|

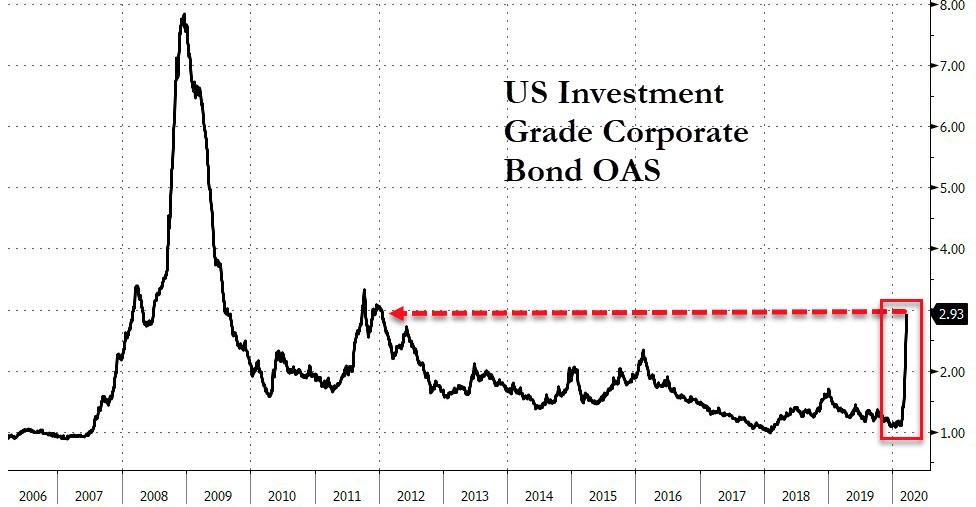

On The dollar standard epic finale, I explained that the current downturn will give rise to increasing debt-to-GDP ratio, which ultimately will lead to a sovereign debt crisis. The US government's response will likely be to monetise the debt, resulting in a currency crisis. In today's post, I am expanding in more detail on the dynamics that may cause the dollar to collapse, taking every other fiat currency with it. To wit, I am taking a closer look at the money and the credit markets debacle that is happening before our very eyes. To begin with, let me shed some light on these markets. The money market involves the purchase and sale of large volumes of very short-term debt instruments, such as overnight reserves or commercial paper. Some of the types of instruments used are certificates of deposit, eurodollars, commercial paper and repurchase agreements (repos). Furthermore, the credit market refers to the market through which companies and governments issue debt, such as investment-grade and junk bonds, commercial paper, notes and securitized obligations, including collateralized debt obligations (CDOs), mortgage-backed securities, and credit default swaps (CDS). The repo market is an overnight lending money market, where financial institutions sell US Treasury securities, a.k.a. Treasuries or UST, and other securities deemed low risk to other institutions, with an agreement to purchase them at an agreed price and date. Moreover, the commercial paper market is for buying and selling unsecured loans for corporations in need of a short-term cash infusion. Only highly creditworthy companies participate, making it a low risk instrument. Moving on to the matters on the table. In September, inefficiencies in the repo market became apparent. The overnight repo rate, which is supposed to stay in line with the Fed funds rate, shoot up to around 7%, when the Fed funds rate was at the 2-2.25% interval. This episode became know as the Repo-calypse and it demanded the Fed to intervene in the repo market, for the first time since the 2008 Global Financial Crisis (GFC). According to the Fed, although this was expected to be temporary, it is still going and becoming worse by the day. This is being provoked by a lack of collateral and increased counterparty risk. The financial intitutions have been searching for liquidity, yet they are short of "good quality" UST. Thus, for one party to accept to take inferior collateral, the returns must be greater, hence, the higher repo rate. The ongoing repo operations by the Fed, besides indicating the lack of superior collateral, could be pointing out the increasing intability of the financial system and the rising insolvency risk of the banks, hedge funds and other intitutions. Likewise, these two aspects are contributing to the liquidation of everything, from equities and bonds to gold and silver, to cover expenses and margin calls. Over the last 4/5 weeks, problems have emerged in the credit market. Firstly, the spreads between corporate bonds, investment grade and high yield (look at the two graphs below), and Treasuries have been growing wider, leading to a spate of insolvencies in the corporate sector and investment funds, as well as losses on collateralised loan obligations (CLO) held by the banks on a systemically threatening scale. Secondly, the commercial paper market began to freeze . Investors started to demand a bigger return to lend to corporations, causing the rates to spike, which means it became more expensive for corporations to borrow through this instrument. Accordingly, corporations are using other means that are draining liquidity from the money market. On the one hand, corporations that have cash at their banks will draw it down, forcing the banks to go into the money market, either through the international interbank market or the repo market, to make up the balance, sell government bonds, or foreclose on borrowers. On the other hand, corporations that do not have cash will test their working capital facilities, likely to force their banks to cover increased lending in wholesale money markets. Where banks experience drawdowns on both sides of their balance sheets, outstanding bank credit contracts, sending the sort of signal that terrifies central bankers. The situation will be increasingly reflected by central banks having to backstop both liquidity and bank reserves through repos and new rounds of quantitative easing. In an interesting paper, Zoltan Pozsar of Credit Suisse describes the process that leads to what he terms deficit agents in supply chains (businesses experiencing payment failures) turning their banks into deficit agents as well. Pozsar demonstrates that a reluctant Fed will have to backstop not just soaring domestic dollar deficits but global ones as well, and he assumes for the purpose of clarity that foreign central banks will manage the payment crises in their own currencies.

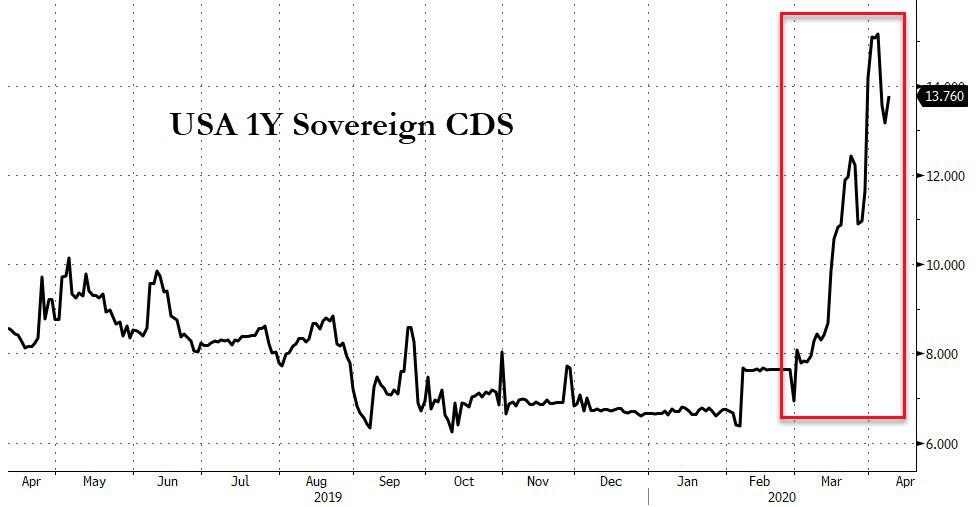

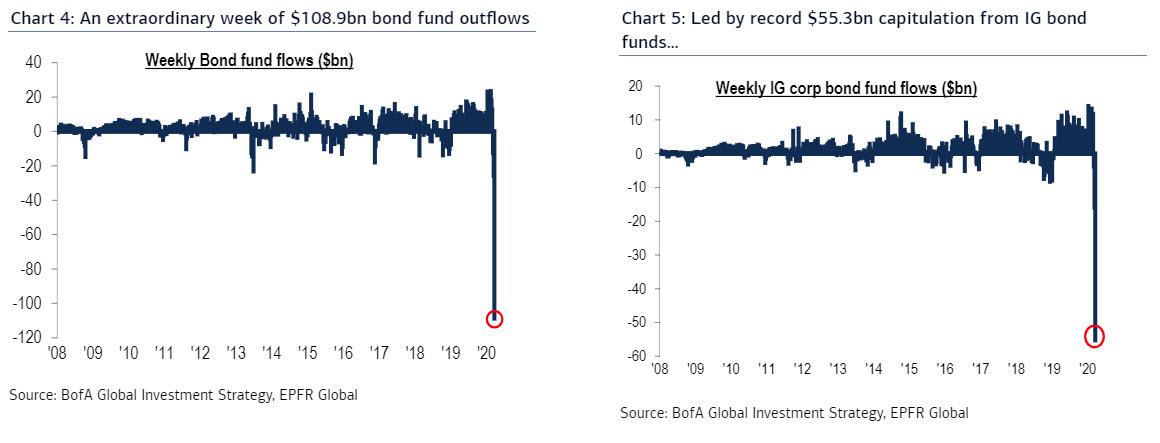

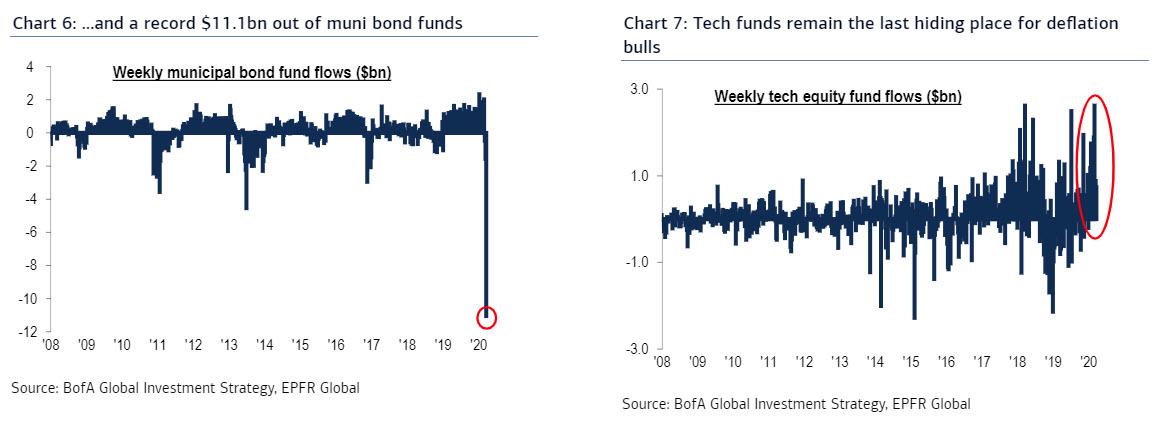

In addition, US hedge funds have ventured in enormous quantities of fx swaps to strip out interest rate differentials between euros and yen on one side, and the dollar on the other. Now that the Fed is closing down the rate differential by cutting its funds rate these arbitrages need to be unwound, leading to substantial liquidation of USTs and dollars to repay obligations in euros and yen. This will put significant downward pressure on the dollar. Furthermore, a reduction in outstanding derivatives will be the consequence of banks freeing up liquidity in desperation for their own balance sheets. The cost of hedging risk will increase significantly and in many instances become unavailable. Hedge funds and the like will be forced to restrict their activities, raising the possibility of widespread losses and potential failures in financial markets. Moreover, foreign governments will also be liquidating Treasuries to obtain dollars to satisfy their liquidity demands. As of now, Treasuries are still regarded as safe havens. However, when investors realise US insolvency risk is rising (look at the graph below), the safe haven status will fall. In any case, foreigners are getting the dollars they need via other means. One of those is the dollar liquidity swap lines between the Fed and foreign central banks. The Fed has had agreements in place since 2013 with 5 other central banks: ECB, Bank of England, Bank of Japan, Swiss National Bank and Bank of Canada. Yesterday, the Fed announced temporary dollar liquidity swap lines with 9 more central banks in Australia, Brazil, Denmark, Mexico, New Zeland, Norway, Singapore, South Korea and Sweden. It will not be long for them and others to lose faith in the Treasury creditworthiness. Additionally, foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. Nations with dollar-centric supply chains in their domains, such as China, South Korea or Taiwan, will probably have to unwind their long-dollar fx swap positions and sell Treasuries in order to release the necessary liquidity.  On top of that, US hedge funds and foreigners getting rid of dollars to get euros and yens, and to pay their dollar obligations, respectively, results in the reduction of the money supply, i.e. broad money. Specifically, it is the bank credit that contracts. Therefore, the Fed will have no alternative but to expand the base money to compensate the waning bank credit. The Fed will act this way because they have bought Irving Fisher's, Milton Friedman's and Ben Bernanke's description of how contracting bank credit led to the Great Depression. Up until a month ago or so, the 2020 budget deficit was estimated, by the CBO, to be around the 2019 figure of over a trillion dollars. This estimate seems ridiculously optimistic now. The Director of the National Economic Council, Larry Kudlow, is expecting to spend 2 trillion dollars in a stimulis package. With a stagnant or even declining (most likely!) economic activity, the fiscal revenue will not follow the growth in government expenditures. This means the budget deficit could reach $3 trillion and, consequently, the national debt may hit $26.5 trillion. For the sake of argument, the GDP for 2020 will remain the same as last year, $21.2 trillion, which renders the debt-to-GDP ratio at 125%. Thus, the Treasuries will not attract investors at the present low yields - the insolvency risk demands higher yields-, leading to Treasuries selloffs. In order to allow all that government spending, the Fed will have to absorb not only the newly issued debt but also the Treasuries sold by foreigners. By doing so, the Fed will end up ballooning its balance sheet by many trillions. As of now, the assets on the balance sheet amount to $4.3 trillion, aproximately, and by the end of the year it could be double that. Otherwise, if the Fed chooses to protect the value of the dollar, the debt is not monetised, wreaking havoc on the government's finances. In addition, it is not only the US banks which are in trouble. A glance at their share prices confirms that major European banks have long been at severe risk of failure, a fact which has been concealed by the ECB’s provision of liquidity. If nothing else, a new escalation of non-performing loans brought about by the coronavirus now threatens to collapse Italian, French, German, Spanish and other Euro Area members’ commercial banks, despite the ECB’s efforts. Hence, bailouts of Euro Area banks are on the cards. As a result, this will likely lead to widespread liquidation of euro commitments for speculation and arbitrage. Loans in the trillions have been taken out in euros as the counterpart in fx swaps to the dollar. As these positions are squared the euro will rise and the dollar will fall, transmitting a Euro Area banking crisis into liquidation of UST-bills and short-term US Government coupon debt by US hedge funds. A heightened risk of counterparty failure in fx swaps could spread to other derivative markets, requiring bailouts of non-banks, including major hedge funds. Furthermore, base money will be increased substantially to offset a contraction in bank credit and to give banks extra liquidity to compensate for becoming deficit agents as supply chains dislocate and retail sales of non-essentials goods and services collapse. On March 17, the Fed announced a Primary Dealer Credit Facility, with backing from Treasury. This facility will offer overnight and term funding with maturities up to 90 days. It became available for at least six months from March 20, at an interest rate equal to the discount rate, which was lowered to 0.25% on Sunday, as part of the central bank’s emergency action. This kind of measures are set to escalate. As a result, a coordinated G-20 global bank rescue scheme involving open-ended monetary expansion by central banks is likely to be instigated, in a widespread act of currency inflation. In respect to the fiscal stimuli, helicopter money is already being used in Hong Kong, where each citizen is receiving HK$10,000. Likewise, the US followed Hong Kong's lead and has commited to offering two tranches of $1,200 to every adult. There are also other expedients, such as deferral of tax payments and business rates to help provide liquidity, which will shift to governments some of the deficits building up in businesses. Mortgage payment holidays are offered in some countries. Helicopter money is already being provided to investors through share support operations, such as the Bank of Japan’s purchases of ETFs, which is likely to be expanded, and the ECB's €750 billion Pandemic Emergency Purchase Programme (PEPP) which commits to buy private and public sectors' securities. A few days from now, I am sure the Fed and US government is going to announce something along these lines, like buying corporate bonds, as has already been suggested by Ben Bernanke and Janet Yellen. Regarding the US, all of this stimulus is going to be financed through debt, which in turn will be monetised, diluting the dollar. A declining dollar will increase portfolio liquidation pressures on foreigners, leading to indiscriminate offerings of Treasuries, agency debt and equities (look at the graphs below). The Fed will have to take on not only the financing of an increasing budget deficit, but also absorb foreign sales of dollar-denominated securities (not just USTs), if it is to retain control of prices.   Accordingly, this is set to devastate the repo market. As you know, this market has become increasingly illiquid in part for lack of "good quality" collateral, USTs. As the public debt jacks up, the outstanding Treasuries carry on swelling because there are new ones being issued. In spite of the accruing "good quality" collateral, i.e. Treasuries, financial intitutions will continue to find difficulties in getting funding due to USTs losing quality. Therefore, the Fed will have to keep on backstopping this market through the repo operations, debasing the dollar even further. We have already seen daily repos by the Fed increasing from about $40 billions in recent weeks to between $130 to $200 billions currently.

In addition, so as to help keep credit flowing to corporations, the Fed came up with an emergency lending program on March 17. With the approval of the Treasury, the Commercial Paper Funding Facility was established. The Treasury will provide, through the Fed, $10 billion to a special-purpose vehicle that will purchase commercial paper from eligible companies, and purchases will last for one year, unless the Fed extends the program. As the title of this post claims, the Fed has painted itself into a corner. By providing an insanely cheap amount of liquidity, via zero interest rate and QE since the GFC of 2008, the financial system developed to a ridiculous size when compared to the economy as a whole. Because of the COVID-19 shock, the daisy chain of financial engineering is starting to come apart. Thus, the Fed and the US government have to support the financial system, intervening in each and every market. In doing so, the Fed has to ultimately devalue the dollar, putting the trust and faith in this debt-based monetary system, the dollar standard, at risk of collapse. At this stage it will become increasingly obvious to investors and domestic bank deposit holders as well that the dollar’s purchasing power is being destroyed by the Fed’s escalating asset support commitments. In effect, the Fed will be the only significant buyer of financial assets, paid for through quantitative easing on a far greater scale than what followed the GFC. Ergo, the dollar crash will bring the Treasuries and the entire financial system down with it. With the dollar as the world’s reserve currency and nearly all other fiat currencies having taken their cue from it since the Nixon shock in 1971, they also seem doomed to failure with the greenback. To conclude, this is the beginning of the end for the pervasive keynesian influence on the economic affairs of every realm, the monetary, the financial and the political ones, as well as at the individual and institutional levels. The preposterous fiat currency experiment is about to crumble. Obviously, the keynesians are not going to simply throw the towel. Being very sure and proud of themselves, they will stay the course. Accordingly, the central banks will either ramp up QE or implement negative rates, as discussed in the previous post. Only afterwards, will an economic system be erected on the pillars of a sound monetary system, based on gold.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed