|

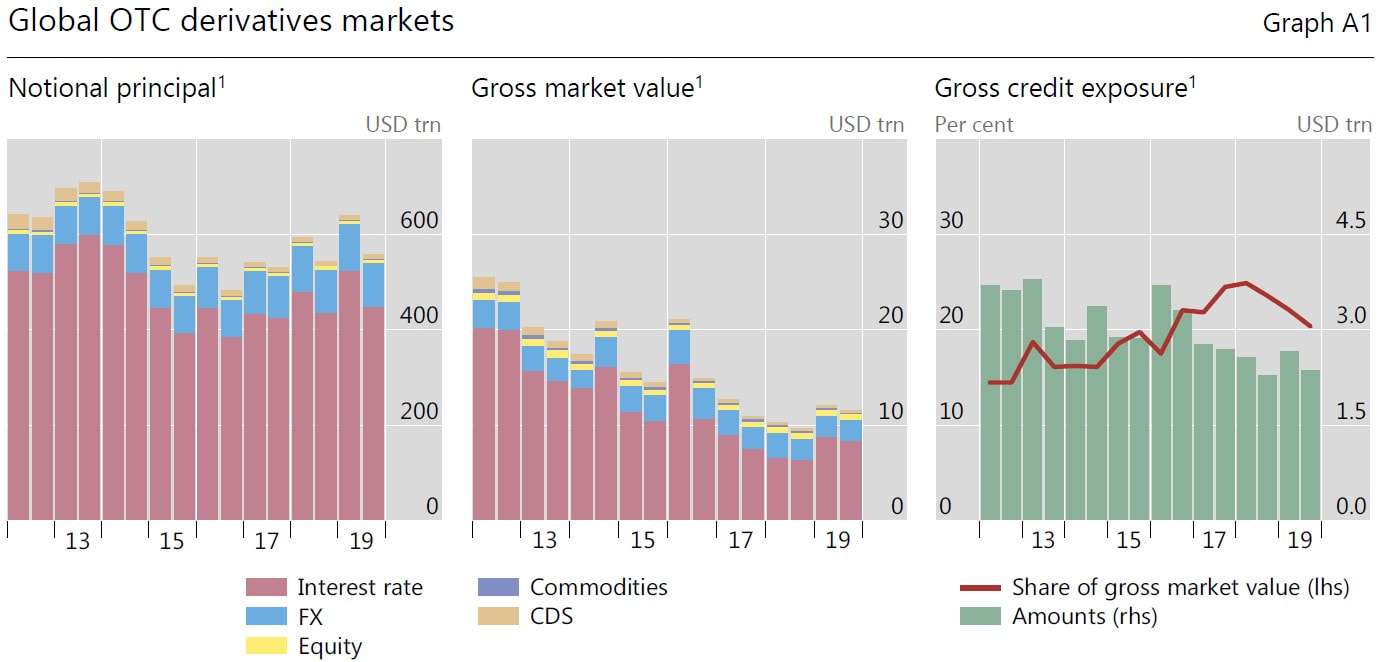

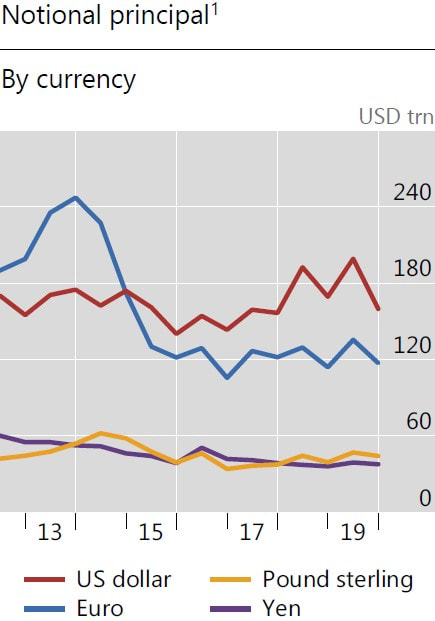

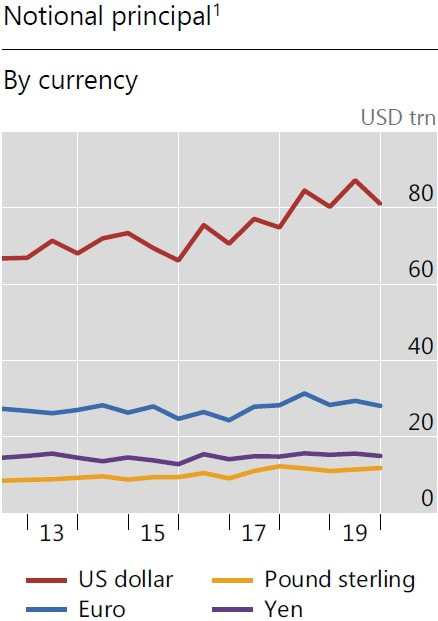

Continuing where we left off, even though the biggest enemies and "frenemies" of Uncle Sam have been planning to terminate or, at least, circumvent the dollar for roughly a decade, this task is proving to be much more tricky than anticipated. The implementation of trading agreements and payment systems are just the first and easy steps. The next steps are the ones which are going to be hard to follow through. The truth is that the international financial system, the Eurodollar, for being both complex and nontransparent, is making the culmination of the US dollar hegemony a herculean ordeal. In order to improve the system or move on to another one, the Eurodollar needs to be understood. However, how can we understand the issues underlying this system and, thus, come up solutions, if nobody knows its ins and outs. To add insult to injury, in any discussion about the economy and its problems, like the anemic growth, the swelling debt and so on, the Eurodollar is completely removed from the conversation and yet it is part of the root for all those evils. Accordingly, on this final part of this series, I am setting out to present the possible scenarios for the US dollar supremacy in the current conjecture, taking into account the actions of some countries and the resilience of the Eurodollar system. Despite being essential to overcome the American dominance, creating alternative transaction systems is not enough. To wit, China's Cross-border Interbank Payment System (CIPS), Russia's System for Transfer of Financial Messages (SPFS) and even EU's Instrument in Support of Trade Exchanges (INSTEX) have all been established with the purpose of circumventing the US-controlled SWIFT system. The INSTEX was established to transact with Iran without breaking the US sanctions. Until now, it used for humanitarian reasons only, such as the purchase of otherwise embargoed foods or medicines. The SPFS was created in 2014 owing to threats made by the US that Washington would disconnect Russia from SWIFT. This system is regarded as a last resort, rather than as a replacement for the SWIFT network, though it is being negotiated with other countries to expand across the border, like India, Iran, Turkey and China. Speaking of the devil, the CIPS, as it stands, is to be used only for cross-border yuan trade deals rather than including capital-related transactions. On 25 March 2016, CIPS signed an memorandum of understanding with SWIFT for deploying the latter as a secure, efficient and reliable communication channel for CIPS's connection with SWIFT's members. This would provide a network that enables financial institutions worldwide to send and receive information about financial transactions in a secure, standardised and reliable environment. Hence, SWIFT is a mere transaction network where members send messages related to payments and transfers, without the need for capital to move around. That is the essence of the Eurodollar system and seeing that there is a whole infrastructure and financial markets built around the US dollar, setting up an alternative network is insufficient. These other payment systems are only used as a recourse for whenever Washington blocks them from SWIFT. Having said that, we should revisit the definition of the Eurodollar system, which was presented in a previous post: "(...) the Eurodollar turned into a system of interbank liabilities that real economy participants were using, once they connected to it, in order to achieve real-world activities, as the Head of Global Research for Alhambra Investment Partners defines it. Additionally, it is a currency-like system based around the banks, scattered all throughout the world, which participate in it." Furthermore, it arose in the 1950's and grew quickly ever since because capital was not necessary. To actually have to count physical Federal Reserve notes or bars of gold were restrictions that the Eurodollar system did not want. On account of having capital flowing around, the transactions would be much slower and, therefore, this system would never come into prominence. For instance, there are two banks, one in London and the other in Shanghai, both connected by a network, SWIFT. The one in Shanghai needs to get some US dollars and gives as collateral a 10-year US Treasury. However, there is no currency or assets changing hands, only numbers in each other's computers. In short, they both have computer screens that are linked by a network, and if one's numbers come up the same as what the other's numbers say, then it is all good. Basically, the Eurodollar is a ledger system. In addition, dethroning the dollar is a very demanding task due to the logistics of the financial system. Inasmuch as the financial system comprises trillions upon trillions of derivatives with underlying dollar-denominated assets, these contracts would have to be rewritten and revalued, which would certainly generate a worldwide panic, most likely leading to a global economic collapse. By the end of last year, the outstanding notional amount - which determine contractual payments - of over-the-counter (OTC) derivatives totaled $559 trillion, while their gross market value - which provides a measure of amounts at risk – amounted to $11.9 trillion, according to the BIS. As you can see below, the OTC derivatives universe is mainly comprised of interest rate derivatives, like interest rate swaps, and US dollar-denominated contracts are the prevailing ones, adding up to $160 trillion at end-2019, or 36% of all contracts. Turning to foreign exchange (FX) derivatives, their notional amounts outstanding have risen steadily since the turn of the century. The US dollar is the primary vehicle currency, being almost always (around 90% of the time) one of the two currencies exchanged in FX swaps and forwards, with $81 trillion. Therefore, these figures, combined with the $3 trillion in equity-linked derivatives on US equities plus the other types of derivatives that are presumed to be mostly negotiated in US dollars, imply there are in the neighborhood of $245 trillion derivatives denominated in dollars, entailing the greenback is in the middle of roughly 45% of derivative contracts worldwide.

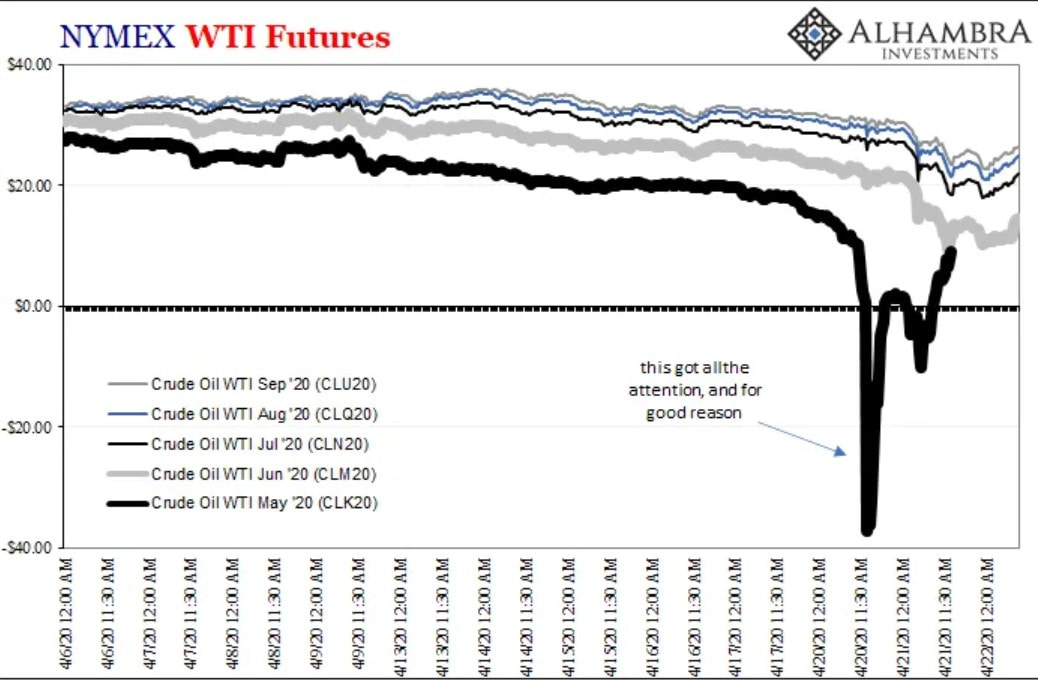

Moreover, that scenario of rewriting and revaluing contracts will hardly take place. As a reminder, the Eurodollar is a system of banks liabilities. If they have liabilities then they also have assets. These assets are not just loans. In fact, usually when a bank makes a loan the borrower has to provide some collateral, of which the more liquid the better. This is why the financial system is dollar-centric. The financial markets of the US are generally the most liquid of them all. Thus, in the realm of collateral, the US Treasuries are king. To this point, liquidity is the only thing that matters. Market participants perceive the dollar assets to be accepted by everybody in the world owing to the fact the dollar is the global reserve currency. Ergo, one thing led to another. The US dollar became the reserve currency, causing everybody to use and accept them, which helped give rise to the Eurodollar system. The ongoing development of this system due to the marvel of financial engineering led the American economy to be increasingly financialised. As a result, even if the dollar ceased to be the global reserve currency, for having this logistic support resulting in the most liquid assets, the Eurodollar, or the dollar standard, will keep on exerting its supremacy for the time being. Bearing the Eurodollar's resilience in mind, if anyone wishes to bring down the dollar standard, one could come to the conclusion the way to to do it is by crashing the financial system. That is what I take from the "oil war" between Russia and Saudi Arabia that began in March. As I explained on part one, both those countries are fed up with the mastery of Uncle Sam and his green paper. Consequently, they share the same interest of terminating that hegemony. In my opinion, the so-called oil dispute was a mere diversion for they are actually on the same side. More than to destroy the US oil and gas industry, this concerted action aimed at wreaking havoc on the entire global financial system. On account of lower crude oil prices, oil-producing countries are having their inflow of dollars diminished. Thus, these countries are finding it harder to meet their dollar obligations, which prompts the decline of those countries' currencies. Because it reduces their citizens standard of living, tensions are starting to escalate, lifting the prospects of war (not necessarily boots-on-the-ground war, but currency and trade wars), particularly in the Middle East. By looking at the next graph, the contango beyond front months hints at economic troubles for a long time.  As a result, this weak business sentiment and reduced expectations of international trade and global economic growth are and will continue to send shock waves throughout the whole financial system. Hence, the dollar will carry on soaring, due to financial woes brought about by the Eurodollar participants facing difficulties in getting the dollars to support their funding gap - talked about in the Eurodollar system: the untamable beast series. In spite of causing more harm to the EM than the DE, this financial panic and economic collapse, triggered by the devaluation of oil, may be part of the Russian-Saudi plan, as you will understand later. Moving on, the Fed can print dollars to bail out the domestic corporations and financial institutions, while the other central banks, which cannot print the USD, have to deplete their reserves to rescue their own cronies, putting the trust on their currencies at serious risk. By and large, the EM nations have their currencies tacitly backed by the dollar. Inasmuch as these countries, compared to the DE, are viewed as reckless and financially irresponsible, the greenback gives their currencies some credibility. Taking China for example, there’s a direct relationship between dollar inflows, or what people call hot money, and the supply of Eurodollars on the market, resulting in the Chinese monetary system to be dollar-based. The picture below is a visual representation of how the Chinese system works.  In other words, more dollars means banks are able to create more renminbi (RMB). The way the People's Bank of China (PBOC), the country's central bank, tries to control that is by increasing the required rate of reserves (RRR) to lock up some of those created reserves so as not to become runaway reflationary. Inversely, less inflow of dollars has deflationary effects. To encourage banks to continue lending the same amount of yuan, the PBOC could decrease the RRR to foment inflation, as it did in 2014 and 2015. Yet, this policy did not have expected outcome. To tackle this, the PBOC in 2016 decided to print an exorbitant amount of RMB, worth a trillion dollars, and lent them to the banks against some relaxed standards for collateral. Therefore, although this spurred the Chinese as well as the world economy, the RMB was devalued. To this point, China may have reversed the course of the waning global economy, but its citizens paid the price by having the purchasing power of their currency diminished. Look at the world (or even just the United States) from the position of China. What makes America a super power? Is it the military? Partly. Is it nuclear weapons? Not so much. What really gives us leverage is the position of the dollar as the base currency. In the last financial crisis, we escaped largely by printing money. Other countries can’t get away with that without causing massive inflation. On the flip side, the US enjoys an exorbitant privilege that appears to have no limit. In view of the fact the demand for dollars, especially at periods of financial distress such as the present one, is unquenchable, Washington can indulge in tremendous deficit spending and finance it by activating the printing presses, something that the emerging countries can only dream about. Considering that the US has virtually no real productive economy, this is quite the achievement. Specifically, the American economy is made up almost entirely by the service sector, having very little manufacturing. At least, the manufacturing that it has consists of high-tech industries which require a lot of expertise and skilled workforce. However, keeping in mind the not-so-high-tech industries, including the ones that serve the high-tech, have been transferred overseas - which is most of the manufacturing sector -, that is not enough to have a current account surplus, far from it. This is the essence of the Triffin paradox. Evidently, with the dollar as the global reserve currency, the demand for it pushes its value up, to a level that is unjustified by the never-ending negative current account and budget deficits. Regarding the latter subject, one would infer that with the national debt ballooning, the yields of the Treasuries are going to surge. Consequently, insofar the threshold is reached, where Uncle Sam cannot tax its nephews the sufficient dollars to service his debt, the Fed would have to monetise all the debt, which would provoke the yields of the UST to rise out of control.  Despite nothing has indicated the Treasury debacle is imminent, that is certainly a possibility in the not so distance future. At this moment, the opposite scenario has shown signs of being the most likely scenario. The following graph offers a hint. Alternatively, and as ludicrous as it may sound, the Treasury yields will subside further, presumably into negative territory. This will happen since there is not yet a good enough alternative that could prevail over the Eurodollar system and jeopardise the dollar dominance. Therefore, there is nothing else that can supply the kind of liquidity at the international level that the American financial markets provide. As a result, the Eurodollar system will proceed as it has for now.  In addition, this makes you wonder how this is going to end. In my view, there are three possible situations that may occur:

In relation to the first one, the day Uncle Sam has to pay the piper is going to come at some point. Yet, because of the particular modus operandi and infrastructure built around the dollar, i.e. the Eurodollar system, the dollar hegemony still has some legs to stand. So what we’re looking at is the possible use by others in the world of our dependence on the dollar to give us so much power that we otherwise would not have…Charles de Gaulle once said it was vicious what we did after the war when we had the world’s reserve currency…and take that power away from us. On the next point, owing to the funding gap carried by the market participants of the Eurodollar, the current financial constraints, which are bound to last for awhile, are going to strengthen the USD to extremely overvalued magnitudes, considering its poor fundamentals. Thus, the dichotomy of the US economy will become even more disparate. As I stated above, high-tech industries, like aircraft and the ones in Silicon Valley, and financial services are the only thriving sectors in America. All of these are concentrated in the major cities. If one happens to live in any of these cities, he should be living well. But most likely he is not. On account of ever increasing rent and overall everyday expenses, the average Joe is failing to reap the benefits of the dollar supremacy. Now, imagine how bad it must be for those in Middle America who are witnessing the vanishing of their jobs and livelihood, ending up settling for less or moving to another place, like a big city. for better opportunities and standard of living, which they will hardly find. No wonder the American people are getting increasingly displeased with their political establishment, despite their anti-establishment picks have been coming short of expectation. In 2008 and 2012, the people voted for Obama but he did not deliver. Then, they voted for someone more radical, Trump (not to forget that Bernie Sanders could have won the Democrat's primaries), and still their prayers are to be answered. Unsurprisingly, the current presidential run has turned every candidate, even the previously moderate ones, into extreme demagogues, rivaling any marxist or fascist despot America claims to despise and fights against as well. Finally, this financial distress could be of such magnitude the whole financial system will be forced to collapse. Like I said above, this may be the rationale behind the "oil war" between Russia and Saudi Arabia. In more detail, that quarrel has the objective of, besides knocking the American oi and gas industry down, amplifying the already colossal financial distress of the Eurodollar system and escalating the tensions in the Middle East and possibly other pockets around the globe, which would intensify even more the financial troubles and, therefore, hindering economic activity. The situation will get tremendously precarious, especially in the EM dominion, though the DE will also be impaired. As a result, these countries and Western Europe, Japan, Australia, etc. will unite to fight the dollar hegemony and bring this common enemy to its knees. Unfortunately, inasmuch as the ruling elites of the US in all likelihood will not simply surrender this godsend that enables Washington to essentially conquer the world, this fight could turn into a war. Insofar the US has been involved in currency and trade wars, the next presumed step seems to be a real war. What generates war is the economic philosophy of nationalism: embargoes, trade and foreign exchange controls, monetary devaluation, etc. The philosophy of protectionism is a philosophy of war. To conclude, I take the view we are going to experience a mix of those three circumstances. Because of the spiraling US dollar, prompted by the massive financial distress, the whole world, including the American people, will urge their policy makers to resolve whatever needs fixing. Since the issue will be at plain sight for everyone to see, and almost impossible to ignore, the world will join forces in order to overcome and supersede the dollar from its reserve status.

Furthermore, the despicable behaviour carried out by the US, with its monumental deficit spending and debt monetisation, is going to turn market participants more concerned about the state of American finances and will begin to lose faith in the Treasuries. Seeing that the Fed can print as it pleases and the Eurodollar system will absorb them easily, this is not a menace for the USD. However, this obnoxious privilege will galvanise the rest of the world to multiply its efforts to end the reign of the greenback. Ultimately, once the dollar is dethroned, if the US government refuses to abandon both its reckless ways of pandering to the electorate, promising them all kinds of entitlements, and its imperialistic agenda - which they certainly will because it cannot be done secretively and inexpensively without the dollar as the global reserve currency -, the US could lose its credibility, giving rise to a sovereign debt crisis. Therefore, if they do not kick the habit of turning on the printing presses, a hyperinflation episode could ensue.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed