|

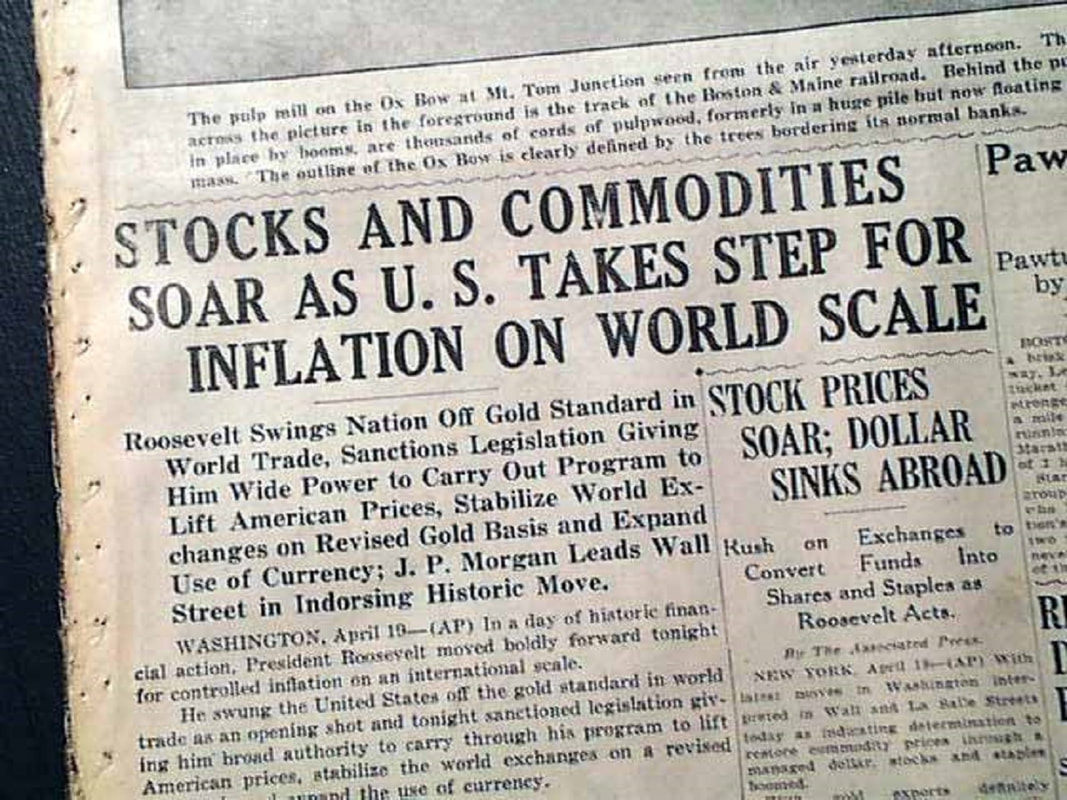

In this day and age, of all the fields that make up the vast concepts of science and human knowledge, you are hard pressed to find one that is more misunderstood than Economics. Of course, there are several fields that have been corrupted by malicious endeavours to foil the public’s freethinking and pursuit of the truth. Although there is much to add about this, I am going to stick with the theme of this series, which is money. Indeed, monetary economics has been, in my humble opinion, an utter disservice to us all, whether we are aware of it or not, since the dawn of civilization. To make matters worse, I contend the neglect and failure to correctly and honestly assess matters of money and exchange has only got more pronounced. Yet, it is not the case that scrupulous and precise reasoning has never been made, divulged or even applied in the real world. Notwithstanding, the powerful vicious intents of our overlords have been quite successful at thwarting the truth from reaching the masses, keeping us in a continual state of confusion and oblivion. The purpose of this three-part series is to clarify the definition, usefulness and history of money. If you are familiar with my work, perhaps you already know what I mean by the term “money”. As the title hints at, gold and to a slightly lesser degree silver are the purest, most complete forms of money. On this first instalment, I will go through the History of money, examining its evolution, from the ancient times until just before we arrived at this abortion of a system dubbed eurodollar. Then, in the second part, I am going to expose the contraptions behind the gold market and its pricing mechanisms. To finish off, taking from what I have found out, I will announce my verdict on the machinations and intentions of the-powers-that-be to muddle the perceptions of the masses on this current, irrational and ignoble state of affairs, in addition to halt the emergence of a well-grounded and fair monetary regime.  Before we had the currency we all use nowadays, barter was the first system of exchange, consisting of trading goods directly, tit for tat. For instance, I will give you one cow and you give me five bottles of wine because that is kind of a fair exchange on cows and wine. As one can easily ascertain, it gets tricky. Thus, someone had to invent a solution to this double coincidence of wants, as it is labelled. Accordingly, this thing called money was born. As time went by, different populations used different media of exchange. While some would use salt, others would use shells. Ultimately, people came to the conclusion that gold and silver were the greatest contenders to play the role of money. For all we know, roughly 5,000 years ago, the Babylonians started using gold and silver as their predominant form of currency. Still, the pieces of gold and silver that they were using were odd sizes and weights. In other words, odd purities. Ergo, trade was still difficult seeing that the currency units were not interchangeable, where each unit is the same as the next. According to many historians, only in 7th century BC the first standardly minted and fungible coins appeared. King Alyattes of Lydia, in what is today Turkey, issued a form of coinage made of electrum, a natural mixture of gold and silver. One of the reasons that we are in the financial mess that we are today globally is that people do not understand the difference between currency and money. On the one hand, currency is a medium of exchange, a unit of account, it is portable, durable, divisible, and something called fungible, which essentially means that each unit is the same as the next unit. On the other hand, money is all of those things plus a store of value over a long period of time. Even financial planners, bankers, your accountant, they do not understand the difference between currency and money. The currency in your pocket is a medium of exchange and a unit of account due to having numbers on it. Moreover, it is somewhat durable (certainly not anywhere close to gold and silver durability), portable, divisible in that you can make change, and it is fungible. For example, a dollar or a euro in my pocket buys the same amount as a dollar or a euro in your pocket. Be that as it may, in view of the possibility, or rather the inevitability, the amount of currency keeps on expanding, there is a continuous dilution of its value. On that account, your wealth is transferred, indirectly, to the receivers of the freshly created currency. Unsurprisingly, the biggest beneficiaries of this phenomenon, the Cantillon effect, are the biggest borrowers, i.e., governments, financial institutions and their cronies. The reason that gold and silver are the optima forms of money is because of their properties. Besides storing large amounts of value in a very small area, they are units of account, fungible in their pure state, extremely durable – they do not corrode –, very portable and clean and hygienic – unlike crude oil or coal –, and, for being highly scarce, their value maintains fairly stable over time, functioning as a tremendously reliable store of value. Attesting to its durability, the same gold the Babylonians were using in trade is still here with us today. Over the last 5,000 years, only gold and silver have maintained their purchasing power. During this period, there have been thousands upon thousands of fiat currencies, which are unbacked by gold or silver, having all gone to zero. Believe it or not, it has been a 100% failure rate. Nevertheless, the first recorded use of paper money was purported to be in the country of China during the 11th century AD as a means of reducing the need to carry heavy and cumbersome strings of metallic coins to conduct transactions. Similar to making a deposit at a modern bank, individuals would transfer their coins to a trustworthy party and then receive a note denoting how much money they had deposited. Then, the note could be redeemed for currency at a later date. At the same time, parts of Europe were still using metal coins as their sole form of currency until the 16th century. Colonial acquisitions of new territories via European conquest provided new sources of precious metals and enabled European nations to keep minting a greater quantity of coins. However, banks eventually started using paper banknotes for depositors and borrowers to carry around in place of metal coins. These notes could be taken to the bank at any time and exchanged for their face value in metal (usually silver or gold) coins. This paper money could be used to buy goods and services. In this way, it operated much like currency does today in the modern world. However, it was issued by banks and private institutions, not governments nor central banks, which are now responsible for issuing paper money in most countries. In spite of the proper “classical gold standard era” having begun in the United Kingdom in 1821 and then spreading to France, Germany, Switzerland, the United States and so on, the UK, along with Portugal, were already in a de facto gold standard. In this system, which officially began in 1870, each government pegged its national currency to a fixed weight in gold. For example, by 1834, US dollars were convertible to gold at a rate of $20.67 per ounce. These parity rates were used to price international transactions. Other countries later joined to gain access to Western trade markets. There were many interruptions in the gold standard, especially during wartime, and many countries experimented with bimetallic (gold and silver) standards. Governments frequently spent more than their gold reserves could back, and suspensions of national gold standards were extremely common. In addition, governments struggled to correctly peg the relationship between their national currencies and gold without creating distortions. Finally, as long as banks operated on a fractional reserve scheme, besides the recurrent boom and bust cycles generated by the expansion of credit, there was a permanent state of instability in the monetary system, with the threat of financial panics and bank runs relentlessly hovering over the horizon. Naturally, sooner or later, the bankers would harvest the turmoil and insolvencies that they sowed. Those who insist that a reserve currency need to take the form of a physical commodity are misguidingly backing a relic of a time when governments were less trustworthy in these matters than they are now, and when it was the fashion to imitate uncritically the system which had been established in England and had seemed to work so well during the second quarter of the nineteenth century.” For that reason, the gold standard slowly eroded during the 20th century. This began with World War I and then the distress provoked by the erroneous pound sterling peg to gold the British implemented in 1925, so as to return to the gold standard at the pre-WWI peg. Because the belief in the gold standard had already practically vanished by the time the depths of the Great Depression were baffling and wrecking the lives of everyone, on September 21, 1931, the UK government took its country out of the gold standard, rendering the global reserve currency, the pound sterling, a fiat currency. Indubitably, it was not long till the other countries followed suit. In 1932, 23 more countries abandoned the gold standard, then the US on April 20, 1933, and France in 1936. Curiously, before departing the gold standard, President Roosevelt made sure the public was not going to panic and indulge on a gold buying spree by mandating the citizenry to renounce their gold.

Simply put, our true wealth is our time and freedom to put our abilities to work. Furthermore, money is just a tool for trading our time and fruits of our labour and ventures, acting as a container to store our economic energy until we are ready to deploy it. However, the whole world has been turned away from real money and has been fooled into using a deceitful imposter, called fiat, which is silently stealing our two most valuable assets: our time and our freedom. Sadly, we lost having things of value be our currency, replacing it with plain numbers and accounts. But trust me, it is not real. In point of fact, whenever the financial system entered a crisis or merely were cracks showing up, the culprits, a.k.a., the (fractional reserve) banking cabal and its governmental puppets were always quick to pin the blame on the gold reserve and its rigidity. This is a colossal failure, and maybe an intentional one, at realising that an unhampered and solid monetary arrangement is a vital element for a well-functioning economy and free society to boot. This finger pointing should come as no surprise. As Milton Friedman succinctly surmised in the 1980 speech titled Myths that Conceal Reality, as part of the Free to Choose series, the free market is forced to be the scape goat whenever the bust ensues and takes its toll. According to the 1976 Nobel Prize in Economics recipient, the condemnation of the private enterprise happens because “[it] has no press agents, the free market has no press agents; the government has a great many press agents, the Federal Reserve has a great many press agents.” Back in the day, when the economy operated on some sort of “hard” money regime, currencies were a fixed weight of gold, silver or even base metals. Before the advent of paper money, when the sovereigns were lost in profligacy, in order to fulfil their liabilities, they could ask the minters to either clip and reduce the size of the coins or, better yet, dilute the value of them by meshing the precious metals with a base one, like nickel or copper. Afterwards, during the classical gold standard, when banks gave out credit, in the form of paper money, without the full backing of gold or silver, the real value of the currency would dwindle. That is to say, if the banks’ customers, and the populace generally speaking, wised up to the innate state of bankruptcy that the banks were consistently on, they would run to these institutions and demand to have their hard-earned money (i.e., gold and silver) back before the house of cards collapsed. Evidently, as one might expect, this has occurred repeatedly for being an inherent feature of the system. Nevertheless, in the mid-19th century, there were a prominent group of economists, who were followers of the writings of David Ricardo that together became to be known as the British Currency School. In essence, they contended that the excessive issuance of banknotes was a major cause of rising prices, and believed that, in order to restrict circulation, issuers of new banknotes should be required to hold an equivalent value of gold in reserve. On the opposite side, there was the British Banking School that defended the “banking principle”, which consisted of banks maintaining the convertibility of their banknotes into specie (gold) by keeping “adequate” reserves. As a result, it is impossible to overissue banknotes against sound commercial paper with fixed short term (90 days or less) maturities. Moreover, currency issuance, they asserted, could be naturally restricted by the desire of bank depositors to redeem their notes for gold. Clearly, the Currency School with its “currency principle” were sort of proto-Austrian, while the Banking School was proto-Keynesian. The former argued against inflation and for full backing of the currency with gold or silver. Conversely, the latter supported fractional reserve banking, though it recommended banking supervision by the central bank to curtail the moral hazard that this regime caused. The Banking School once more resembles the modern Positive Economics offspring, in this case the Monetarists, when it professes that the financial cycle has to be smoothed. Specifically, the discount rate offered by the central bank has to rise above the market rate in normal times and fall below it in crisis times. Unmistakably, this is also akin to the Keynesian belief that fiscal and/or monetary authorities ought to “hit the brakes” when the economy is “overheating” and “hit the gas pedal” when it is “overcooling”, so to speak, to restore growth to its natural rate of full employment equilibrium. Despite winning the battle in 1844 against the Banking School by implementing a 100% reserve backing of banknote issue, their subsequent mistakes and incomplete endeavours in the Peel’s Act cost them the war. Namely, it gave monopoly power on the issuance of banknotes to the Bank of England (BoE) and failed to comprehend that demand deposits also pertain to the money supply. For these reasons, the BoE would take advantage of its monopolistic privileges, beginning a large-scale expansion of its deposit-banking activities. Hence, this monetary ballooning fuelled a speculative bubble that caused a drain on the specie reserves of the bank and resulted in severe panics in 1847. In addition, the fact that the BoE was permitted to inflate pretty much uncontrollably through demand deposits, and that this Act remained valid until the outbreak of the WWI in 1914, there were two other banking panics that sprang in 1857 and 1866. As a response, the English government decided to suspend on both occasions, as it did in 1847, the full reserve backing requirement to preclude the deflationary spiral. Unfortunately, the perception that the contemporaries were left with was that the “banking principle” was superior and central banks were fundamental to a well-functioning economy and financial system. Naturally, this resulted in the disappearance of the Currency School. Even though the Peelites were ostensibly free market advocates, this absurdity to submit to the BoE exclusive rights to expand the money supply had horrific effects. Among them, the main one was that the private issuance of paper money gradually faded away, having completely ceased in 1921. Therefore, a crucial step towards the centralisation and control of money by the banking cabal had just been taken. In this manner, the next phase was to separate credit origination from the shackles of gold and silver. In 1873, Walter Bagehot published his immensely influential book titled Lombard Street, awarding him the accolade: “prophet of central banking”. Albeit a believer in the gold standard, though likely just agnostic to it, his conclusions and suggestions were the antithesis of a proper, stable financial system, not to mention the tenets of property rights and laissez faire capitalism. Afterall, he was a proponent of central banking. Still, he argued the central bank should only exist as a lender of last resort, providing liquidity to those banks which really did not manage to find lenders in the market despite presenting good collateral. As his dictum goes: “lend freely against good collateral at a high [discount] rate”. Insofar as central banking advocates come, Bagehot seems to be of the most reasonable kind, even more so than the British Currency School. Precisely, he apparently contrasted starkly with his coevals. As the 19th century approached its zenith, the trend was for the economist and banking classes to grow increasingly disheartened with the gold standard and capitalism as well. The types of Bagehot were ostensibly a dying breed. In the same year that Bagehot published his magnum opus, US President Ulysses S. Grant and his cabinet were set to implement the Coinage Act of 1873, which put the American economy back in the gold standard after divorcing from it during the Civil War. Among the voices critical of this move was John Austin Steven, who was born into a prominent banking family and close to the political establishment. Writing to the New York Times, he affirmed “gold is a relic of barbarism to be tabooed by all civilized nation.” Those who advocate the return to a gold standard do not always appreciate along what different lines our actual practice has been drifting. If we restore the gold standard, are we to return also to the pre-war conceptions of bank-rate, allowing the tides of gold to play what tricks they like with the internal price-level, and abandoning the attempt to moderate the disastrous influence of the credit-cycle on the stability of prices and employment? Or are we to continue and develop the experimental innovations of our present policy, ignoring the "bank ration" and, if necessary, allowing unmoved a piling up of gold reserves far beyond our requirements or their depletion far below them? Unquestionably, Keynes was not the first to think of gold as a “relic of barbarism”. Indeed, there have been many others. From the Marxists and the 18th century utopian socialists to the chartalists – followers of the scientific charlatan Georg Friedrich Knapp and precursor of the Modern Monetary Theory – the mood was surely getting progressively averse to a free market, “hard” money regime.

Bearing a less radical approach, there were those, so as to tap into other sources of money, who rallied for a bimetallic standard, such as former US Secretary of the Treasury and three-time Democratic nominee for President, William Jennings Bryan. Furthermore, in lieu of abandoning the gold standard in 1933, President Roosevelt considered introducing a bimetallic regime. Inasmuch as the currency is backed 100% by the gold and silver, there is no dispute on my part. To bring this first part to an end, when the Armistice drew the Great War to a close, the return to some sort of metallic regime was in doubt. Since Europe was devastated after the war, governments were planning on spending greatly, in addition to having to pay colossal debt expenses, politicians delayed the reinstatement of the gold standard for a few years. Because the UK, which was the global hegemon at the time, refused to account for the inflation, its policy makers came up with some creative solutions to protect the pre-war parity of $4.86/£1 and pretend that the inflation had never happened. As you will see on the next instalments, this tradition has never died out. More emphatically, though, the technocratic, progressive and socialist movements were appealing more and more to the masses. Thus, economists and politicians wanted to have a shot at engineering the economic structure, “to stabilise prices” and “control inflation”. On this account, controlling the monetary system was essential. As Keynes pleaded above, we had to disregard the gold standard in order to “moderate the disastrous influence of the credit-cycle on the stability of prices and employment”. What a fool!

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed