|

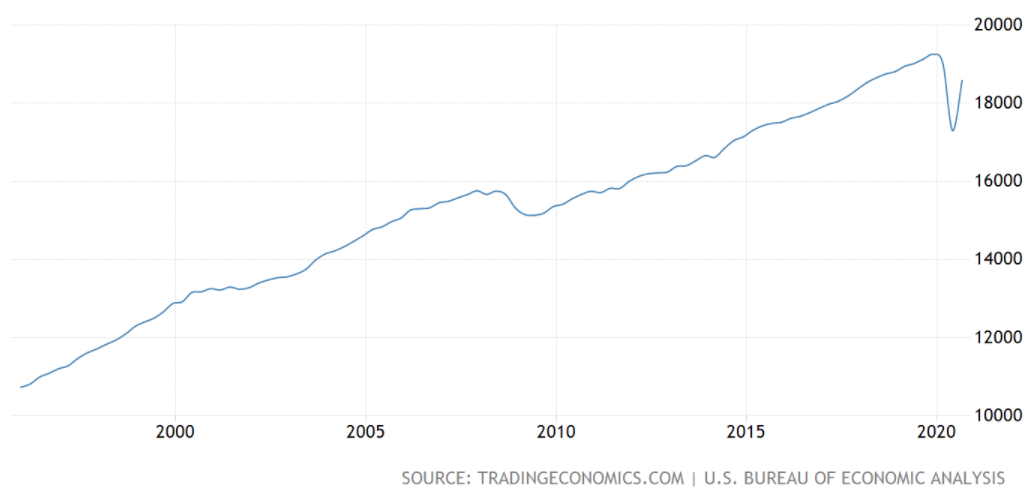

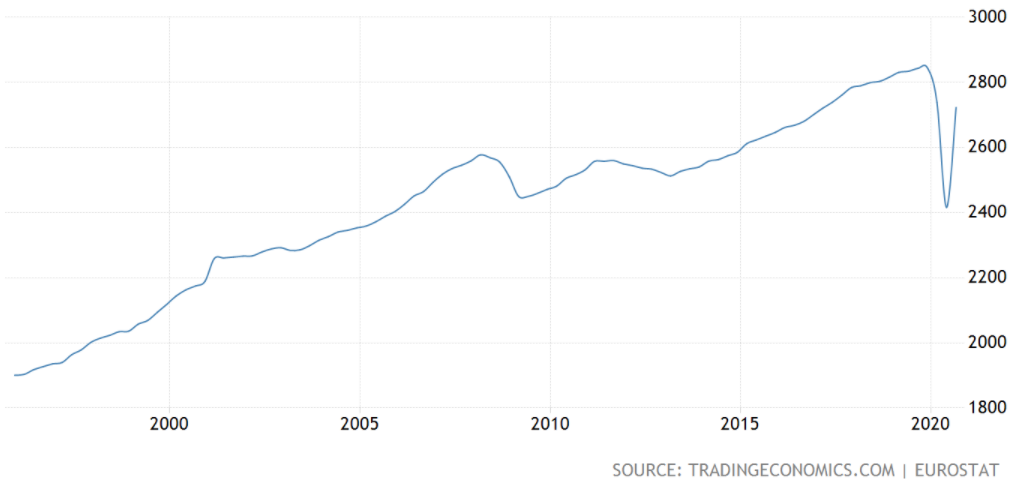

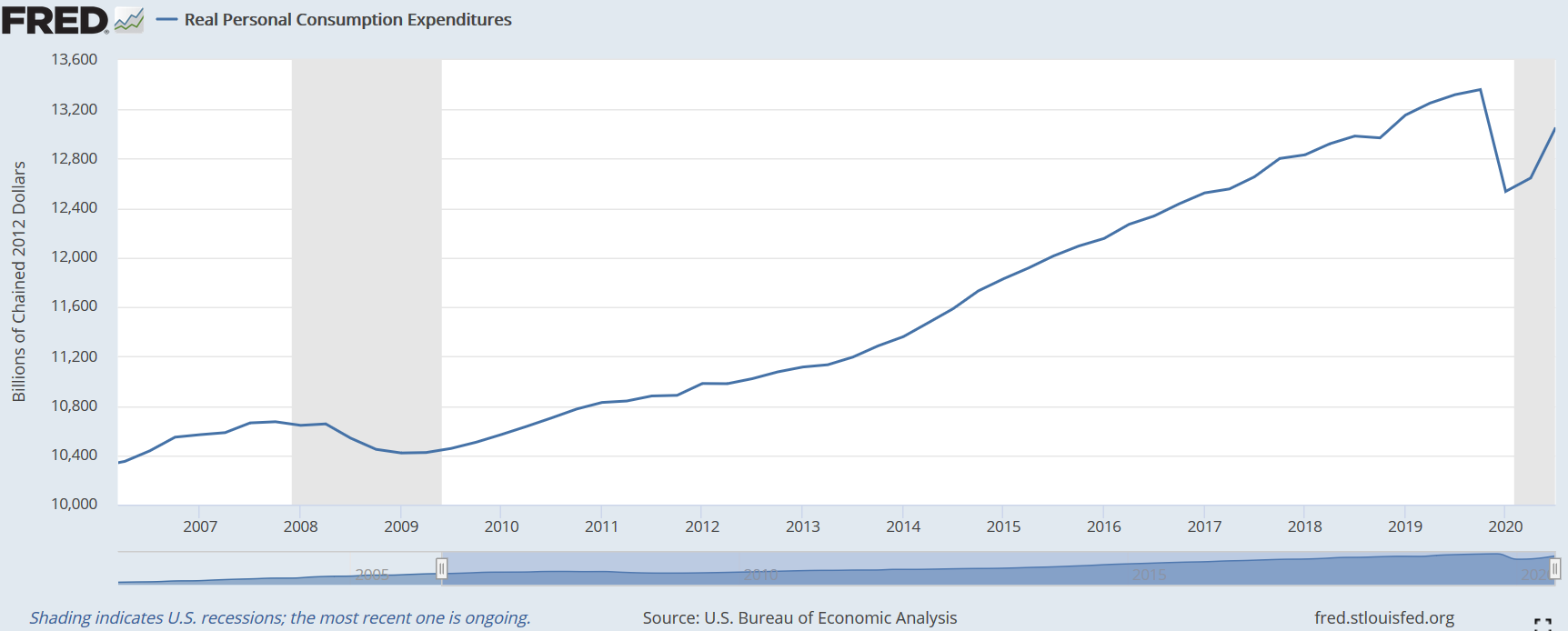

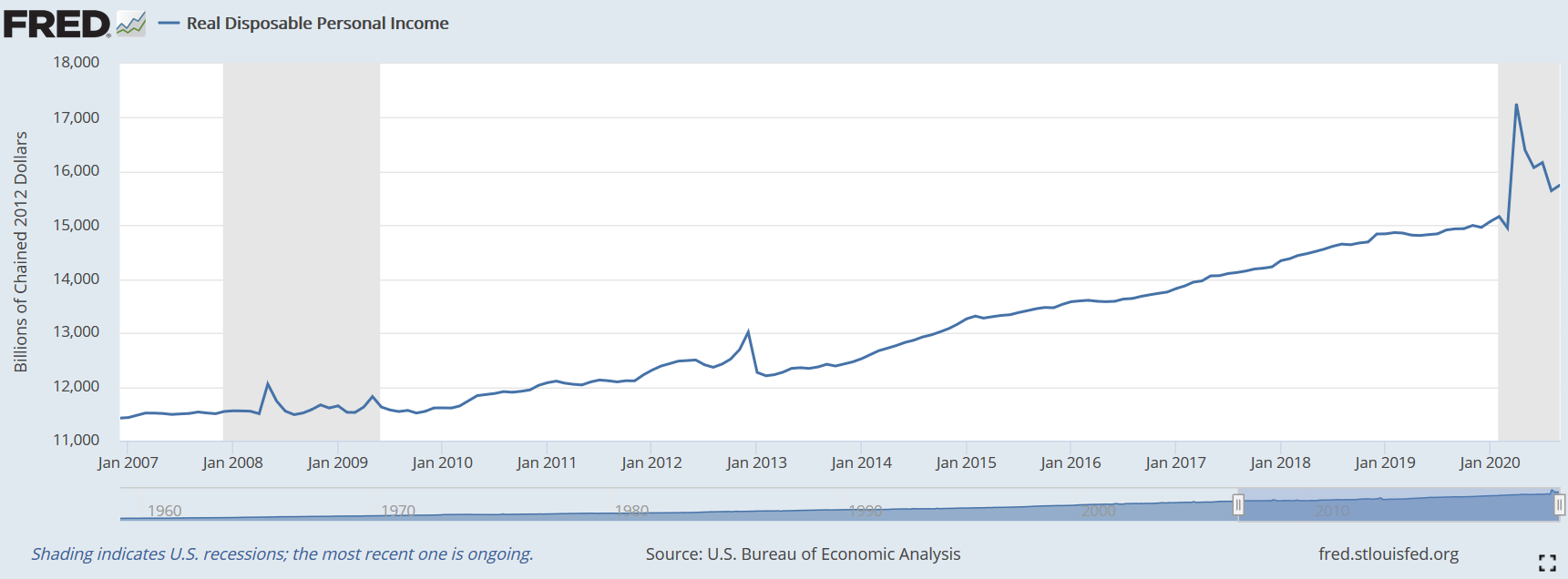

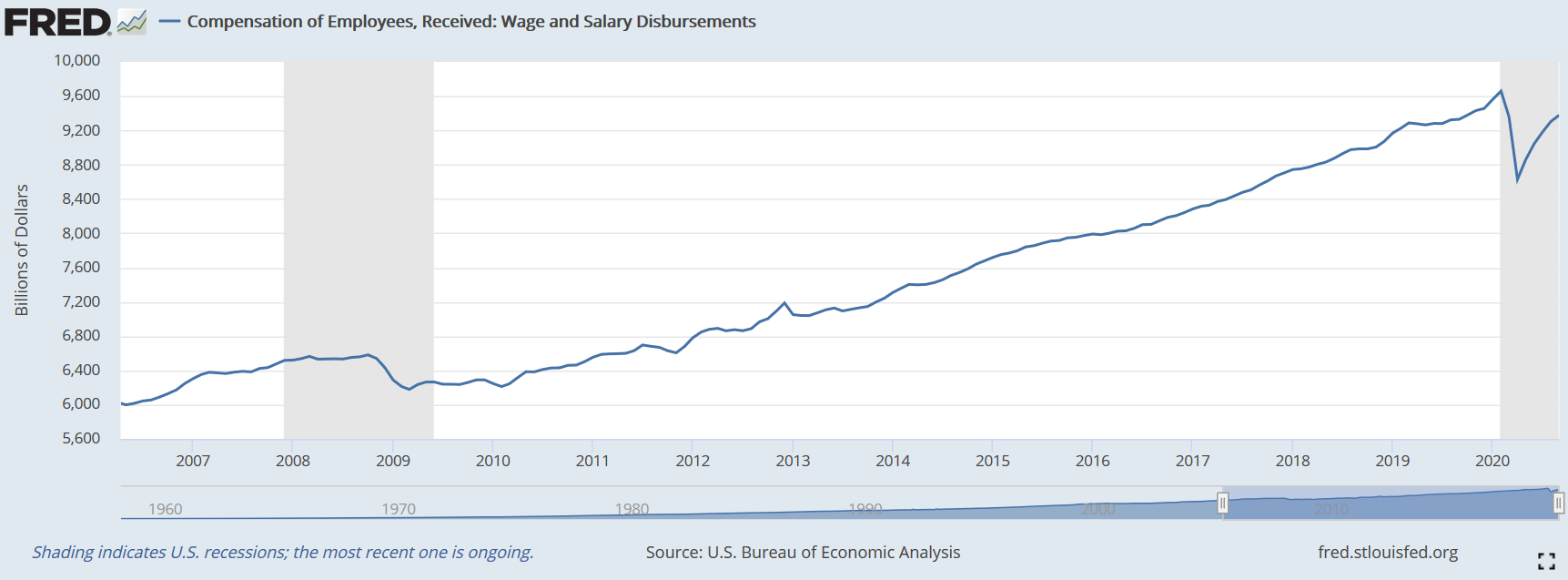

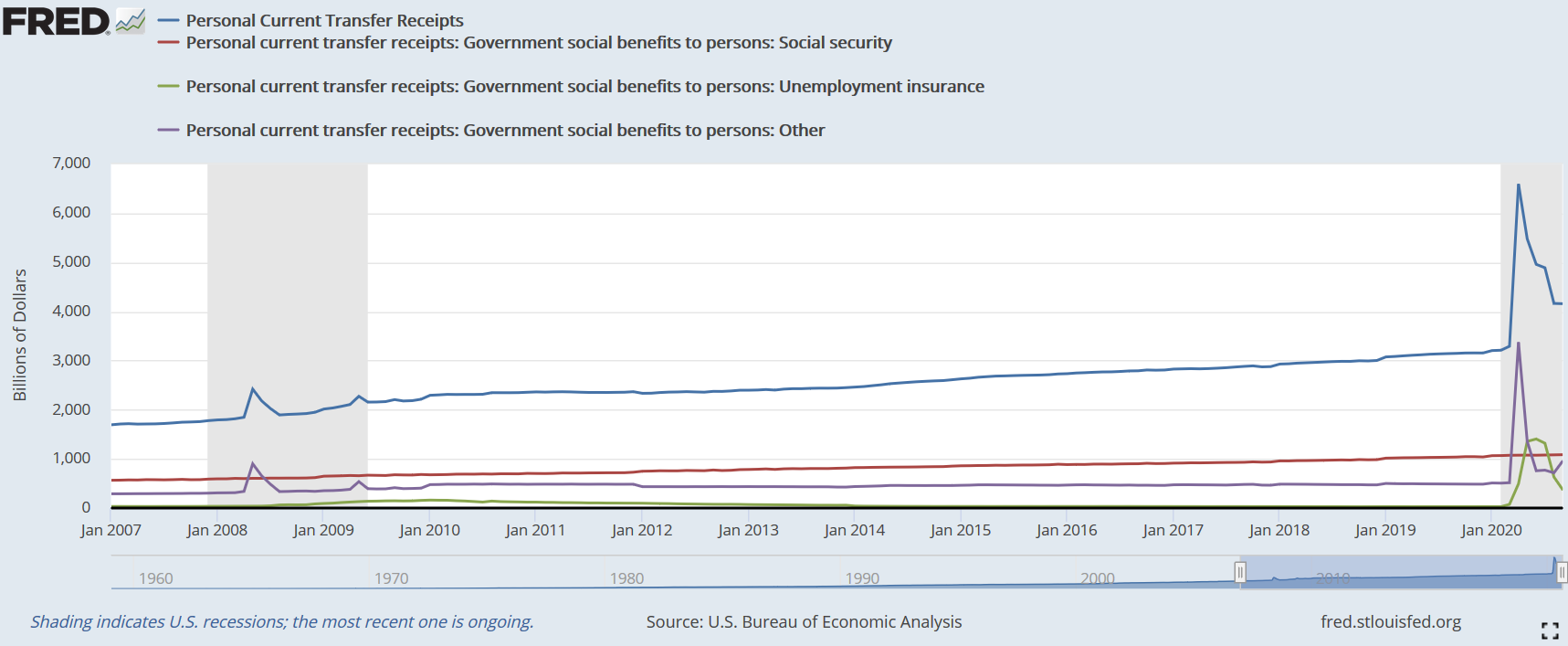

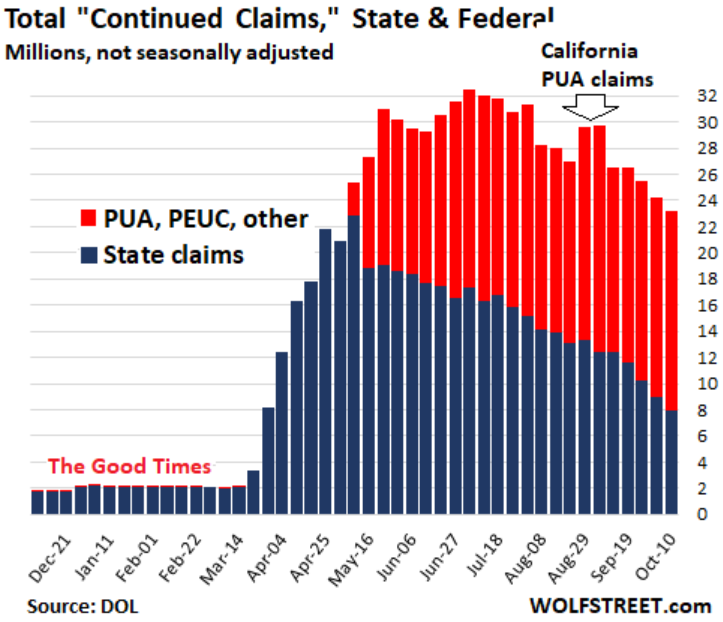

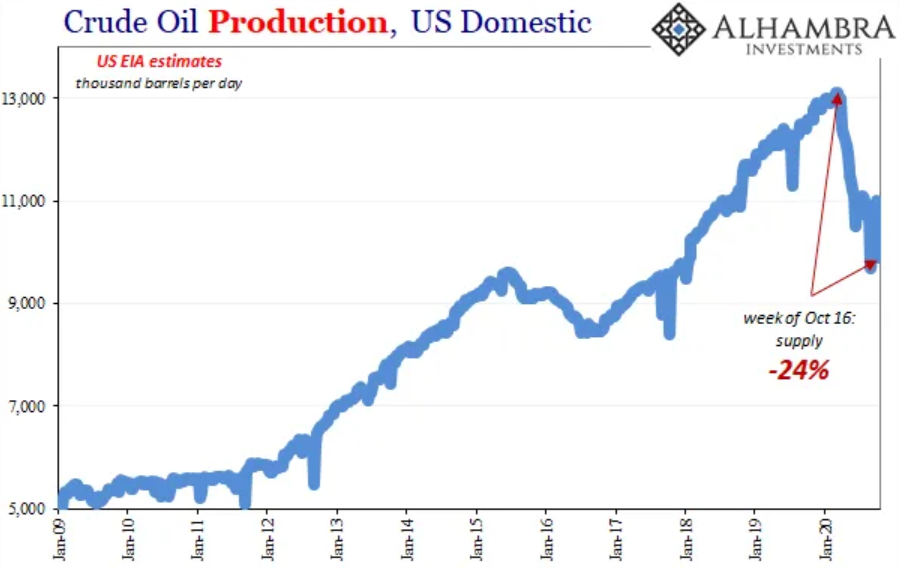

Surprisingly to some, the third quarter GDP growth was a record-settler, with an annualised rate of 33.1%, in relation to the previous quarter, beating the 32% consensus estimate. So, the V-shaped recovery is in the house! Or is it? Let's dig deeper. Firstly, the US (and global) economy is still climbing out of the huge hole brought about by the hysteria-induced economic shutdown (see chart below). Although the gap from the 2019 Q4 peak is a seemingly minute 3.48%, this means the rift is actually colossal. To get some perspective, the trough of the Great Recession, which arrived at Q2 of 2009, had 3.98% less output than the last quarter of 2007, in real terms. Hence, the current respite of activity is comparable to what was till this year the worst economic contraction of the post-war era, and we are supposed to be happy? As you are going to see, there is no reason to be happy or bullish.  In Europe, the situation is just as delusional as across the pond. The third quarter yielded a record-breaking QoQ rate of 12.7% for the whole Euro Area. Notwithstanding, compared to 2019 Q4, real GDP is trailing 4.29%, as the next graph depicts. Again, to get some perspective, from peak to trough, the output on 2009 Q2 was 5.65% less than the 2008 Q1's level. Thus, no reason to be optimistic too.  Getting back to the States, what were the factors that led to this outstanding GDP growth? The surge in growth was mostly driven by personal spending, which climbed an annualised 40.7%, also a record, while business investment and housing also posted strong increases. Looking at the data breakdown, the third quarter increase in real GDP reflected increases in consumer spending, inventory investment, exports, business investment, and housing investment that were partially offset by a drop in government spending. Moreover, imports, a subtraction in the calculation of GDP, surged. Interestingly, the uptick in consumer spending reflected increases in services (led by health care) and durable goods (led by motor vehicles and parts). Basically, due to the paranoia spurred by the kung-flu, people who were in need of some kind of healthcare simply postponed their appointments and treatments, either because they were forced to or they pussied out. Regardless of the reason, the hospitals and other medical facilities spent the last trimester cleaning the backlogs that surely appeared insurmountable Similarly, seeing that COVID-19 installed in the collective psyche the moronic fear of human contact and even proximity, it is no wonder nobody wants (even more so now) to commute on public transports, where there is hardly any chance of (anti-)social-distancing. As a result, auto sales had a much needed hike. Obviously, this personal consumption strengthning is to all intents and purposes rather impressive considering the massive contraction that preceded it. However, taking the terrific amplification of the Disposable Personal Income (DPI; second graph below) into consideration, one would think the typical American shopper had become as thrifty as Warren Buffet or Scrooge McDuck.   On the one hand, the first of the next couple of graphs shows that the DPI increment did not come from productive sources. Despite rebounding stupendously from the Spring lows, wages and salaries have been losing momentum. This is not good sign for the V-shaped recovery narrative. In fact, it foreshadows a prolonged recovery or even a "double-dip". On the other hand, one can clearly see that the DPI surge on Q2 and Q3 resulted from government transfers, in exclusive and in most terms, respectively. Specifically, the component "Other", in purple, is the main factor for that increase in income. The Coronavirus Aid, Relief, and Economic Security (CARES) Act signed into bill on March 27, created a bunch of programmes, totalling $2.3 trillion, to stimulate the economy and alleviate some financial woes that families and businesses were beginning to experience. Among these, there were: direct payments to families of $1,200 per adult and $500 per child for households making up to $75,000, on a yearly basis; the Federal Pandemic Unemployment Compensation (FPUC), which provided a federal benefit of $600 a week through July 31, 2020; the Pandemic Unemployment Assistance (PUA) that extends benefits to the self-employed, freelancers, and independent contractors; and the Pandemic Emergency Unemployment Compensation (PEUC), which extends benefits for an extra 13 weeks after regular unemployment compensation benefits are exhausted. In aggregate, these extra joblessness compensations add up to roughly $253 billion, while the direct payments totalled almost $300 billion. In addition, the law appropriates $349 billion, on the Paycheck Protection Programme, to be used to support small businesses to maintain their payroll and some overhead expenses through the period of emergency, with the goal of keeping workers paid and employed during the period of the emergency. Likewise, the cash grants of $25 billion for airlines (in addition to loans), $4 billion for air cargo carriers, $3 billion for airline contractors (caterers, etc.) aimed for payroll support. Finally, one can make the case that the $500 bn in loans for corporations, the $150 bn to state and local governments, plus the over $130 billion to hospitals, health care systems, and providers, had the objective of thwarting the monumental lay-offs and furloughs that were occurring - it turns out it failed to follow-through.   As a possible harbinger of what is to come - or is already coming - the "Other" component above is rising, even though most of the CARES Act programmes have been fully exhausted. The chart below, depicting the evolution of the different claims at state and federal level, indicates that although state claims are falling rapidly, the extraordinary joblessness benefits brought by the CARES Act are increasing in demand. Therefore, the continued (state) claims are plunging only because the recipients are exhausting their eligibility (each unemployed person has the right to receive unemployment insurance up to 20 weeks). Then, since they still cannot find a job, they move over to the federal level for the unemployment compensation. As a reminder, the PUA and the PEUC are going extint by the end of the year. These people ought to pray for the economy to get back to pre-pandemic levels as soon as possible so as not to fall further behind and get under even more financial trouble. Alternatively, - as we shall see after next Tuesday - the 2021 Republican-controlled Congress and federal government could easily pass a CARES Act 2.o to keep the debt indulgence on forever and ever... until it finally breaks.  Finally, one can claim with profound confidence the prospects for the quick V-shaped recovery are definitely naught. Like I showed on the last post, both banks and more importantly the UST market are signaling the rebound that just took place during the Summer is rolling over. Even before the resurgence of the kung-flu in the Northern hemisphere, which started as Autumn was as well, the economy was turning sour once more from late August or early September, as the bond and stock markets, as well as the dollar, portray. Besides, the oil market, which is a pretty good indicator of economic activity, is flashing ominous warning signs of reduced economic activity. Since late August, the price of the benchmark WTI crude oil has plummeted, returning to early June levels, when the lockdowns and other restrictions were being lifted. The price drop becomes even more impressive once you factor in the 24% production tumble of US oil.   Owing to the madness of our rulers, for insisting on fearmongering and utterly useless movement restrictions and lockdowns, they are turning this already horrendous economic debacle into an epic catastrophe that will result in millions of casualties worldwide, which effects will be felt for many years.

In other words, one of the biggest crimes against humanity is happening right now. Thus, we have to throw a monkey wrench to the global tyranny machinations and make the narcissistic sociopaths in the seats of power sit, instead, in a Nuremberg-style trials. Honestly, those who remain silent and obey these despots should consider themselves lucky as to only getting a slap on the wrist. What picture do all these factors paint? An extremely bleak and disturbing one. In spite of these impressive figures, the day of reckoning is undoubtfully coming. Everybody has just been delaying the inevitable. In addition to all the benefits and compensations, loans and grants mentioned above, moratoriums, frozen evictions and the belief this setback is an ephemeral nuisance easily curbed by fiscal and monetary stimuli were the reasons that made the economy rebound and postpone its inescapable collapse. In order to continue turning a blind eye to the laws of economics, the governments and central banks will throw everything they got out of pure desperation, though it will either ultimately not be enough, too much or completely irrelevant (the latter in the case of monetary policy).

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed