|

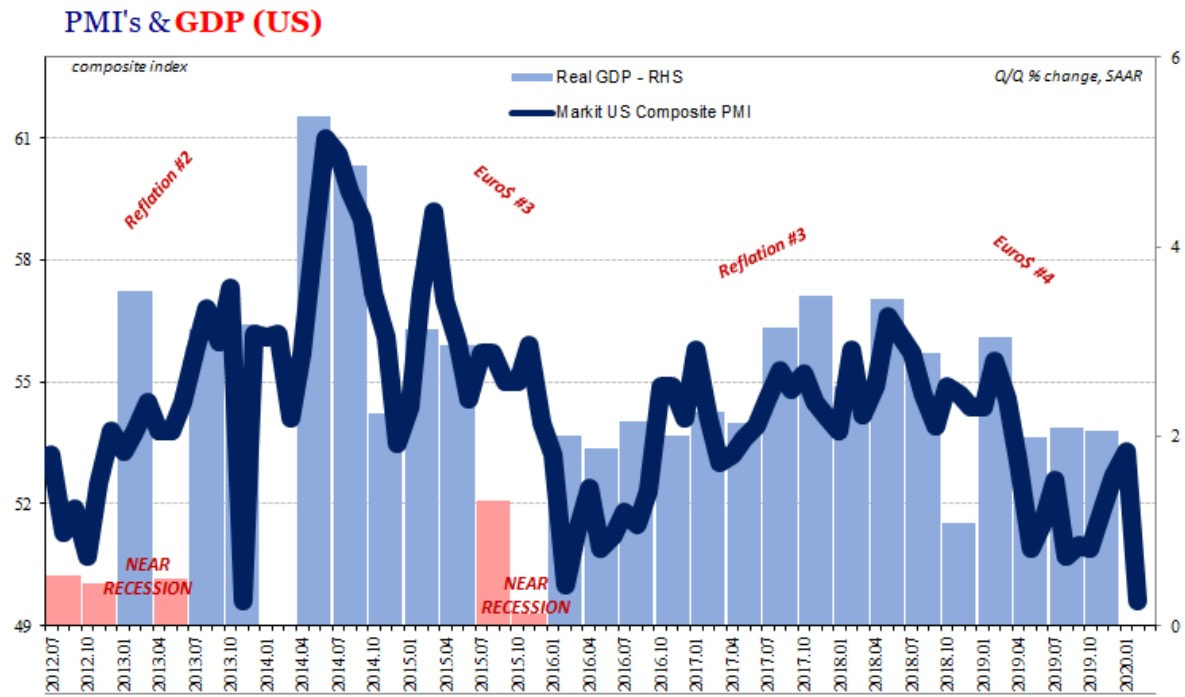

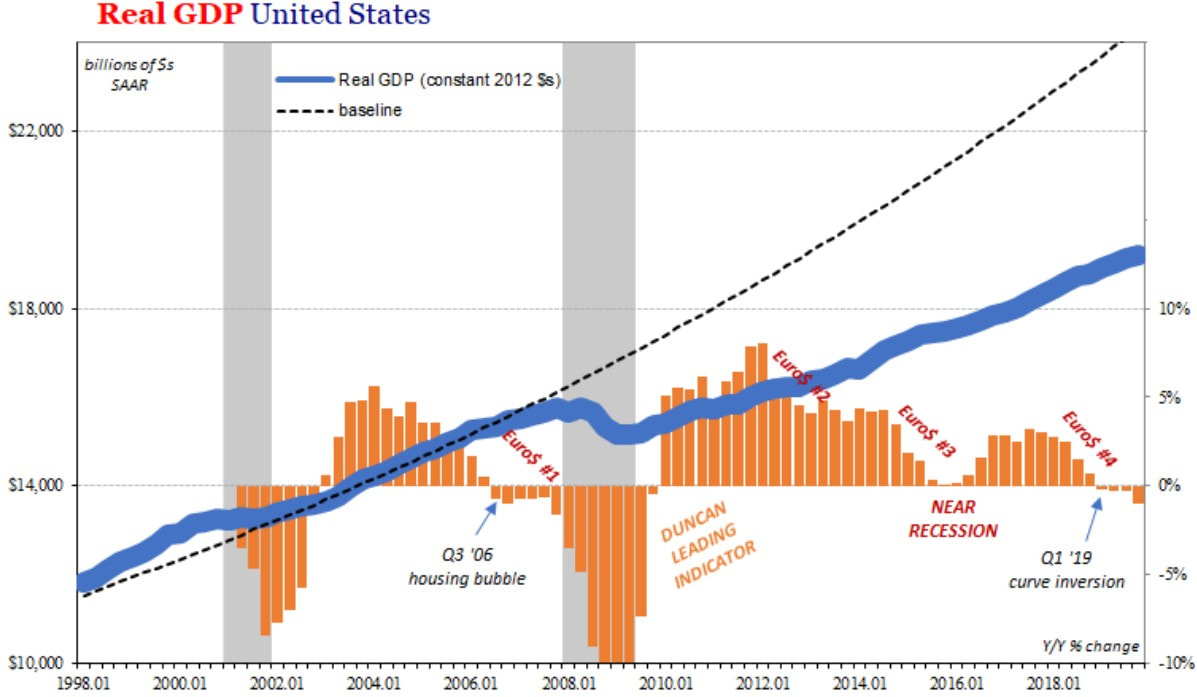

Picking up on the analogy presented on the second part's introduction, the Eurodollar system's liver has been severely impaired ever since the GFC. With the current financial meltdown that is bound to be of greater magnitude than the 2008 crisis, the liver will collapse at last. If a transplant does not follow, then the patient will die. In this last part of the series, I am going to delve into the various aspects surrounding the crash, why it should have surprised nobody, and whether it is over or just beginning. As I explained on part two, starting on early 2018, some signals of rising financial tightening were appearing, like soaring repo rates above the EFF rate and the dollar appreciating. Those signals began to materialise very soon on the GDP figures. Looking at the graph on the left, the PMI had been dwindling since the second quarter of 2018. The GDP, historically, has been following the PMI. Therefore, the PMI is a good indicator of the economic performance, depicting the health of the economy before the GDP statistics finally come out. An even better prognosticator of near-term economic activity is the Duncan Leading Indicator (DLI). As the name suggests, this indicator is a harbinger of future economic performance, signaling a contraction or recession for several quarters in advance. The DLI is the ratio of consumer durables spending plus residential and business fixed investment to final sales, with all data adjusted for inflation. Final sales are defined as the gross national product less the change in business inventories. As a result, the indicator is the ratio of the cyclical components of expenditure to GDP, except that the change in business inventories has been subtracted from both the numerator and denominator.

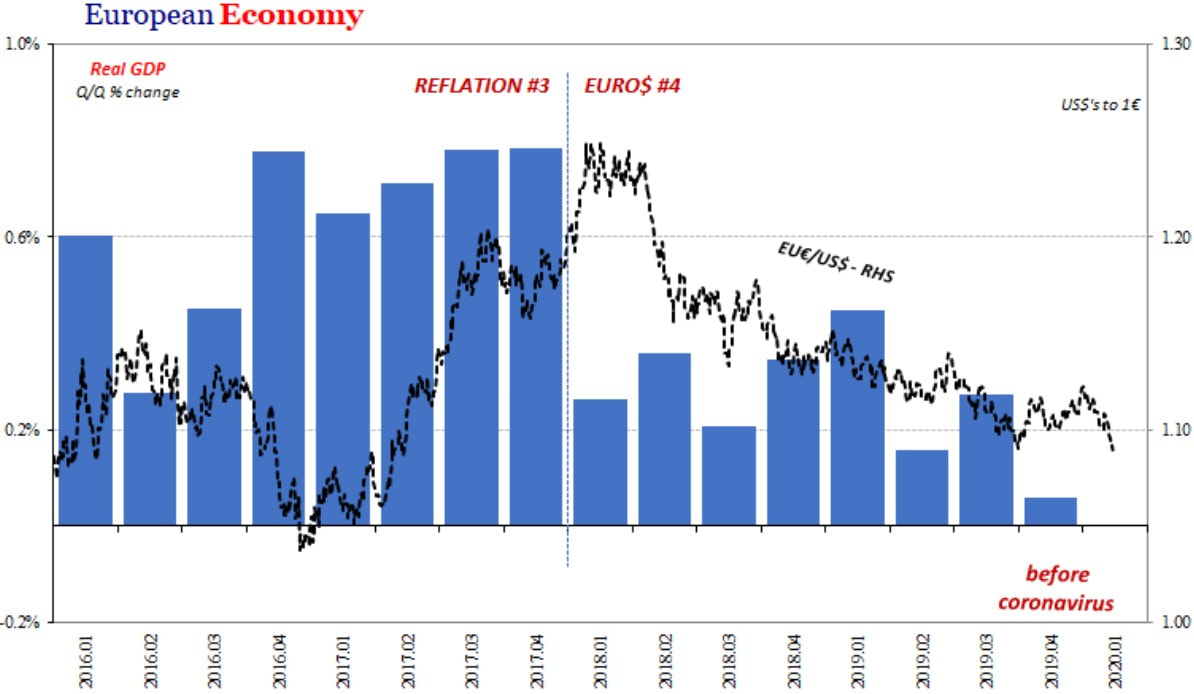

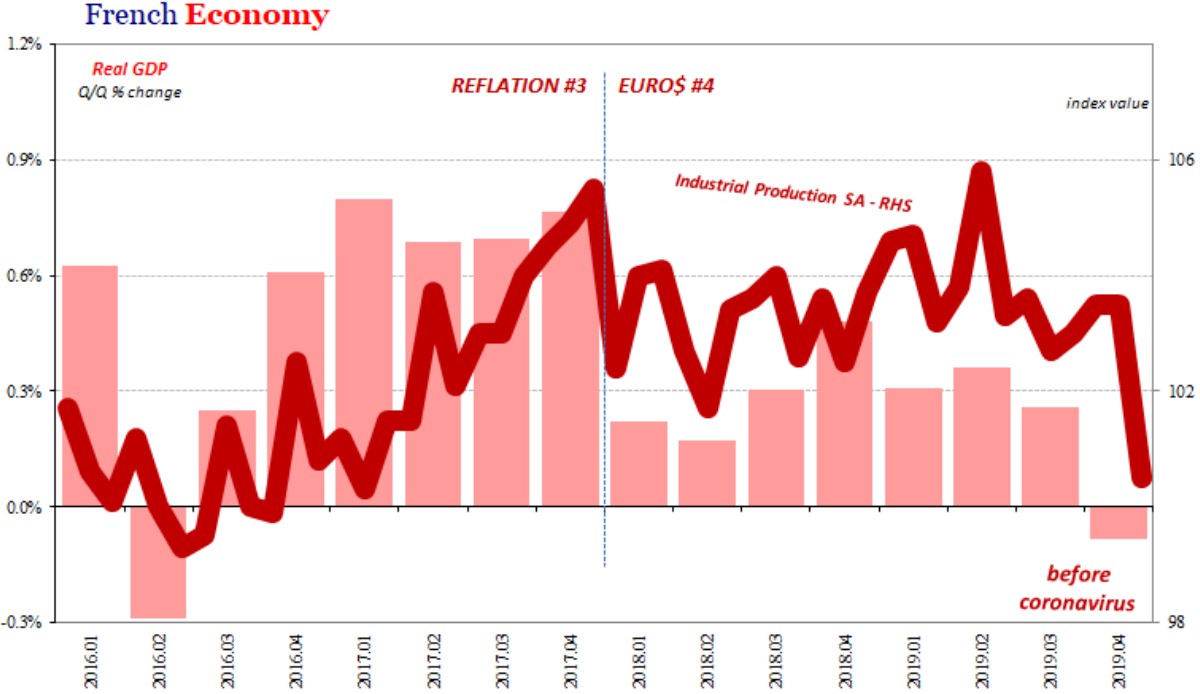

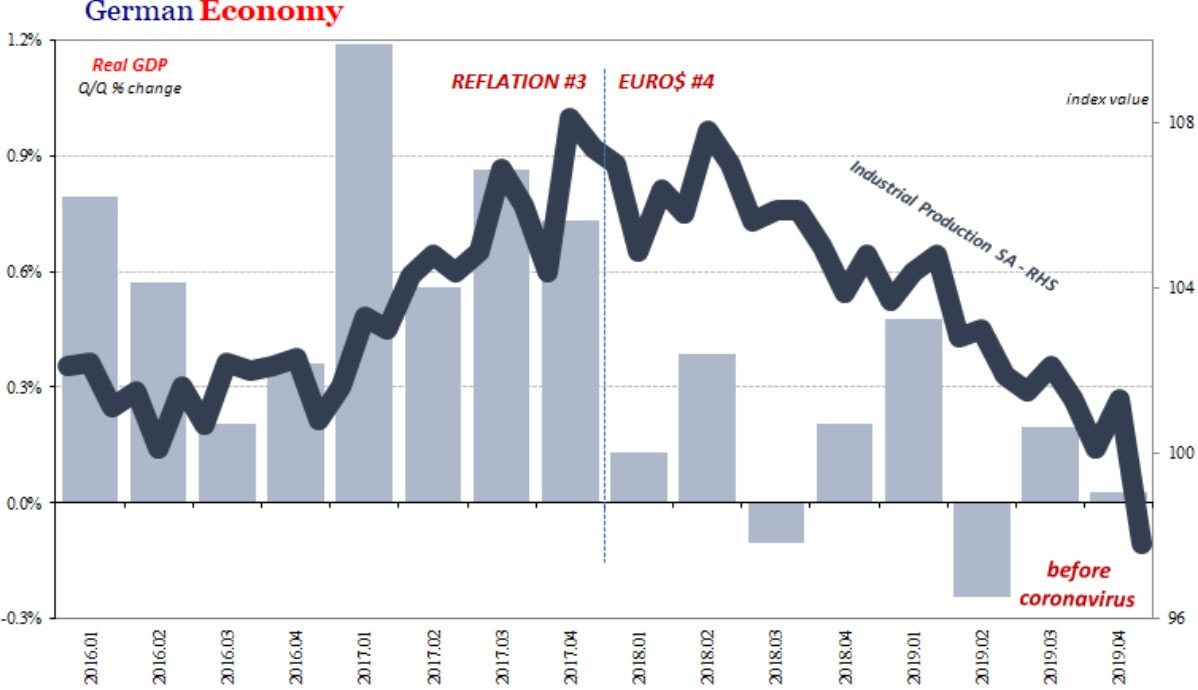

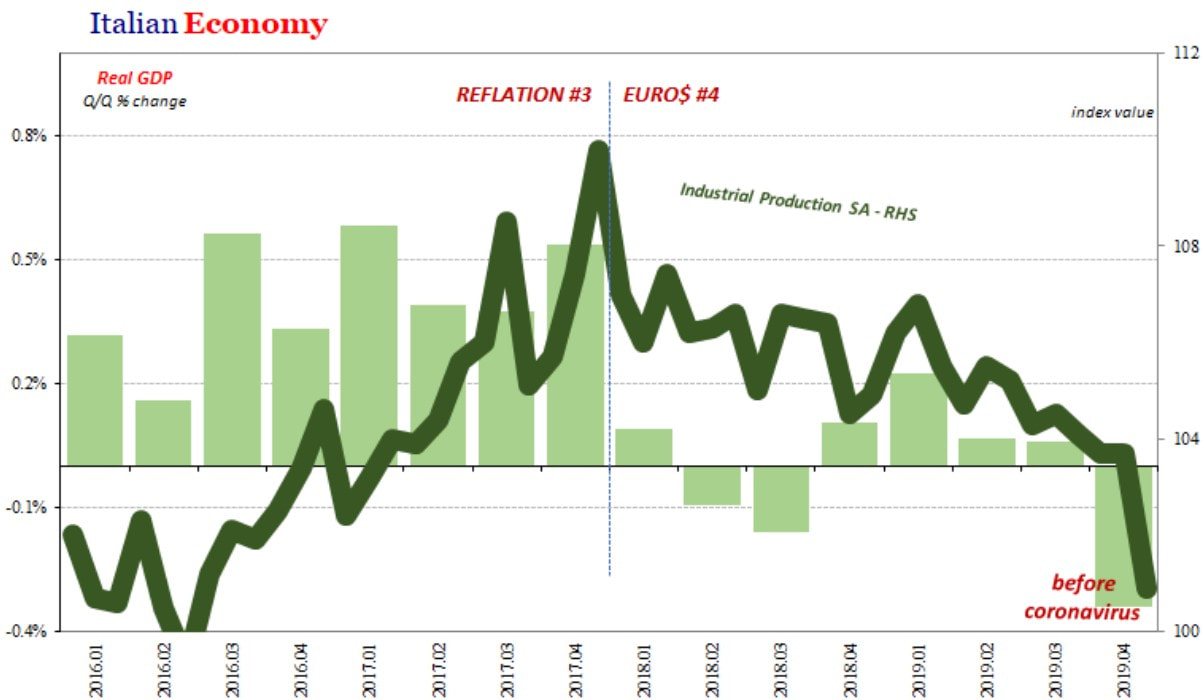

Hence, the US economy's check engine light had been flashing for more than a year, which means it could have broke down in the middle of the road at any given time. Instead, it got hit by an eighteen-wheeler truck. The evidence of a slowdown was far greater in Western Europe. From 2018 onward, the three biggest economies have struggled to increase industrial production. Although, Germany and Italy had shown no signs of a rebound throughout this time frame, France had presented some promising figures up to Q2 2019, joining the rest of the pack thereafter, having posted a negative value for the final quarter of last year, just like Italy.

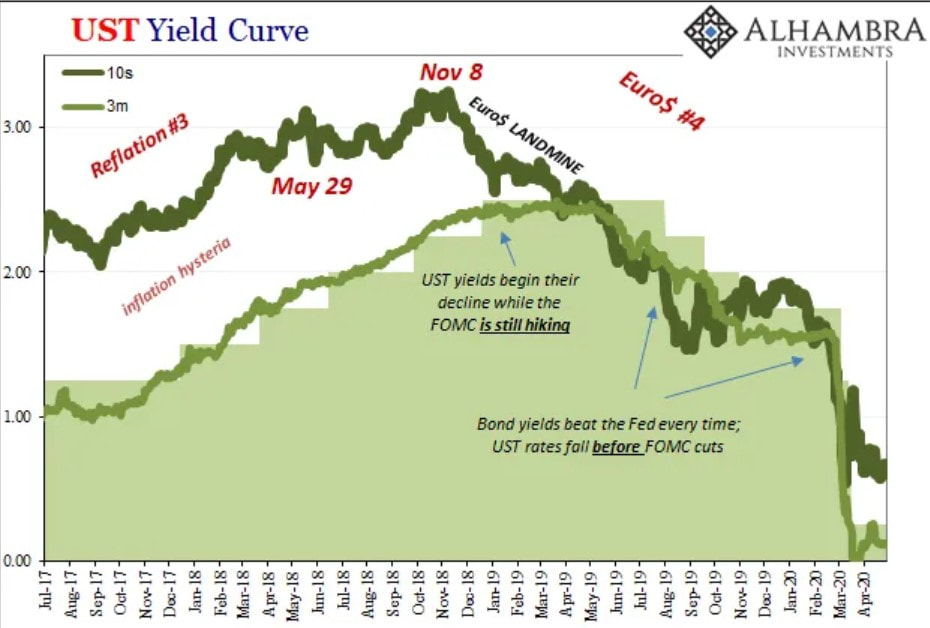

Furthermore, since late 2018, the yields of the US Treasuries had been transmitting, to those paying attention, that the financial state was decaying, which precipitated the central bankers all around the world to ease their monetary policies. Let's not forget this occurred long before the word coronavirus being bombarded on every news and social media outlet. Hence, the developed economies were set for a recession sooner or later - again, it would have broken down in the middle of the road -, dragging the emerging markets with them. For some reason, almost everybody was gobsmacked by the financial debacle that took place in March. However, the financial markets, as I said, were shouting that financial conditions were deteriorating and that commerce was going to wane down, more than a year ago.

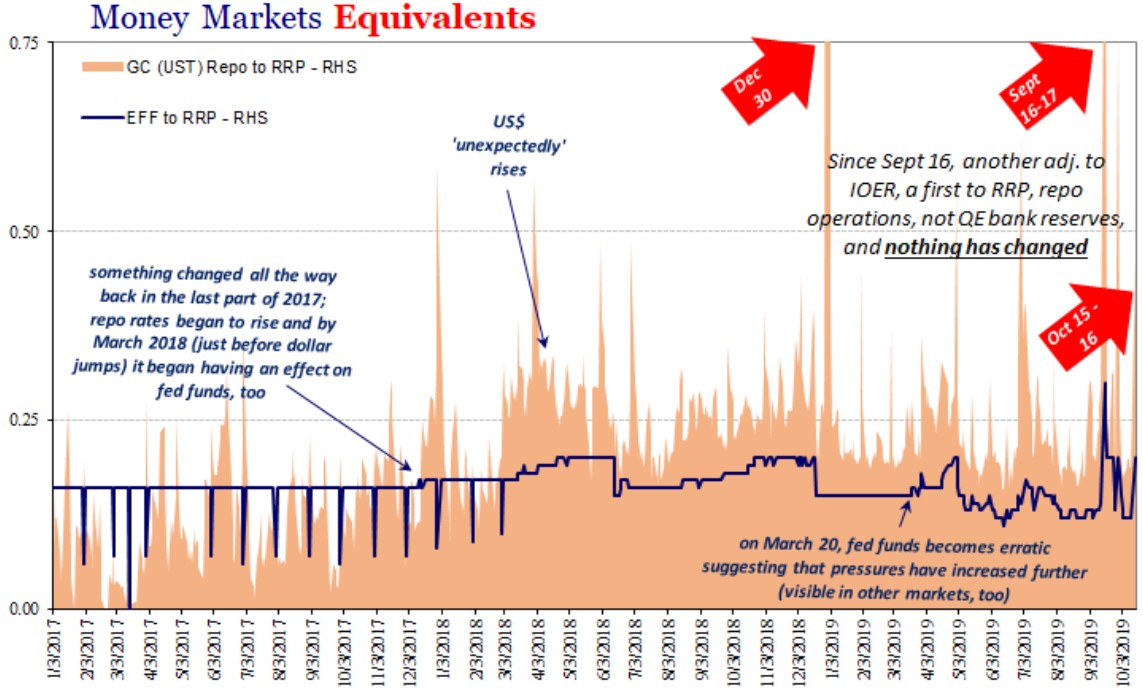

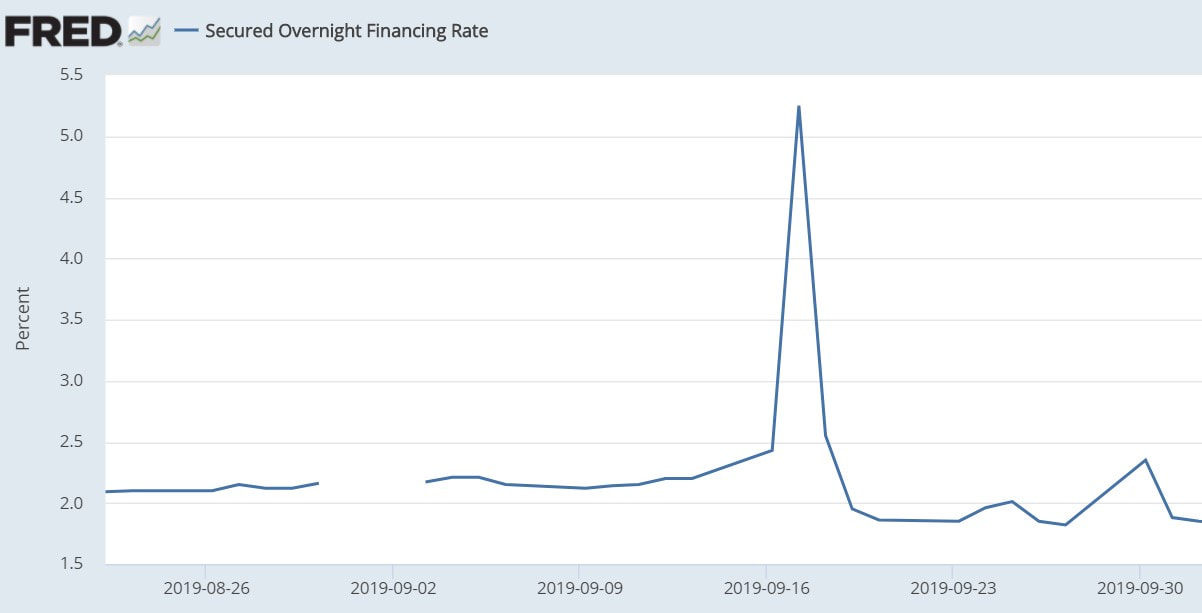

Moving on to last summer, on July 31, the Fed cut interest rates targets (for the EFF) for the first time since December 2008. As the graph above on the left demonstrates, the FOMC was forced to reverse their hiking course and embark on easing efforts, due to declining Treasuries yields. The 10-year tenor hit its dip in September, which happened to be when the "repo-calypse" began. Accordingly, the already erratic EFF rate jumped, and the GC repo rate and the Secured Overnight Financing Rate (SOFR) - broad measure of the cost of borrowing cash overnight collateralised by Treasury securities - spiked tremendously. These fluctuations of rates only calmed down when the Fed interjected. So they want us to believe. In reality, the actions undertaken by the Fed were only smoke and mirrors. The adjustments on the interest rate on excess reserves (IOER) and the reverse repurchase agreement rate (RRP), the "temporary" repo operations and the comeback of the beloved quantitative easing, though Jay Powell and his pack emphatically stated it was not QE, were simply a sleight of hand. The truth is that the markets soothed themselves (only slightly and for awhile).

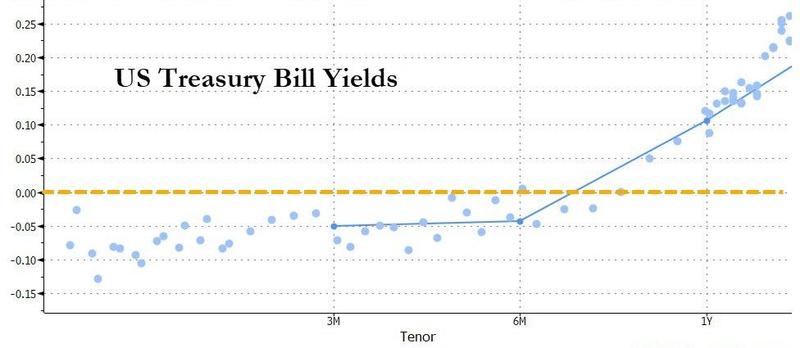

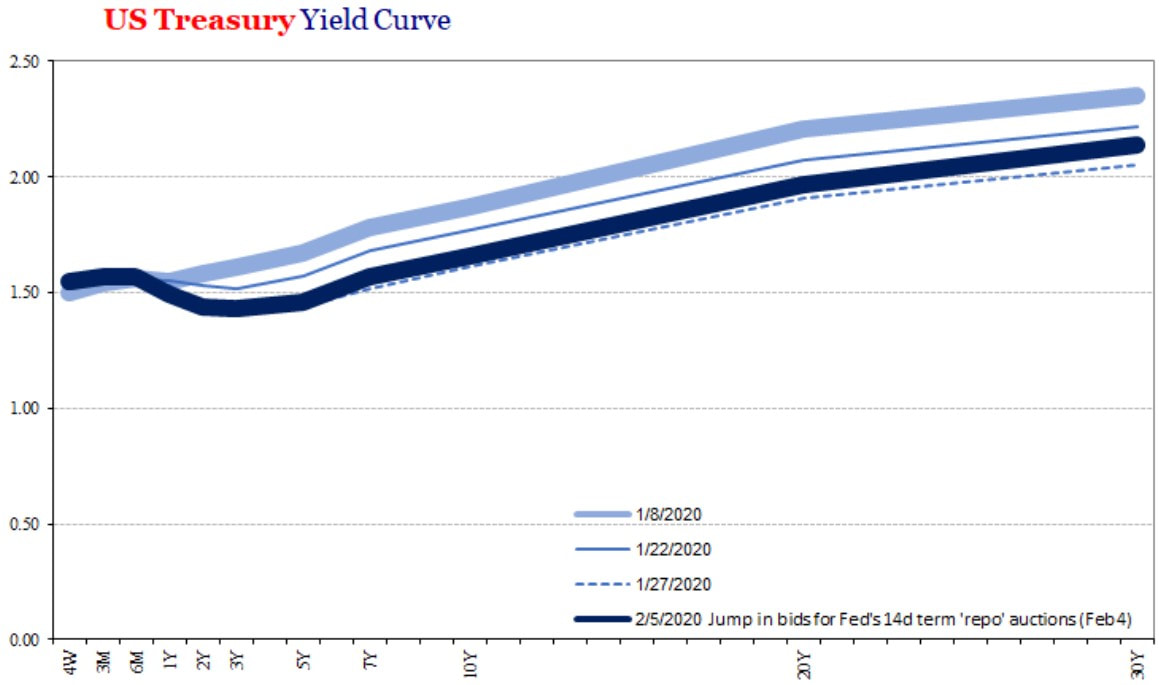

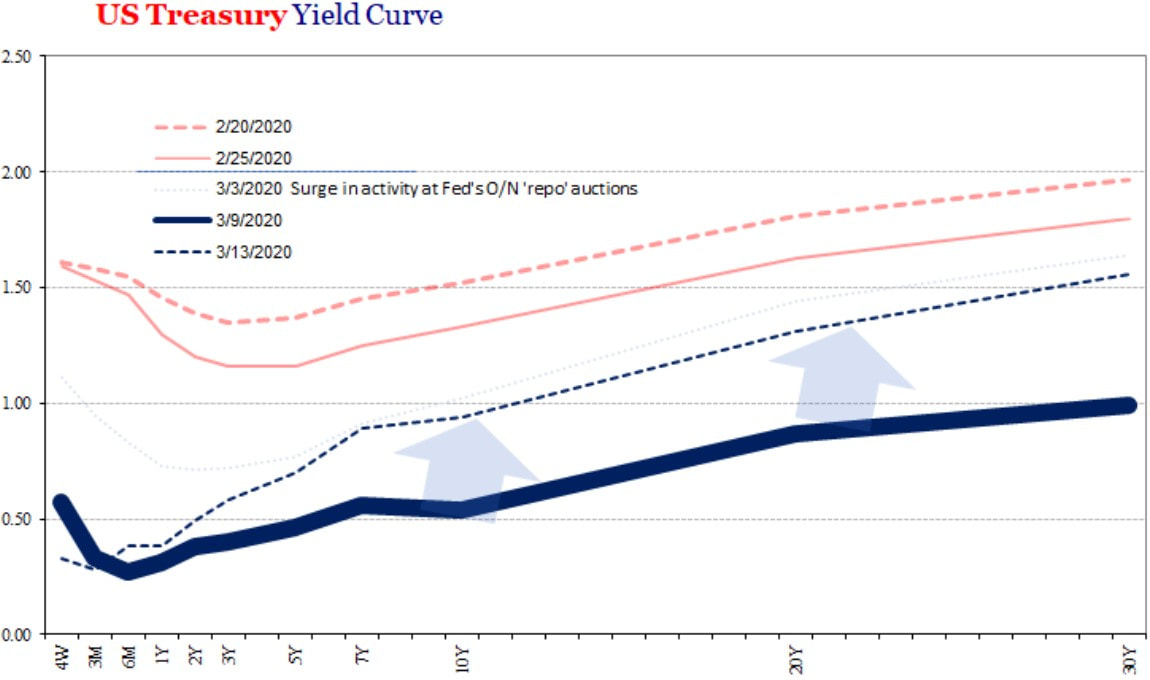

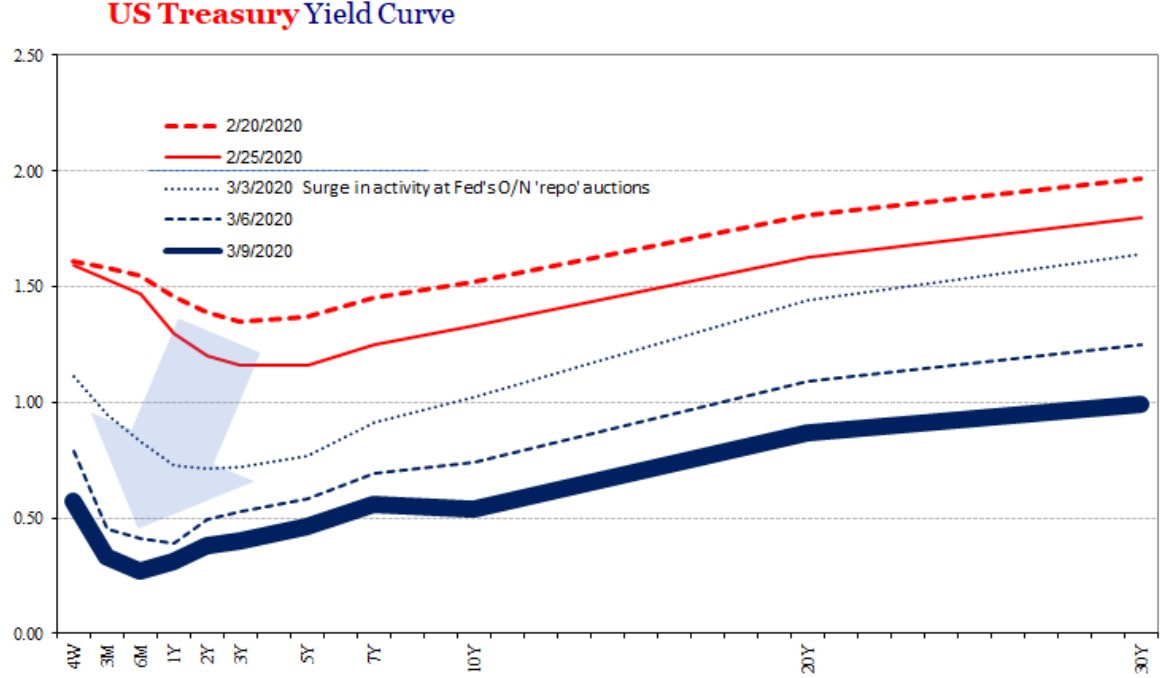

With COVID-19 entering the picture, the already frightful scenario got much worse very quickly. The yield curve was inverted once again by the end of January, when the kung-flu was only a Chinese affair. Then, from February through early March, the whole curve gradually subsided, indicating, as you know, a slipping economy and, consequently, the falling apart of the financial conditions. Subsequently, during the worst part of the financial turmoil, in mid-March, the T-bills' yields (maturities of a year at most) remained close to the zero bound, while the other yields, of the notes and bonds, climbed till the end of the markets' sell-off in March 23, steepening the curve substantially. Afterwards, the short-end increased a little bit and the long-end dropped close to early March rates and so it remains to this day.

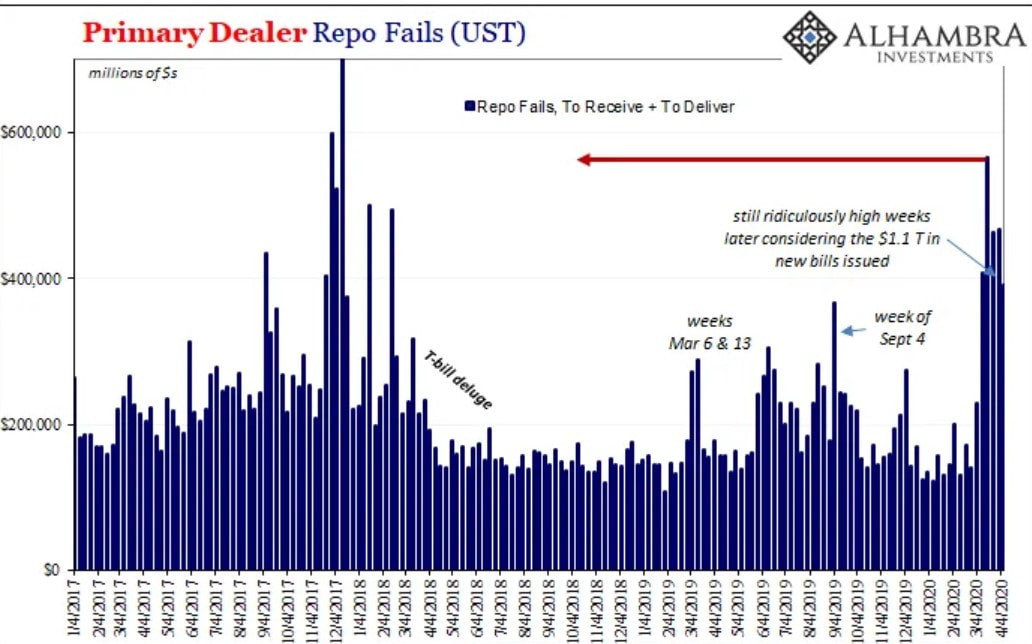

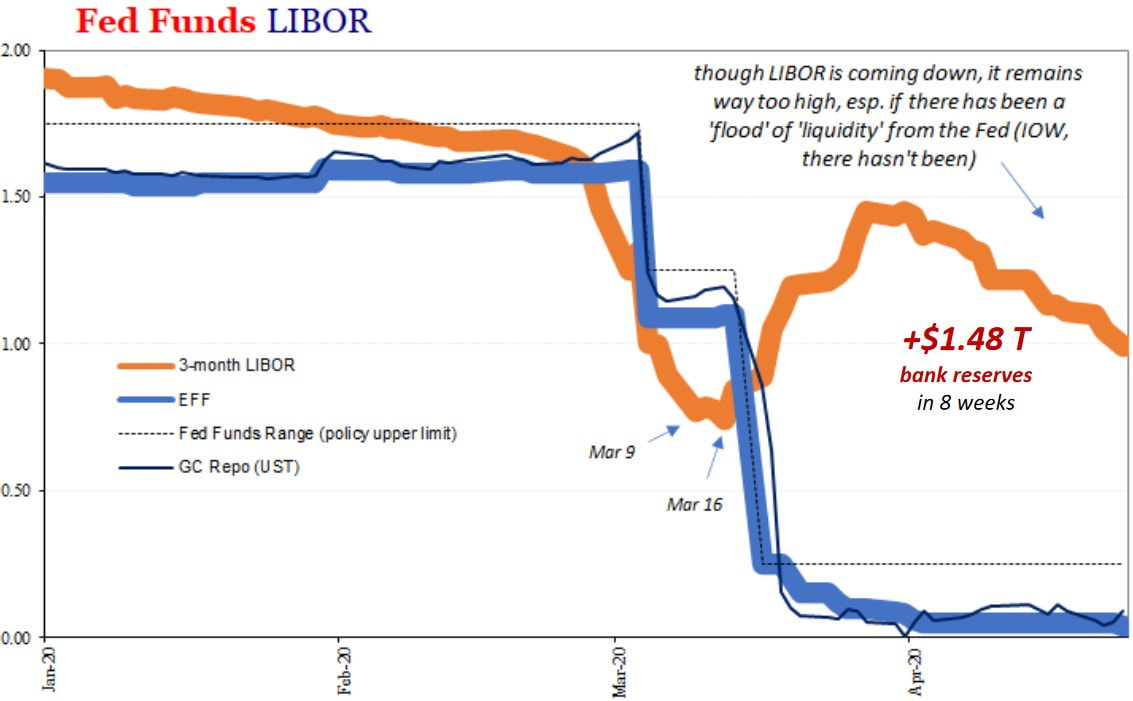

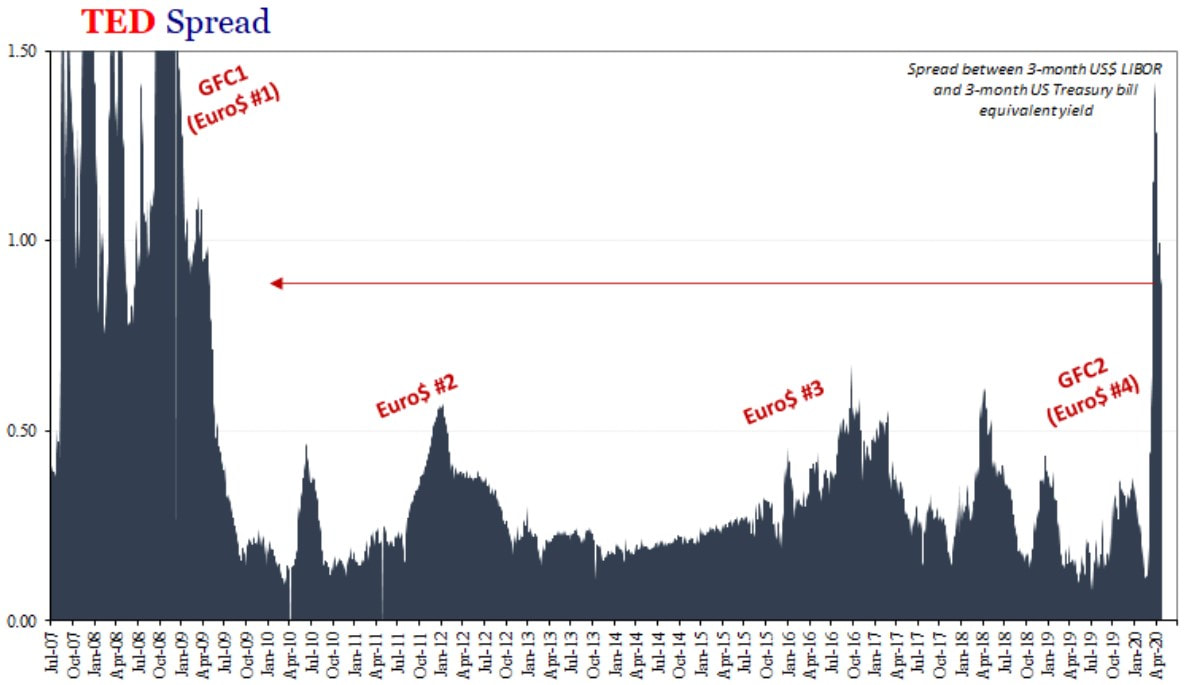

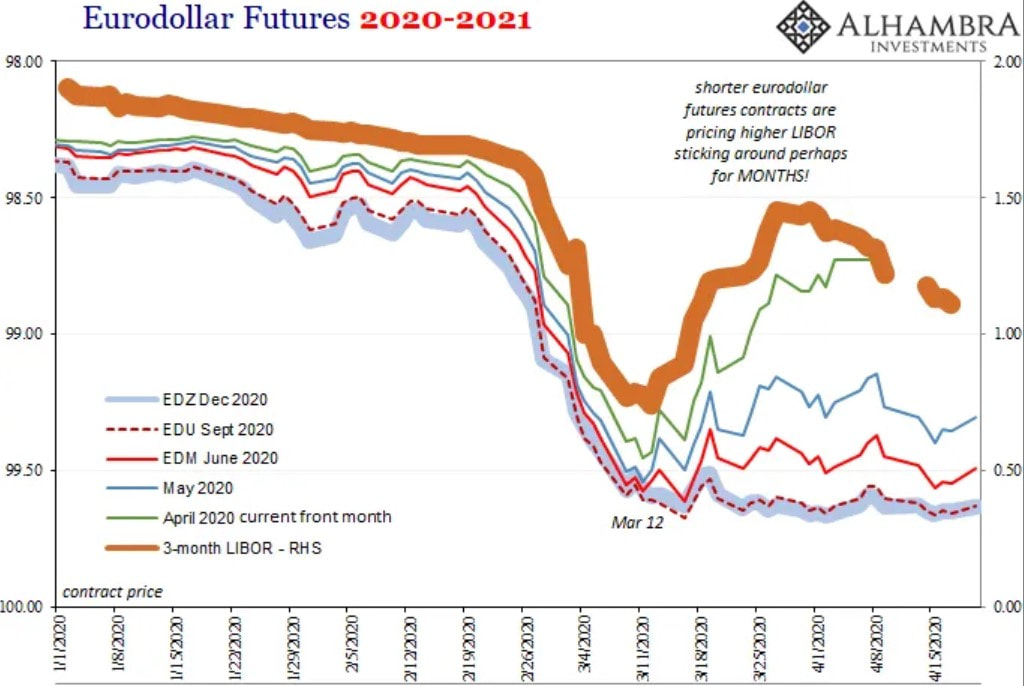

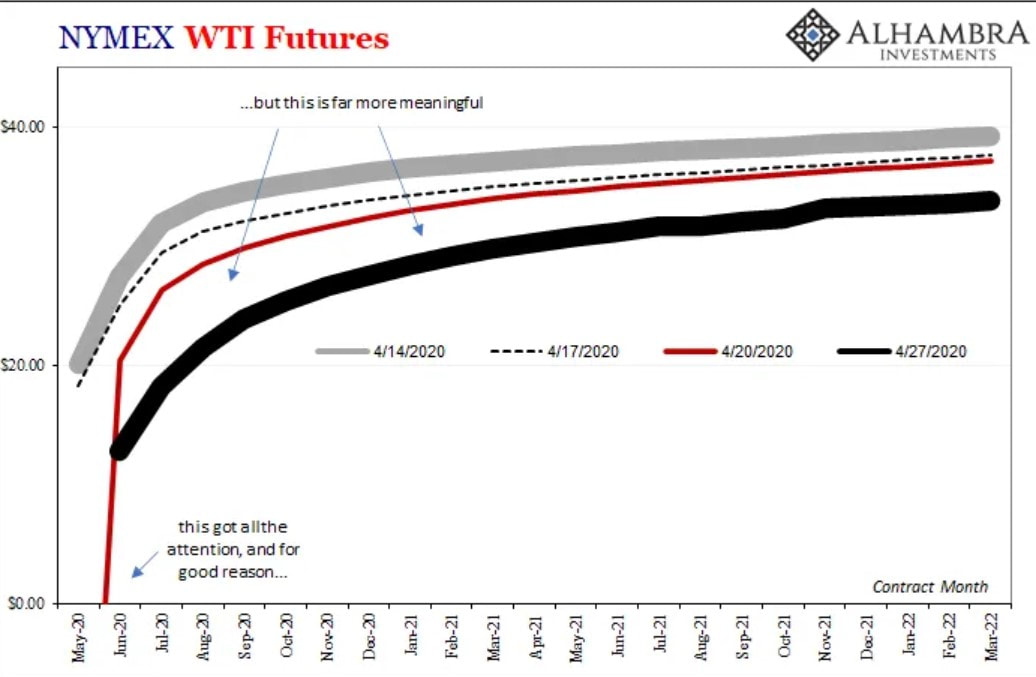

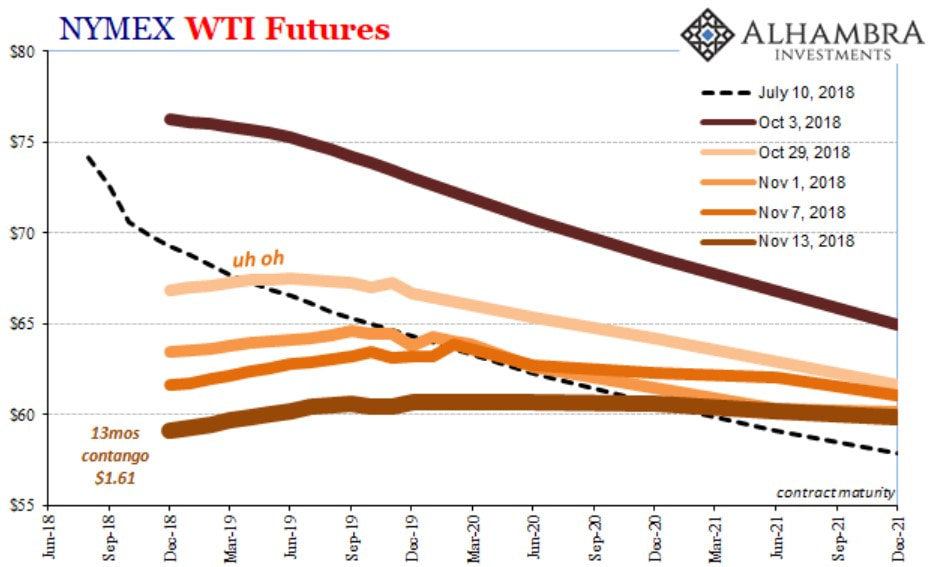

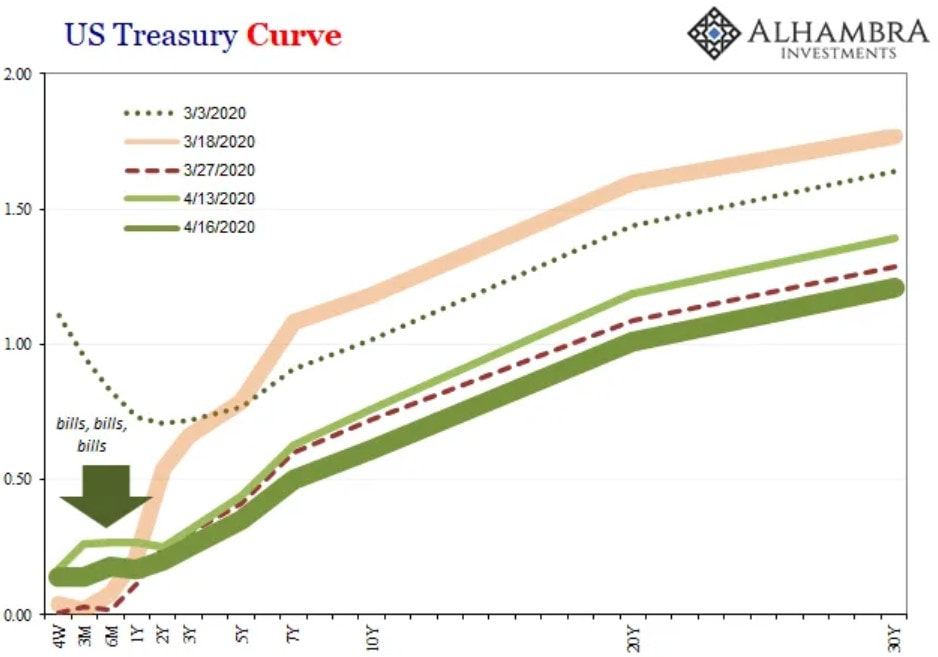

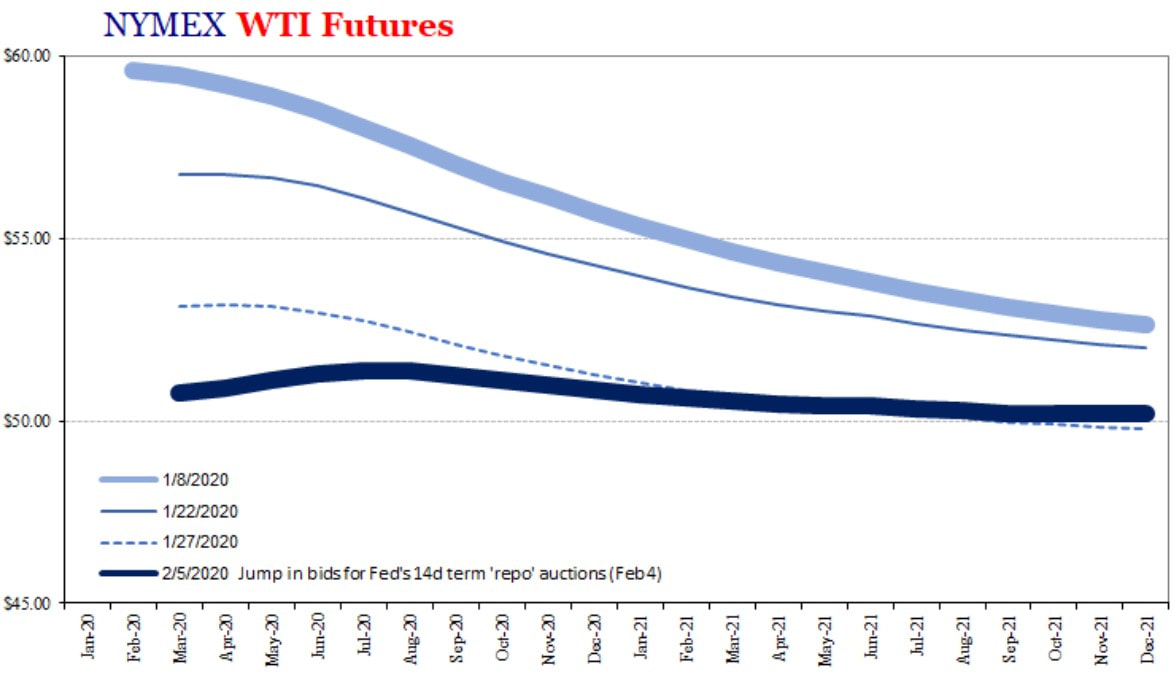

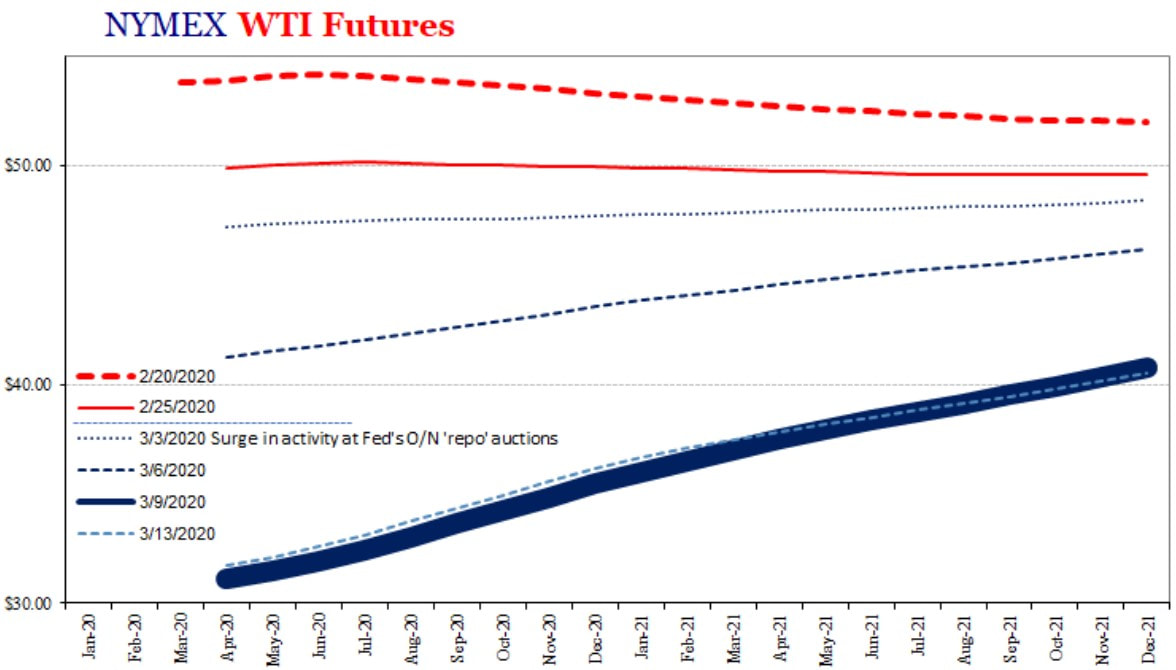

Similar to the GFC, which I exposed in part one, during this financial panic, there is a run on "cash". Despite the cash lenders having funds available and the financial institutions with funding needs having collateral to exchange for liquidity, the lenders became extremely picky on the eligible collateral. Previously accepted assets, such as CLO and other ABS, corporate bonds including HY, and even equities, were blacklisted by the lenders. These became so cautious that they were only taking collateral of the most "pristine" kind. Consequently, everybody tried to get the crème de la crème collateral, the T-bills. This makes their prices to surge and, therefore, their yields to plummet. Throughout the worst period of the meltdown, these yields turned negative, as the next graph portrays.  Likewise, the amount of repo fails, which are the repurchase agreements that do not come to pass, skyrocketed in the middle of March and have remained in high levels ever since.  Inasmuch as the variety of eligible collateral was immensely reduced, market participants had to get liquidity selling assets, specifically the ones denominated in US dollar, to meet their obligations, whether it was debt servicing, margin calls, payroll expenses or any other routine expenses. No asset class escaped the fire sale liquidations, except the T-bills. Paradoxically, gold, which is viewed as a safe-haven in episodes of financial trouble and, consequently, was expected to have soared, it joined the others and plunged too. Yet, since the crash climax on March 23, gold prices have recouped its ascending trajectory.  Additionally, another peculiar situation unfolded at that time that hardly went away. Whereas the EFF rate and the GC repo rate were dropping, the US dollar LIBOR went its own way, moving upward. On the one hand, the EFF rate decreased and has stayed low owing to the fact that primary dealers are tremendously well supplied with reserves and if there are depository institutions looking for funding but are deemed unreliable, the others refuse to provide them with the funds at any interest rate. As a result, because those risky institutions are left out from this market, the EFF rate does not express the financial health of its participants. Seeing that this rate is low, everybody thinks that the banking system is operating smoothly, when in fact the complete opposite applies. Similarly, the repo rate has been in very diminished levels, it even got lower than the EFF for awhile, which in normal times denotes a perfectly functional and liquid financial system. Obviously this is not the case. The reason is there was such a scarcity of eligible collateral that only the ones holding these (T-bills) could participate in the repo market. On one side, there are banking institutions with plenty of funds to lend, ergo there is a glut of supply. On the other side, a few institutions holding T-bills make up the demand. Therefore, the repo rate fell to near the zero bound. On the other hand, although the Fed has injected almost $1.5 trillion reserves in the primary dealers' balance sheets in eight weeks, the LIBOR, which depicts the willingness to lend and the perceived risk of shadow bankers operating in the London Eurodollar markets, shot up. Indeed, the participants of the Eurodollar system felt there was a lot of credit/counterparty risk in the system, regardless of the interventions pursued by the Fed.  In spite of the LIBOR having abated somewhat, it is still at a higher level since the end of the GFC. Looking at that crisis, the LIBOR lessened for long periods, with each spike upward being shorter than the previous one, making everybody believe that the worst had passed due to the efforts made by Ben Bernanke and fellow technocrats. Little did they know that the most horrible part was yet to come. So, you may be wondering if March was just the amuse-bouche and that the main course is yet to be served.  One way those doubts could be cleared is by checking out the Eurodollar futures curve. In a nutshell, these curves are indicating that the financial constraints will remain for awhile. In more detail, Eurodollar futures get settled in three-month LIBOR. Hence, it has an enormous potential to describe what participants are thinking about where the LIBOR will be at certain points in the future. Thus, the back-end of the curve expresses the participants' expectations of the liquidity conditions for next year and beyond. For that matter, it conveys their presumptions on the Fed's monetary policy to be enacted then and on the LIBOR as well.  Taking the oil market's signals into account, one could assume the Eurodollar participants are being overly sanguine, meaning that the main course is still being prepared. The relentless decline in the oil prices points to reduced demand, which reflects the anemic global economy that we are experiencing. One may think that this is because of the corona-induced economic shutdown and once the lockdowns are lifted the economy will return to its prior level in a jiffy. Although it is true that the present weak demand for oil was indirectly caused by the COVID-19, the oil futures are alerting to a continuously subdued demand (compared to the pre-virus paradigm) until at least March of 2022. This is not just about oil, this concerns the economic activity as a whole. Inasmuch as oil is by far the most used commodity in the world, for all kinds of industries, investors are speculating that the worldwide economy will not bounce back before for the following two years, at least.

Consequently, if these signals coming from the oil market do in fact transpire, even if just partly, the current financial woe will not have an end in sight. The market participants that comprise the Eurodollar system, whether they are governments, financial institutions, companies or individuals, with debt obligations (denominated in US dollar of course) will continue to struggle to come up with the needed greenbacks. Unsurprisingly, several countries in the emerging world will likely go through sovereign debt crises, once their reserves of US dollars reach a certain threshold. Some people au courant with these matters say that a Plaza Accord 2.0 will have to take place to prevent that massive crisis from hitting a big chunk of the world. Albeit this matter is a topic for another post(s), I take the view that the dollar shortage crisis in the emerging market realm may prompt the end of the dollar hegemony, giving rise to a new era where a neutral means of exchange will be the global reserve. One day, everybody, especially at the emerging bloc, is going to realise this system has, since 2008, benefited nobody because economic and, ergo, financial conditions have been severely hindered. Therefore, they will unite and demand for a new monetary system based on a neutral, fair and solid grounds. The outbreak of the current crisis and its spillover in the world have confronted us with a long-existing but still unanswered question, i.e., what kind of international reserve currency do we need to secure global financial stability and facilitate world economic growth, which was one of the purposes for establishing the IMF? In conclusion, the resentment felt by the emerging countries, and to some extent the developed ones too, towards the dollar privilege will lead in its collapse.

Moreover, the United States acting like a spoiled brat, as it has been - and it seems to get worse by the day - since their currency gained the global reserve status, it only helps speeding up the process of abandoning the dollar. During this crisis, the US government is embarking on a spending spree to rescue businesses and individuals and to keep markets afloat. As a result, the national debt is shooting to the moon, while the output growth becomes negative and anemic in the foreseeable future. To pay for all of this, the Fed simply introduces QE infinity, ZIRP and a myriad of alphabet soup programmes. Accordingly, when the whole world stops considering the US dollars as a global reserve currency, there will be nobody to absorb that flood of US dollars, except the American people. As a final remark, this does not augur well for America.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed