|

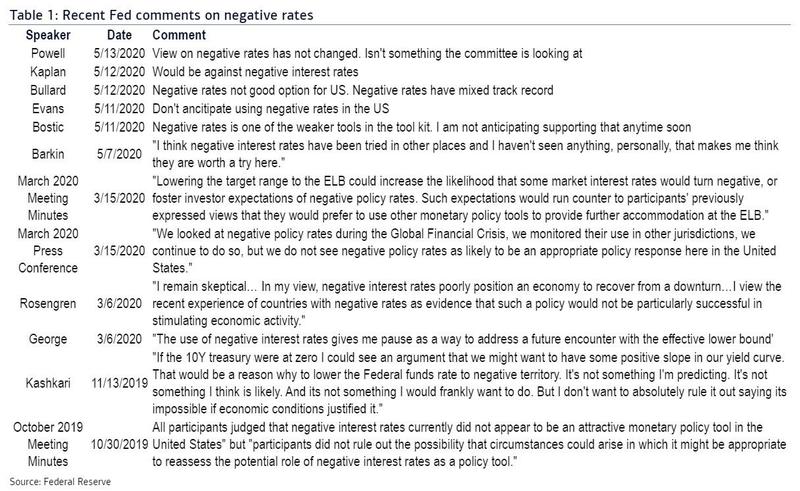

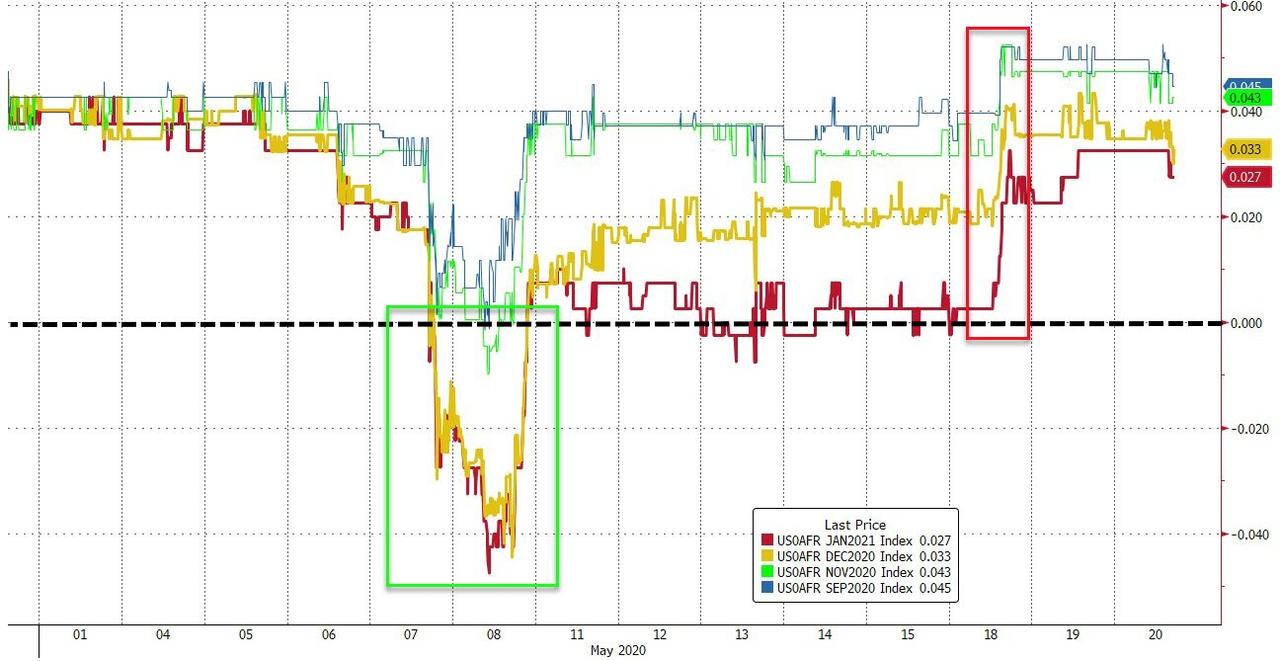

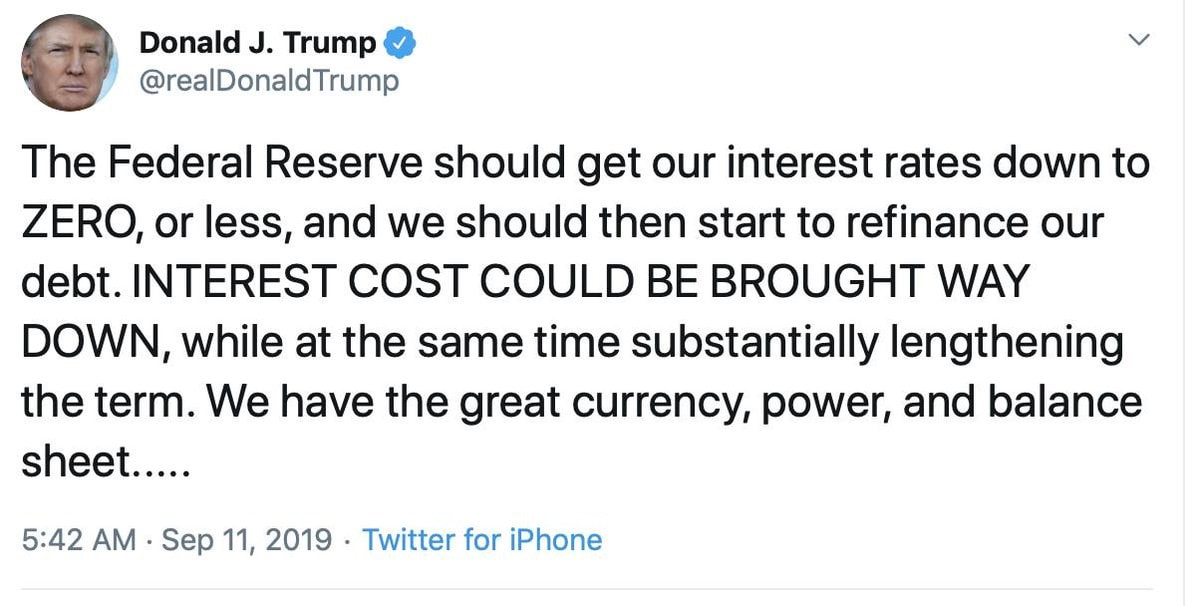

If Jerome Powell hoped that he had put to rest the topic (and debate) of negative interest rates in the US (if only for a few weeks), it turns out he failed. One day after Powell's ad hoc appearance in a Peterson Institute video chat in which Powell was very clear: the Fed does not support negative rates, even with downside economic risks - the question of when, not if, rates will turn negative continues to dominate. In an attempt to amplify Powell's message, Bank of America's rates strategist and former NY Fed staffer Mark Cabana wrote last Thursday, May 14, that the Fed is rarely this unified in any view: "US negative rates are not an attractive monetary policy tool". Adding that Chair Powell was very clear in this view the previous day. In addition, it is not just Powell of course, a whole bunch of Fed officials are uniformly opposed to negative rates. The most striking rebuke of negative rates came from the October 2019 FOMC meeting minutes when "all participants judged that negative interest rates currently did not appear to be an attractive monetary policy tool in the United States", though "participants did not rule out the possibility that circumstances could arise in which it might be appropriate to reassess the potential role of negative interest rates as a policy tool". Again, it is very unusual to see this type of broad based agreement on any potential policy stance, according to Cabana who adds that in order to see a material change in thinking on negative rates, "it would likely require a leadership change and large scale Fed turnover. Neither of these is likely in the near term". Below there is a summary of the uniform and widespread opposition to negative rates from the technocrats at the Fed.  For the first time ever, the fed funds futures market two weeks ago, on May 7 and 8, priced in slightly negative rates starting this autumn, as is shown in the next graph. After a violent repricing in Eurodollar contracts as near as November 2020, for the first time ever, the market was pricing in that negative interest rates are not only coming to the US, but would arrive sometime around the presidential election. This move prompted a barrage of Fed speakers, including the Fed Chairman, to remind the public that the Fed really does not believe in negative rates (but never say never), even though one could say the same thing for the BOJ, the ECB and the SNB... and look at them now. In fact, in a world where growth is only possible with trillions in new debt injections and with debt already at crushing levels, interest rates have to be as close to zero if not below it. Hence, the Fed has, ironically, emerged as the "irrational" outlier that refuses to take rates negative. And yet, in a world where the economy was already sinking - since at least Q4 2018 - ahead of the catastrophic collapse spawned by the coronavirus, there is only so much the Fed can do before it is sucked into the NIRP vortex.  For the clueless financial analysts and investors, seeing that the Fed is simply not doing enough QE to monetize the massive upcoming flood of Treasuries let alone stimulate a global reflationary wave, the expectation for negative rates appears to be rational. Taking Nordea's Andreas Steno Larsen as Exhibit A, "the Fed is still not buying enough to fully re-ignite the global credit cycle. We find that the Fed needs to buy a lot of bonds compared to issuance before USD scarcity is finally fully eased in the system, leading to easier financial conditions in EM and ultimately global growth prospects being repriced positively". In other words, "the Fed will have to buy more than currently. This speaks in favour of even lower long USD bond yields, not higher". Likewise, with Mark Cabana as Exhibit B, he argues that in alternative to negative rates, Jay Powell has indicated the Fed can ease through forward guidance - promise to do whatever is needed to support the markets, without having to act -, UST and agency MBS asset purchases, or other extraordinary market programmes, although here again we run into a huge problem facing the Fed. The most likely alternative to NIRP would be a massive expansion in QE (one which Deutsche Bank calculated at over $3 trillion in more QE), yet such a dramatic move would also require - most likely - some sort of market event to give the Fed the cover to take QEternity to a truly unprecedented level. Evidently, these experts have it all backwards. They want the Fed to embark on a colossal Treasuries shopping spree so as to provide the financial system with all the greenbacks the market participants demand, aiming at easing the financial conditions. Therefore, the US bond yields must fall. This reasoning is so flawed I do not even know where to begin. Contrary to the common orthodoxy and beliefs withheld by these buffoons, neither QE or any other asset purchase programme alleviate financial constraints. Additionally, even if they did, the yields of the Treasuries would rise. By reading the Eurodollar system: the untamable beast series, you become aware that QE and the like are a huge failure. In spite of having the goal of keeping the plumbing of the financial system running smoothly and, as a result, creating the conditions for the economic activity to resume its pre-GFC growing pace, these unconventional policies have been much ado about nothing. The reality is market participants will only move on to riskier investments, when they assess that the economic landscape offers good opportunities, regarding the expected returns and risks. Once they notice good investment opportunities are multiplying, either in the real economy or the financial markets, investors will shift from safer investments into riskier ones. Accordingly, the Treasuries start to get dumped, resulting in higher yields. Although not for the reasons stated by Andreas Steno Larsen, the UST yields are set to continue subsided, though, due to dreadful economic prospects, which lead to a continuation, or even worsening, of the liquidity constraints. Moreover, Mark Cabana writes that he does not think "the market can 'bully' the Fed into adopting negative interest rates". As he explains, while the market can push the Fed to adopt a number of policies, "the case for negative rates is fundamentally different. Negative rates have meaningful implications for the financial system and financial intermediation. In addition, Cabana elaborated an extensive list laying out all the various reasons why negative rates are virtually impossible, ranging from legal, to structural, to behavioral - a topic for another day. However, it is fascinating that despite Powell's solemn admonition and the myriad of reasons why NIRP is likely not on the agenda, the market simply refuses to care. According to Bloomberg, in an article explaining why negative rates "are the Only Game in Town" for Eurodollar option traders, bets that negative rates are coming have soared, as calls that pay off if the Fed sets the target floor of the Fed Funds rate below the Zero Lower Bound (ZLB) between September 2020 and June 2021 have been in high demand this month.  The bottom line is that far from not "bullying" Powell, the market is just waiting for the next opportunity to pounce on what now seems to be a monetary inevitability: negative rates in the US. Obviously, the Fed is a laggard, acting solely on what the markets are signaling, despite the convictions that the central bankers are at the helm of the financial system. Furthermore, with the US following the path of Japan for more than a decade, it is only a matter of time before the Fed imitates every wrong move in the BoJ playbook, starting with negative rates and concluding with buying equities. All the technocrats need is a catalyst for the next move, like for example the next sharp drop in equities, which will happen sooner or later (very soon, in my opinion). Finally, at least President Trump would be happy, considering he may have been the biggest bully of Powell and his posse, being very outspoken about his wish to see the EFF rate pass below the ZLB and everyone should be glad to welcome such a "gift". What Trump does not understand - or maybe he does but he is acting in accordance to selfish interests - is that low interest rates are an indication of a terrible economic environment, being very uninviting for business and risk-taking, as I expounded above and before. Undoubtedly, the POTUS has not been the only one voicing the desire for NIRP. Several (keynesian) economists have been insisting on this policy, including researchers at the IMF, as I discussed in a previous post. Similarly, Harvard University professor, Kenneth Rogoff, has said the Fed is making a mistake by not having negative rates in its tool kit. He said the Fed’s purchases of corporate debt and junk bonds allows even weak companies to stay afloat. Additionally, he stated that "if we are able to do deeply negative rate policy, it would keep a lot of companies afloat. There would be others that would need to be restructured. The fact it's taken off the table is a mistake". Thus, the plan is to keep this zombie economy limping and dragging forward, while destroying savings and enriching the wealthy, so that the status quo is maintained. All in all, business as usual. Only an idiotic keynesian (redundant, I know) is capable of such ludicrous ideas, which by the way certainly makes Professor Rogoff one of the greatest contenders for the Nobel Prize in Economics.

In conclusion, with the Fed acting upon the whims of the markets and with these pointing for negative Fed Funds rate, Chairman Powell will reluctantly implement the infamous NIRP. Unsurprisingly, power-grabbers and keynesians (once again, excuse the redundancy), as well as shareholders and corporate executives, will surely rejoice with this huge nail in the coffin of Capitalism being hammered, possibly being the last one needed to bury the free-market system once and for all.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed