|

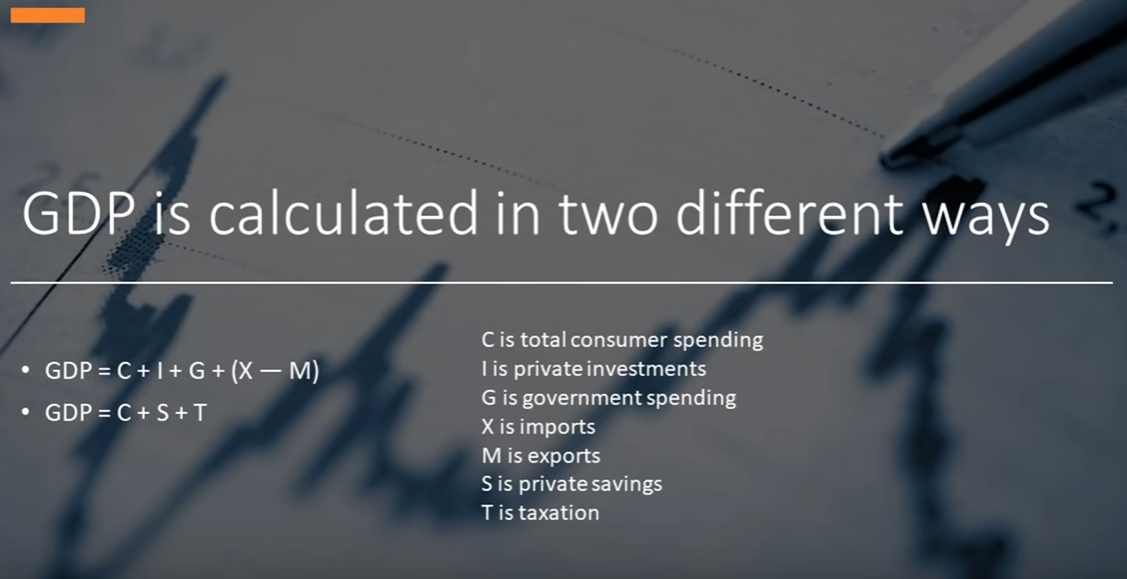

During periods of social turmoil and widespread dissatisfaction with the state of (economic) affairs, while true explanations, not to mention solutions, are hard to find, all kinds of theories and panaceas come to light. In this day and age, the revolutionary breakthrough that is set to cure our economic malaise is the Modern Monethary Theory (MMT). What is it? In a nutshell, it is the idea that governments can use deficit spending to help their economies to reach full-employment and to promote savings with very little downside. Furthermore, if the economy gets "over-heated", meaning that "inflation" becomes too high, government simply raises taxes so as to curtail demand. Unsurprisingly, politicians and technocrats love this "new" school of thought seeing that it provides our overlords the grounds to use the powers at their disposable, or to acquire even more, under the veil of boosting economic activity and, more importantly, the general welfare. Be that as it may, the expansion of the government scope is no recent phenomenon - in March of last year, before I began paying attention to Jeff Snider's work, I wrote about this, though I must warn you that the conclusion comes from the erroneous premiss that central banks create money; so you should stick to just the first seven paragraphs. In fact, the Leviathan has been growing, in the West, since the early twentieth century, or even sooner than that. Like I said on the previous post, the government enlargement reminds me of the film The Blob, where this jelly-like, extra-terrestrial being reaches our planet and immediately starts to consume the people nearby, ballooning a bit more from each person it gollops. Hopefully, you will see this is a great metaphor about the destructive entity we know as government. As Milton Friedman affirmed, "if a private venture fails, it is closed down. If a government venture fails, it is expanded." This little aphorysm sums it up perfectly. At the onset, some politician spots some "issue" or "injustice" or, to be frank, something that he thinks will rally support from some special interest group (or a coalition of them) to get him elected. Once at the office, a programme with the aim at solving the "issue" is carried out. Then, because it is government nonetheless, the programme fails to accomplish its objective. Does this mean the politicians and bureaucrats acknowledge the errors of their ways and decide to shut it down? Definitely not. They just declare the programme lacked sufficient funds and resources. Hence, the government keeps on growing and those "issues" are yet to be resolved. Nevertheless, this enlargement takes its toll on the economy and our liberties and, therefore, on people's well-being. In the end, everybody is made worse off. Firstly, let us find out the rationale behind MMT. For the modern monethary theorists, all of their reasoning derives from looking at how the GDP statistic is calculated and then playing around with equations to show that private savings are somehow the function of government spending. It all boils down to this equation: G-T=S-I. To understand what this means, we have to go back a few steps. As every Economics graduate knows, there are three approaches of measuring GDP: income, expenditure and output. Evidently, the most used method is the expenditure one, which employs the following inputs (next graph) in those two possible formulas.  Obviously, these two equations equal each other and we can eliminate C because they cancel each other out. Then, we can take out net exports (X-M) for matters of simplification. Finally, by swapping T and I, we get to the final equation (G-T=S-I). If you prefer, as Robert P. Murphy has put it much more elegantly: government budget deficit = net private savings.

Thus, the MMT-ers are working at an extraordinary level of remove and abstraction from the real economy. All these figures in the GDP calculation are incredibly broad, rough, crude aggregate numbers, which in reality provide us very little about what is going on under the hood. Notwithstanding, turning the absurdity to eleven, they imagine that playing around with aggregate data in this statistical construct, i.e. econometric model, has causal explanatory power in the real world. Without surprise, this has no explanatory power whatsoever. Mulling over this hypothesis, one can plainly appreciate its silliness. In order for you to forego consumption (that is to set aside some portion of your wages for a rainy day, for instance), you require the government to employ people to dig a ditch or build a bridge. Of course they do not present it in this manner. By surveying them about this, they would say that in aggregate if you add up all of the savings of all the people, then you will get a bigger number were the government to spend more on boondoggles. In short, the story goes like this. For a start, supposing the government concentrated all its efforts solely on ditch digging and bridge building programmes. This would of course affect the prices of all materials used for these public works, such as shovels, helmets, steel, etc. Moreover, the ditch diggers and the bridge builders get paid, making them the first receivers of this freshly-created currency. Accordingly, they get to buy consumer goods first and then the money ripples through the economy. Ergo, the inflationary impact takes root, prompting prices to rise across the board. Due to inflation, people's savings, especially fixed-income, are reduced in real terms. On the flip side, the diggers and the bridge builders got to enjoy cheaper items at the expense of other people's savings. The latter have been made worse for the former cohort's benefit. In effect, it is a redistribution scheme from the public to the government's contractors. As a result, far from increasing aggregate savings, this policy will hurt savers in general. Furthermore, on the one hand, the central banks' monetary policies consist of creating money only on the minds of those in the financial system, as well as the public at large, instead of real, usable money. On the other hand, the government, with its fiscal arm (Ministries of Finance or the Treasury in the US), can actually originate and expand the money supply. Contrary to popular belief, on account of the monetary system being a debt-based one, central banks cannot cause inflation because they are not capable of generating their own debt obligations. All the same, once the deficit spending is implemented, the money supply swells, which alters prices in the real economy. Despite this, there is more to the story. In reality, the outcomes and the chain reaction instigated by government spending are very complex, ending up producing effects that go against what one may initially think. As I have mentioned a few times before, government interventions always brings about a system of pernecious incentives that makes the economy less dynamic due to arising distortions in the production structure (malinvestments). To wit, this meddling by the State has been yielding an increasingly unfriendly landscape for businesses and entrepreneurship, hampering economic development - think about it, shouldn't we all have private jets and flying cars by now -, and has given rise to an ever expanding class of welfare dependents to boot. In such a scenario, how is it possible for credit institutions (banks) to originate loans to individuals and businesses with a devil-may-care attitude? In the pre-GFC era they did and it ended horribly, as you know. Because of that experience, banks have learned their lesson and, as I demonstrated on the previous post, they have since then taken a much safer, risk-averse stance. Regardless, what really grinds my gear is the fact that the MMT-ers think this is some groundbreaking theory. For presumed experts in the field of economics, their ignorance is really astounding - which just goes to show, once again, how economists seldom do economics. For a true (monetary) economist, money has emerged as a natural market phenomena to solve the problem of a barter system having to rely on the double coincidence of wants. Some commodity would emerge, be it shells, precious stones or metals to act as a medium of exchange. For example, this process is at work in prisons where it is often the case that cigarettes come forth as the medium of exchange. However, the advocates of MMT reject this explanation of the origin of money and follow a doctrine known as chartalism, initiated by Georg Friedrich Knapp from Germany, which holds that all money derives from government. Accordingly, all money is fiat money (charta, in Latin), arising out of the government's need to levy taxes. In this view, money is not a commodity, but a function of law. Actually, money comes about spontaneously in the free-market, not by legislative decree. The former approach is exactly how the Eurodollar system came to fruition and we also have the recent interest in cryptocurrencies to prove this. Just ask Venezuelans if the latter approach works. Besides the domestic currency, bolívar, having lost all its credibility owing to its debacle in the last four or five years, their state-sponsored cryptocurrency, Petro, launched in 2018, and allegedly backed by the country's oil and mineral reserves, is used by nobody. Instead of these two, can you guess which currency is favoured? US dollar. Speaking of money, let us resume our discussion about inflation. Curiously, in spite of the MMT-ers and their biggest critics (those on the inflation camp and dollar bears) being so ideologically opposed to one another, they are equally wrong - to be fair, MMT-ers are far worse. For the aforementioned critics, they are sort of right with regard to EM countries, due to what I showed in the January 13 post, when they claim deficit spending to curb an economic contraction or a downside deviation from the potential has a serious risk of opening the Pandora's box of inflation. Nevertheless, considering the developed countries, they are utterly mistaken. As I stated earlier in this post, the gradual encroaching in the economy by the government has led to risk-off, deflationary conditions, provoking a shift from risky assets and investments to more safe and liquid instruments and securities, of which sovereign bonds, particularly US Treasuries and German bunds are the taken as the best. Turning to the MMT supporters, their view is flawed on two fronts. For one, they believe they can get the government to spend limitlessly, because of the printing press, until the economy is growing at full-potential, or as they often call, at full-employment. Interestingly, they use these terms interchangeably as if they are the same thing. In my opinion, this simple confusion is perhaps the main source of this lunacy. Supposing, for the sake of argument, every According to MMT advocate Phil Armstrong, of York College, "[t]he existence of unemployment is clear de facto evidence that net government spending is too small to move the economy to full employment, (...) [the government] must use its position as a monopoly issuer of the currency to ensure full employment." Thus, when the private sector is unable to push the economy to full-employment, MMT-ers came up with the idea of a "jobs guarantee" that provides government-funded jobs to anyone who wants or needs one, begetting a long-awaited boom at last - easy-peasy, lemonsqueezy. However, the spending on such a programme would be curtailed when the economy reaches full-employment, having also the ability to raise taxes if the economy gets "over-heated". As you can predict, it will not become "over-heated". Just because everyone has a job, and owing to being created by a bunch of bureaucrats who are not guided by the profit and price system but by special interest groups, it does not mean these are productive jobs. This brings us to the other flaw in their view. They defend that once full-employment is reached, having been absorbed by that "jobs guarantee" programme, the private sector, on account of being starved for workers and having the government as a competitor in the labour market, will have to increase wages. As one prominent MMT-er stated, L. Randall Wray (on the same article linked above), "if the private sector can match you [the government], then you get into a bidding war and you can cause inflation and you will drive up prices. You can cause inflation, and you will cause inflation, if you reach full employment, and you continue to try to increase spending." Therefore, they reject the notion that inflation is always and everywhere a monetary phenomenon and that it causes distortions in the price system - what I take from this this, inflation for them only occurs when the YoY rate of the CPI or the PCE is above the 2% target, or something like that. MMT-ers argue that inflation only crops up when the supply of goods or labour, or the capacity is filled, is too little to meet the demand for them. Finally, this is the long discredited theory of idle resources, a special from our old chum John Maynard Keynes, back in a new disguised form. As you may be presuming, this theory was demolished almost as soon as it was birthed, although very few people have apparently noticed it. To put it succintly, Keynes' argument may be simplified as follows. Full-employment should be our goal. The market system will not get us there, as a result it requires government help and guidance as well. In practice, this means that government will continually "print money" to reduce interest rates, ultimately to zero if it has to, and also borrow and spend as needed. As he affirmed, "the right remedy for the trade cycle is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom." In a nutshell, this is absolutely absurd. For starters, one cannot create wealth simply by "printing money" or by borrowing and spending funds. Moreover, the real source of unemployment is some disturbance in the price and profit system. Like I pointed out earlier on, the government cannot possibly help matters by intervening in ways which further distort and perturb that system. As a matter of fact, a permanent condition of full-employment is not only indefinable, but also undesirable. In short, unemployment is an inescapable condition of a dynamic economy due to the creative destruction phenomenon, coined by the Austrian economist Joseph Schumpeter. To conclude, Modern Monethary Theory is not some "new economics". It is just a lot of old, debunked ideas, which have been exposed in both theory and practice countless times before. Having been repackaged and rebranded, it has been then sold to gullible journalists and idiotic politicians who have an interest in bribing voters with shiny goodies. To cap it all off, if there is anything as certain as death and taxes in this world, it is that journalists, politicians and the electorate, by and large, proceed to be moronic, no matter how many times these terrible ideas are proven to fail. Consequently, the Blob keeps on growing. Furthermore, while reading this you have surely sensed some familiarity with the MMT thesis, which I have already alluded to. Seeing that this post is getting too long and there is still much to analyse, I will save the rest for another day.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed