|

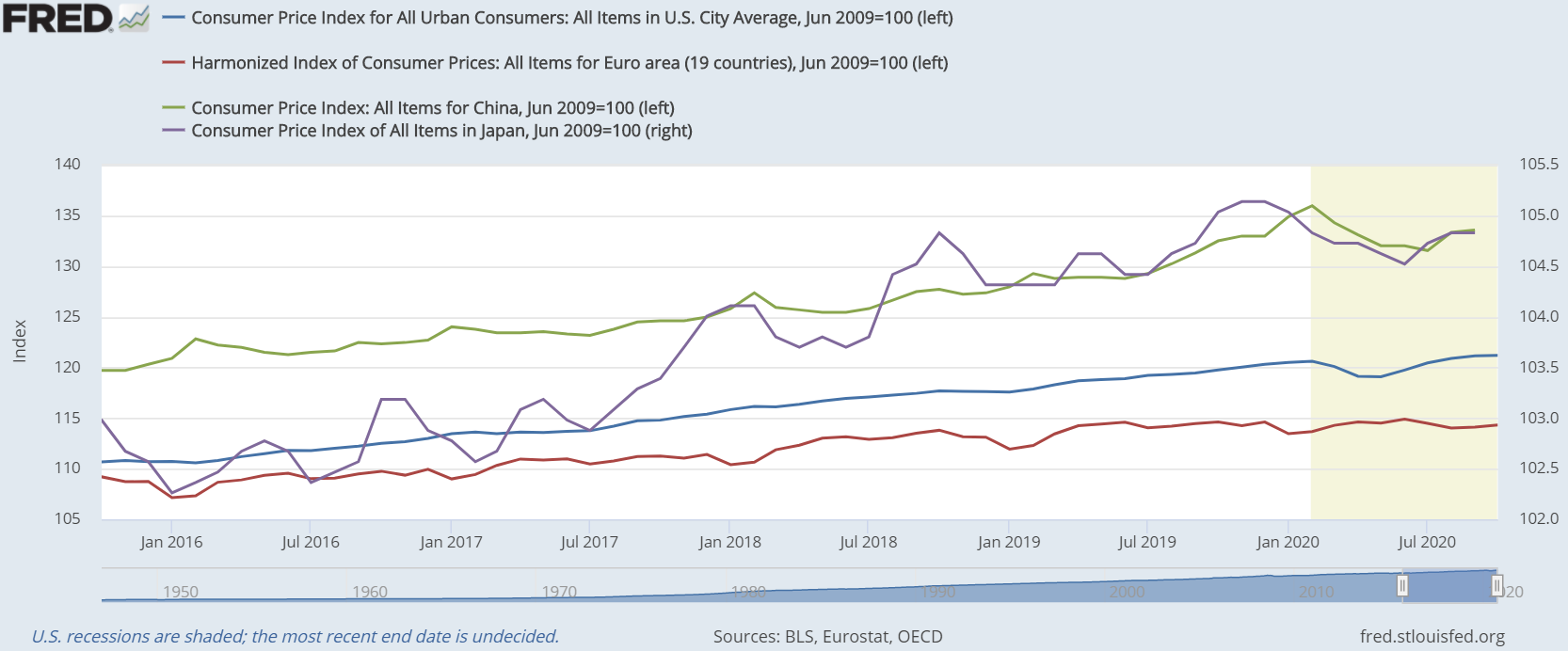

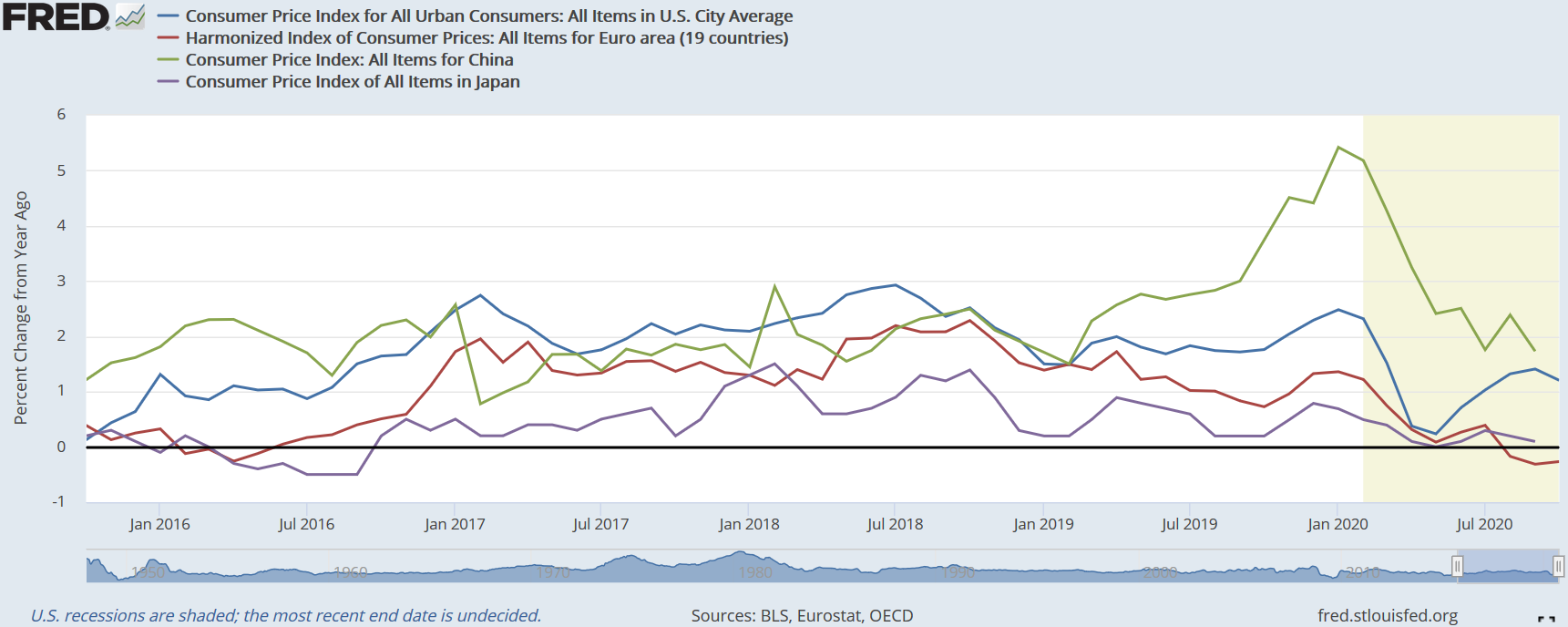

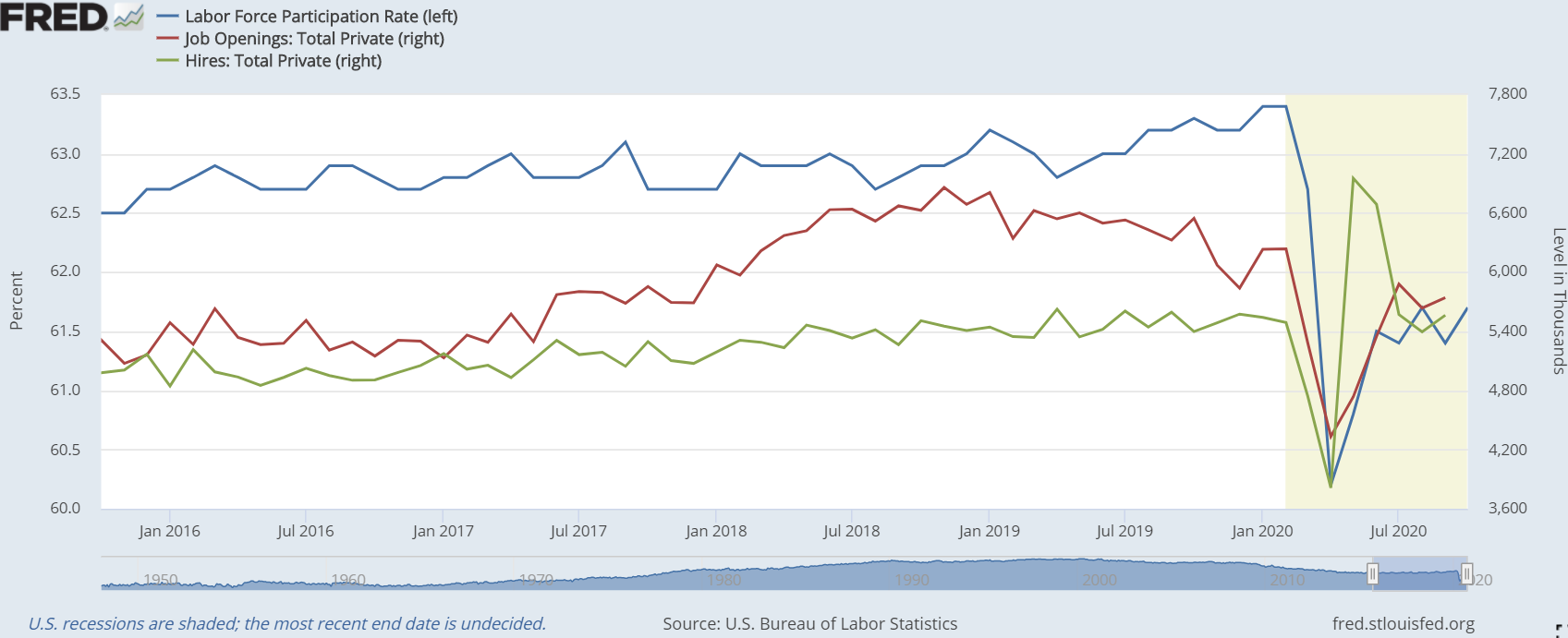

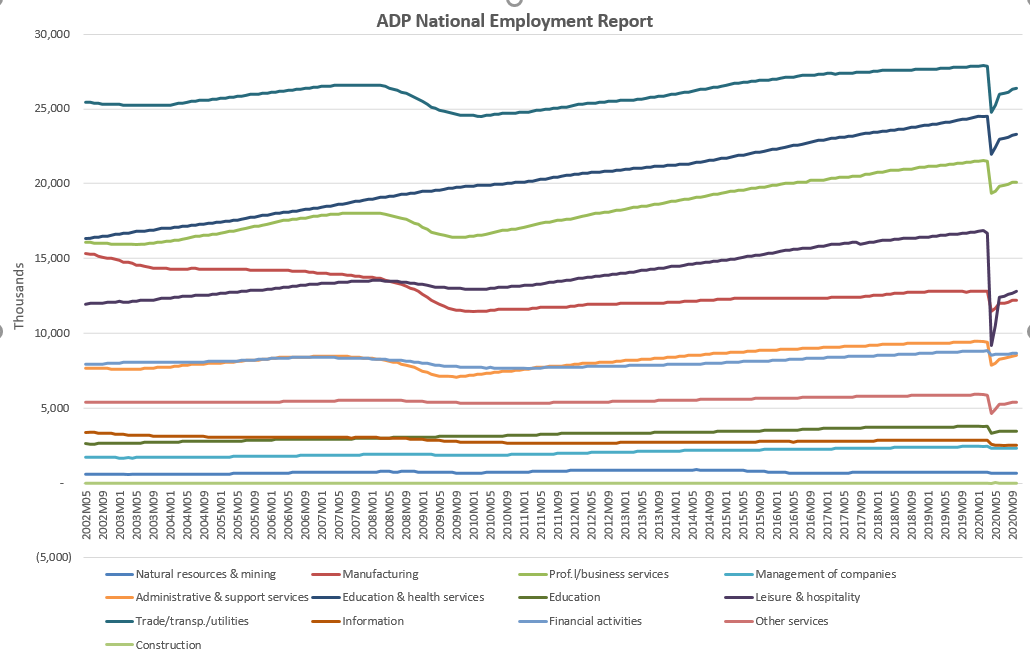

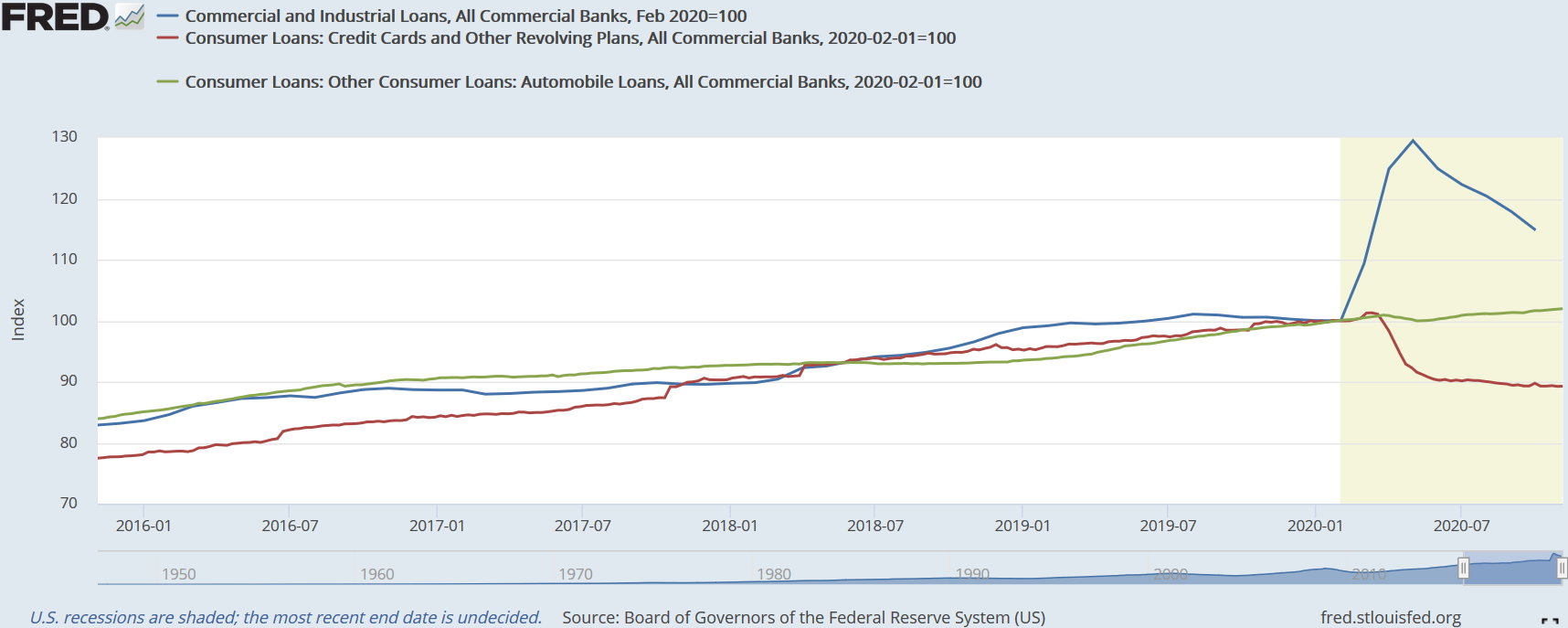

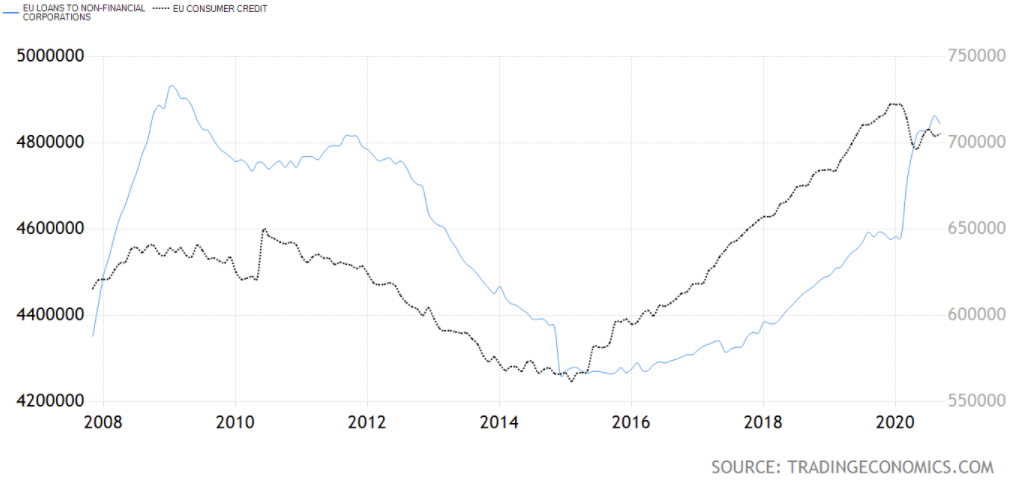

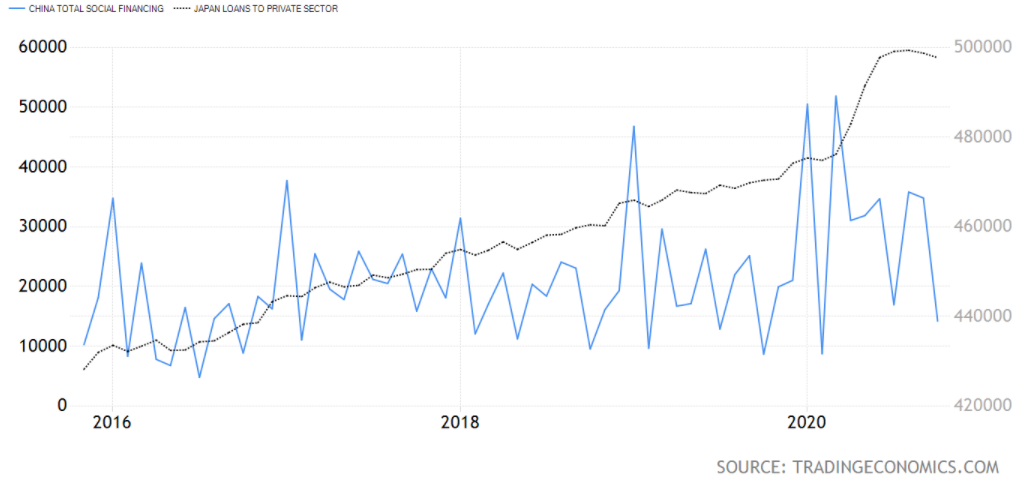

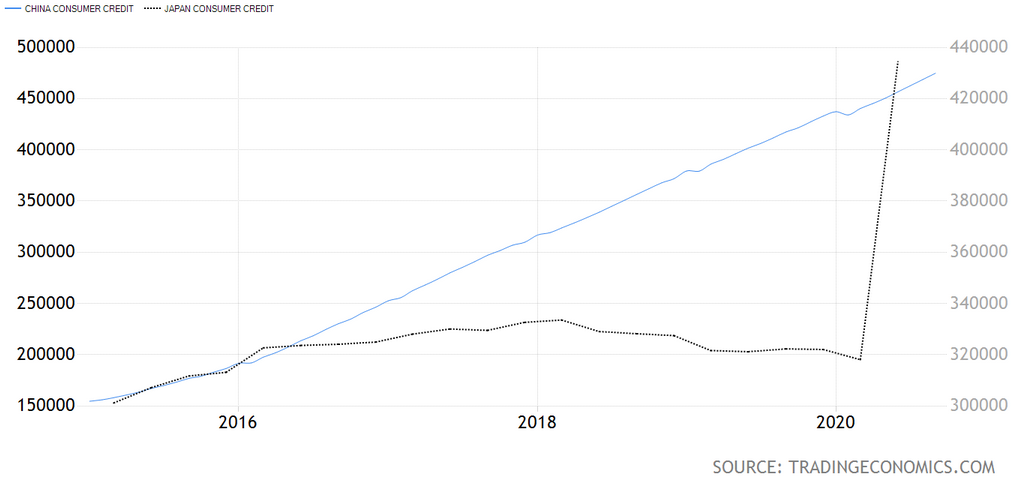

Resuming this three-part series about the health of the economy and the power of the vaccine plus stimuli combo to keep the boom alive, I am going to pick up where we left off on the first segment, exploring some macro data. As a reminder, part one concluded with the business and consumer confidence surveys for the featured geographies, namely the US, the EA, China and Japan. Despite shooting up from their March bottom, these sentiment surveys were pointing out the rebound was losing momentum. To add insult to injury, European consumers' confidence has turned more pessimistic since the end of summer. In view of the fact Germany has been a harbinger for the global economy, since at least the GFC, its ZEW figures are hinting at alarming prospects. All the same, is there any real reason to doubt the reflation story? After all, governments and central banks around the world are doing more than ever before to prop up their economies. As I claimed at the conclusion of part one, "the amount of optimistic figures are very scarce and becoming even more so as time goes on". Hence, it is now time to present the more dreadful data which happen to paint a more realistic picture of the state of the (global) economy. Because the monetary (eurodollar) system is a debt-based one, in order for the economy to keep on expanding, the money supply must inflate equally, either through government debt or bank credit. As you ought to already know, the original definition of inflation is the expansion of the money supply. However, this definition was gradually lost. Instead, the currently established definition is a general rise in prices. Although that is the case, as Milton Friedman put it, "inflation is always and everywhere a monetary phenomenon". Therefore, an increase of the money supply begets a general rise in prices. In any event, inflation brings about rather dreadful consequences. In spite of not being a necessary condition for economic growth, owing to the present monetary system being based on debt, soaring prices are an indication the economy is booming. Now that I have jogged your memory, let's look into the statistics. Across the board, the CPI figures have climbed from the March lows. Nevertheless, in China it has been dwindling since the end of last year, on account of pork supply and, consequently, price returning to normal levels after a serious outbreak of African swine fever (Rabobank estimated China lost up to 55% of its pig herd last year). With Europe, in addition to Japan, acting as forewarnings, and the US being a laggard, the lack of acceleration and even the falling prices, in the case of the EA, imply economic activity is rolling over. Be that as it may, a deeper dive into more data is on the way.   Focusing on the US, due to the easing of restrictions, companies began hiring some of the workers they had let go during the lockdowns. Unfortunetely, the number of openings is still fewer than the pre-covid era. Similarly, the amount of hires has not been enough to absorb the laid-off workers victimised by the hysteria, as the ADP payroll report below shows. To make matters worse, employment growth is dangerously stalling, especially in the industries most affected by the economic shutdown. Furthermore, that may explain why the labor force participation rate has remained subdued for a few months at very low levels, though after an initial rebound. Ergo, all of this measures up, not to the reflation - even less to the "V-shaped" recovery - narrative, but to the deflationary slowdown one.   Evidently, so as to experience the much anticipated reflation, as I explained above, credit has to grow as a direct consequence. Curiously, credit creation has been somewhat disparate between the type of borrower, as well as between the East and the West. On the one hand, in America and Europe, loans aimed at businesses skyrocketed during the restrictions to compensate the plunge in revenues. Likewise, the same thing occurred in the Orient, though in China the spike peaked in February because they caught the lockdown fever in late January. Like I said on the post of October 24, "[t]hat surge at the beginning of the pandemic is explained by the rolling out of lines of credit directed to businesses in order to keep up with current expenses, such as salaries, rent, etc., by making up for the diminishing revenues. (...) Yet, this kind of loans plus real estate loans have joined the downward trend set by consumer loans, which has been decreasing since the kung-flu hysteria invaded the New World, especially credit cards and other revolving plans". On the other hand, credit directed towards consumption has been decreasing in both the States and Europe, while over in Asia it has been the complete opposite. In China, consumer credit continued swelling at the same pace as if nothing happened. Even more remarkable, the uptick in Japan has put this kind of credit at levels not seen for almost a decade. Notwithstanding, as I exposed on part one, this has not been enough to push retail sales to decade old highs, not even one year old highs.

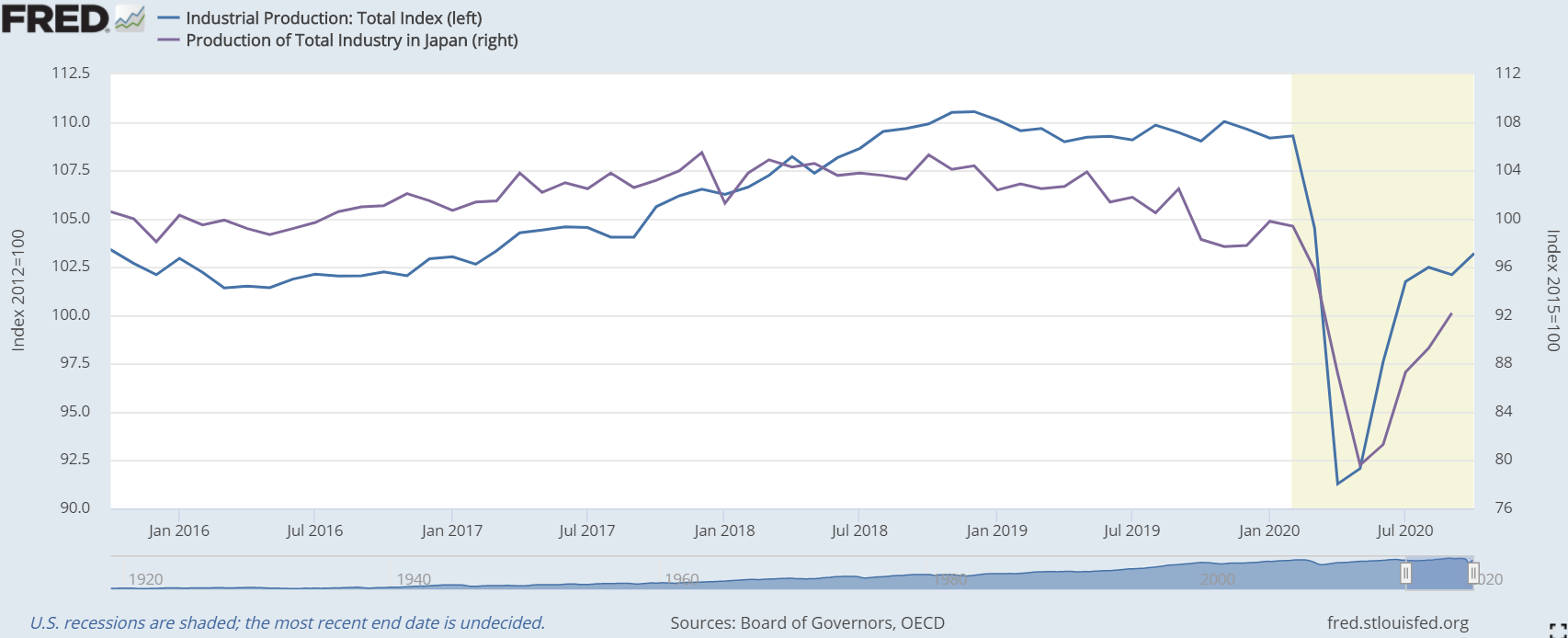

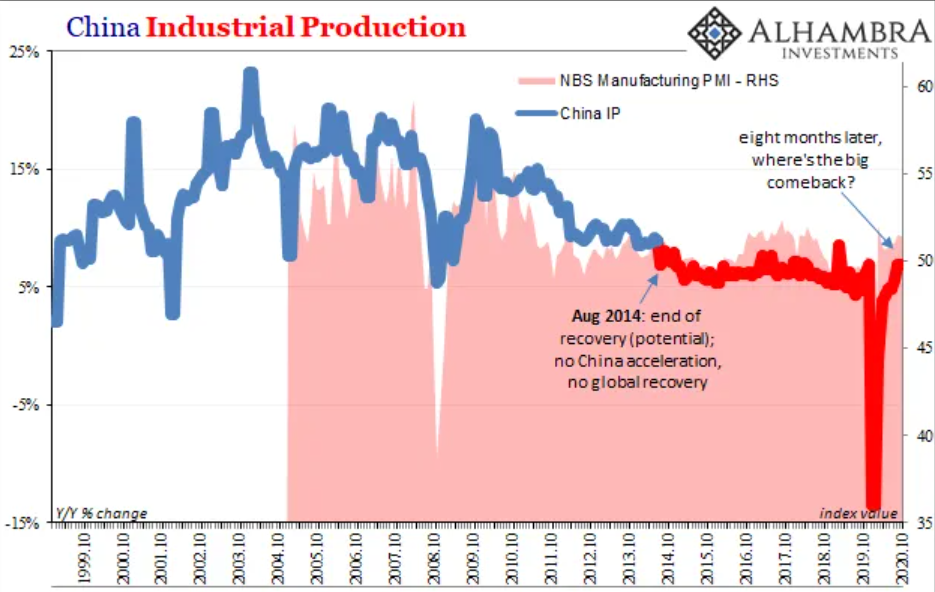

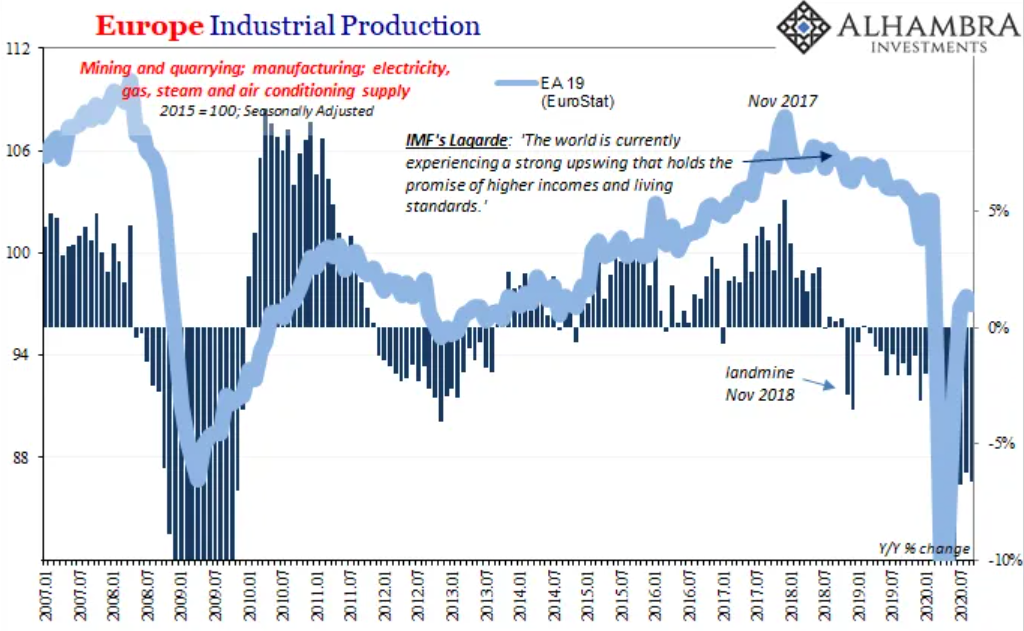

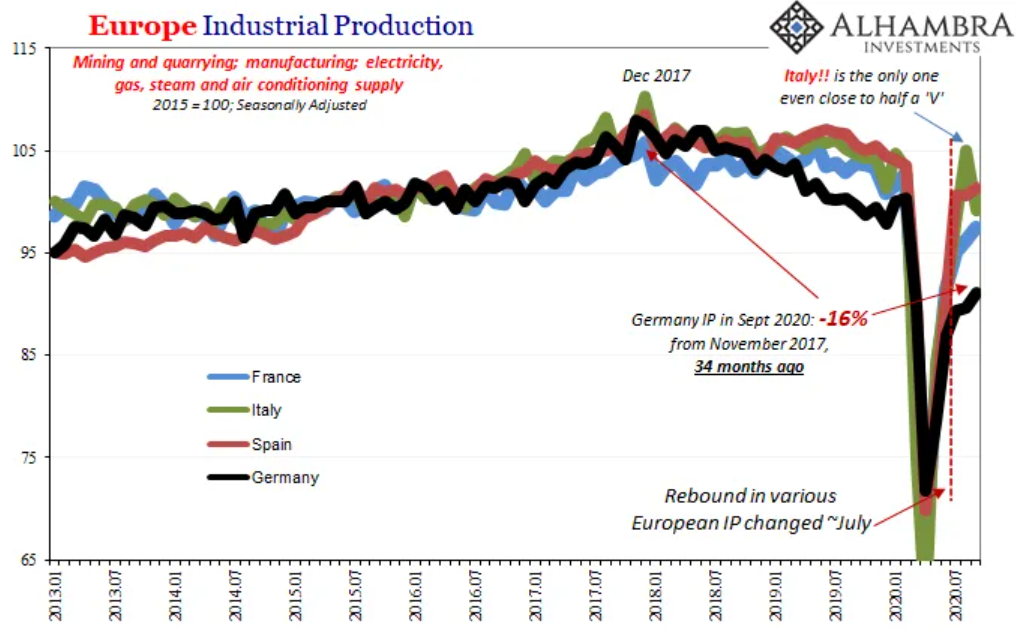

Insofar as banks are the true money creators, when they believe economic opportunities are proliferating more credit is originated by providing loans and other types of debt to consumers and businesses. Having said this, the surge in business borrowing has not spurred an equal amplification of the industrial production, having even come up short of tagging the level of 2019, which had notoriously failed to surpass the previous year's peak in all these countries - yes! including China. Once again, the fact that the IP comeback in Germany, which is a manufacturing powerhouse, is halting at such a low level speaks volumes about the state of future demand in the short-term. It goes without saying, this bodes terribly to the reflation cheerleaders in government buildings and financial centers across the globe, as well as in financial newsrooms.

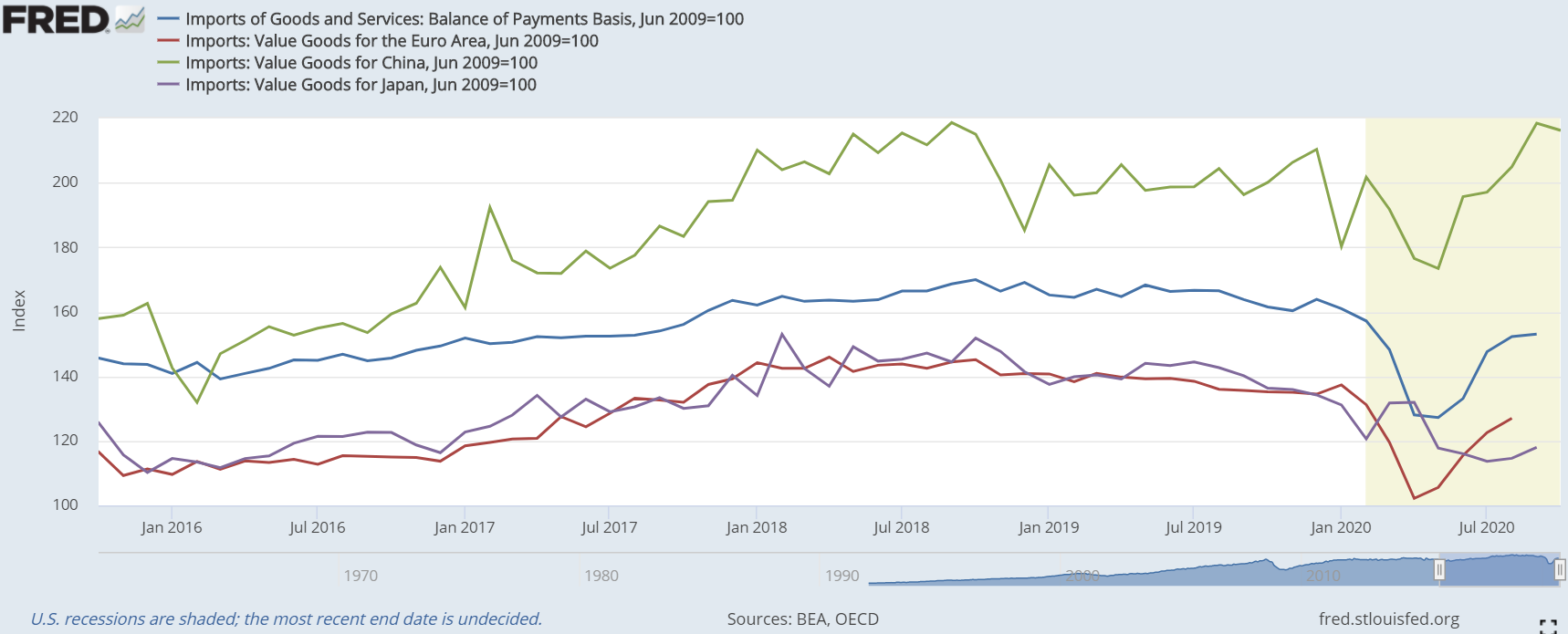

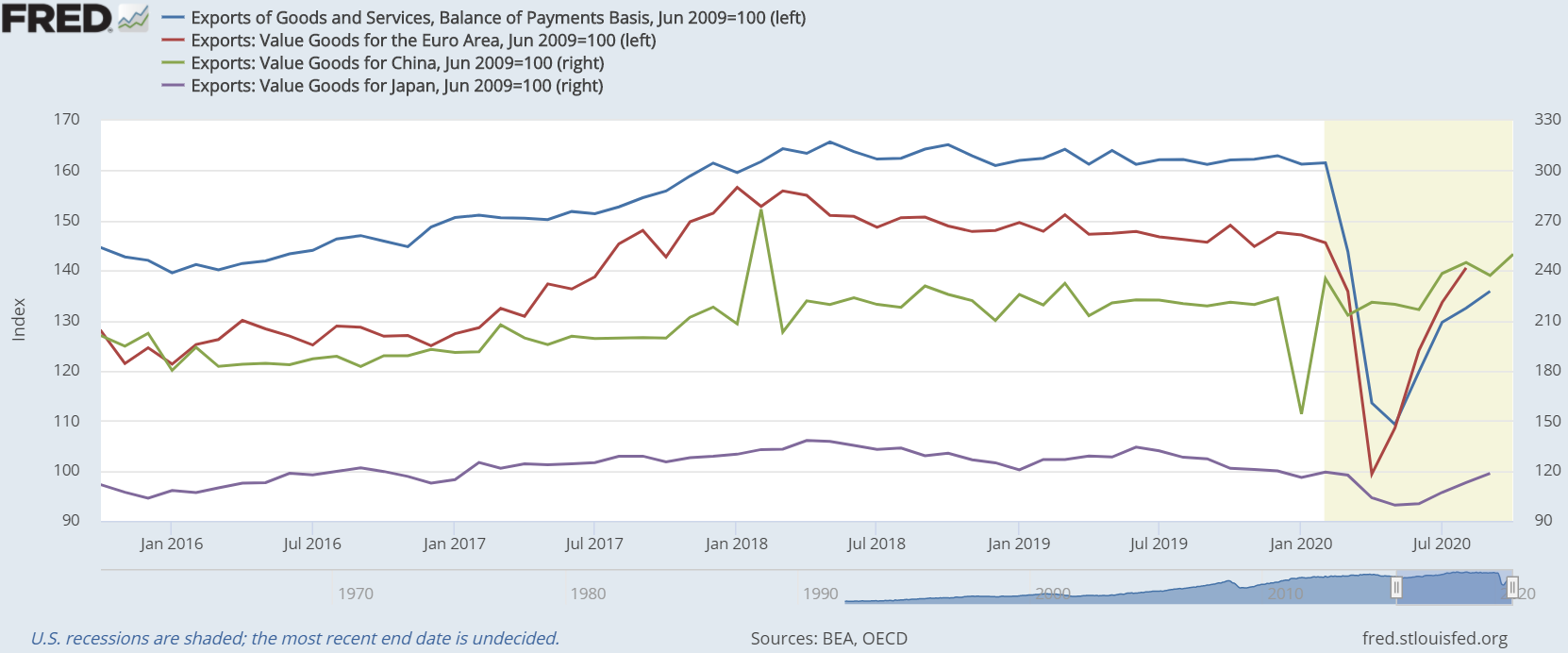

Moving on to the last piece of macro data (but not to be the least), imports and exports, which represent the condition of global trade, suggest what I have been claiming, despite the apparent absolute recovery in China. Unfortunately, the developed realm has yet to follow the Red Dragon. Without a recovery of global trade, you can kiss the reflation story goodbye. The reason for the DM being struggling to get these figures, particularly exports, to pre-covid levels is that their currencies jacked up, in comparison to the EM ones during the March financial meltdown. On account of financial conditions remaining rather tight, although liquidity woes have gradually alleviated, these currencies are still relatively strong. Accordingly, the goods from the EM are cheap(er) to us and our goods are, in turn, (more) expensive to them.

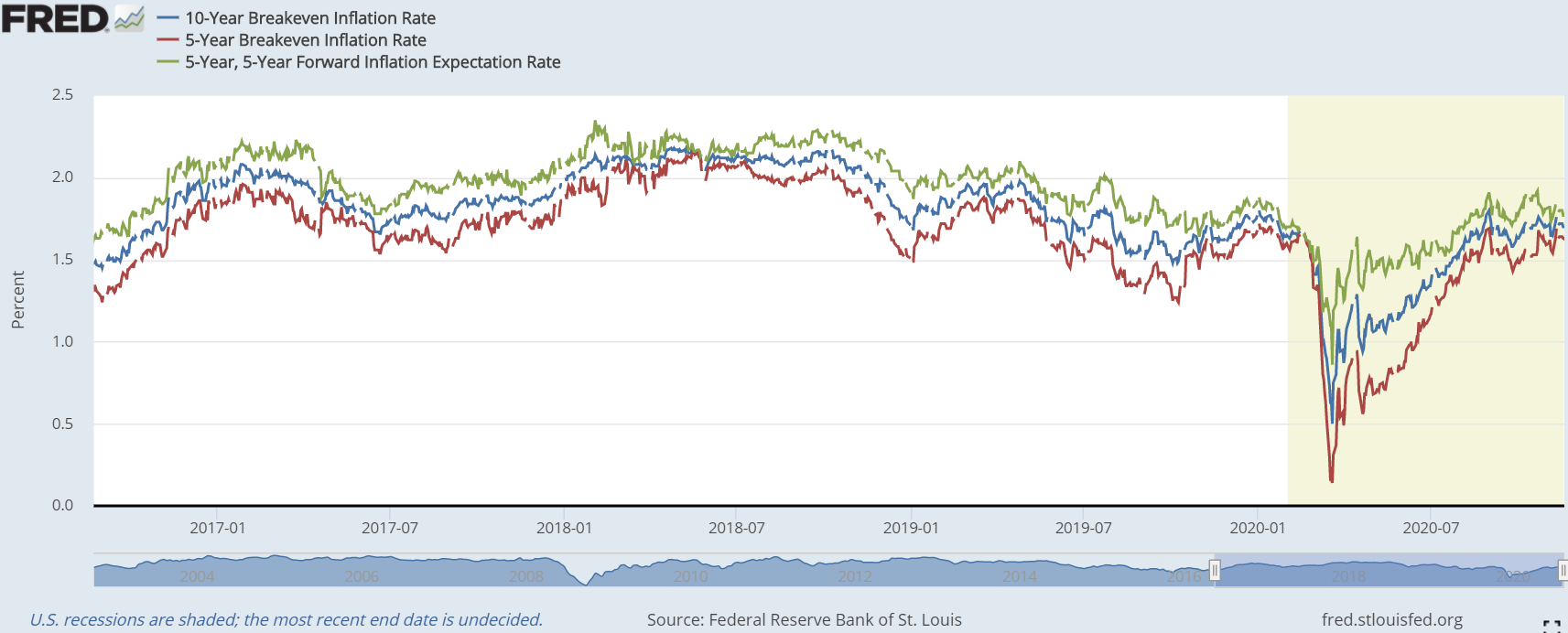

Finally, in terms of market-based inflation expectations, which are more illustrative than any survey and any bank's or government entity's forecast, these indicate a much more terrifying outlook. For all the hype around the ballooning balance sheets of central banks and strategy review announcements, like the recent one made by the Fed, market participants do not even believe the inflation rate, in the US, is going to average 2% in the second half of this decade. Obviously, if you tune in on the financial channels, read their articles or listen to the speeches by central bankers, you are definitely not going to get these insights. In view of the fact these are (financial) market signals, these will set the stage nicely for the final instalment of this series, which is going to be fully dedicated to the financial domain.   In conclusion, I think I have demonstrated the summer rebound was not sufficiently strong to make up for the lost output during the lockdown-mania. Having lost quite of its momentum around June, the rebound had exhausted almost completely by the time September came.

On the next and final chapter of the series, you are going to see that financial markets, from the bond to the stock market and from oil to the dollar, are messaging this exact information. In addition, we are going to figure out how these market participants reacted to the alleged Biden victory - and western civilisation loss - and to the vaccine news.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed