|

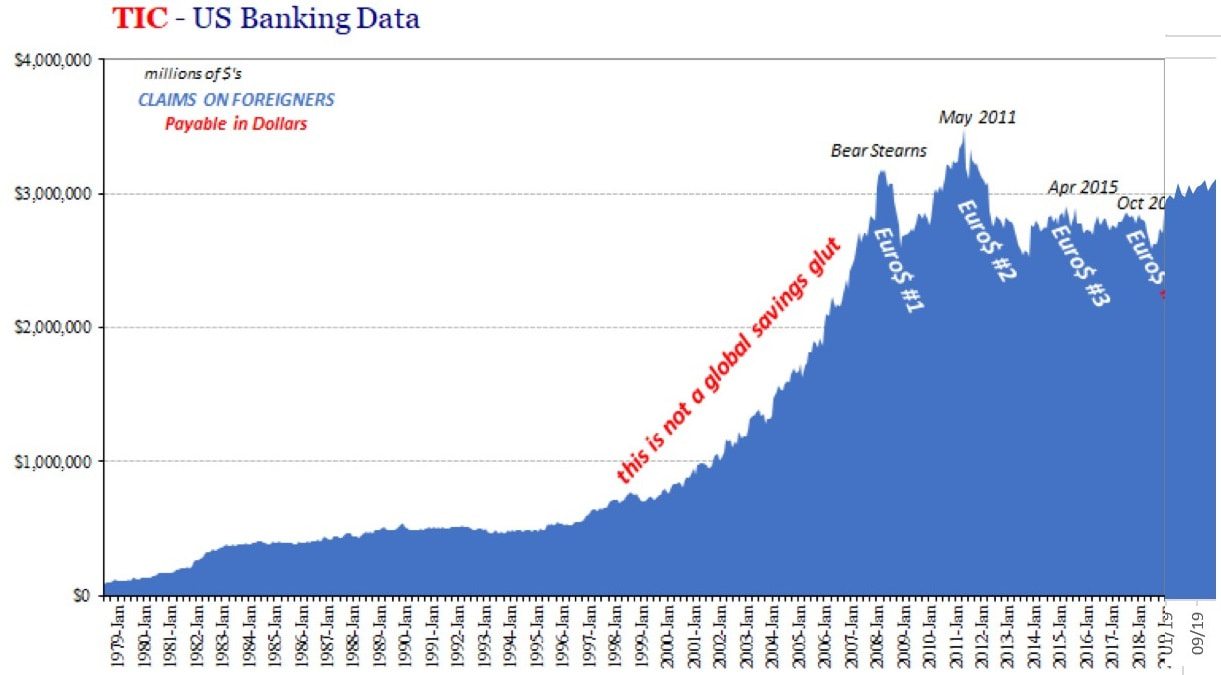

In view of the fact that some issues were not scrutinised and discussed as thoroughly as I felt appropriate, so as to clear any doubts that might have come up, I decided to add this bonus part. Specifically, I am going to delve into the central bankers' trickery. By the end, you are going to know their true powers, or lack of them, and the maneuvers perpetrated as attempts to manipulate the impetus of the financial markets. Accordingly, we are going to know, at last, in the head-to-head between central bankers and market participants who comes out triumphant. Spoil alert: the market participants. Finally, as you may know if you are familiar with the Austrian school, this debt-based economic system is doomed for failure. Therefore, the endgame of this system is going to be discussed to some extent. To recap, the Eurodollar system grew ceaselessly from the 1950's up to 2008. Thereafter, despite all the unconventional policies pursued by the central banks around the globe, the system had hit a roadblock and never managed to recoup its momentum. The goal of the central bankers' policies, to tackle the economic slump of the Great Recession, was to lift inflation expectations and to reflate asset prices in order to prevent debt deflation from happening, continuing to foment the professed "wealth effect". Firstly, as I explained before, inflation is not necessarily an outcome of an economic expansion nor does it make, in turn, the economy to boom. This is what transpires in an economy based on a sound monetary system. However, the current system is without surprise utterly flimsy, for being built on debt. As a result, the only way for the economy to develop is through debt expansion, which causes the currency supply to swell. That takes us to the asset reflation. Secondly, the keynesian technocrats at the central banks, during the GFC, wanted to keep assets overpriced as they were. Inasmuch as households, businesses and financial institutions were immensely leveraged, once financial constraints started cropping up, a deflationary spiral kicked in. In detail, those economic agents could not get liquidity from cash lenders, except if they had good quality collateral or an already existing line of credit. Hence, so as to get the liquidity to pay their obligations that were coming due, they had to sell some assets. Consequently, the prices of the assets fell even more, resulting in ever greater asset sell-offs. Even though the measures taken by the central banks had been unprecedented in its amount and scope, the deflationary vortex was still brutal. Thus, the Fed and company failed at maintaining asset prices elevated, impeding the pricking of the debt-fueled bubble. Yet, with their rhetoric combined with market participants' naïveté, the monethary technocrats were in fact able to persuade everybody that they managed to rescue the financial system from absolute collapse. Actually, like I have claimed on part two, regardless of the assertions made by the keynesians and the financial media, neither the Fed nor any other central bank has the power to steer the financial markets. As a matter of fact, the Eurodollar system is the force propelling the financial markets.

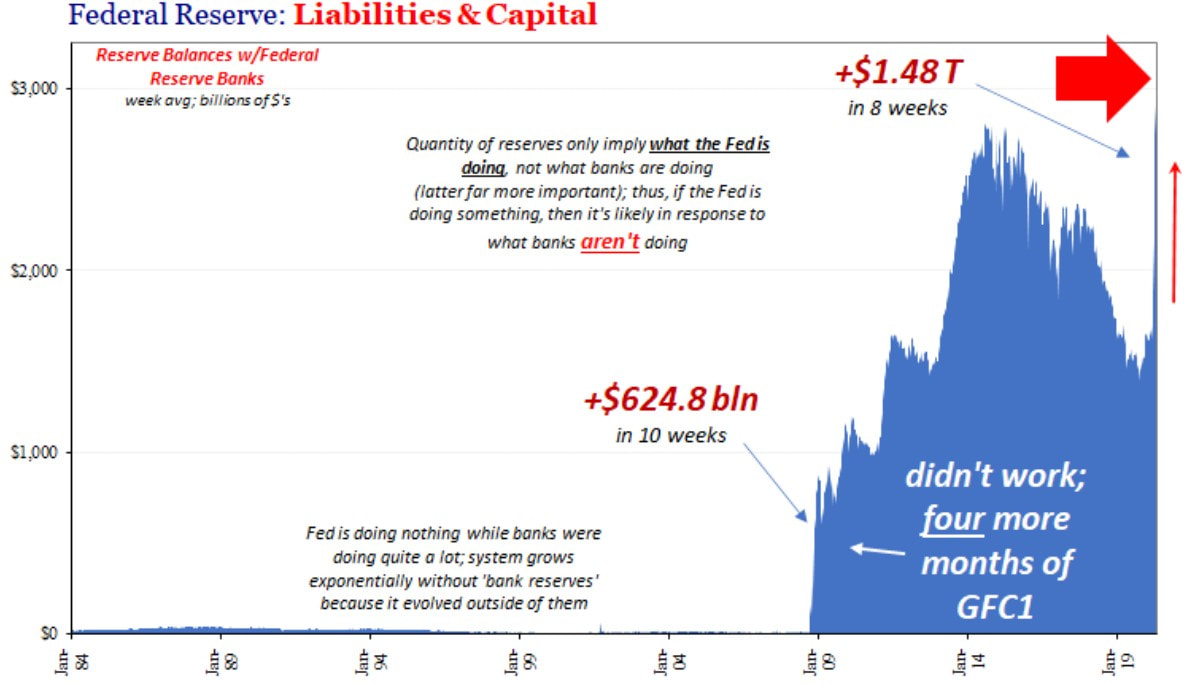

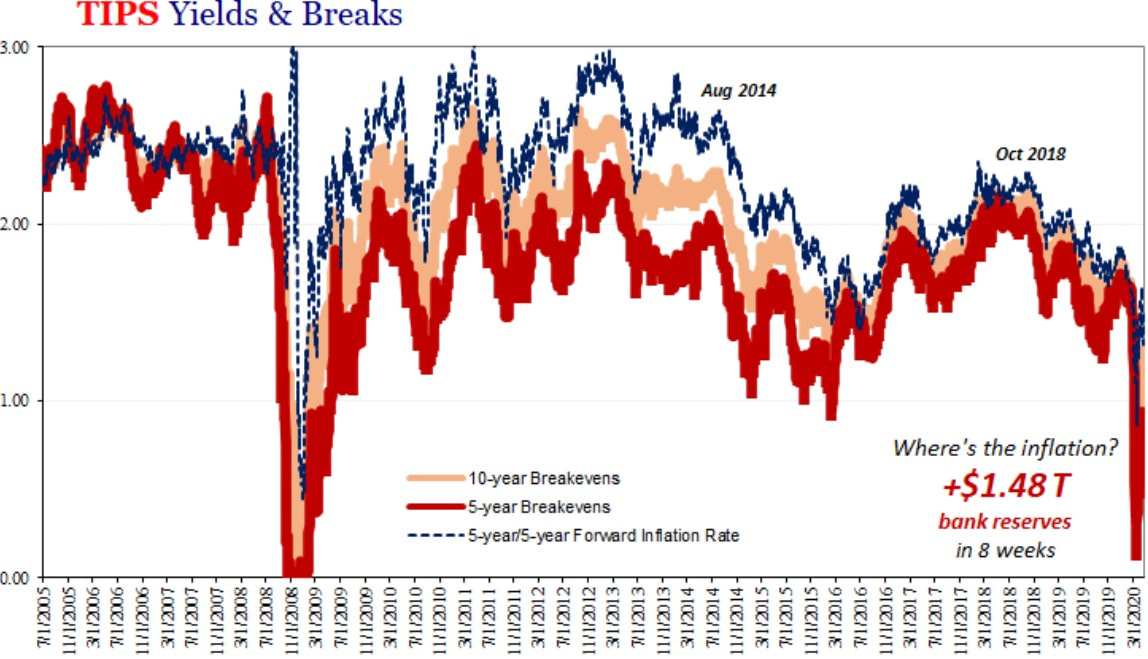

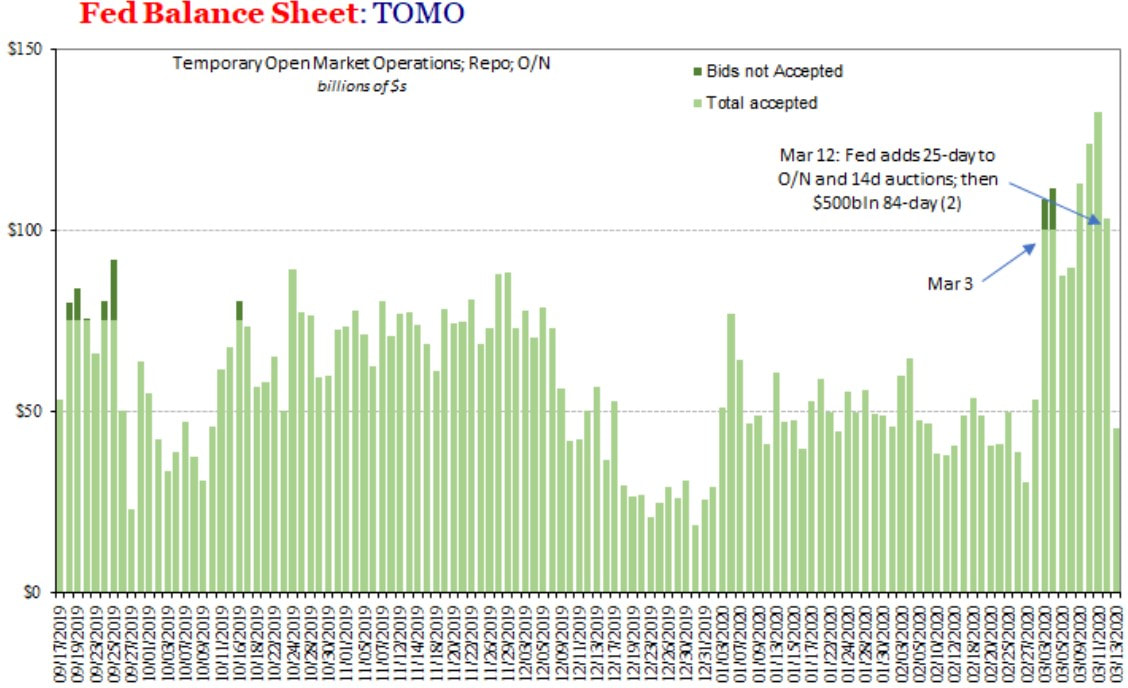

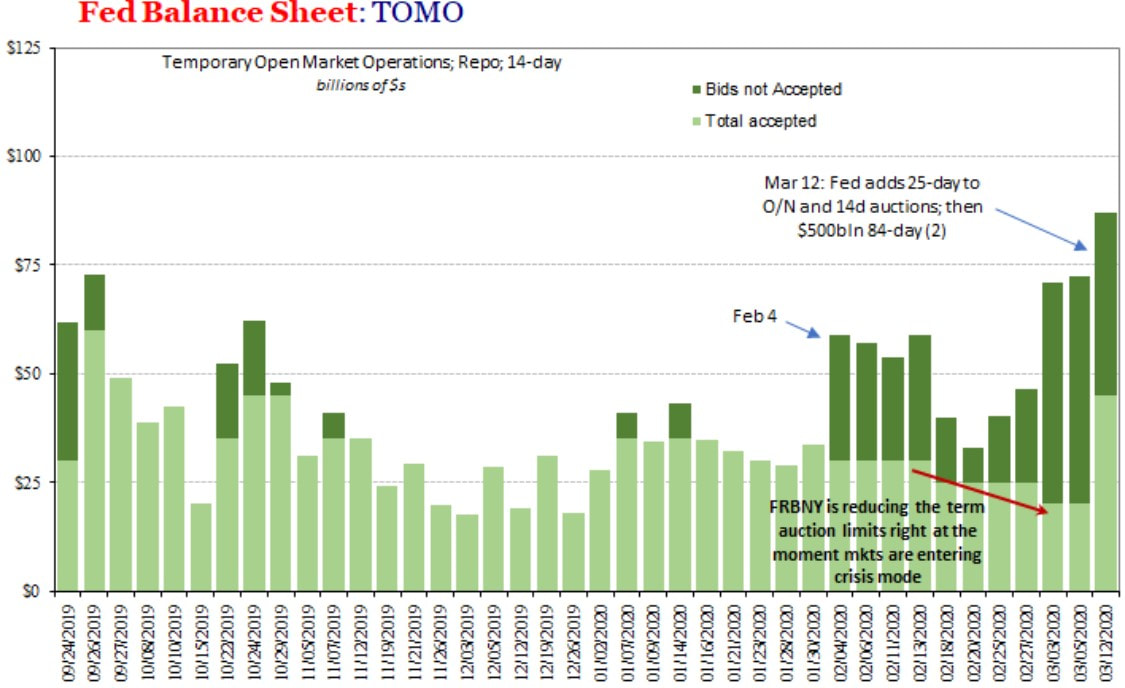

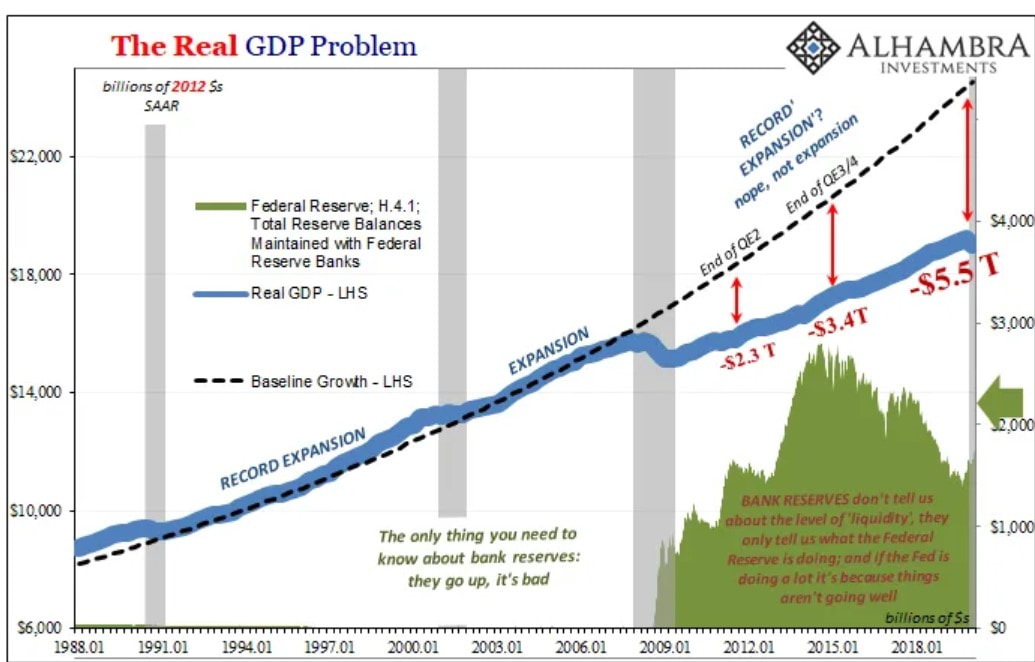

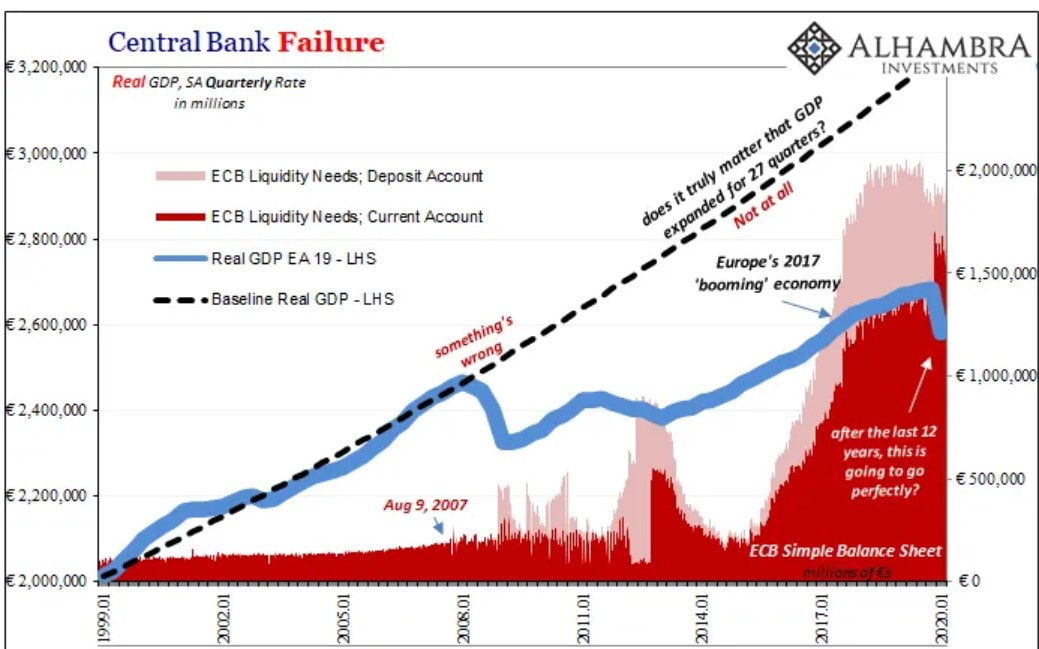

Furthermore, that is what the three graphs above and below demonstrate. In spite of all the efforts to reflate the economic growth of the yesteryear, the Fed has led everyone who believed in it down. No matter how much base currency it has created out of thin air, the financial activity has hit a ceiling, indicating that the financial system has reached its saturation point. Additionally, they have failed to produce sustained periods of inflation expectations. These reflation episodes always turned out to be flops, ending up in deflationary scares including this one, which commenced in 2018 as you know.  Throughout this financial debacle, the Fed has once more engaged in futile experiments to swindle the market participants, the first one being the repos of the Temporary Open Market Operations. This programme was devised to imitate the repo market for Treasuries. Although it may seem, for the credulous ones, this action was fundamental to keep the system running without a hitch on account of being overbidded on various days, in reality this did nothing to provide the liquidity to those in need.

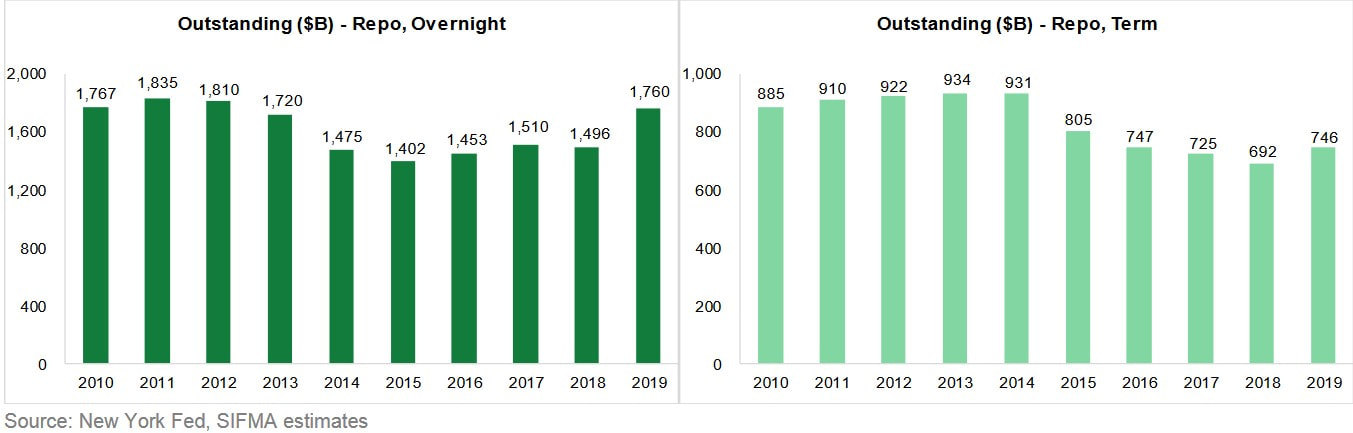

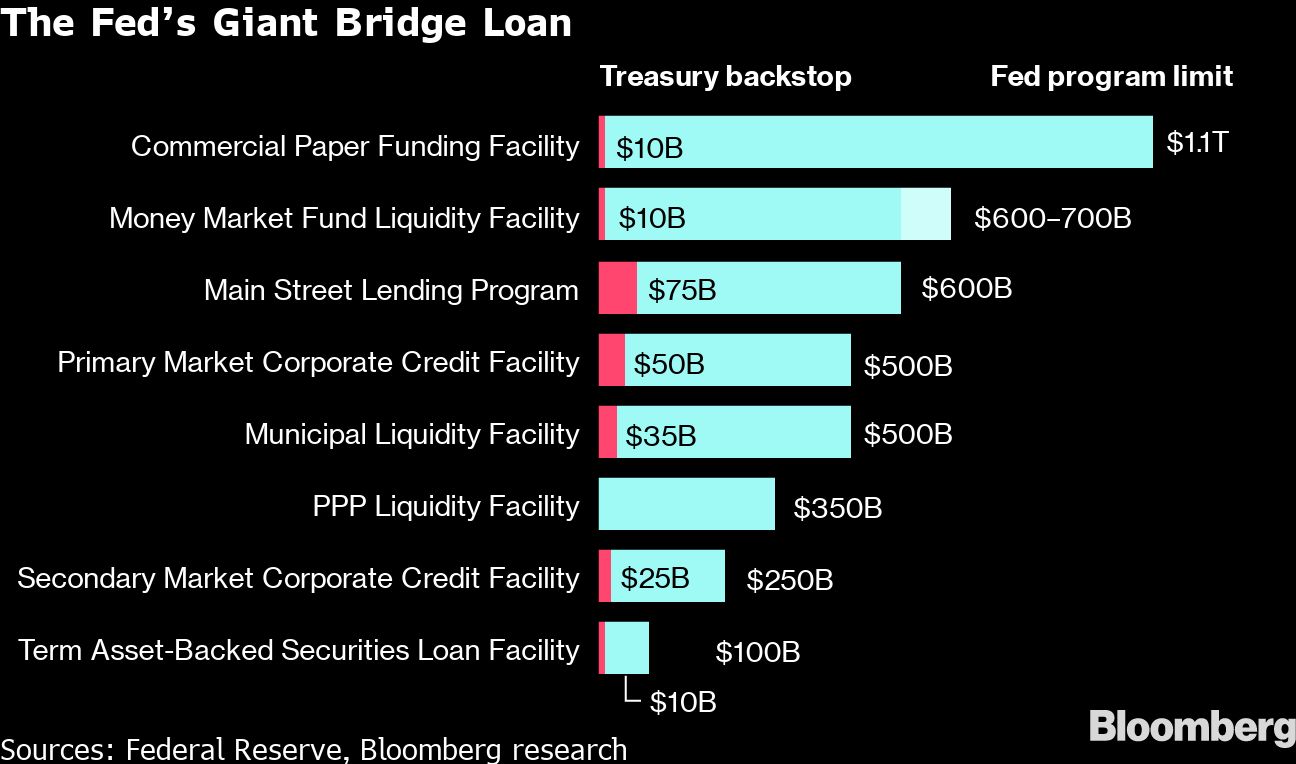

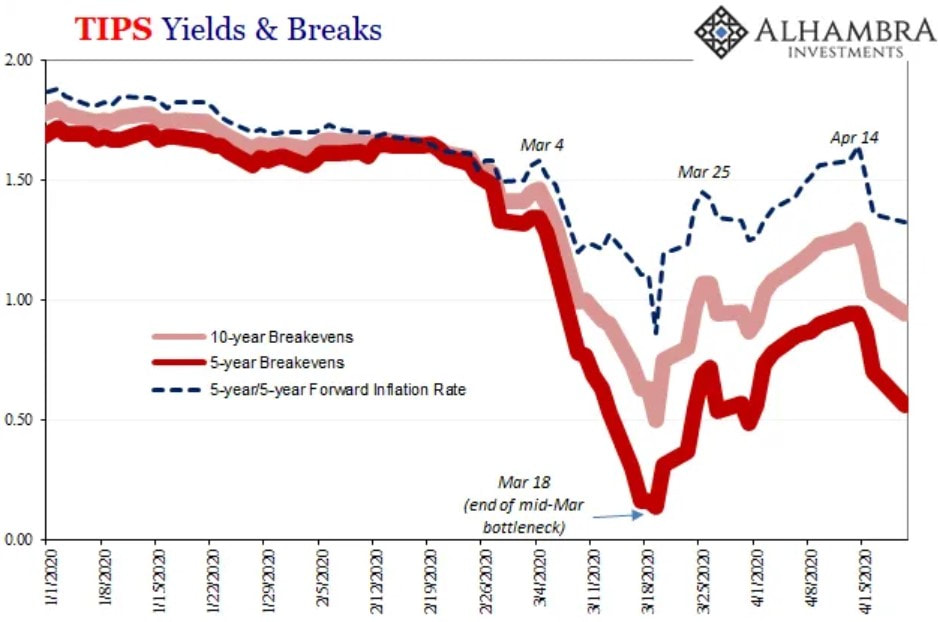

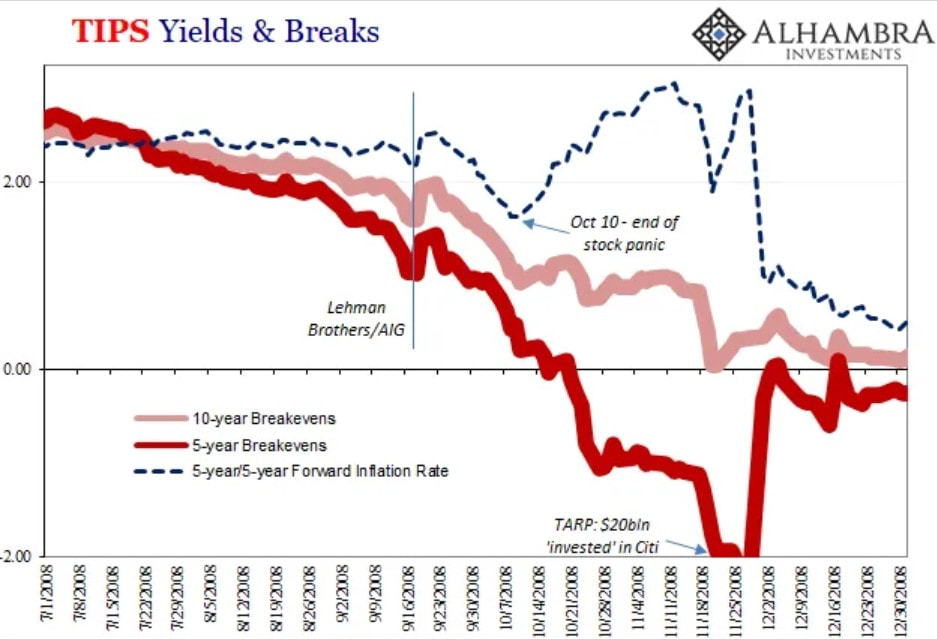

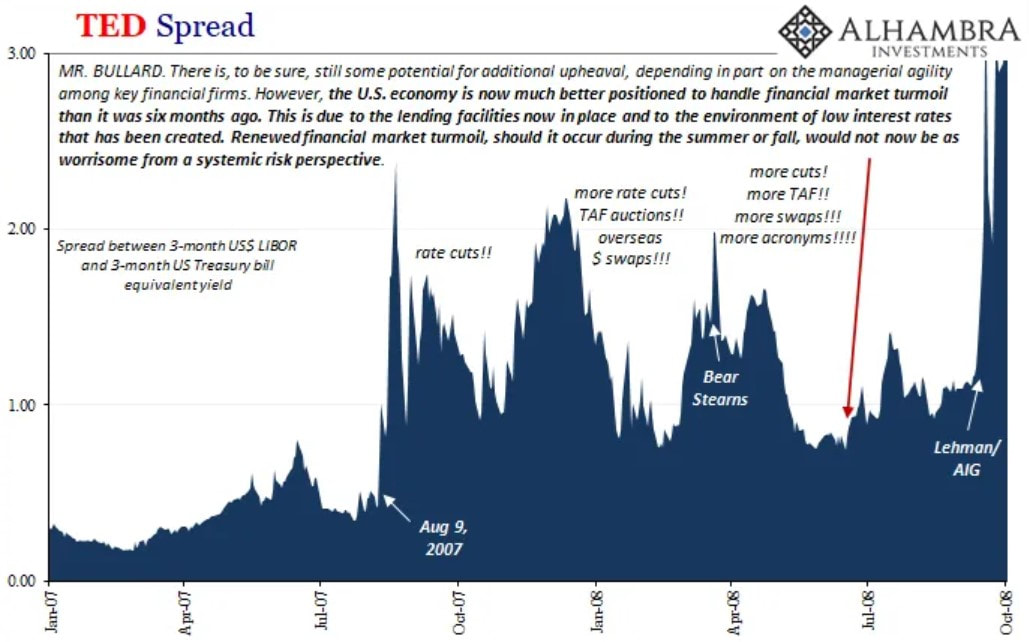

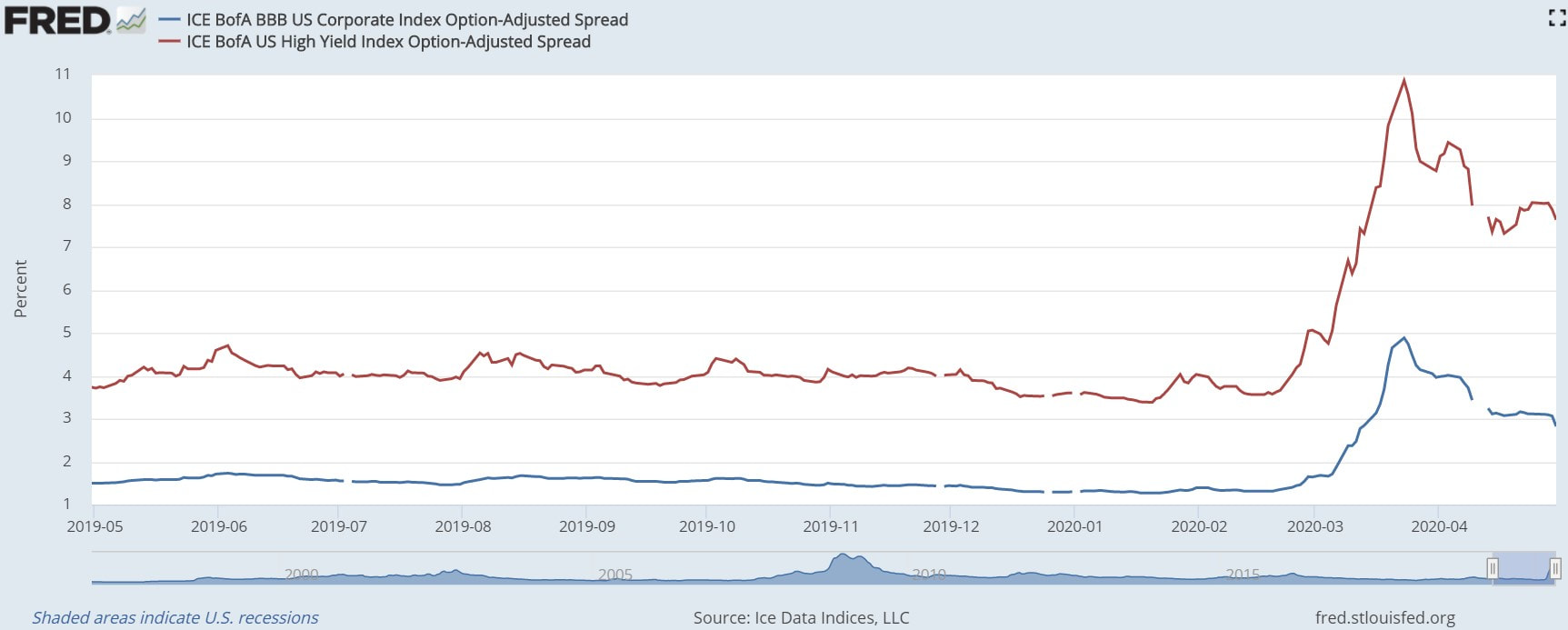

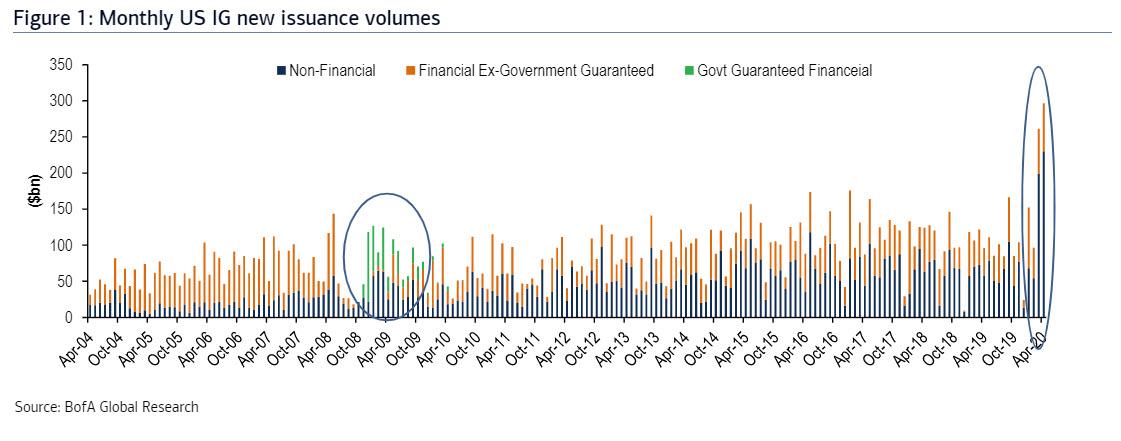

To begin with, these "repo" operations represent a small fraction of the repo market. On the days with highest demand, March 11 and 12 for the overnight and 14-day respectively, the "rush" for the overnight scheme made up around 7.4% of the $1,760 billion overnight repo's 2019 daily average, while for the other scheme it amounted to 12% of the term repo market. Moreover, if you recall part three's graph portraying repo fails, the rate of these fails spiked to very ominous heights during the March meltdown. This programme was absolutely irrelevant because the fundamental problem was, and still is, not being addressed by the Fed. Evidently, the culprit for the system's malaise is the collateral.  Despite the bundle of facilities (like those on the image below) designed to stem the markets crash, these do not relieve the financial constraints. The capacity of each facility is far to small to backstop these markets. In addition, the Fed does not have the competence nor the permission to provide the liquidity to where is needed in an effective and efficient fashion. Through these facilities, the Fed either acquires them or gives out loans to the primary dealers to acquire the stressed assets. Being a bureaucracy, the Fed has certain guidelines that only allow it to purchase the assets or lend to the institutions determined days or weeks before, not to mention the amount of the transactions. This means that the liquidity made available by Jay Powell and his posse are not channeled exclusively to those participants going through a drought. In fact, some, if not most, of the funds could be getting deviated to better-shaped participants, who happened to be well-positioned. More importantly, these facilities do not solve the collateral problem. As long as the securities used as collateral have their underlying assets performing poorly, cash lenders in the repo market will deem them as eligible.  Moving on to false signals, the TIPS (Treasury Inflation-Protected Security), which are a type of Treasury securities indexed to inflation in order to, supposedly, protect investors from a decline in the purchasing power of the dollar, have been behaving unusually. During the March meltdown, the 5- and 10-year maturities decoupled from each other, even though both their yields plunged. Then, they began surging, but still decoupled. Consequently, the implied inflation rate expectation mounted up, nearing the level from a month or so ago. This led some to declare the financial woe was over and that the "V-shaped" recovery was in fact going to occur, extolling the interventions undertaken by the Fed. What truly ensued was the TIPS market became less liquid. In short, during the collateral bottleneck, market participants would rather hold the 5-year tenor than the 10-year for having a longer maturity, just like it happened to the "normal" Treasuries.  Back in 2008, the same circumstance unfolded. The TIPS market became practically bid-less, meaning that there were very few market participants willing to buy. Thus, the implied inflation rate shot up, resulting in the Fed's cheerleaders to claim the financial turmoil was for all intents and purposes resolved, just water under the bridge. Unsurprisingly, nothing was resolved and we are up to this day dealing with the same problems.  Ironically, the premature praise of the almighty technocrats had already come forth in the spring of 2008, after the Bear Stearns issue had been resolved. Hardly were the Fed, the media and the gullible idiots done cheering and patting themselves in the back for rescuing the financial system, when the gruesome second leg of the crisis erupted.  In addition, more than one month after the Fed announced its backstop for investment-grade bonds and ETFs (followed shortly after by an expansion into fallen angel junk bonds), interestingly the Fed so far has not yet purchased a single corporate bond, whether investment-grade or fallen angel. In other words, with the simple promise to act, the Fed's assurance managed to get the markets, especially the stock market, to jack up trillions of dollars in value. Or so they want us to believe. As I have expounded, the Fed has an insignificant influence in the markets. Obviously, that applies to the corporate bond market as well. Like the following chart depicts, bond prices began to fall, which led their yields to rise, in tandem with the rest of the financial system. Once the panic climaxed on March 23, so did the corporate bond market, giving rise to an alleviation of financial conditions and, hence, the corporate bond yields started to subside.  Although the Fed's powerlessness should have been clear by now, most of the analysts and "experts" on the matter have not yet awaken from their keynesian-induced stupor. In fact, as Bank of America wrote on May 1 in "A Note To Fed" - a report apparently meant to precipitate the Fed's decision to get off the fence and to start waving it in - "a lot of investors (including non-credit ones) have bought IG bonds corporate bonds the past two months on the expectation they can sell to you. So would be helpful if you soon began buying broadly and in size." By all accounts, Bank of America fears that the record IG bond issuance that has taken place in the past couple months will break the market if the Fed does not start buying. New investment-grade issuance reached another monthly record of $296.6 billion in April, following a $261.4 billion tally in March - significantly above the previous record of $175.5 billion from January 2017 -, bringing the YTD cumulative to $807.1 billion, the fastest start to a year ever and 82% ahead of the pace in 2019. According to the Securities Industry and Financial Markets Association (SIFMA), as of Q1 2017, the US corporate bond market size was $8,630.6 billion. For the sake of argument, the size of this market has stayed constant. Ergo, the total commitment by the Fed, regarding the corporate bonds - the Primary and the Secondary Market Corporate Credit Facilities - adds up to $750 billion, representing something like 8.7% of the total market. To believe the Fed can prop up this and the other financial markets takes a magnitude of credulity beyond belief. In this case, it is the market participants, in their quest to find relatively good collateral, who are inflicting this record debt extravagance, while the financial conditions remain tight.  Finally, the ultimate reason for the lackluster economic growth globally, but more noteworthy of mention the US and the EA, is purely and simply the debt. Because of the ZIRP, and even NIRP in Europe, being implemented for such a long period, there has been low savings accumulation. Additionally, fixed investment (capex) has been subdued, hampering productivity growth. Therefore, households have had less savings and lower wage growth, promoting less than desirable disposable income. With individuals having little income to consume, in order to go back to the pre-GFC pace of economic expansion, consumers would have to borrow massively to make up the slack. However, seeing that they are already extremely indebted, banking institutions got very wary of lending as they used to. Again, the Fed and the ECB are completely impotent against the might of the Eurodollar system's impulses. Notwithstanding, the astonishing debt buildup has turned the economy tremendously frail. Even though the lockdowns only arose in mid-March, the very end of the quarter, the first GDP estimates for Q1 (on annualised terms) for the US and the Euro Area are a ghastly -4.8% and -14.4%, respectively. This speaks volumes about the fragility of this economic system.

To conclude, market participants have learned their lesson back in 2008. After all, there is such a thing as (credit) risk. That said, those fancy derivatives could turn sour when the underlying assets stop performing smoothly due to and economic slowdown or contraction. For instance, consider a junk-rated CLO that has as underlying asset a pool of various subprime credit card debts. Once the economic activity starts to lose some steam, these subprime borrowers will begin to forbear or even default on their debt servicing expenses. As a result, that risky CLO will be launched into the path of devaluation till it turns worthless. Expanding that exercise, you figure out that as the state of the economy keeps on deteriorating, it would not just be the low credit-score individuals that would struggle to pay their debt obligations. Even the prime consumers could face the same kind of hardship. In addition, other types of ABS that have as underlying assets leveraged loans to companies, auto loans, student debts, etc, would also go south. Moreover, having a dwindling economy as a backdrop, any other asset class would go through a period of affliction, from MBS to equities, and possibly sovereign bonds. Obviously, companies make less profit or even generate losses, people cannot pay their mortgages and governments may not be able to steal enough wealth from their citizens, via taxation, to meet their debt expenses. In turn, this all encompassing asset rot would lead to cash lenders becoming far more cautious to whom they lend and against which collateral. Hence, an inescapable deflationary spiral would be in the cards. Unsurprisingly, this is what occurred in March and in all likelihood will happen again, very soon, as economic activity remains virtually stalled. There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved. As discussed on the third part, owing to this debt-based monetary system being utterly unstable and, to add insult to injury, to being centered around the US dollar, everybody will want a change of scenery. This system may have induced a great period of economic development and international trade in its heyday. Nevertheless, since 2008, the system is now hindering economic development and international trade. Therefore, the establishment of a new monetary system, with fair and sound bases, would be beneficial for everybody, including the American people.

Furthermore, as the financial debacle proceeds, the wizards at the Eccles Building are hopefully going to be uncovered for what they truly are, mere con men.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed