|

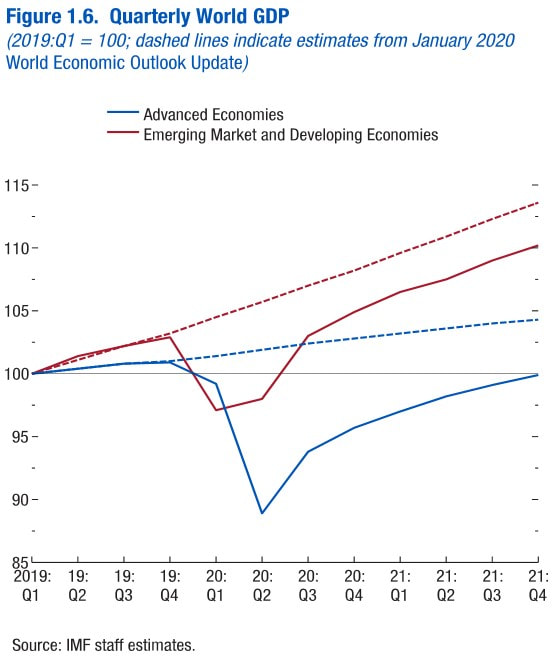

On 1850, french economist Frédéric Bastiat presented the world with his magnum opus, Ce qu'on voit et ce. qu'on ne voit pas, which translated to english is "What is Seen and What is Unseen". In this essay, Bastiat introduced the concept of opportunity cost - he did not named it that, this term was coined later - through the parable of the broken window. In this day and age of coronavirus-induced turmoil, it is of paramount importance to revisit the lessons taught by that parable. The parable seeks to show how opportunity costs, as well as the law of unintended consequences, affect economic activity in ways that are unseen or ignored. The resources spent on one or a few sectors are resources that cannot be spent on other sectors. Thus, the stimulus felt in one sector of the economy comes at a direct – but hidden – cost to other sectors. In addition, the COVID-19 has led the governments to grind their economies to a halt. At a first instance, the interventions pursued by the governments to combat the spread of the kung-flu are causing a collapse of the economic activity. On that account, to tackle this issue, governments are again stepping in, which is set to bring about a whole series of negative outcomes that will leave the economies at an even worse shape. Firstly, shutting down the economy, in order to prevent the coronavirus from spreading, is proving to cause far more harm to society than the virus, with the unemployment soaring worldwide and the global economy entering a depression not experienced since the Great Depression. According to the IMF in its April 2020 World Economic Outlook, the World GDP is going to fall 3% this year, in relation to 2019. In more detail, the Advanced economies will plunge 6.5%, with -5.9% for the US, -7.5% for the Euro Area, -5.2% for the Japan and -6.5% for the UK; and the Emerging markets and Developing economies will decrease only by 1%, with 1.2% and 1.9% increases for China and India respectively, -5.5% for Russia, -5.3% for Brazil, -6.6% for Mexico, -3.3% for the Middle East and North Africa aggregate and -1.6% for Sub-Saharan Africa.  Despite the IMF being prone to contrive optimistic projections that fail to materialise, this time it provides alternative dreadful scenarios for the evolution of the pandemic. Yet, they seem to be too hopeful. Seeing that the base case for the pandemic will almost inevitably cause this debt-based economic system to fall apart, if any worse scenario for the coronavirus evolution occurs, the collapse of the dollar standard is in the bag, prolonging the depression even further.  Additionally, the social implications of the economic lockdown are extremely dire. Individuals are losing their jobs and, consequently, their incomes. By having a more diminished wealth, their standard of living is going to be severily reduced. Hence, expenses on both healthcare and nutritious food are bound to drop, leading to shorter average lifetimes and higher mortality rates. To make matters worse, the social fabric will deteriorate tremendously, causing suicides and crime-pushed fatalities to skyrocket. Therefore, far more people, especially young and middle-aged individuals, will die because of the economic downturn than from the COVID-19.

At least the politicians know the shutdown of economic activity gives rise to the freezing of the cash flows for businesses and the income streams for individuals, as well as the complete standstill of credit origination, which is the bloodlife of this monetary and financial system. Accordingly, governments and central banks are compelled to meddle in their economies, which takes us to the way the well-intentioned policy makers are hampering the economic recovery. Secondly, so as to counter the economic debacle, the keynesian technocrats, especially at the Fed and the US Treasury, have been coming up with a more preposterous programme or policy after another. However, the bailouts for corporations, Main Street businesses and households, and the ever increasing liquidity injections to the financial system are precluding the malinvestments done post-GFC from being corrected. Furthermore, governments' actions could discourage people from looking or going to work due to overly generous unemployment benefits and other policies, such as the Universal Basic Income. As a result, inasmuch as the pool of potential workers shrinks and businesses and individuals continue to be constrained by high levels of debt, the output will struggle to get back to where it was two months ago. If individuals and businesses were allowed to go on default and on bankruptcy, the debt would be wiped out and, thus, the economy would grow much quicker for there would be less debt weighting on it. To add insult to injury, the maintenance of the status quo pursued by the governments, central banks and supranational institutions is impeding the distortions on the production structure from being rectified. There is a myriad of businesses that are only alive because of extremely cheap and easy credit. The so-called "zombie" companies can only get enough cash flow to pay their operating expenses and service the debt, but are unable to pay off the debt principal. These companies, for being unprofitable, they do not create value. In fact, the "zombies" are just the tip of the iceberg. As you become aware by reading the Austrian Business Cycle Theory section, the boom is prompted by a subdued interest rate that results in an unsustainable production structure that will eventually crash. In a real capitalist regime, interest rates are not manipulated by central planners. Instead, they are a function of savings and the time preference (learn more here). Therefore, if the interest rates were allowed to adjust by the free market, it would not be just the "zombies" to die at last, but several businesses would vanish or would have to restructure in order to survive. Only then could the economy grow sustainably, reflecting the pursuit of each individual's best interests. In conclusion, in both instances - policies to restrict the COVID-19 spread and interventions to tackle the economic issues aroused by those policies - the governments and central banks come to the rescue, the economy and society come out, nevertheless, in an even worse shape. By looking at protests that are starting to occur, like the one in Michigan, it seems people are beginning to wake up and realise that the governments' cure is worse than the disease.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed