|

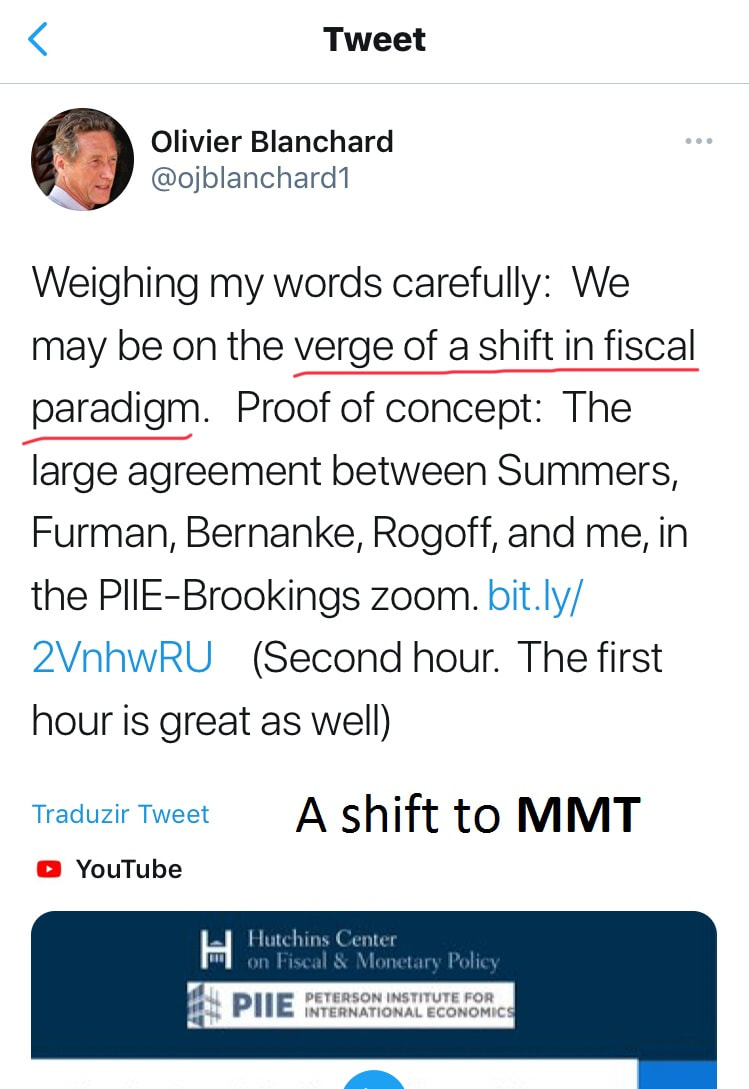

Following our theme introduced a couple of posts ago, I am going to demonstrate how mainstream economists, the supporters of Keynesianism, are providing the logical basis for more action and intervention on the part of the government, getting, in the process, closer and closer to the advocates of MMT (or, as I am calling them now, Knappers). Just how similar to each other are they? That is what we are going to find out. To begin with, the keynesian prescription for a recessionary trough is, in theory, to simply fill it in. To accomplish this, government spending - funded by borrowing rather than taxation - is jacked up so as to limit the economy's downside. In addition, the wizards at the central banks do their magic by, supposedly, keeping interest rates under control, or at least preventing them from spiraling. Notwithstanding, failing to spur the economy back to its previous vivacity, in a quick enough fashion, time becomes a serious problem. Basically, long-run economic damage crops up when hindrances emerge, taking the economic rebound too much time, or too much depth around the trough, which may harmfully reshape economic potential. By the same token, Larry Summers, the former Secretary of the Treasury for President Clinton, during a discussion sponsored by the Brookings Institution on December 1 - I know it is from a while ago, but I was saving it for a post worthy of such a gem -, affirmed that although "there are all kinds of mistakes that are made going into crises (...) among the most important things to do is to make sure we do not have a sustained period of slow growth". Nicely put! According to the paper presented by Jason Furman, former Chair of the Council of Economic Advisers for President Obama, that preceded the debate (if we can call it that), which was elaborated by him and Larry Summers, during contractions, fiscal expansions apparently lead to reductions in the debt-to-GDP ratio. Interestingly, it allegedly "works the same way in any country with high debt", which is corroborated by some fancy econometric models from the IMF or the OECD. Be that as it may, you know this is not true. Hence, the empirical evidence backing the usefulness and the necessity of increased government spending exists and it seems to be almost consensual. This sounds like terrific news for all of us, in terms of recovery prospects. Resuming the presentation of his paper, Furman stated that "demand (…) is something that we are concerned about even in normal times. The interest rate that might be required to absorb all of the savings might be an unattainable negative number. We need to gear the economy towards greater demand to prevent that slow growth in normal times [and] the risks associated with low interest rates". Typical keynesian reasoning: the government has to make up for the slack from the private sector. Nevertheless, he granted that low interest rates pose some challenges, which, since it is not crutial to this discussion, I am not going to dwell on. Despite that, once again, I am making Larry Summers words my own when he claimed that "there are good reasons, not certain reasons, for believing that an economy with a positive neutral real interest rate is going to be a healthier, safer, more productive and more financially stable economy than na economy with negative normal real interest rate". However, I will be departing from Summers from now on seeing that he posits, among other things, that "maintaining a posture of fiscal policy that permits a positive real interest rate is (…) in general the healthier strategy" - the "posture" he is referring to is an expansionary on, aiming at generating inflation. Continuing with that paper, the actions and policies that ought to be taken in order to boost aggregate demand are presented, setting the stage for the putative debate that followed between the authors of the paper, Jason Furman and Larry Summers, Ben Bernanke, former Chairman of the Federal Reserve, as well as Kenneth Rogoff and Olivier Blanchard, who are both former chief-economists of the IMF. A real who's who of Keynesianism. Before we get to that, however, I have to point out one last thing Furman said in his presentation. Talking about the automatic stabilisers, which consist of essentially unemployment insurance and other government handouts, he spouted "[this] is especially important in the United States, where the automatic stabilisers are relatively weak, largely because of the relatively small size of our government as compared to other ones". This is just a downright falsehood. By comparing the government expenditures' weight in GDP, you clearly recognise the US is in line with the major (and most productive) economies – in fact, you cannot make out any correlation between any government's weight on GDP and the respective country's level of development. All the same, this ridiculous remark sets the tone perfectly for the tête-à-tête that followed it. Since the purpose of this post is not to make an exhaustive analysis of the topics conversed about, I am going to highlight only the essential to get us going, although I strongly urge everybody to listen to this economics prattle. Firstly, in the middle of this colloquium, Ken Rogoff ushered in an interesting issue asserting they "do not understand why interest rates are so low [and why it] is a global phenomenon", he continued commenting that "[this] is not just about what the US debt is, (...) [there] is much more going on". To finish his intervention, he claimed to suspect, as Blanchard had before him, the boom in Asia was the greatest contributing factor for Ben Bernanke's "global savings glut". Adding to this hypothesis, Bernanke asserted to be "three key elements. The first is that demographics and rapid growth of the middle-class globally has greatly increased desired saving. Secondly, (...) to an historically unusual degree, the productive investments in the world are in the public sector, in our public goods, as opposed to private sector, which means that to finance them, you need to have fiscal borrowing capacity". Because the third point is sort of irrelevant for today, let me try to decipher what Helicopter Ben meant in his second point. Maybe Summers gave us the answer afterwards, postulating the (real) interest rate to be "a kind of measure of the risk-adjusted productivity of capital", which for being low "is telling you that [the] private investment that [the government crowds] out is not a very costly kind of investment to crowd out". In other words, investment in risky or simply riskier instruments and ventures is subdued, while the safest and most liquid securities are in super high demand. Therefore, how about you investigate why that is the case, instead of immediately opting to request the government to come to the rescue. Regardless, the best was really Furman: "In some sense, we do not need to know exactly what caused [low interest rates]. Was it a global savings glut, was it inequality, was it demography, etc? The important threshold question is how likely is it to continue?". The utter stupidity of these people never ceases to surprise me. How can you know the likelihood of this to persist, if you do not bother to look for the cause? Thank God these imbeciles are not engineers or medical doctors. Just call Uncle Sam and Oma Merkel and they will solve it. Moreover, Furman concluded by defending that "[because] it was gradual across a range of places, (...) your best guess is it will continue. Then, we can debate why it is and again that is a best guess". Let me take a guess then. How about the government? Maybe this is the reason they are so reluctant to examine thoroughly. Bearing in mind Bernanke's first point (about the global savings glut), supposing, for the sake of argument, savings have been building up over the last decade (perhaps, for much longer than that), entailing that consumers are putting aside more of their income on the sidelines. For some reason, these economists believe that there is an almost fetish-like yearning for low-yielding government. So much so, people apparently do not mind earning at most a couple of pennies on the dollar or, in the case of Europe and Japan, pay these nations' governments for the privilege of being one of their lenders. Secondly, to tackle what Larry Summers called "secular stagnation", according to Blanchard, we have "to increase demand, private demand, and the most natural way of doing it is fiscal deficit. (...) It seems to me social insurance and (...) if we provided health care [in] the US, if we basically had tuition-free college education [and] all kinds of things like this, this would make a fairly major difference to a private savings rate". So, budget deficits and something about private savings - is anyone else getting this sense of déjà vu? Having said this, he wants the government to take care of these nuisances, regarded (by most, hopefully) as individual responsabilities, by extending even more support in these areas or outright collectivising these services. In addition, infrastructure projects are to be under consideration, which was mentioned in the paper and proposed by Rogoff to boot. How about an anti-extra-terrestrial defense mechanism, as Paul Krugman once proposed. As Summers went on to affirm, "we have the paradigm shift to the view that having a fiscal policy that absorbs all the savings and maintains demand, (...) therefore we get to full-employment". To sum up, get the government to do anything they can, even if that means changing the constitution, to make people focus all their attention and resources solely on consumption - they are, after all, consumers. Thirdly, due to presumably being fact-driven, if these keynesians take these positions is because the data compels them to take them. According to Rogoff, "there is a lot of evidence now that higher debts [are] associated with lower growth , but (...) emphasis is that, [otherwise], maybe interest rates [would be] even lower and, so, who cares?". Who says interest rates could be even lower? Oh right, the econometric models. Furthermore, to Summers, Japan has been a success, so the story goes. "In fact, Japan has got lower unemployment, has done very well in terms of per capita output, relative to the rest of the world, and the reasons have to do with (...) expansionary fiscal policy". In spite of Bernanke conceding fiscal policy to be the "go-to [automatic] stabiliser", he doe not seem to concur with Summers on account of believing that with effective fiscal expansion, "interest rate will go up, inflation will go up", which has definitely not occurred in Japan for the last three decades. Of course, Rogoff would simply reply that, otherwise, if nothing had been done, interest rates and inflation would have been even more subdued. Finally, we are reaching the focal interest of today's subject. In the opinion of the former Fed Chairman, "monetary policy has actually been, in the United States at least, pretty effective in the last couple of years". To Bernanke, the Fed pivot in late 2018/early 2019, which meant cuts on the target of the federal funds rate, led the economy to full-employment. Albeit, he claims, an effective fiscal policy would render "monetary policy again more effective", because rates would rise and give more room for the central bankers to, supposedly, tackle an economic contraction. Ergo, the explanation for the declared success of monetary policy is that "it is run by a non-partisan, independent [and] professional organisation, which can respond quickly and sensitively". On the flip side, "fiscal policy is for political reasons (...) slow". You still cannot discern what he is hinting at? Fret no more, another member of the panel spelled it out for us. Moving on to Rogoff's view, for being unable to "get around the fact that it is political, (...) the question is (...) how much can you make it technocratic? (...) we read Larry and Jason's paper, it is very calm and logical and if they could be in charge, maybe things would run that way, but we have this very political system". There you go, admission at last. Two sides of the same coin, that is what the keynesians and knappers really are. Despite having some differences, these are not of the ideological kind, but mere technical ones. While the MMT-ers want the central bank and the Ministry of Finance/ Treasury to be one entity (at least in de facto terms) for the government to finance itself, for some reason, the keynesians defend their separation , arguing for central bank independence (for whatever reason). Moreover, the former thinks that knows what money is, while the latter cannot find it. To cap it all off, both factions' rationales may be put like this, quoting them once again, though this time is what they truly reckon, were they to have no filter: "since people in the real world refuse to act like they do in our models, we are just going to force them to act the way we want them to". Unfortunately, the public indulges them by regarding them as experts, whereas a common mortal is just a layman who knows nothing about econometrics. In conclusion, MMT is only a natural progression from Keynesianism. Or is it a regression, seeing that Knapp's State Theory of Money came out far before, four decades to be exact, Keynes' General Theory. Either way, considering that these two schools of thought have many followers, particularly the keynesian ones (the neo-Keynesian, the New Keynesian, the post-Keynesian, etc), across the globe, that dominate economics departments on the most prestigious universities, have the attention of lawmakers and the media, packing the most influential think-tanks like the Brookings Institution, is all you need know to admit that the Blob will carry on growing incessantly, unlike the economy, prompting ever more suffering and resentment as a result. God willing, and to end on a positive note, it is never too late to reverse course and embrace the ideals of liberalism and laissez-faire capitalism, which includes giving the technocrats the boot.  Finally, we are reaching the focal interest of today's subject. In the opinion of the former Fed Chairman, "monetary policy has actually been, in the United States at least, pretty effective in the last couple of years". To Bernanke, the Fed pivot in late 2018/early 2019, which meant cuts on the target of the federal funds rate, led the economy to full-employment. Albeit, he claims, an effective fiscal policy would render "monetary policy again more effective", because rates would rise and give more room for the central bankers to, supposedly, tackle an economic contraction. Ergo, the explanation for the declared success of monetary policy is that "it is run by a non-partisan, independent [and] professional organisation, which can respond quickly and sensitively". On the flip side, "fiscal policy is for political reasons (...) slow". You still cannot discern what he is hinting at? Fret no more, another member of the panel spelled it out for us.

Moving on to Rogoff's view, for being unable to "get around the fact that it is political, (...) the question is (...) how much can you make it technocratic? (...) we read Larry and Jason's paper, it is very calm and logical and if they could be in charge, maybe things would run that way, but we have this very political system". There you go, admission at last. Two sides of the same coin, that is what the keynesians and knappers really are. Despite having some differences, these are not of the ideological kind, but mere technical ones. While the MMT-ers want the central bank and the Ministry of Finance/ Treasury to be one entity (at least in de facto terms) for the government to finance itself, for some reason, the keynesians defend their separation , arguing for central bank independence (for whatever reason). Moreover, the former thinks that knows what money is, while the latter cannot find it. To cap it all off, both factions' rationales may be put like this, quoting them once again, though this time is what they truly reckon, were they to have no filter: "since people in the real world refuse to act like they do in our models, we are just going to force them to act the way we want them to". Unfortunately, the public indulges them by regarding them as experts, whereas a common mortal is just a layman who knows nothing about econometrics. In conclusion, MMT is only a natural progression from Keynesianism. Or is it a regression, seeing that Knapp's State Theory of Money came out far before, four decades to be exact, Keynes' General Theory. Either way, considering that these two schools of thought have many followers, particularly the keynesian ones (the neo-Keynesian, the New Keynesian, the post-Keynesian, etc), across the globe, that dominate economics departments on the most prestigious universities, have the attention of lawmakers and the media, packing the most influential think-tanks like the Brookings Institution, is all you need know to admit that the Blob will carry on growing incessantly, unlike the economy, prompting ever more suffering and resentment as a result. God willing, and to end on a positive note, it is never too late to reverse course and embrace the ideals of liberalism and laissez-faire capitalism, which includes giving the technocrats the boot.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed