|

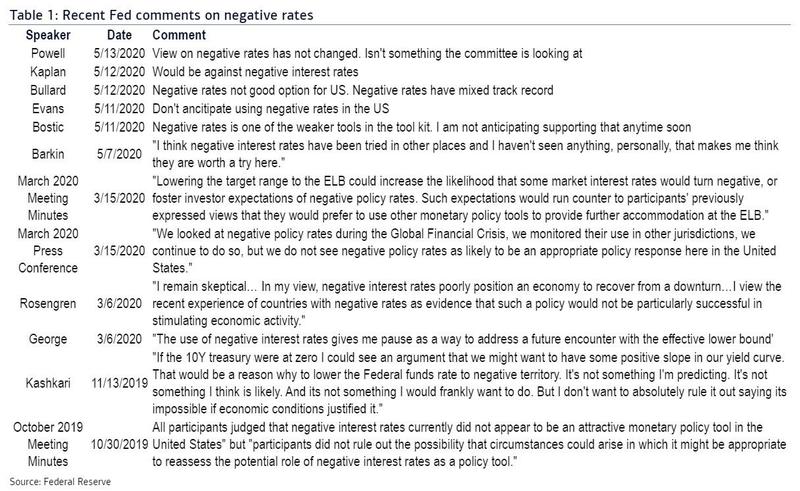

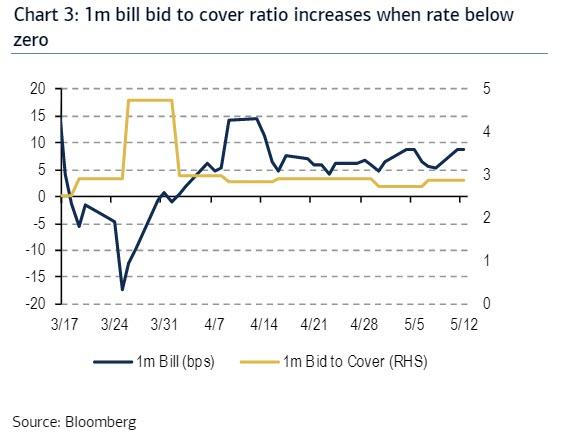

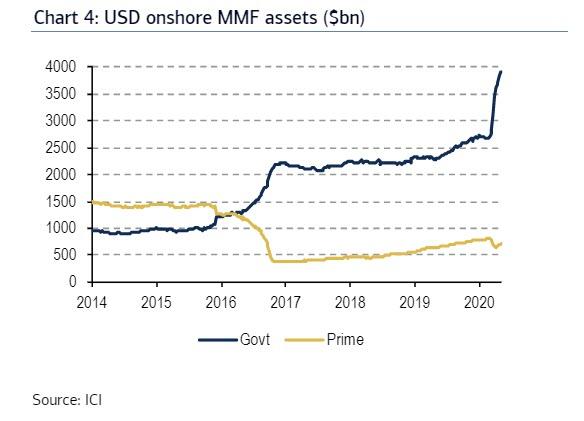

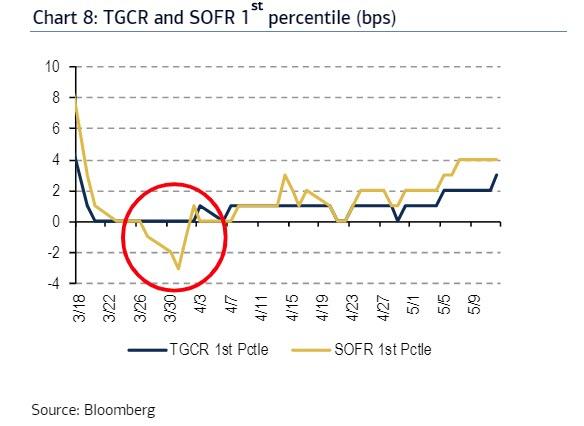

A month ago, on May 7, an unprecedented event took place, as I reported on May 21. After a violent repricing in Eurodollar contracts as near as November 2020, for the first time ever, the market was pricing in that negative interest rates are not only coming to the US, but would arrive sometime around the presidential election.  This move prompted a barrage of Fed speakers, including the Fed chair, to remind the public that the Fed really does not believe in negative rates, even though one could say the same thing for the BOJ, the ECB and the SNB... and look at them now. In fact, in a world where growth is only possible with trillions in new debt injections - and with debt already at crushing levels, interest rates have to be as close to zero if not below it - the Fed has emerged as the seemingly rational outlier that refuses to take rates below the zero lower bound (ZLB). Yet, in a world where the economy was already sinking ahead of the catastrophic collapse spawned by the kung-flu, there is only so much the Fed can do before it is dragged into the NIRP vortex. In many ways the market's expectation for negative rates is rational. Even Goldman Sachs is concerned that the Fed is simply not doing enough QE to monetise the massive upcoming Treasury flood let alone stimulate a global reflationary wave, which leaves it with just one other option: negative rates. Similarly, Nordea's Andreas Steno Larsen looked at this dynamic and reached a similar conclusion: "the Fed is still not buying enough to fully re-ignite the global credit cycle. We find that the Fed needs to buy a lot of bonds compared to issuance before USD scarcity is finally fully eased in the system, leading to easier financial conditions in EM and ultimately global growth prospects being repriced positively". In other words, "the Fed will have to buy more than currently. This speaks in favour of even lower long USD bond yields, not higher". By now, you must know what is wrong with the rationale of the analysts at Goldman and Mr. Larsen. To be sure, the Fed is not central to the monetary and financial system (Eurodollar). Nothing more than a spectator and illusionist. In addition, the market may also be taking hints from former Minneapolis Fed president, Narayana Kocherlakota who argued in an op-ed that the Fed should take interest rates below zero. To use his words, "unprecedented situations require unprecedented actions". On the other hand, there may simply be something in the Minneapolis water that makes local Fed presidents raving monetary lunatics - besides vandals that wreak havoc in their own communities with the poor excuse of a criminal being killed for being black - (here one envisions not only Kocherlakota but his successor, former Goldman banker and TARP author, Neel Kashkari), because while it is quite simple to extrapolate the catastrophic experience the Japanese and European financial sectors have had with NIRP to the US, the truth is that the Fed is rarely this unified in any view. As former Fed staffer and current Bank of America (BofA) rates strategist, Mark Cabana writes, "US negative rates are not an attractive monetary policy tool" and Powell was very clear in this view during his videoconference on May 13. As an alternative to negative rates, Chairman Powell has indicated the Fed can ease through forward guidance, UST and agency MBS asset purchases, or "13-3" extraordinary market programs (i.e. various kinds of facilities and programmes like the ones implemented in March), although here again we run into the huge problem facing the Fed. The most likely alternative to NIRP would be a massive expansion in QE (one which Deutsche Bank calculated at over $3 trillion in more QE). Still, such a dramatic move would also require - most likely - some sort of market event to give the Fed the cover to take QEternity to a truly unprecedented level. It remains unclear how the Fed will square those two constraints. Moreover, Cabana expects Fed officials to "overweight" the above-mentioned tools in support of expansive fiscal policies, "but not shift their thinking on negative interest rates in the near term." As an aside, for those who have missed the recent "Fed talk", below is a summary of the uniform and widespread opposition to negative rates from a range of Fed technocrats.  Of the above, the most striking rebuke of negative rates came from the October 2019 FOMC meeting minutes, when "all participants judged that negative rates currently did not appear to be an attractive monetary policy tool in the United States". It is very unusual to see this type of broad based agreement on any potential policy stance, and as BofA concludes, "in order to see a material change in thinking on negative rates it would likely require a leadership change and large scale Fed turnover". While neither of these is likely in the near term, Trump recent endorsement of negative rates leaves open the door that the president may appoint an even more dovish Fed president in his second term. Undoubtedly, Kashkari would be delighted to be considered for the post of the man who devastates the Eurodollar once and for all. Regardless of all the talk and speculation surrounding the implementation of NIRP in the US, let's see the view taken by Mark Cabana on this policy, concerning the legality, framework and outcomes of this madness. Operational hurdles: IOER Legality In addition to the Fed's own preference - which as events in the past two years have shown can change on a dime, especially once a "shock" triggers a violent market meltdown - there are countless operational hurdles, starting with the question of whether negative rates are even legal. Consider, that in the Federal Reserve Act, it is specifically stated that banks can "receive" interest on reserves. There is no specification for banks paying interest or how negative rates could be set in this context. In her 2016 Semiannual Monetary Policy Report to the House, former Fed Chairwoman Yellen noted that the legality of negative rates "remains a question that we still would need to investigate more thoroughly". This question has not been definitively answered and it is not clear whether the Fed would actually charge negative interest or implement a fee for holding reserves. Indeed, the Fed having not ruled out negative rates suggests it likely has adequate legal cover to establish such a regime. Additionally, while just two months ago one would have argued that it is illegal for the Fed to buy corporate bonds, a quick meeting between Chairman Powell and Secretary Mnuchin, which led to a bizarre joint venture between the Fed and the Treasury, changed all that in the blink of an eye. In short, as Cabana writes, "if the Fed wanted to implement negative rates they could find a way to do so but could face pushback". Despite being an important hurdle, it is turning out to be a surmountable one for the Fed to clear before implementing negative rates. Treasury auction obstacles NIRP legality aside, treasury auctions provide another obstacle for bills and nominal coupons. Treasury auction regulations via the "Uniform Offering Circular" state that nominal coupons and bills are permitted only to have a bid rate that is "a positive number or zero". This is striking since in August 2012, Treasury announced it was in the process of building the operational capabilities to allow for negative rate bidding in Treasury bill auctions. Therefore, it is safe to assume that the Treasury has subsequently built the operational capacity to auction bills and nominal coupons with negative rate bidding, though it is unwilling to take this capacity live. In spite of being unclear why the Treasury might be reluctant to take this step, it could be on account of: (i) Treasury is worried about sending a signal about the economic or monetary policy outlook; (ii) there may be legal or accounting hurdles that need to be cleared up. Furthermore, Treasury's inability to auction bills or nominal coupon securities with negative rates results in an inefficient primary issuance process, when secondary market rates are negative. Inasmuch as the Treasury offers securities at par, bidders can then sell these securities into the secondary market at a premium. Basically, this brings about a subsidy to the primary dealer or Treasury bidder community that should be captured by the Treasury - you can learn more in "Here Is The Treasury's (Not So) Secret Trade Printing Millions In Guaranteed, Risk-Free Profits Every Day"). Treasury auction rules suggest that when a security is auctioned at par, the bidders have their allocations determined on a proportional basis to their auction offers. Consequently, bid-to-covers spike when secondary market levels are below zero at auction.  Likewise, Treasury rules state that among fixed rate debt, only TIPS can have a negative bid rate. Even though Treasury floating rate debt can be auctioned with a discount margin that may be positive, negative, or zero, there is a 0% minimum on interest accrual. Because of the Treasury rules, an investor is never required to pay the US Treasury during a period of CPI deflation or during any future period in which bills might be auctioned at negative rates. Notwithstanding, just like the legality issue, BofA does not see Treasury auction limitations as a material constraint to adopting negative rates "since we assume operational hurdles can easily be overcome. However, allowing negative UST bidding for bills and nominal coupons is another important operational hurdle that will need to be addressed before negative rates can be more widely adopted". Money Market Funds in a negative rate environment As Cabana continues, a key concern around negative rates in the US is the viability of money market funds (MMFs). The MMFs' AUM (assets under management) total $4.8 trillion with the vast majority in government funds. Also, MMFs play an important role in funding, making up roughly 25% of all cash lending in repo markets. Concerning net asset value (NAV), negative rates are particularly problematic for stable NAV MMF. To recall, 2a-7 MMF reform requires institutional prime & municipal funds to have floating NAV, while government and retail prime plus muni funds to have $1 stable NAVs. Negative rates are an issue for stable NAV funds owing to the fact the fund value will decline by virtue of investing in negative yielding assets. To address this NAV stability in a negative rate environment, MMFs in the US would need to move to a floating NAV regime, potentially increase customer fees, or use a share cancellation regime. The latter two options are more likely given that changes in the stable NAV structure could potentially cause sudden changes in fund allocation, as it occurred during the 2016 MMF reform.  Increased MMF customer fees or a share cancellation regime are more likely in a negative rate environment versus a shift to floating NAV for all funds. In a regime with higher MMF customer fees, the stable $1 NAV could still be retained, although the principal invested in the fund would gradually be reduced by the fees charged to compensate the fund for the negative yielding securities. On the flip side, in a share cancellation regime, a MMF would retain the $1 stable NAV, but gradually reduce the number of shares an investor is entitled to at redemption. For example, an investor that deposits $100 and receives 100 MMF shares in a -1% negative rate environment would see their shares gradually cancelled; 1Y later they would receive $99 in cash at redemption. Depending on the implementation of negative rates in the US, MMFs may also face competition with deposits. If the Fed sets IOER negative, despite immediately impacting market rates, it may not be passed onto consumers. Hence, banks may charge fees or other service costs so as to offset their negative IOER rate, prompting outflows from MMFs into deposits, which are often considered close alternatives. As a result, retail MMF investors would be the most prone to shift to bank deposits given reluctance in the banking industry to charge negative deposit rates for retail consumers. The bottom line is the US MMF industry would in all likelihood be able to adapt to a regime of negative yielding interest rates if given enough time to prepare. Nevertheless, MMFs and front end investors would possibly need at least 6 months to 1 year of heads-up from the Fed that negative rates are in the making, so that they could properly adjust their system. Ominously, Cabana says that his "sense is that several MMFs are already preparing for the possibility of negative rates". The Eurodollar futures' market participants are certainly betting on it. Other issues: systems and repo The take home from the above, is that if the Fed were to take rates negative, Cabana is confident that it would need to provide ample lead time to the market to arrange the financial system for such a change. Ergo, market participants would need to adjust trading, settlement, accounting, tax, and legal systems or procedures to prepare for negative rate trading. While some of these operational hurdles have already been cleared for large global firms given the periodic negative rate trading of US Treasuries and other developed market sovereign bonds, more time would be needed to prepare for domestically oriented firms. In addition, the Fed would presumably prefer that firms focus their operational resources on preparing for the transition away from LIBOR rather than on negative rates, which may further limit the Fed's willingness to take rates below the ZLB in the near term. One area where Cabana does have serious questions on the operational readiness for negative rates is in the repo market. Albeit not an issue for specific UST collateral, which has frequently traded at negative rates following UST fails charge in 2009, this is a question centered on the tri-party repo market where it is unclear if there is operational capacity for rates to trade at negative levels. Recently, questions emerged given that in late March, the 1st percentile of the SOFR rates traded in negative territory, while the 1st percentile of tri-party general collateral repo rate (TGCR) remained at zero. This was the first time this segment of low-rate TGCR trades exceeded SOFR.  Finally, if this is correct, and there are operational issues with taking tri-party GC repo into negative territory, then this is a material operational impediment, and as Cabana writes, "we cannot envision the Fed moving into negative territory until the tri-party repo market can easily follow suit".

To conclude, NIRP surely entails several challenges to the functioning of the present financial system. Although the technical and legal issues can be overcome rather easily (as is shown above), the real world consequences of such a policy, were it be put to practice, would be severely disastrous. On part two, I am going to delve into the manner two important segments of the financial system will be operating: the repo market and, obviously, the financial intermediation. Lastly, the winners and losers of the absurd NIRP paradigm are going to be exposed, as well as the grounds and motivations for its implementation.

0 Comments

|

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed