|

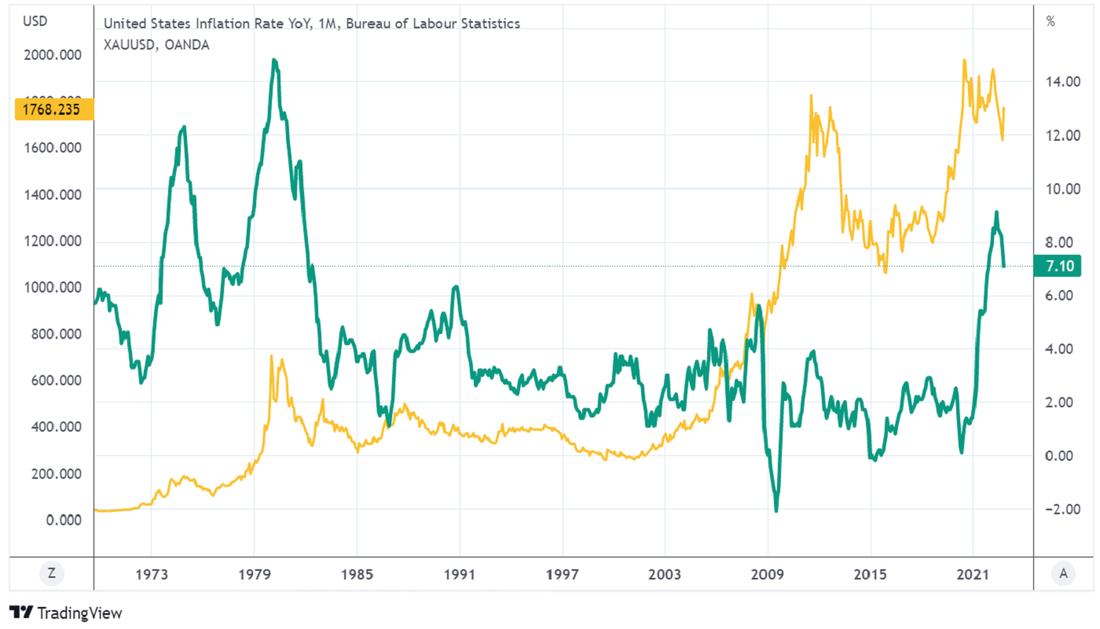

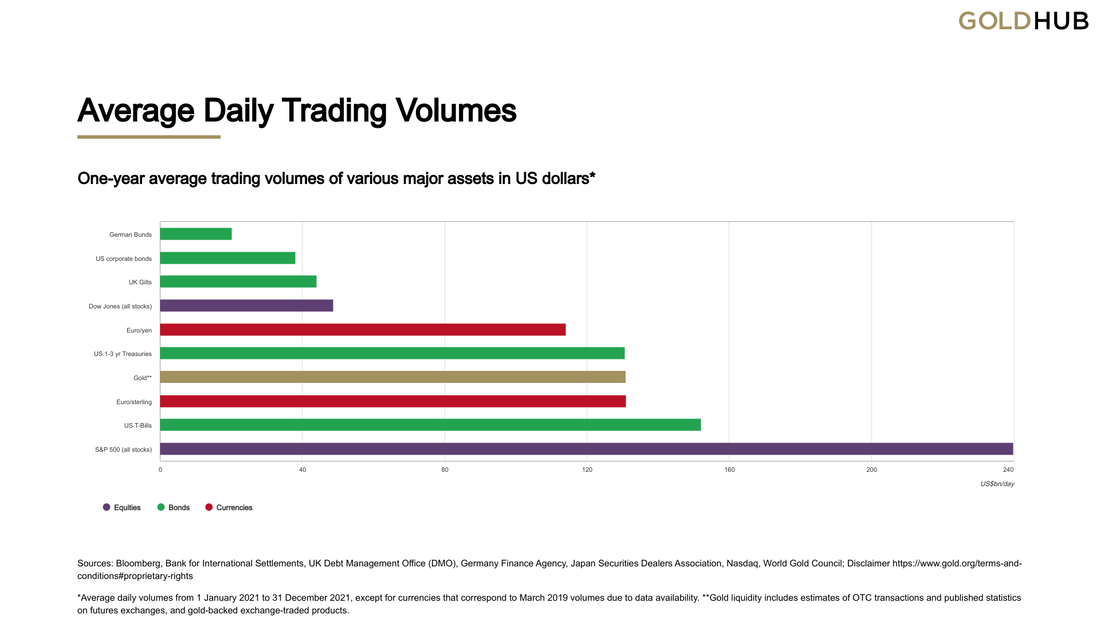

Resuming the history of gold where we left off in the first part, this second instalment is completely dedicated to understanding the factors influencing the price of gold since the advent of the eurodollar system. Specifically, even though this monetary and financial revolution had cropped up in the 1950’s, those factors only took the helm on August 15, 1971, when the gold window was closed by President Richard Nixon. Since the end of the Bretton Woods system (BWS) and all currencies in the world became detached from gold, the era of fiat currencies started. However, gold was not dismissed and forgotten. In lieu of having its price fixed to the US dollar and indirectly to the other currencies – in the BWS, the dollar was pegged at 35$ per ounce of gold with all other currencies having each one its own peg to the dollar –, gold became subject to market forces just like any other asset. When inquiring financial analysts and investors, including goldbugs, on the reasons to acquiring gold, they respond that the precious metal acts as a hedge against inflation and as a safe-haven. In other words, they project the gold price to follow the expansion of the (debt-based) money supply. Nevertheless, they commit a terrible mistake by equating inflation with “inflation” – i.e., a general rise in prices, Machiavellianly computed in government statistics like the CPI. In reality, gold has performed its functions rather well, despite the alleged inertia during the occasional bursts of “inflation”.  As the graph above shows, the relation between gold and “inflation” is not clear, at all. Naturally, this bewilders most observers and frustrates gold standard advocates. In view of being unaware of the dominance of the Eurodollar beasts and instead putting the central banks at the centre of the monetary world, the goldbugs presume either that there is some trickery going on or that the central banks’ credibility is persuading speculators and investors to stay away from gold. Taking the latter into account, some analysts think gold has not reacted to the recent surge in the CPI, of most countries, because the central banks are hiking rates and quashing the market’s inflationary expectations. Thus, due to trusting the capabilities of the monetary authorities and forecasting a higher yield paradigm, the participants are being lured into other assets that bear interest. Simply put, this is utter nonsense. Making the words of the author of the article just referenced, Claudio Grass, my own, “I do not believe that short-term price considerations should play a pivotal role in the decision-making process of investors who hold gold for the right reasons and who understand why they do. What is important, however, is to look beyond the mainstream headlines and to be able to separate the signal from the noise.” Indeed, that is exactly what I am going to do now. To be fair, it does involve some trickery, though, totally legal. All the same, there is a method to this madness. Disclaimers aside, let’s dig in. To begin with, the international gold price usually refers to the price of gold quoted in US Dollars per troy ounce as traded on the 24-hour global wholesale gold market. During the entire business week, gold is traded non-stop globally, allowing the incessant quoting of international gold prices, from Sunday night London time all the way through to Friday night. Depending on the context, this international gold price sometimes refers to a spot gold market quote, such as spot gold traded in the London over-the-counter (OTC) market, and at other times may refer to the front month of a gold futures contract price as traded on the US Commodity Exchange (COMEX). Some years ago, an academic paper has determined that gold price discovery is jointly driven by London OTC spot gold market trading and COMEX gold futures trading, and that the “international gold price” is derived from a combination of London OTC gold prices and COMEX gold futures prices. In general, the higher the trading volume and liquidity in a specific asset market, the more that market contributes to discovering prices for that asset. Obviously, this is also true of the global gold market. Between them, the London OTC (a.k.a. Loco London) and New York trading venues account for the vast majority of global gold trading volume, and in 2021, the London OTC venue, which englobes spot, forwards and options trading, represented approximately 45% of the global gold market turnover, while COMEX accounted for a further 32%. Although this pair holds the dominance of the market, their supremacy is crumbling down quickly. Demonstrably, that academic paper points out that in 2015, the London OTC market gathered 78% of global gold market trading volume, while COMEX had a mere 8% share of the marketplace. Fundamentally, the two reasons for this occurrence are the demand for gold being increasingly coming from the East, mainly China and India, and the regulatory burden imposed after the GFC is forcing a shift towards exchange trading, which includes futures markets such as the COMEX or the SHFE. On that account, beyond the London OTC gold market and the COMEX, all the other gold secondary trading venues negotiate with the price settled in London and New York. Ergo, they are considered price takers. Still, the trend is for these exchanges to turn progressively into price setters, contributing more to the price discovery mechanisms, as the balance of power swings eastward. Furthermore, the international gold price can also at times be referring to the LBMA Gold Price benchmark price – LBMA is an abbreviation for London Bullion Market Association –, as derived during the London daily gold price auctions (morning and afternoon auctions). Before it got this name, in 2015, it was called the London Gold Fix, which had been clouded by mistrust and even repudiation for a very long time. Ultimately, this led to its restructuring and rebranding, albeit not managing to shake off its reputation, rightly so. Therefore, insofar as they are all similar in magnitude, this international price could be referencing a spot gold price, a futures gold price, or an auctioned gold price. Be that as it may, the trio can each one be considered a benchmark. In spite of having been found, as we have just seen, to have lower trading volumes, COMEX presents a larger influence on price discovery than Loco London. This is most likely due to a combination of factors such as COMEX’ accessibility and extended trading hours via use of the GLOBEX platform, the higher transparency of futures trading compared to OTC trading, and the lower transaction costs and ease of leverage in COMEX trading. Conversely, the London OTC gold market has limited trading hours (during London business hours), barriers to wider participation since it is an opaque wholesale market without central clearing, and trading spreads that are dictated by a small number of LBMA bullion bank market-makers and a handful of London-based commodity brokerages. Hence, efforts are being made so that the exchange-traded contracts of the London Metals Exchange gain prominence, in order for London to keep the “terminal market” epithet. To make long story short, the international gold price is fundamentally set by paper gold markets. In other words, it is set by non-physical gold derivatives. Based on their respective gold market structures, Loco London and COMEX are both paper gold markets. Perversely, the supply of and demand for physical gold plays no role in setting the gold price. Because of this, physical gold transactions in all other gold markets just accept the gold prices that are discovered in these paper gold markets. On the one hand, London OTC gold market predominantly involves the trading of synthetic unallocated gold, where trades are cash-settled and not physically delivered (i.e., no delivery of physical gold). Due to convention, unallocated gold positions are merely a series of claims on bullion banks where the holder is an unsecured creditor of the bank, and the bank has a liability to that claim holder for an amount of gold. In turn, the holder, takes on credit risk towards the bullion bank. As a result, London OTC gold market is nothing more than a venue for trading gold credits, employing fractional reserve gold trading with colossal amounts of paper gold born ex nihilo. On the other hand, COMEX only trades exchange-based gold futures contracts, rendering it, unmistakably, a derivatives market. However, less than 1% of COMEX gold futures contracts are usually registered to take delivery. Perhaps this why this venue only stores 1 of every 600 oz in existence worldwide, even though, as I have exposed, the COMEX contributes the most to the discovery of the international gold price. Seeing that very little physical gold is ever delivered on COMEX, and even less physical gold is withdrawn from its approved gold vaults, COMEX registered gold stocks are relatively small. COMEX gold trading also employs significant leverage. In their paper, Hauptfleisch, Putniņš, and Lucey state that “such trades [on COMEX] contribute disproportionately to price discovery”. Note that the COMEX gold futures market is actually a 24-hour market, but its liquidity is highest during US trading hours. Turning to Loco London, nearly the entire trading volume of the London OTC gold market represents trading in unallocated gold, which merely represents a claim by a position holder on a bullion bank for a certain amount of gold, a claim which is rarely exercised. In addition, traders, speculators and investors in unallocated gold positions virtually never take delivery of physical gold. Consequently, Loco London trades also predominantly cash-settle. In 2013, this was confirmed by a UK HMRC/LBMA/LPPM Memorandum of Understanding affirming that in the London gold market “investors acquire an interest in the metals, although in most situations, physical delivery will not occur and in 95% of trades, trading in unallocated metals will be undertaken.” Before that, in 2011, the then LBMA CEO Stuart Murray also confirmed – interestingly, the page has been deleted, but one can find it in the archive – that “various investors hold very substantial amounts [of] unallocated gold and silver in the London vaults” – emphasis mine. Clearly, what Stuart Murray failed to explain is that unallocated gold and silver do not exist in a vault because they are not physical. As Dentons law firm reinforced what we already knew, those are simply paper claims on bullion banks for a quantity of gold and silver that the banks are obliged to find somewhere, if the claimant wanted to execute the claim. To sum up, given COMEX trading gold futures and London trading synthetic unallocated gold, both the London and COMEX gold markets essentially trade gold derivatives, or paper gold instruments, and by extension, the international gold price is being determined in these paper gold markets. (…) the reality of unallocated bullion trading is that buyers and sellers rarely intend for physical delivery to ever take place. Unallocated bullion is used as a means to have ‘synthetic’ holdings of gold and so obtain exposure to the price of gold by reference to the London gold fixing. (…) According to the LBMA bullion bankers who established the reporting of London gold clearing statistics, the then London Precious Metal Clearing Limited (LPMCL) chairman, Peter Fava, and JP Morgan’s Peter Smith, these LBMA gold clearing statistics include trading activities such as “leveraged speculative forward bets on the gold price” and “investment fund spot price exposure via unallocated positions”, activities which are merely side bets on the gold price. Nevertheless, the deficiency of the clearing statistics is explained by the fact that they do not measure individual transactions, gauging instead the metal that is transferred from one clearing account to another on a net basis. Besides that, there are other factors in play: 1) the premature termination of a forward contract, which precludes the transfer of any metal and, hence, being counted for the clearing statistics; 2) spot transactions usually being netted against exchange for physicals (EFP), which swap the original exposure to the spot London market with a futures contract, offsetting the initial OTC transaction by moving the position to the exchange; and 3) for having greater efficiency, the banks have chosen to replace the old FX-based systems, which tracked individual transactions, to this netting one. Unlike the reporting of clearing statistics, the LBMA does not publish gold trading volumes on a regular basis. Notwithstanding, it did publish a one-off gold trading survey covering Q1 2011. Here, it was revealed that during the first quarter of 2011, 10.9 bn oz of gold (340,000 tonnes) were traded in the London OTC gold market. During the same period, 1.18 bn oz of gold (36,700 tonnes) were cleared in the London OTC gold market. This would suggest a trading turnover to clearing turnover ratio in the ballpark of 10:1. In the absence of live trading data, we can take this 10:1 ratio as a proxy and continue to use it as a multiplier to the LBMA London Gold Market daily clearing statistics, which are published on a monthly basis. For example, average daily clearing volumes in the London Gold Market in October 2022, which is the last reported month, totalled 18.3 mn ounces. Converting to tonnages, there was 571.875 tonnes of gold cleared per day in London. On a 10:1 trading to clearing multiple, that is the equivalent to 5,719 tonnes of gold traded per day, or 1.48 mn tonnes of gold traded per year. Owing to storing only around 8,000 tonnes of gold, most of which represents static holdings of central banks – 5,000 tonnes in the Bank of England (BoE) –, ETFs and other holders, the London OTC gold trading activities are totally disconnected from the underlying physical gold holdings. To get a sense of the absurdity, this suggests that approximately 71.5% of the gold kept in the London vaults was being traded. Comparing it to the S&P 500 equities, one of the most traded asset categories in the world, in December 2022, up to the 16th, the average daily volume was $6,714.72 mn. Using the total market capitalization figure at the end of September of $46,460,463.2 mn, this implies that only about 0.01% of the shares of the largest American corporations trade daily, on average.  To cement the ridiculousness, just 205,238 tonnes of gold are estimated to having ever been mined throughout history. In terms of yearly numbers, in the last ten years, gold supply increased on average 4,632 tonnes, 3,409 of which being freshly mined. On the flip side, the average for the gold demand has been 4,314 tonnes.

Remarkably, this would indicate, if it was real, that 2.8% or thereabouts of all the gold in the globe is transacted in London, every day. Keeping in mind that almost half (46%) of the gold is held in the form of jewellery, it appears that 5.16% of the non-jewellery gold trades daily, while a huge 12.58% of all the gold bars and coins in the world seem to “change hands” every day, just in London. Thus, the trading of nearly 5,719 tonnes of gold per day within the London gold market has nothing to do with the physical gold market. Calculating for the whole 2021, total trading volume in the London gold market is estimated to have been in the neighbourhood of 1.38 mn tonnes of gold, while the trading volume of the 100 oz COMEX gold futures reached 41.9 mn contracts, equivalent to 188,325 tonnes. For those paying attention, these figures are insane. Ipso facto, on a daily average, gold trading in New York and London are, respectively, more or less 44 and 319 times the annual amount demanded by jewellers, bullion investors and other manufacturers that need or desire the real thing. Similarly, this trading represents roughly 41 and 297 times the annual gold supply, in New York and London venues respectively. Consequently, gold trading volume on the London OTC gold market, in 2021, was about 7.3 times the turnover in the COMEX 100 oz gold futures market. Finally, in August of last year, the combined gold stock, including paper claims, of all the COMEX depositories added up to 37,486,859 ounces, or 1,171.5 tonnes. For those keeping score, with approximately 8,000 tonnes of gold in London (or under it), the Loco London to COMEX ratio comes to 6.83, being close to the trading volume one. Therefore, we can safely assume their fractional reserve trading is identical in magnitude in these two trading channels. Moving on, now that the basic concepts have been laid out, it is time to present the heart of the matter. As an inheritance of the all-powerful British Empire, the London Gold Lending Market, which is a global marketplace, revolves around the BoE. Here, central banks and commercial bullion banks interact in the execution of obscure gold lending and gold swap transactions that increase the available supply of gold. Unsurprisingly, the bullion banks dubbed this scheme of smuggling a few pieces of gold to show their customers and the suits as liquidity provision. Evidently, few if any transactional details about the gold lending market are ever made public. Likewise gold lending and gold swaps are not reported distinctly from central bank gold holdings. In this mad, clown world we live in, gold held and gold lent/swapped is merely reported as one line item of ‘Gold and Gold Receivables’ on central banks’ balance sheets. Therefore, the real state of central bank gold holdings is concealed for any central bank engaged in gold lending or gold swaps. Notwithstanding, gold lending and swaps provide borrowed physical gold for bullion banks to engage in leveraged fractional reserve bullion banking and trading to boot, mostly in London and New York, where the international spot gold price is predominantly determined. On that account, gold lending and swaps, the leveraged and fractional reserve nature of gold trading, and the lack of transparency and accountability, all align to have a potentially depressing effect on the gold price. Or do they? For having still a lot to say and already surpassing the three thousand word count, I am taking a breather and come back to it a couple of days from now.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed