|

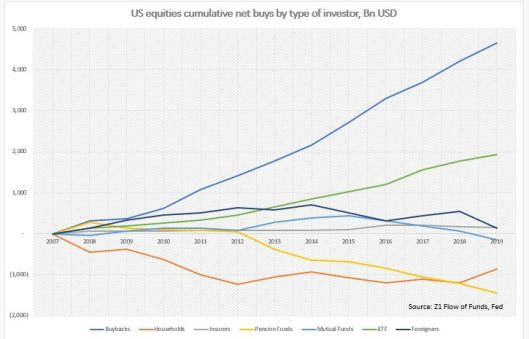

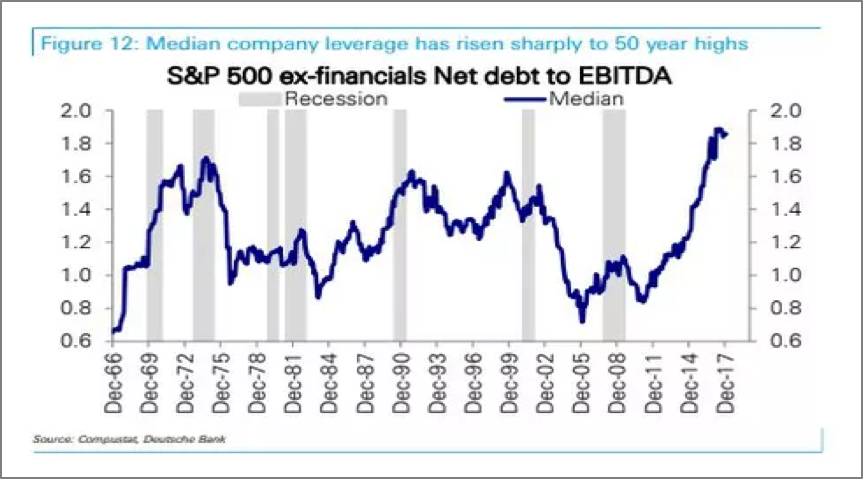

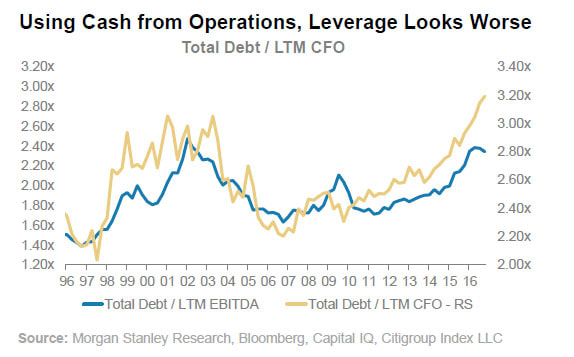

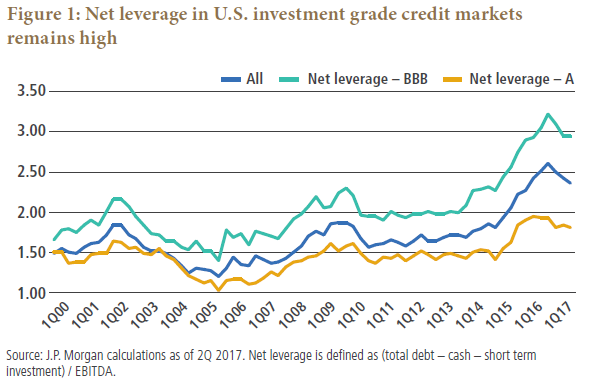

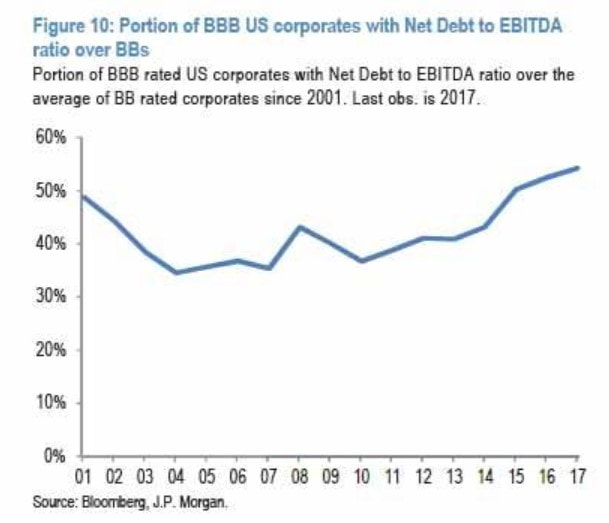

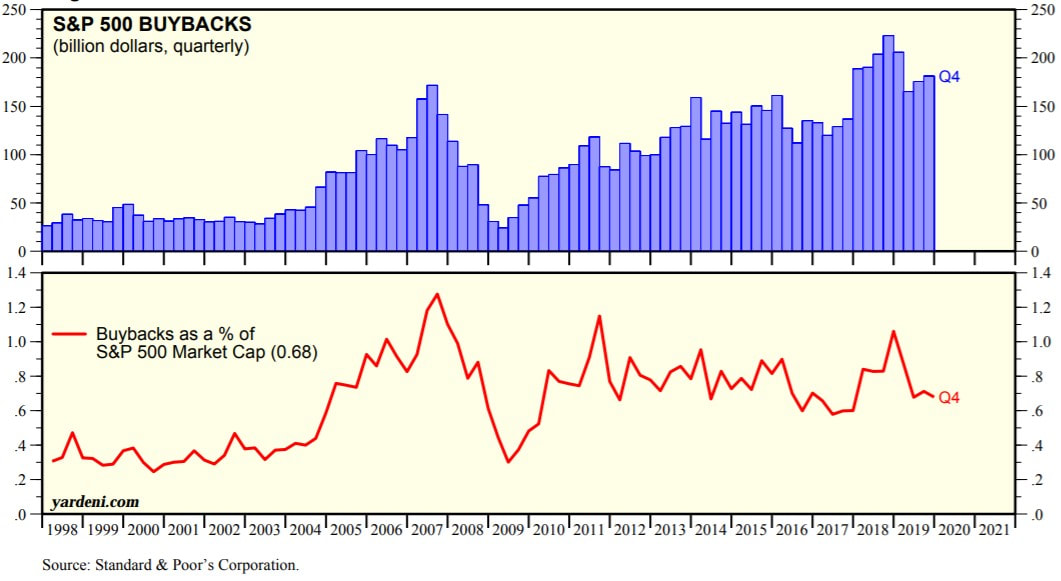

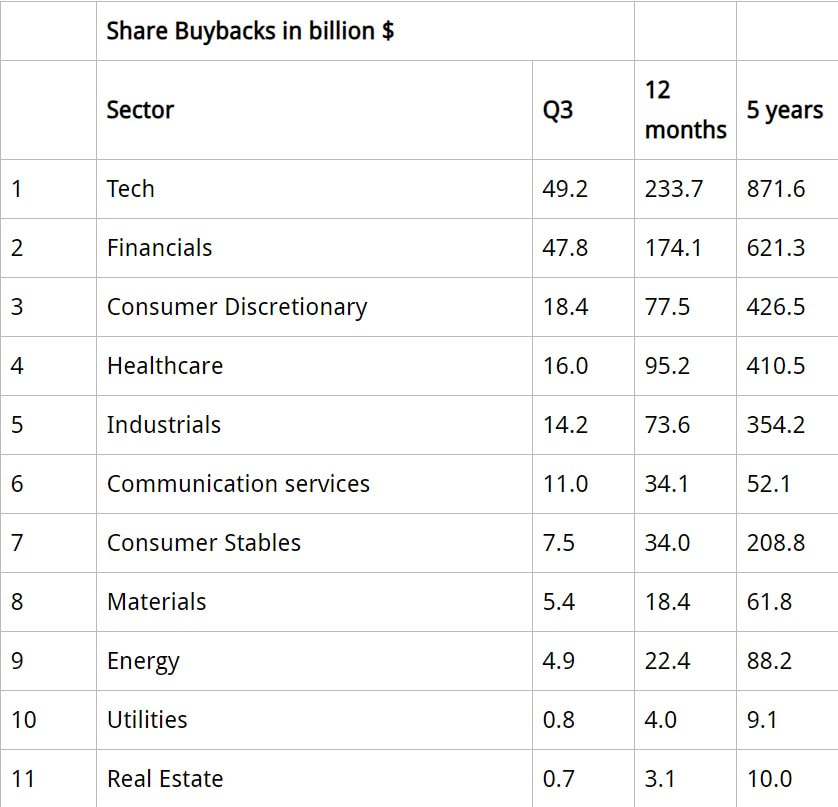

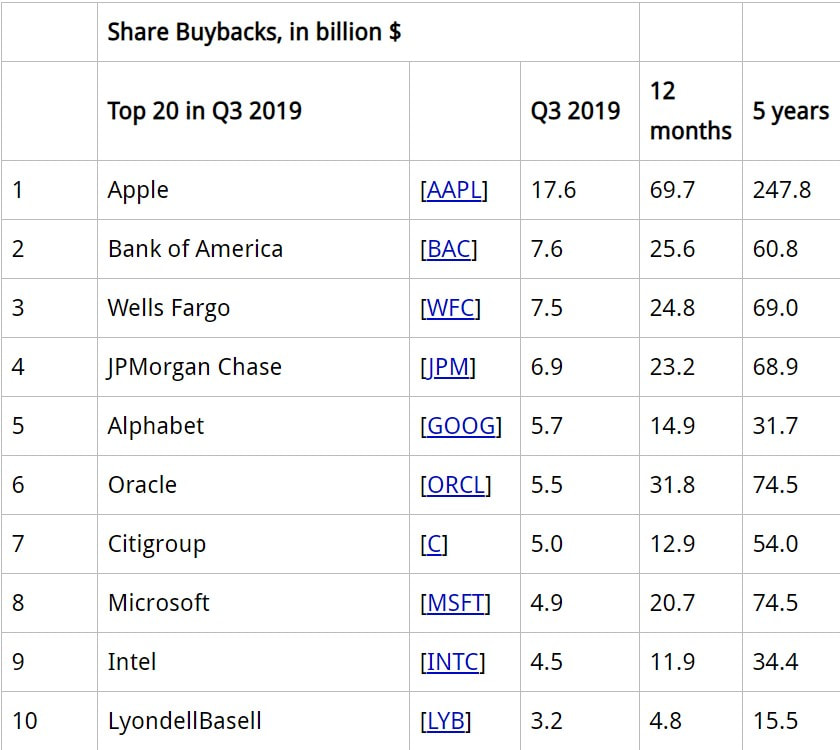

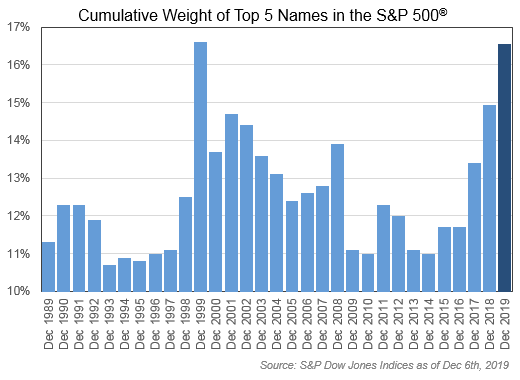

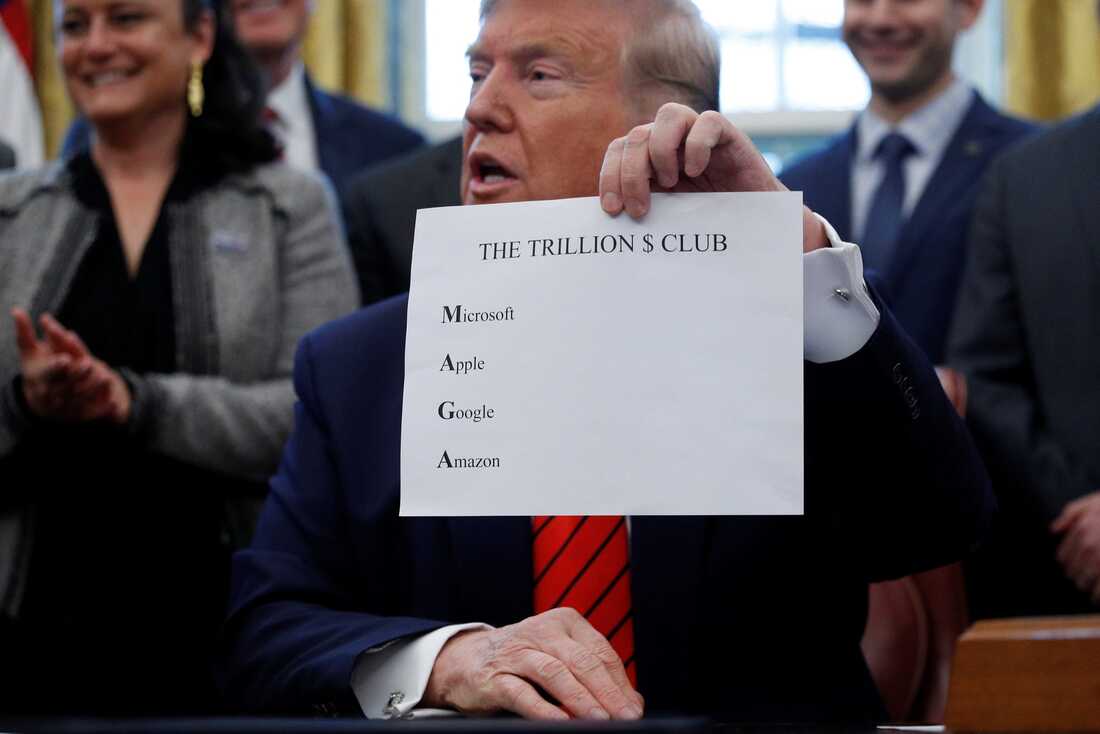

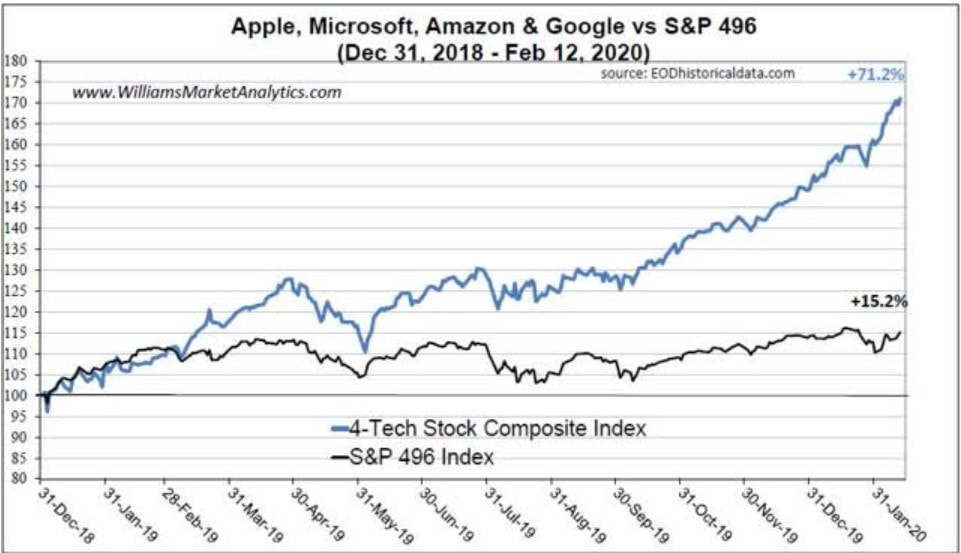

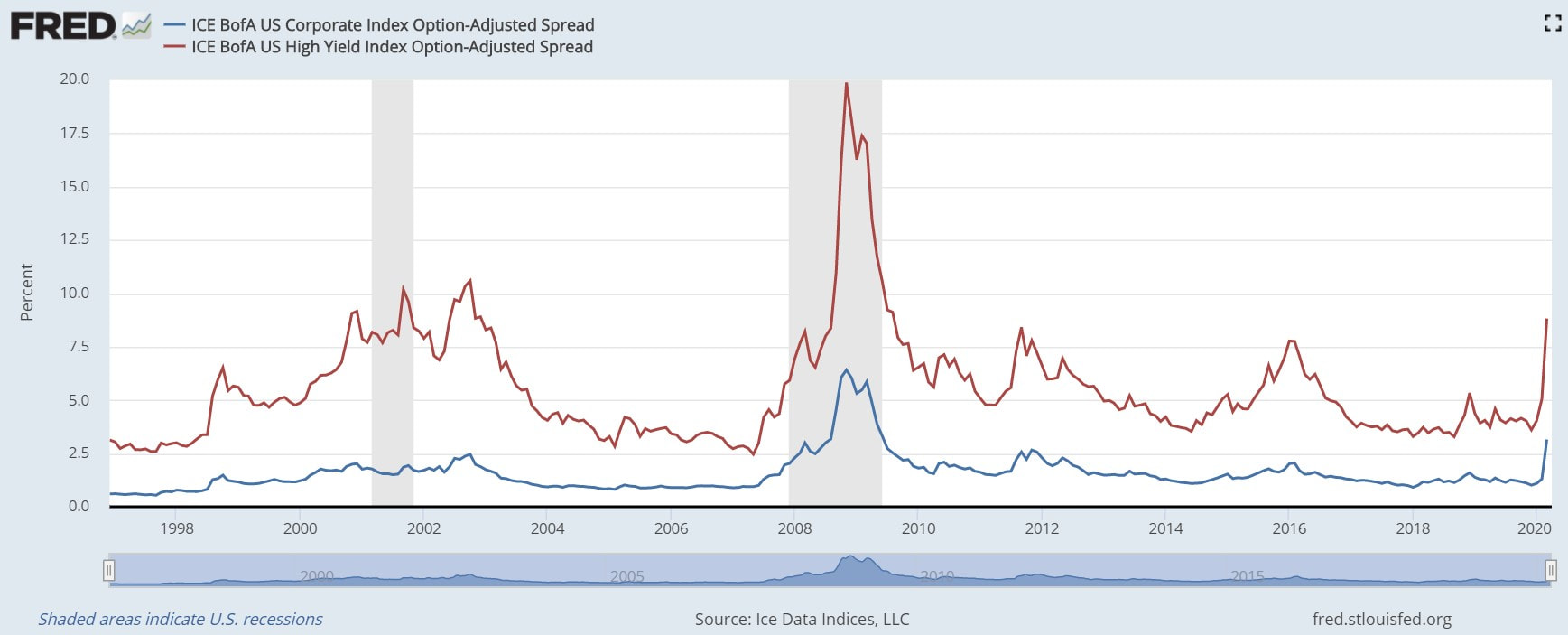

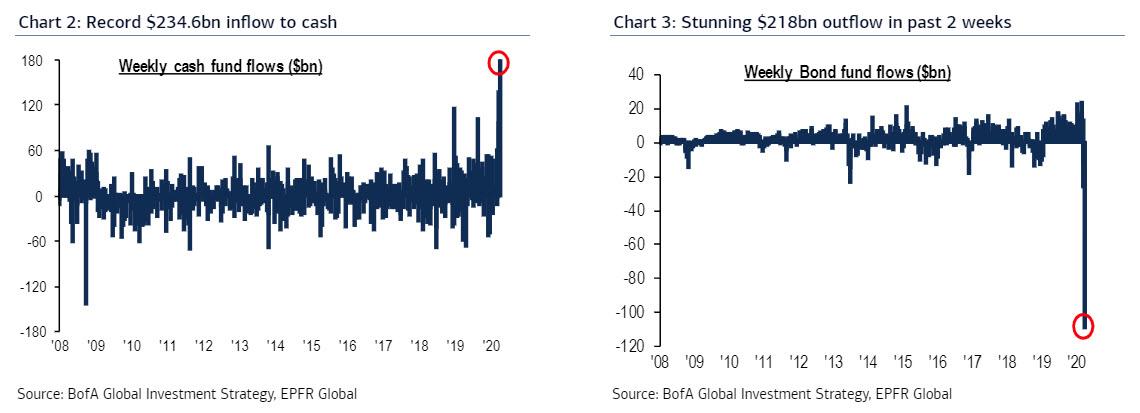

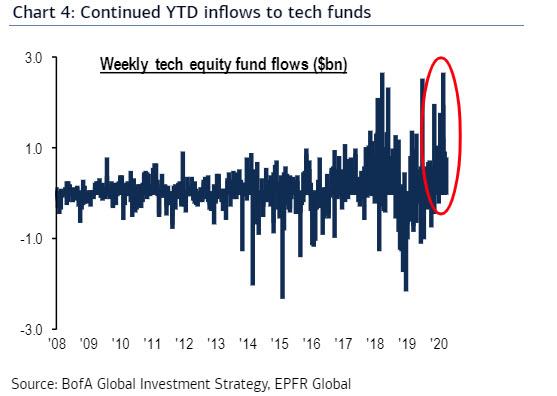

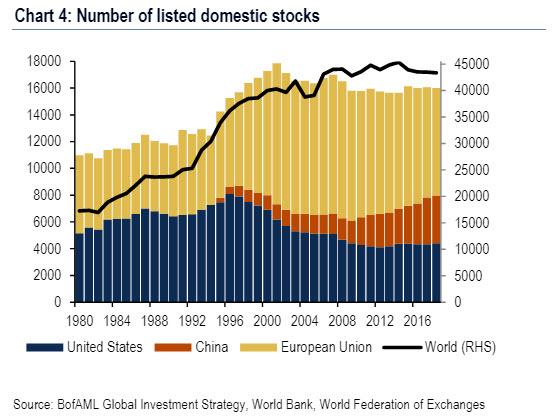

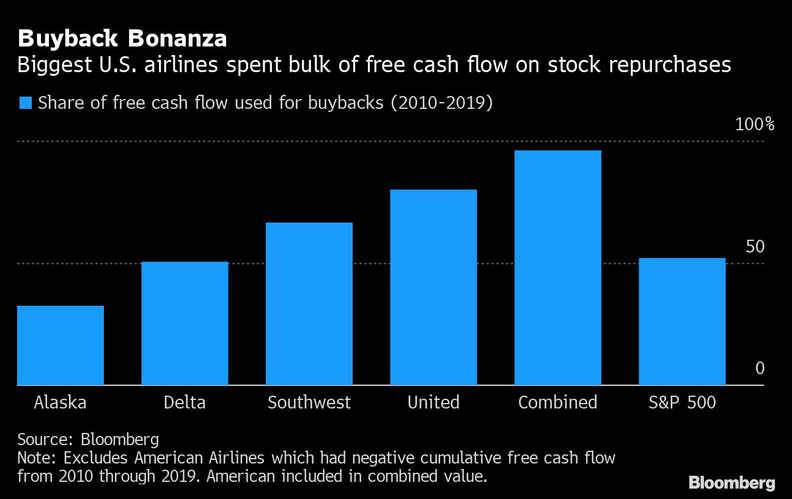

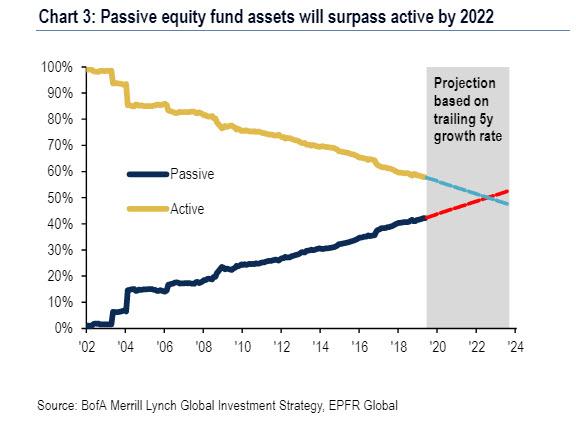

The biggest buyers of US equities since the GFC were corporations. With the buybacks coming to a halt due to the meltdown of the corporate bond market, and the financial system in general, corporations can no longer get the cheap and easy financing to buy their own shares. Therefore, the stock market will only surge again if some other market participants step up. If you have been following this blog recently, then you already know which one will be. As I just stated, buybacks were by far the biggest contributors for the longest bull market in the history of the US, followed by the passive investment in ETFs. Additionally, foreigners and insurance companies were buyers too, though insignificantly. On the opposite side, mutual funds, pension funds and households were all sellers.  The corporations took advantage of the ZIRP and the liquidity provided by the Fed to lever up to record levels. Furthermore, because investors were in search for yield in a low interest rate environment, they were forced to pursue greater risk in their portfolios. As a result, the demand for corporate bonds increased and the corporations were happy to supply them.  In addition, it was not just a few bad apples that got themselves into so much debt and, consequently, made corporations as an aggregate look reckless. By looking at the chart below, it is clear this strategy was pervasive. The net debt (debt minus cash and cash equivalents) to EBITDA (earnings before interest, taxes, depreciation and amortisation) reached levels never seen before.  Likewise, the debt to cash flows of the last twelve months from operations also arrived at historical magnitudes. This means the ability to pay their liabilities became relatively very diminished.  Moreover, 50% of the investment-grade bond market sitted (until a month ago) on the lowest rung of the investment-grade ladder. In a recession, BBB-rated bonds are the most vulnerable of all investment-grade bonds. According to Moody’s, 10% of BBB-rated corporate bonds are downgraded to “junk” status in a recession. Since the number of BBB-rated bonds has exploded, we will see more such cases than ever before in this one. Taking a look at the graphs below, you can see BBB-rated corporations have been especially reckless, with more of them setting themselves up to being downgraded to junk.   Furthermore, one of the reasons companies accrued so much debt was to repurchase their own shares. Despite the absolute amount having piled on year after year, the buybacks in relation to the market capitalisation actually stayed below the levels of the housing bubble.  In terms of sectors, tech companies bought back $49.2 billion shares in Q3 2019, while the financial institutions repurchased $47.8 billion, for an aggregate amount of $97 billion, which means those two sectors made up for 55% of all share buybacks.  The four beloved banks – Bank of America, Wells Fargo, JP Morgan Chase, and Citibank, in that order – among the top seven share-buyback queens below, between them bought back $86 billion of their own shares from the start of Q4 2018 to Q3 2019, and thereby reduced their equity capital by $86 billion, which is what share buybacks do - when a company buys back its own shares, it pays cash for those shares, the shares get canceled and disappear, and the cash is gone, and the company's equity on the balance sheet drops by that amount. Yet, those $86 billion could have come in handy right now so as to deal with their losses on their loans to commercial real estate projects, to businesses, and to consumers. Instead, those $86 billion have gone to waste.   In addition, of the five most valuable US corporations - up to mid-February -, four make the list above: Apple, Google (Alphabet), Microsoft and Facebook, only Amazon was left out. These companies are the spurs that made this bull ferocious, being the only ones that significantly surged in the last decade. Thus, their weight in the S&P 500 index gradually rose. Even though the graph below shows that the their cumulative weight did not pass by the end of last year the 1999 level, by February 11 of this year, which was pretty much the market high, the top five made up 18% of the S&P 500, breaking the record.  Likewise, the MAGA stocks (Microsoft, Apple, Google and Amazon) were given this nickname this year when all of them achieved the trillion dollar valuation, prompting President Trump to exalt.  Anyway, these corporations carried the whole S&P 500 on their backs. On an equal-weighted index comprised of the MAGA, from the start of 2019 till February 12 of this year, they shot up 71.2%. Still, the index composed of the other S&P 500 companies, the S&P 496, throughout the same interval, only rose 15.2%.  Additionally, like I said above, the low rate environment enabled corporations to lever up. In spite of the mounting risk associated with lending to such indebted entities, seeing that the appetite for yield could not be satisfied with low-risk assets, investors had to satiate themselves with risky assets such as corporate bonds. Consequently, the demand hardly decreased when the leverage intensified, keeping yields at quite modest levels. However, the party has come to an end. The spreads are widening and the easy financing is no more.  Since the start of the bear market, there has been record inflows to cash and cash equivalents, on one side, and, on the other, unimaginable record outflows from bonds - data until March 25. Because investors are fleeing the corporate bond market, their prices are plunging, resulting in the expanding spreads between theirs and the Treasuries' yields.  However, the MAGA posse continues to attract investors, which may be making their weight in the S&P 500 to swell.  Moreover, the cheap and easy currency creation provided by the Fed leads CEOs and CFOs to invest in themselves. The rationale is that the interest rates are cyclical. Hence, when these start to climb, the companies finance themselves more so through share issuance. Critics of the buybacks complain that companies should be taking advantage of the low interest rates to invest in productive capacity and R&D, as well as pay bigger wages to their workers. Well, they already do these things. Although it would be nice if they did even more, the reality is that there is a limit for such actions. That limit is the demand. Consumers are extremely indebted and, as a result, they cannot indulge themselves in impulsive shopping sprees. By looking below, consumers are still recovering from the GFC.  Financial engineering is what share buybacks are all about. They lower the shares outstanding, and so earnings are divided by a smaller number of shares, which produces a larger earnings per share figure, when in fact the actual profit of the company has not changed.  The question of how stocks can keep rising in the face of these massive outflows from stocks emerges, although as BofA's CIO Michael Hartnett writes, the puzzle of record equity prices and sustained equity outflows is solved by i) US corporate Great Rotation... from 2013 to 2018, US corporate debt issuance = $10.5tn, stock buybacks = $4.2tn; and number of listed US stocks down from 8090 to 4397 past two decades, up to 2018, in sharp contrast to Europe, China & rest of the world. As I have been discussing in this blog, it is certain that a complete meltdown of the financial system is cropping up. Likewise, the economy is set to enter in a depression. Many businesses are starting to close their doors and millions of Americans will lose their jobs. According to a projection by the St. Louis Fed, the unemployment rate may reach 32%. Thus, a colossal series pf defaults is ensuing, halting the debt-based financial system. Therefore, the Fed is going to have to crank up its interventions in the markets to save the whole system. This includes the infamous helicopter money. The $1,200 is just the beginning. The Fed and the Treasury will take this policy to an absurd extent, letting the inflation Titan break free from Tartarus. Americans are going to need a demi-god like Paul Volcker to imprison it once again. Unfortunately, neither Powell nor any keynesian technocrat could play the part. Furthermore, corporations could have used the easy money policy to build up some savings in cash for a rainy day. Because most of them wasted that opportunity, the US government and the Fed will most likely bail them out. Take the airlines for instance, from 2010 to 2019, they spent 96% of their combined free cash flow on buybacks. Now that the proverbial has hit the fan, they are going bankrupt.  Additionally, once the dollar starts falling due to massive currency printing, the government is going to have to increase the checks to citizens for goods, especially the basic ones, since these are getting more expensive (and it will accelerate as time goes by). This makes the Treasury to issue more debt. Seeing that there would be no more buyers of Treasuries (at such low yields), the Fed is going to monetise them all, creating further debasement of the greenback. Consequently, the government increases its check amounts to the citizens and... America gets trapped in a vicious cycle of inflation. Inasmuch as this will impoverish individuals, taking them to third-world wealth, they will not be in financial conditions to gamble in the stock market. More importantly, people are definitely not going to be buying US equities in the near future because their earnings are going to stay at very low levels. Hence, households, mutual funds and other financial institutions will not be acquiring US stock. Moving to ETFs, in spite of the transformation of the financial services industry from a human to a robot-led one rendering the trend depicted on the graph below, I take the view this trend will reverse. Investors are going to be looking for experts that can find the best opportunities in the new paradigm. Obviously, I do not know which particular companies, markets and instruments will perform the best. Yet, it is indisputable the US, in general, is going to become extremely toxic for investors. Therefore, ETFs and other investment funds as well are not going to be the ones pushing US equities into a new bull market. By the way, the same goes to foreign investors.  In conclusion, with corporations being unable to get cheap funding due to the financial system being in shambles, the only way the Fed could try to get the stock market to rally, so as to get the wealth effect desired by the keynesians, is to purchase the shares itself. Therefore, the Fed will start acquiring the means of production. Like I discussed in The Road to Serfdom is reaching its destination, America will turn increasingly more in a marxist socialist nation.

Despite the country becoming the United Socialist States of America, USSA, because of all the Fed-induced inflation the prices of the US shares may achieve levels that go far beyond anybody's wildest fantasies, as I compared it to the Caracas stock market in a previous post. Thus, the silver lining is the next bull market will make this last one look like a newborn calf - in nominal terms, of course.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed