|

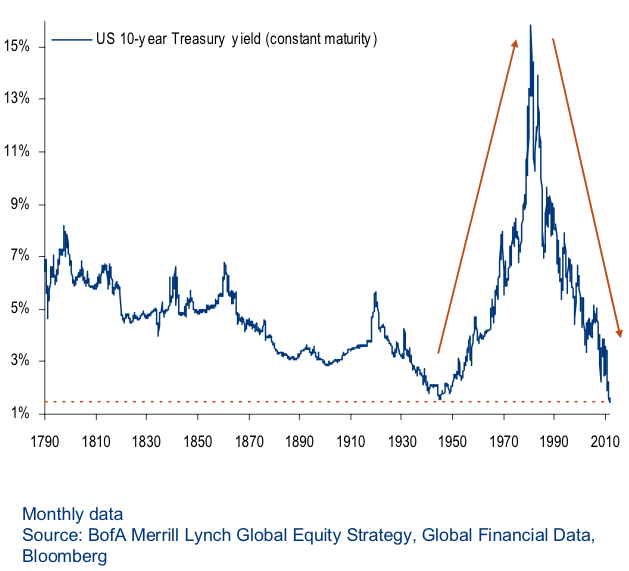

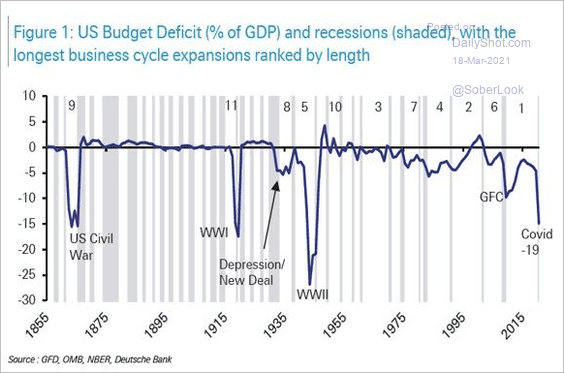

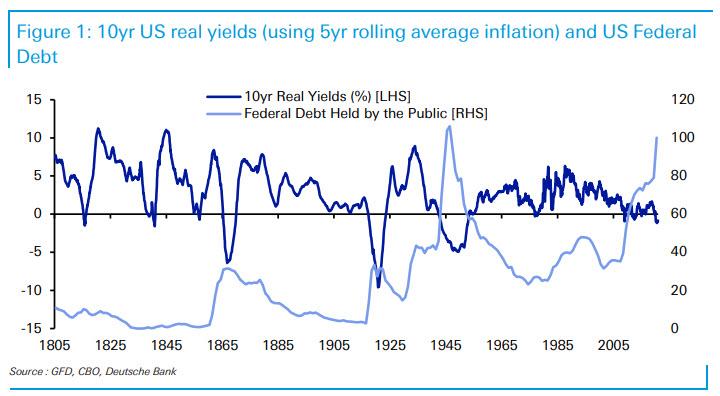

Resuming this two-part series, after describing the primary features of the ABCT, I am now going to dwell on the secondary ones, as well as the role of government, finishing off with the proper course of action. Accordingly, some secondary features may develop. One of them is the deflationary credit contraction, although it is not a certain condition throughout a bust. The contraction phase begins with the end of the inflation, as you saw in the first installment, and can carry on without any further changes from the monetary camp. Nevertheless, deflation has almost always set in. Undeniably, after bankruptcies and financial woes amongst borrowers pervade the economy due to the excessive credit creation, the money supply starts to contract. However, there is no need for deflation to arise. Understandably, it is often posited that seeing that entrepreneurs can find few viable projects in a depression, business demand for loans plummets and, consequently, loans and money supply will shrink. Regardless, this argument overlooks the fact that banks, if they are willing, can purchase securities, thereby sustaining the money supply by increasing their investments to compensate for dwindling loans. Needless to say, this condition brings about some important implications that I am going to elucidate afterwards. Having said this, contractionist pressures always stem from banks and not from business borrowers. Be that as it may, the terrible economic landscape that is accompanied by widespread business failures could lead to questioning the banks' health and solvency state. Therefore, the money supply will decrease because of bank runs or "shadow bank" runs - like I showed previously. Even just the fear of such runs, owing to banks being inherently bankrupt in a fractional reserve system (or in sort of one), is enough for banks to tighten their positions. Furthermore, another common secondary trait of the bust is the surge in the demand for money. This "scramble for liquidity" as is frequently referred to, is provoked by three factors: i) people expect falling prices on account of the flagging economy and the emerging deflation, causing them to save more money and spend less, awaiting the drop in prices; ii) borrowers will try to pay off their debts, which are being promptly called by banks and other creditors, by liquidating other assets in exchange for cash; iii) the torrent of business losses and insolvencies makes businessmen wary of investing until the financial distress and the liquidation process cease. With the supply of money waning, and the demand for it rising, general falling prices are a consequent attribute of most busts, chiefly in its most gruelling stage. Notwithstanding, declining prices overall is precipitated by the secondary, rather than by the inherent, features of busts. In spite of regarding that the readjustments induced during the contraction phase should be permitted to unwind, almost all economists (not just the Keynesians) take the rather unfavourable view that the deflation and the general price fall that derives from it unnecessarily aggravate the severity of recessions. Despite that, this notion is incorrect for they have beneficial effects and definitely do not exacerbate the economic contraction. Firstly, on account of the general subside in prices, the demand for money can more easily be fulfilled because lower prices mean that the same total of cash balances have greater command over goods and services. As a result, the desire for increased real cash balances has now been satisfied. In the end, the demand for money will decline as soon as the liquidation and adjustment processes are finished. Once the liquidation is completed, the uncertainties surrounding the lousy financial panorama vanish and the scramble for liquidity terminates as well. So, a quick unhampered drop in prices, both in general (adjusting to the credit reduction) and especially in goods of higher orders (adjusting to the malinvestments of the boom), will speed up the recovery processes and remove expectations of further downturn. In defiance of prices waning as a whole, the important characteristic to note of the primary adjustments is that the prices of producers' goods plunge more rapidly than do consumer goods' prices. Secondly, the deflationary credit contraction is tremendously helpful to the recovery processes in the accounting of companies. Considering that firms record the value of assets at their original cost, when prices increase altogether, what seems to be a large profit may only be just sufficient to replace the now higher-priced assets. During an inflation, business profits are greatly overstated, with consumption of capital being greater than it would be if the accounting illusion were not operating - perhaps capital is even consumed without the entrepreneur realising it. On the flip side, in a period of deflation, the accounting illusion is reversed since what seem like losses and capital consumption, may actually mean profits for the firm due to assets now costing much less to be replaced. By merely thinking that he is replacing capital, the businessman is in reality incrementing the investment in his company. Thus, this overstatement of losses encourages saving, while restricting consumption. Finally, credit contraction will have yet another beneficial effect in promoting the recovery. Since credit expansion distorts the free-market by lowering price differentials between stages of production (lower differences between selling prices and costs), the curtailment of credit, au contraire, mangles the free-market in the opposing direction by diminishing the amount of funds in the businesses' hands, distinctly in the higher stages of production. Specifically, in view of the demand for factors in the higher stages dwindling, factor prices and incomes follow suit, increasing price differentials. Ergo, it encourages the shift of factors from the higher to the lower orders. Despite being abhorred by most economists, credit contraction returns the economy to (true) free-market proportions much sooner than otherwise. The more the government intervenes to delay the market's adjustment, the longer and more gruelling the depression will be, and the more difficult will be the road to complete recovery. Government hampering aggravates and perpetuates the depression." What is then the correct course of action that governments ought to pursue? If governments wish to see the economy actually recovering, breaking the shackles of the deflationary constraints and return to the suitable productive structure that respects society's time preferences, as quickly as possible, the first and clearest prescription, albeit very broad and basic, is not to interfere with the market's correction processes. Basically, the more the government intervenes, aiming at curing the economic malaises of the bust, those much-needed corrections are simply deferred. As a result, the deflationary/disinflationary environment will linger for longer, hindering "the road to complete recovery". As a matter of fact, were we to list the several ways that governments can hamper market adjustments, we would find that we had precisely catalogued the favourite measures of curbing recessions that make up the governments' fiscal and monetary arsenals. To wit, here are the ways the adjustments can be hobbled: 1. Preventing or retarding liquidation by keeping the credit spigots open, such as putting up a credit facility or guaranteeing loans backed by government; 2. By inflating further, the necessary fall in prices, mainly in the higher order goods, is blocked, thus delaying the corrections and prolonging the recession. The expansionary fiscal policies carried out by profligate governments that resort to debt and the accommodative monetary policies of central banks, in case they are actual "money printers", preclude the required structural reshaping to beget the recovery; 3. Keeping wage rates up insures permanent mass unemployment. In addition, when prices are declining because of deflation, trying to peg the rate of nominal wages results in pushing real wage rates higher. In the face of plummeting business activity and, accordingly, demand for labour, this aggravates immensely the unemployment problem; 4. Keeping prices up, above their true free-market levels, will create unsalable surpluses and prevent a return to adequate and sustained growth; 5. Stimulating consumption and discouraging saving worsen the shortage of saved funds even further, which is of course not conducive to a speedy recovery, being in fact a colossal drag. So as to encourage consumption, governments can provide all kinds of "helicopter money" payments, from food stamps to "stimmy" checks. Conversely, it can discourage saving and investment by increasing taxes, particularly on the wealthy, on corporations and estates. In case you do not know, any increment in government spending will discourage saving and investment, while spurring consumption, since government spending boils down to consumption. Although some of the private funds would have been saved and invested, all of the government funds are consumed (or rather wasted). Therefore, any amplification in the relative size of government in the economy, among other consequences, shifts the societal consumption/saving ratio in favour of consumption, extending the recession; 6. Subsidising unemployment via "insurance" payments or any other welfare programme will protract joblessness indefinitely, deferring the reshuffle of workers to the sectors where jobs are available. It is indeed probable that more harm and misery have been caused by men determined to use coercion to stamp out a moral evil than by men intent on doing evil." To conclude, credit expansion sets into motion the business cycle in all its phases. Beginning with the inflationary boom, marked by the swelling of the money supply and by malinvestment, then the crisis comes into light when the credit origination ceases, exposing the malinvestments, and reaches its finale when the corrections of the production structure are carried out. Ultimately, the economy gets back to the most efficient ways of satisfying consumers' wants and needs. Nevertheless, there is one huge caveat. Seeing that in the real world governments always feel the urge to save the day and rescue its constituency from the distress that crises generate, mainly for the public wanting a paternalistic State, the recovery phase is always restrained. Hardly ever does economic activity recover swiftly from its trough, at the full potential growth of a true free-market regime. Hence, government interventionism with the mission of combating the downturn and restoring the upward trajectory of the economy as fast as possible, will emphatically have the opposite effect. Bearing in mind that the banks, while reducing loans to businesses during the crisis phase, they stock up on securities, because of liquidity preferences. As you know, in times of outright financial panic or just meagre growth, the most liquid, meaning the safest, assets are the most sought after. These assets happen to be the debt securities issued by the governments of the most predominant and developed economies, such as the US, Germany, Japan and so on. For that reason, the prices of these government bonds (and notes and bills) skyrocket due to being in high demand, causing their interest rates (yields) to plunge. Despite becoming more prevalent since the inception of the eurodollar system, with its Markowitz foundations, these processes have abided by these methods, vis-à-vis liquidity preferences, since long before then (as the next graphs demonstrate). Consequently, noticing the low cost of servicing their debts, governments feel compelled to act. Obviously, they cannot refuse this invitation of profligacy. How could they? It is simply too tempting. Thus, the adjustments required to bring about a rapid recovery will be inhibited.

Moreover, even though banks are able to trigger another boom by resuming their inflationary proclivities, if they perceive that economic conditions and their prospects are grim, they are not going to return to the prior "easy money" ways, owing to the outlook not being fitting to do so. Taking into account that banks are always looking for opportunities to lend to businesses in order to improve their profits, the fact that they refrain from doing so - the more governments butt in, the more they shy away from lending -, it really tells you a lot about the harm that government interference engenders.

Ergo, the best thing that governments can do is to essentially get out of the way and enact policies that adhere to the principles of laissez-faire capitalism. Fundamentally, let entrepreneurs find the best manners to satisfy the desires of the people, by getting rid of all kinds of arbitrary rules and regulations that erect barriers and hindrances which prevent the smooth functioning of the free-market system. To cap it all off, applying this philosophy to the banking industry and the monetary system, in general, is of the utmost importance to prevent the endless recurrence of the boom and bust cycle. On that account, only then can we grow and develop at the maximum rate imaginable, lifting along the way the standards of living at a pace never before witnessed. Above all, it would be done in a sustainable fashion, in view of conforming to the societal time preferences and the actual amount of savings. Otherwise, the governmental meddling acts as a tremendous drag on economic growth and all the things associated with it. Evidently, technological progress, social advance and rising living standards become gradually constrained. Therefore, the do-gooding politicians and technocrats that claim to know what is best for us, the commoners can very well, though unwittingly, turn a run-of-the-mill bust, a mere recession if you will, into a prolonged and dreadful depression.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed