it then? The answer is the desperate borrower is putting gold towards the cash lender on the opposite side, frankly, because they have no other choice. A commercial bank or some other institution that is running into collateral issues in the repo market might draw from their store of gold, or whomever else’s store of gold they can find, as a last resort collateralised method to get the much-desired cash, mostly in the form of US dollars. Thus, if somebody is lending cash against gold, with the sole intention to use gold for something else, that entity has over-collateralised its lend/lease deal. For instance, say a bank is doing $100 worth of gold lending with a hedge fund, the former puts on a 10% haircut on the collateralised gold and gives the cash in return. In this scenario, seeing that the bank is over-collateralised (on account that it does not want to hold gold), there is nothing to stop it from dumping it all at once in the morning. Its only obligation in that lending contract is to return some form of gold, either physical or paper, at some future date, to the hedge fund. In essence, the bank does not care what the price is, merely moving on from the gold completely. Succinctly, the more the repo market system is stressed in terms of a collateral shortage, the more people must appeal to last resort alternatives, including gold. This means the amount of gold lending (dislodging previously stored-up and off-market supply of metal – both paper and physical) jumps. As a result, owing to the connection between funding market illiquidity and collateral issues, the gold price ultimately tumbles precipitously, seemingly, out of nowhere. Taking the following graph into consideration, one immediately realises that there is some significant correlation between the BoE gold holdings and the price of gold. Despite not always signifying causation, I think we can confidently claim there is some degree of it. Except, it is not in the causal direction most goldbugs surmise.  Indeed, bearing in mind all the reasoning presented above, it is not the English central bank that manipulates the price of this “relic” by flooding the market with its vast reserves of gold. Afterall, the BoE is the second biggest custodian of the precious metal worldwide, only bested by the New York Fed. Au contraire, the inventory of gold in the BoE simply follows the lead set by the metal.

To be more precise, it is heavily influenced by the liquidity conditions of the financial structure. When the Eurodollar beasts are becoming increasingly distressed, gold attracts more demand, resulting in higher prices. Before we go any further, let me remind you that the BoE gold holdings are not just its own, but belong to other central banks and bullion banks too. With this said, as the interest in the precious metal rises, the activity in the gold market surges as well. Since it is the BoE we are examining, then it is the Loco London, OTC gold venue that is experiencing a lot of business. As I demonstrated on Part I, in all likelihood the ensuing enlargement of the gold holdings takes the form of synthetic unallocated gold. Likewise, we can assume the COMEX behaves the same way because, as I expounded on the first part, the magnitude of their fractional reserve trading is equivalent. Evidently, the more the demand for gold heightens, the more will gold, physical and paper, show up in the BoE balance sheet, akin to COMEX stocks (click on Comex Data, then Inventory Data). Chiefly, this increment in demand occurs on account of the medium term factor, the fall in real interest rates, as I have already clarified. Visibly, the same is true in reverse. In any event, the repo fails resulting in more gold lending facet is also discernible in the last chart. In periods of noticeable strain, especially financial crises such as the GFC in 2008 and the European sovereign crisis in 2011 – unfortunately, the BoE only began publishing this type of numbers in 2011, so we have no monthly data for 2008 –, the utilisation of gold as collateral, in the repo market, is multiplied. Hence, BoE gold reserves are drained pronouncedly. Nevertheless, the same did not occur in 2020. Perhaps, on account of the crushing constraint only lasting about a month, being over before the banksters managed to persuade the snail-like bureaucrats to let them exploit some of that shiny unallocated gold. In conclusion, the three paramount determinants of the price of gold are inflation, the real yield of the risk-free asset and the smoothness of the financial system. Each one has its effect perceptible on the long, the medium and the short terms, respectively. Taken together, we realise that gold resembles a volcano. After laying dormant for most of the time, it then slowly starts to move, gradually gaining momentum until it bursts to the sky. By the same token, the performance of this metal is the mirror image of an inflationary boom and bust cycle. As the booming phase of the cycle runs its course, everyone cheers the increment in economic activity, indulging on credit, while being utterly oblivious to its future inescapable collapse. Consequently, when the boom turns to bust, suddenly, the inflation becomes obvious and the statistics for labour, economic output and productivity turned out to be just an illusion. For this reason, sensing the imminent financial ruin, or feeling it even, investors and the general public to boot will seek a safe-haven. Therefore, gold always prevails in the end. On the next and final instalment, I am going to give my final remarks. In addition, I am going to take a dive into the Gold Pools and other shenanigans orchestrated by the central banks, and how it all relates.

0 Comments

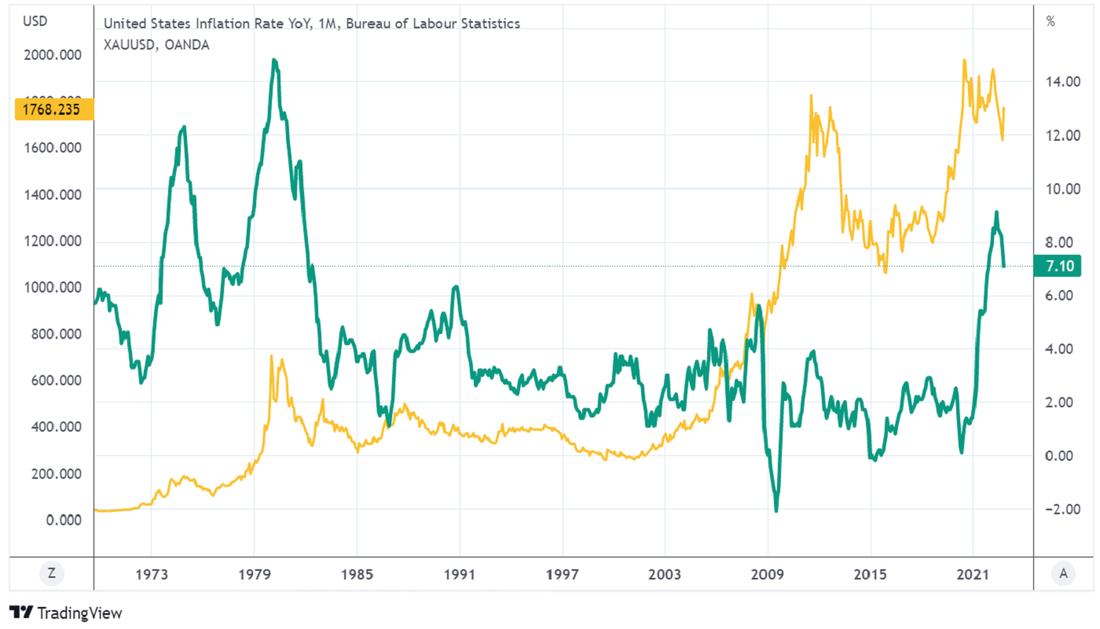

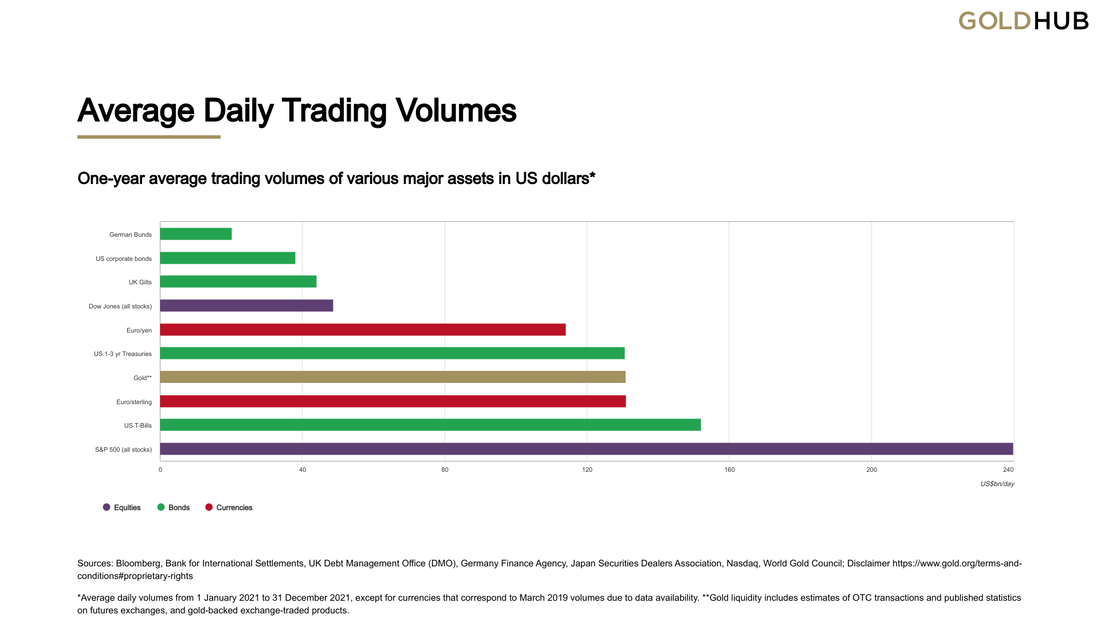

Resuming the history of gold where we left off in the first part, this second instalment is completely dedicated to understanding the factors influencing the price of gold since the advent of the eurodollar system. Specifically, even though this monetary and financial revolution had cropped up in the 1950’s, those factors only took the helm on August 15, 1971, when the gold window was closed by President Richard Nixon. Since the end of the Bretton Woods system (BWS) and all currencies in the world became detached from gold, the era of fiat currencies started. However, gold was not dismissed and forgotten. In lieu of having its price fixed to the US dollar and indirectly to the other currencies – in the BWS, the dollar was pegged at 35$ per ounce of gold with all other currencies having each one its own peg to the dollar –, gold became subject to market forces just like any other asset. When inquiring financial analysts and investors, including goldbugs, on the reasons to acquiring gold, they respond that the precious metal acts as a hedge against inflation and as a safe-haven. In other words, they project the gold price to follow the expansion of the (debt-based) money supply. Nevertheless, they commit a terrible mistake by equating inflation with “inflation” – i.e., a general rise in prices, Machiavellianly computed in government statistics like the CPI. In reality, gold has performed its functions rather well, despite the alleged inertia during the occasional bursts of “inflation”.  As the graph above shows, the relation between gold and “inflation” is not clear, at all. Naturally, this bewilders most observers and frustrates gold standard advocates. In view of being unaware of the dominance of the Eurodollar beasts and instead putting the central banks at the centre of the monetary world, the goldbugs presume either that there is some trickery going on or that the central banks’ credibility is persuading speculators and investors to stay away from gold. Taking the latter into account, some analysts think gold has not reacted to the recent surge in the CPI, of most countries, because the central banks are hiking rates and quashing the market’s inflationary expectations. Thus, due to trusting the capabilities of the monetary authorities and forecasting a higher yield paradigm, the participants are being lured into other assets that bear interest. Simply put, this is utter nonsense. Making the words of the author of the article just referenced, Claudio Grass, my own, “I do not believe that short-term price considerations should play a pivotal role in the decision-making process of investors who hold gold for the right reasons and who understand why they do. What is important, however, is to look beyond the mainstream headlines and to be able to separate the signal from the noise.” Indeed, that is exactly what I am going to do now. To be fair, it does involve some trickery, though, totally legal. All the same, there is a method to this madness. Disclaimers aside, let’s dig in. To begin with, the international gold price usually refers to the price of gold quoted in US Dollars per troy ounce as traded on the 24-hour global wholesale gold market. During the entire business week, gold is traded non-stop globally, allowing the incessant quoting of international gold prices, from Sunday night London time all the way through to Friday night. Depending on the context, this international gold price sometimes refers to a spot gold market quote, such as spot gold traded in the London over-the-counter (OTC) market, and at other times may refer to the front month of a gold futures contract price as traded on the US Commodity Exchange (COMEX). Some years ago, an academic paper has determined that gold price discovery is jointly driven by London OTC spot gold market trading and COMEX gold futures trading, and that the “international gold price” is derived from a combination of London OTC gold prices and COMEX gold futures prices. In general, the higher the trading volume and liquidity in a specific asset market, the more that market contributes to discovering prices for that asset. Obviously, this is also true of the global gold market. Between them, the London OTC (a.k.a. Loco London) and New York trading venues account for the vast majority of global gold trading volume, and in 2021, the London OTC venue, which englobes spot, forwards and options trading, represented approximately 45% of the global gold market turnover, while COMEX accounted for a further 32%. Although this pair holds the dominance of the market, their supremacy is crumbling down quickly. Demonstrably, that academic paper points out that in 2015, the London OTC market gathered 78% of global gold market trading volume, while COMEX had a mere 8% share of the marketplace. Fundamentally, the two reasons for this occurrence are the demand for gold being increasingly coming from the East, mainly China and India, and the regulatory burden imposed after the GFC is forcing a shift towards exchange trading, which includes futures markets such as the COMEX or the SHFE. On that account, beyond the London OTC gold market and the COMEX, all the other gold secondary trading venues negotiate with the price settled in London and New York. Ergo, they are considered price takers. Still, the trend is for these exchanges to turn progressively into price setters, contributing more to the price discovery mechanisms, as the balance of power swings eastward. Furthermore, the international gold price can also at times be referring to the LBMA Gold Price benchmark price – LBMA is an abbreviation for London Bullion Market Association –, as derived during the London daily gold price auctions (morning and afternoon auctions). Before it got this name, in 2015, it was called the London Gold Fix, which had been clouded by mistrust and even repudiation for a very long time. Ultimately, this led to its restructuring and rebranding, albeit not managing to shake off its reputation, rightly so. Therefore, insofar as they are all similar in magnitude, this international price could be referencing a spot gold price, a futures gold price, or an auctioned gold price. Be that as it may, the trio can each one be considered a benchmark. In spite of having been found, as we have just seen, to have lower trading volumes, COMEX presents a larger influence on price discovery than Loco London. This is most likely due to a combination of factors such as COMEX’ accessibility and extended trading hours via use of the GLOBEX platform, the higher transparency of futures trading compared to OTC trading, and the lower transaction costs and ease of leverage in COMEX trading. Conversely, the London OTC gold market has limited trading hours (during London business hours), barriers to wider participation since it is an opaque wholesale market without central clearing, and trading spreads that are dictated by a small number of LBMA bullion bank market-makers and a handful of London-based commodity brokerages. Hence, efforts are being made so that the exchange-traded contracts of the London Metals Exchange gain prominence, in order for London to keep the “terminal market” epithet. To make long story short, the international gold price is fundamentally set by paper gold markets. In other words, it is set by non-physical gold derivatives. Based on their respective gold market structures, Loco London and COMEX are both paper gold markets. Perversely, the supply of and demand for physical gold plays no role in setting the gold price. Because of this, physical gold transactions in all other gold markets just accept the gold prices that are discovered in these paper gold markets. On the one hand, London OTC gold market predominantly involves the trading of synthetic unallocated gold, where trades are cash-settled and not physically delivered (i.e., no delivery of physical gold). Due to convention, unallocated gold positions are merely a series of claims on bullion banks where the holder is an unsecured creditor of the bank, and the bank has a liability to that claim holder for an amount of gold. In turn, the holder, takes on credit risk towards the bullion bank. As a result, London OTC gold market is nothing more than a venue for trading gold credits, employing fractional reserve gold trading with colossal amounts of paper gold born ex nihilo. On the other hand, COMEX only trades exchange-based gold futures contracts, rendering it, unmistakably, a derivatives market. However, less than 1% of COMEX gold futures contracts are usually registered to take delivery. Perhaps this why this venue only stores 1 of every 600 oz in existence worldwide, even though, as I have exposed, the COMEX contributes the most to the discovery of the international gold price. Seeing that very little physical gold is ever delivered on COMEX, and even less physical gold is withdrawn from its approved gold vaults, COMEX registered gold stocks are relatively small. COMEX gold trading also employs significant leverage. In their paper, Hauptfleisch, Putniņš, and Lucey state that “such trades [on COMEX] contribute disproportionately to price discovery”. Note that the COMEX gold futures market is actually a 24-hour market, but its liquidity is highest during US trading hours. Turning to Loco London, nearly the entire trading volume of the London OTC gold market represents trading in unallocated gold, which merely represents a claim by a position holder on a bullion bank for a certain amount of gold, a claim which is rarely exercised. In addition, traders, speculators and investors in unallocated gold positions virtually never take delivery of physical gold. Consequently, Loco London trades also predominantly cash-settle. In 2013, this was confirmed by a UK HMRC/LBMA/LPPM Memorandum of Understanding affirming that in the London gold market “investors acquire an interest in the metals, although in most situations, physical delivery will not occur and in 95% of trades, trading in unallocated metals will be undertaken.” Before that, in 2011, the then LBMA CEO Stuart Murray also confirmed – interestingly, the page has been deleted, but one can find it in the archive – that “various investors hold very substantial amounts [of] unallocated gold and silver in the London vaults” – emphasis mine. Clearly, what Stuart Murray failed to explain is that unallocated gold and silver do not exist in a vault because they are not physical. As Dentons law firm reinforced what we already knew, those are simply paper claims on bullion banks for a quantity of gold and silver that the banks are obliged to find somewhere, if the claimant wanted to execute the claim. To sum up, given COMEX trading gold futures and London trading synthetic unallocated gold, both the London and COMEX gold markets essentially trade gold derivatives, or paper gold instruments, and by extension, the international gold price is being determined in these paper gold markets. (…) the reality of unallocated bullion trading is that buyers and sellers rarely intend for physical delivery to ever take place. Unallocated bullion is used as a means to have ‘synthetic’ holdings of gold and so obtain exposure to the price of gold by reference to the London gold fixing. (…) According to the LBMA bullion bankers who established the reporting of London gold clearing statistics, the then London Precious Metal Clearing Limited (LPMCL) chairman, Peter Fava, and JP Morgan’s Peter Smith, these LBMA gold clearing statistics include trading activities such as “leveraged speculative forward bets on the gold price” and “investment fund spot price exposure via unallocated positions”, activities which are merely side bets on the gold price. Nevertheless, the deficiency of the clearing statistics is explained by the fact that they do not measure individual transactions, gauging instead the metal that is transferred from one clearing account to another on a net basis. Besides that, there are other factors in play: 1) the premature termination of a forward contract, which precludes the transfer of any metal and, hence, being counted for the clearing statistics; 2) spot transactions usually being netted against exchange for physicals (EFP), which swap the original exposure to the spot London market with a futures contract, offsetting the initial OTC transaction by moving the position to the exchange; and 3) for having greater efficiency, the banks have chosen to replace the old FX-based systems, which tracked individual transactions, to this netting one. Unlike the reporting of clearing statistics, the LBMA does not publish gold trading volumes on a regular basis. Notwithstanding, it did publish a one-off gold trading survey covering Q1 2011. Here, it was revealed that during the first quarter of 2011, 10.9 bn oz of gold (340,000 tonnes) were traded in the London OTC gold market. During the same period, 1.18 bn oz of gold (36,700 tonnes) were cleared in the London OTC gold market. This would suggest a trading turnover to clearing turnover ratio in the ballpark of 10:1. In the absence of live trading data, we can take this 10:1 ratio as a proxy and continue to use it as a multiplier to the LBMA London Gold Market daily clearing statistics, which are published on a monthly basis. For example, average daily clearing volumes in the London Gold Market in October 2022, which is the last reported month, totalled 18.3 mn ounces. Converting to tonnages, there was 571.875 tonnes of gold cleared per day in London. On a 10:1 trading to clearing multiple, that is the equivalent to 5,719 tonnes of gold traded per day, or 1.48 mn tonnes of gold traded per year. Owing to storing only around 8,000 tonnes of gold, most of which represents static holdings of central banks – 5,000 tonnes in the Bank of England (BoE) –, ETFs and other holders, the London OTC gold trading activities are totally disconnected from the underlying physical gold holdings. To get a sense of the absurdity, this suggests that approximately 71.5% of the gold kept in the London vaults was being traded. Comparing it to the S&P 500 equities, one of the most traded asset categories in the world, in December 2022, up to the 16th, the average daily volume was $6,714.72 mn. Using the total market capitalization figure at the end of September of $46,460,463.2 mn, this implies that only about 0.01% of the shares of the largest American corporations trade daily, on average.  To cement the ridiculousness, just 205,238 tonnes of gold are estimated to having ever been mined throughout history. In terms of yearly numbers, in the last ten years, gold supply increased on average 4,632 tonnes, 3,409 of which being freshly mined. On the flip side, the average for the gold demand has been 4,314 tonnes.

Remarkably, this would indicate, if it was real, that 2.8% or thereabouts of all the gold in the globe is transacted in London, every day. Keeping in mind that almost half (46%) of the gold is held in the form of jewellery, it appears that 5.16% of the non-jewellery gold trades daily, while a huge 12.58% of all the gold bars and coins in the world seem to “change hands” every day, just in London. Thus, the trading of nearly 5,719 tonnes of gold per day within the London gold market has nothing to do with the physical gold market. Calculating for the whole 2021, total trading volume in the London gold market is estimated to have been in the neighbourhood of 1.38 mn tonnes of gold, while the trading volume of the 100 oz COMEX gold futures reached 41.9 mn contracts, equivalent to 188,325 tonnes. For those paying attention, these figures are insane. Ipso facto, on a daily average, gold trading in New York and London are, respectively, more or less 44 and 319 times the annual amount demanded by jewellers, bullion investors and other manufacturers that need or desire the real thing. Similarly, this trading represents roughly 41 and 297 times the annual gold supply, in New York and London venues respectively. Consequently, gold trading volume on the London OTC gold market, in 2021, was about 7.3 times the turnover in the COMEX 100 oz gold futures market. Finally, in August of last year, the combined gold stock, including paper claims, of all the COMEX depositories added up to 37,486,859 ounces, or 1,171.5 tonnes. For those keeping score, with approximately 8,000 tonnes of gold in London (or under it), the Loco London to COMEX ratio comes to 6.83, being close to the trading volume one. Therefore, we can safely assume their fractional reserve trading is identical in magnitude in these two trading channels. Moving on, now that the basic concepts have been laid out, it is time to present the heart of the matter. As an inheritance of the all-powerful British Empire, the London Gold Lending Market, which is a global marketplace, revolves around the BoE. Here, central banks and commercial bullion banks interact in the execution of obscure gold lending and gold swap transactions that increase the available supply of gold. Unsurprisingly, the bullion banks dubbed this scheme of smuggling a few pieces of gold to show their customers and the suits as liquidity provision. Evidently, few if any transactional details about the gold lending market are ever made public. Likewise gold lending and gold swaps are not reported distinctly from central bank gold holdings. In this mad, clown world we live in, gold held and gold lent/swapped is merely reported as one line item of ‘Gold and Gold Receivables’ on central banks’ balance sheets. Therefore, the real state of central bank gold holdings is concealed for any central bank engaged in gold lending or gold swaps. Notwithstanding, gold lending and swaps provide borrowed physical gold for bullion banks to engage in leveraged fractional reserve bullion banking and trading to boot, mostly in London and New York, where the international spot gold price is predominantly determined. On that account, gold lending and swaps, the leveraged and fractional reserve nature of gold trading, and the lack of transparency and accountability, all align to have a potentially depressing effect on the gold price. Or do they? For having still a lot to say and already surpassing the three thousand word count, I am taking a breather and come back to it a couple of days from now. In this day and age, of all the fields that make up the vast concepts of science and human knowledge, you are hard pressed to find one that is more misunderstood than Economics. Of course, there are several fields that have been corrupted by malicious endeavours to foil the public’s freethinking and pursuit of the truth. Although there is much to add about this, I am going to stick with the theme of this series, which is money. Indeed, monetary economics has been, in my humble opinion, an utter disservice to us all, whether we are aware of it or not, since the dawn of civilization. To make matters worse, I contend the neglect and failure to correctly and honestly assess matters of money and exchange has only got more pronounced. Yet, it is not the case that scrupulous and precise reasoning has never been made, divulged or even applied in the real world. Notwithstanding, the powerful vicious intents of our overlords have been quite successful at thwarting the truth from reaching the masses, keeping us in a continual state of confusion and oblivion. The purpose of this three-part series is to clarify the definition, usefulness and history of money. If you are familiar with my work, perhaps you already know what I mean by the term “money”. As the title hints at, gold and to a slightly lesser degree silver are the purest, most complete forms of money. On this first instalment, I will go through the History of money, examining its evolution, from the ancient times until just before we arrived at this abortion of a system dubbed eurodollar. Then, in the second part, I am going to expose the contraptions behind the gold market and its pricing mechanisms. To finish off, taking from what I have found out, I will announce my verdict on the machinations and intentions of the-powers-that-be to muddle the perceptions of the masses on this current, irrational and ignoble state of affairs, in addition to halt the emergence of a well-grounded and fair monetary regime.  Before we had the currency we all use nowadays, barter was the first system of exchange, consisting of trading goods directly, tit for tat. For instance, I will give you one cow and you give me five bottles of wine because that is kind of a fair exchange on cows and wine. As one can easily ascertain, it gets tricky. Thus, someone had to invent a solution to this double coincidence of wants, as it is labelled. Accordingly, this thing called money was born. As time went by, different populations used different media of exchange. While some would use salt, others would use shells. Ultimately, people came to the conclusion that gold and silver were the greatest contenders to play the role of money. For all we know, roughly 5,000 years ago, the Babylonians started using gold and silver as their predominant form of currency. Still, the pieces of gold and silver that they were using were odd sizes and weights. In other words, odd purities. Ergo, trade was still difficult seeing that the currency units were not interchangeable, where each unit is the same as the next. According to many historians, only in 7th century BC the first standardly minted and fungible coins appeared. King Alyattes of Lydia, in what is today Turkey, issued a form of coinage made of electrum, a natural mixture of gold and silver. One of the reasons that we are in the financial mess that we are today globally is that people do not understand the difference between currency and money. On the one hand, currency is a medium of exchange, a unit of account, it is portable, durable, divisible, and something called fungible, which essentially means that each unit is the same as the next unit. On the other hand, money is all of those things plus a store of value over a long period of time. Even financial planners, bankers, your accountant, they do not understand the difference between currency and money. The currency in your pocket is a medium of exchange and a unit of account due to having numbers on it. Moreover, it is somewhat durable (certainly not anywhere close to gold and silver durability), portable, divisible in that you can make change, and it is fungible. For example, a dollar or a euro in my pocket buys the same amount as a dollar or a euro in your pocket. Be that as it may, in view of the possibility, or rather the inevitability, the amount of currency keeps on expanding, there is a continuous dilution of its value. On that account, your wealth is transferred, indirectly, to the receivers of the freshly created currency. Unsurprisingly, the biggest beneficiaries of this phenomenon, the Cantillon effect, are the biggest borrowers, i.e., governments, financial institutions and their cronies. The reason that gold and silver are the optima forms of money is because of their properties. Besides storing large amounts of value in a very small area, they are units of account, fungible in their pure state, extremely durable – they do not corrode –, very portable and clean and hygienic – unlike crude oil or coal –, and, for being highly scarce, their value maintains fairly stable over time, functioning as a tremendously reliable store of value. Attesting to its durability, the same gold the Babylonians were using in trade is still here with us today. Over the last 5,000 years, only gold and silver have maintained their purchasing power. During this period, there have been thousands upon thousands of fiat currencies, which are unbacked by gold or silver, having all gone to zero. Believe it or not, it has been a 100% failure rate. Nevertheless, the first recorded use of paper money was purported to be in the country of China during the 11th century AD as a means of reducing the need to carry heavy and cumbersome strings of metallic coins to conduct transactions. Similar to making a deposit at a modern bank, individuals would transfer their coins to a trustworthy party and then receive a note denoting how much money they had deposited. Then, the note could be redeemed for currency at a later date. At the same time, parts of Europe were still using metal coins as their sole form of currency until the 16th century. Colonial acquisitions of new territories via European conquest provided new sources of precious metals and enabled European nations to keep minting a greater quantity of coins. However, banks eventually started using paper banknotes for depositors and borrowers to carry around in place of metal coins. These notes could be taken to the bank at any time and exchanged for their face value in metal (usually silver or gold) coins. This paper money could be used to buy goods and services. In this way, it operated much like currency does today in the modern world. However, it was issued by banks and private institutions, not governments nor central banks, which are now responsible for issuing paper money in most countries. In spite of the proper “classical gold standard era” having begun in the United Kingdom in 1821 and then spreading to France, Germany, Switzerland, the United States and so on, the UK, along with Portugal, were already in a de facto gold standard. In this system, which officially began in 1870, each government pegged its national currency to a fixed weight in gold. For example, by 1834, US dollars were convertible to gold at a rate of $20.67 per ounce. These parity rates were used to price international transactions. Other countries later joined to gain access to Western trade markets. There were many interruptions in the gold standard, especially during wartime, and many countries experimented with bimetallic (gold and silver) standards. Governments frequently spent more than their gold reserves could back, and suspensions of national gold standards were extremely common. In addition, governments struggled to correctly peg the relationship between their national currencies and gold without creating distortions. Finally, as long as banks operated on a fractional reserve scheme, besides the recurrent boom and bust cycles generated by the expansion of credit, there was a permanent state of instability in the monetary system, with the threat of financial panics and bank runs relentlessly hovering over the horizon. Naturally, sooner or later, the bankers would harvest the turmoil and insolvencies that they sowed. Those who insist that a reserve currency need to take the form of a physical commodity are misguidingly backing a relic of a time when governments were less trustworthy in these matters than they are now, and when it was the fashion to imitate uncritically the system which had been established in England and had seemed to work so well during the second quarter of the nineteenth century.” For that reason, the gold standard slowly eroded during the 20th century. This began with World War I and then the distress provoked by the erroneous pound sterling peg to gold the British implemented in 1925, so as to return to the gold standard at the pre-WWI peg. Because the belief in the gold standard had already practically vanished by the time the depths of the Great Depression were baffling and wrecking the lives of everyone, on September 21, 1931, the UK government took its country out of the gold standard, rendering the global reserve currency, the pound sterling, a fiat currency. Indubitably, it was not long till the other countries followed suit. In 1932, 23 more countries abandoned the gold standard, then the US on April 20, 1933, and France in 1936. Curiously, before departing the gold standard, President Roosevelt made sure the public was not going to panic and indulge on a gold buying spree by mandating the citizenry to renounce their gold.

Simply put, our true wealth is our time and freedom to put our abilities to work. Furthermore, money is just a tool for trading our time and fruits of our labour and ventures, acting as a container to store our economic energy until we are ready to deploy it. However, the whole world has been turned away from real money and has been fooled into using a deceitful imposter, called fiat, which is silently stealing our two most valuable assets: our time and our freedom. Sadly, we lost having things of value be our currency, replacing it with plain numbers and accounts. But trust me, it is not real. In point of fact, whenever the financial system entered a crisis or merely were cracks showing up, the culprits, a.k.a., the (fractional reserve) banking cabal and its governmental puppets were always quick to pin the blame on the gold reserve and its rigidity. This is a colossal failure, and maybe an intentional one, at realising that an unhampered and solid monetary arrangement is a vital element for a well-functioning economy and free society to boot. This finger pointing should come as no surprise. As Milton Friedman succinctly surmised in the 1980 speech titled Myths that Conceal Reality, as part of the Free to Choose series, the free market is forced to be the scape goat whenever the bust ensues and takes its toll. According to the 1976 Nobel Prize in Economics recipient, the condemnation of the private enterprise happens because “[it] has no press agents, the free market has no press agents; the government has a great many press agents, the Federal Reserve has a great many press agents.” Back in the day, when the economy operated on some sort of “hard” money regime, currencies were a fixed weight of gold, silver or even base metals. Before the advent of paper money, when the sovereigns were lost in profligacy, in order to fulfil their liabilities, they could ask the minters to either clip and reduce the size of the coins or, better yet, dilute the value of them by meshing the precious metals with a base one, like nickel or copper. Afterwards, during the classical gold standard, when banks gave out credit, in the form of paper money, without the full backing of gold or silver, the real value of the currency would dwindle. That is to say, if the banks’ customers, and the populace generally speaking, wised up to the innate state of bankruptcy that the banks were consistently on, they would run to these institutions and demand to have their hard-earned money (i.e., gold and silver) back before the house of cards collapsed. Evidently, as one might expect, this has occurred repeatedly for being an inherent feature of the system. Nevertheless, in the mid-19th century, there were a prominent group of economists, who were followers of the writings of David Ricardo that together became to be known as the British Currency School. In essence, they contended that the excessive issuance of banknotes was a major cause of rising prices, and believed that, in order to restrict circulation, issuers of new banknotes should be required to hold an equivalent value of gold in reserve. On the opposite side, there was the British Banking School that defended the “banking principle”, which consisted of banks maintaining the convertibility of their banknotes into specie (gold) by keeping “adequate” reserves. As a result, it is impossible to overissue banknotes against sound commercial paper with fixed short term (90 days or less) maturities. Moreover, currency issuance, they asserted, could be naturally restricted by the desire of bank depositors to redeem their notes for gold. Clearly, the Currency School with its “currency principle” were sort of proto-Austrian, while the Banking School was proto-Keynesian. The former argued against inflation and for full backing of the currency with gold or silver. Conversely, the latter supported fractional reserve banking, though it recommended banking supervision by the central bank to curtail the moral hazard that this regime caused. The Banking School once more resembles the modern Positive Economics offspring, in this case the Monetarists, when it professes that the financial cycle has to be smoothed. Specifically, the discount rate offered by the central bank has to rise above the market rate in normal times and fall below it in crisis times. Unmistakably, this is also akin to the Keynesian belief that fiscal and/or monetary authorities ought to “hit the brakes” when the economy is “overheating” and “hit the gas pedal” when it is “overcooling”, so to speak, to restore growth to its natural rate of full employment equilibrium. Despite winning the battle in 1844 against the Banking School by implementing a 100% reserve backing of banknote issue, their subsequent mistakes and incomplete endeavours in the Peel’s Act cost them the war. Namely, it gave monopoly power on the issuance of banknotes to the Bank of England (BoE) and failed to comprehend that demand deposits also pertain to the money supply. For these reasons, the BoE would take advantage of its monopolistic privileges, beginning a large-scale expansion of its deposit-banking activities. Hence, this monetary ballooning fuelled a speculative bubble that caused a drain on the specie reserves of the bank and resulted in severe panics in 1847. In addition, the fact that the BoE was permitted to inflate pretty much uncontrollably through demand deposits, and that this Act remained valid until the outbreak of the WWI in 1914, there were two other banking panics that sprang in 1857 and 1866. As a response, the English government decided to suspend on both occasions, as it did in 1847, the full reserve backing requirement to preclude the deflationary spiral. Unfortunately, the perception that the contemporaries were left with was that the “banking principle” was superior and central banks were fundamental to a well-functioning economy and financial system. Naturally, this resulted in the disappearance of the Currency School. Even though the Peelites were ostensibly free market advocates, this absurdity to submit to the BoE exclusive rights to expand the money supply had horrific effects. Among them, the main one was that the private issuance of paper money gradually faded away, having completely ceased in 1921. Therefore, a crucial step towards the centralisation and control of money by the banking cabal had just been taken. In this manner, the next phase was to separate credit origination from the shackles of gold and silver. In 1873, Walter Bagehot published his immensely influential book titled Lombard Street, awarding him the accolade: “prophet of central banking”. Albeit a believer in the gold standard, though likely just agnostic to it, his conclusions and suggestions were the antithesis of a proper, stable financial system, not to mention the tenets of property rights and laissez faire capitalism. Afterall, he was a proponent of central banking. Still, he argued the central bank should only exist as a lender of last resort, providing liquidity to those banks which really did not manage to find lenders in the market despite presenting good collateral. As his dictum goes: “lend freely against good collateral at a high [discount] rate”. Insofar as central banking advocates come, Bagehot seems to be of the most reasonable kind, even more so than the British Currency School. Precisely, he apparently contrasted starkly with his coevals. As the 19th century approached its zenith, the trend was for the economist and banking classes to grow increasingly disheartened with the gold standard and capitalism as well. The types of Bagehot were ostensibly a dying breed. In the same year that Bagehot published his magnum opus, US President Ulysses S. Grant and his cabinet were set to implement the Coinage Act of 1873, which put the American economy back in the gold standard after divorcing from it during the Civil War. Among the voices critical of this move was John Austin Steven, who was born into a prominent banking family and close to the political establishment. Writing to the New York Times, he affirmed “gold is a relic of barbarism to be tabooed by all civilized nation.” Those who advocate the return to a gold standard do not always appreciate along what different lines our actual practice has been drifting. If we restore the gold standard, are we to return also to the pre-war conceptions of bank-rate, allowing the tides of gold to play what tricks they like with the internal price-level, and abandoning the attempt to moderate the disastrous influence of the credit-cycle on the stability of prices and employment? Or are we to continue and develop the experimental innovations of our present policy, ignoring the "bank ration" and, if necessary, allowing unmoved a piling up of gold reserves far beyond our requirements or their depletion far below them? Unquestionably, Keynes was not the first to think of gold as a “relic of barbarism”. Indeed, there have been many others. From the Marxists and the 18th century utopian socialists to the chartalists – followers of the scientific charlatan Georg Friedrich Knapp and precursor of the Modern Monetary Theory – the mood was surely getting progressively averse to a free market, “hard” money regime.

Bearing a less radical approach, there were those, so as to tap into other sources of money, who rallied for a bimetallic standard, such as former US Secretary of the Treasury and three-time Democratic nominee for President, William Jennings Bryan. Furthermore, in lieu of abandoning the gold standard in 1933, President Roosevelt considered introducing a bimetallic regime. Inasmuch as the currency is backed 100% by the gold and silver, there is no dispute on my part. To bring this first part to an end, when the Armistice drew the Great War to a close, the return to some sort of metallic regime was in doubt. Since Europe was devastated after the war, governments were planning on spending greatly, in addition to having to pay colossal debt expenses, politicians delayed the reinstatement of the gold standard for a few years. Because the UK, which was the global hegemon at the time, refused to account for the inflation, its policy makers came up with some creative solutions to protect the pre-war parity of $4.86/£1 and pretend that the inflation had never happened. As you will see on the next instalments, this tradition has never died out. More emphatically, though, the technocratic, progressive and socialist movements were appealing more and more to the masses. Thus, economists and politicians wanted to have a shot at engineering the economic structure, “to stabilise prices” and “control inflation”. On this account, controlling the monetary system was essential. As Keynes pleaded above, we had to disregard the gold standard in order to “moderate the disastrous influence of the credit-cycle on the stability of prices and employment”. What a fool! |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed