|

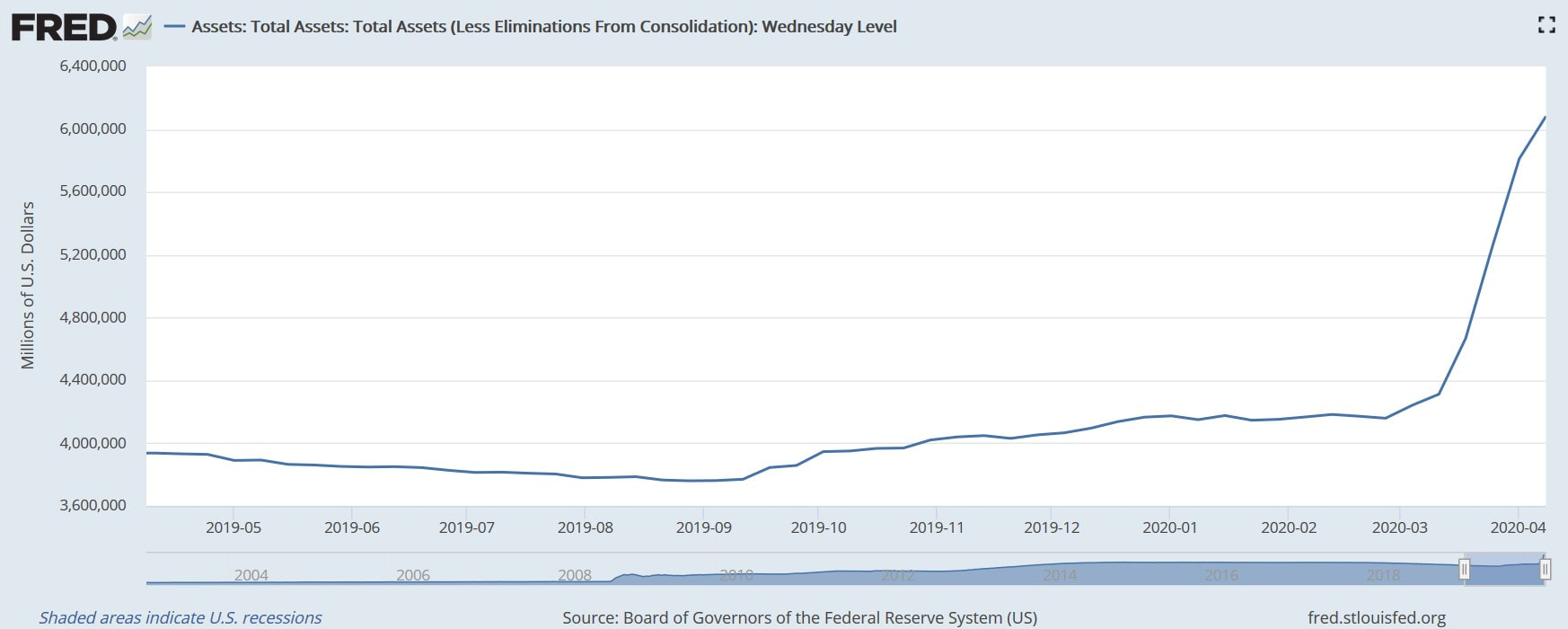

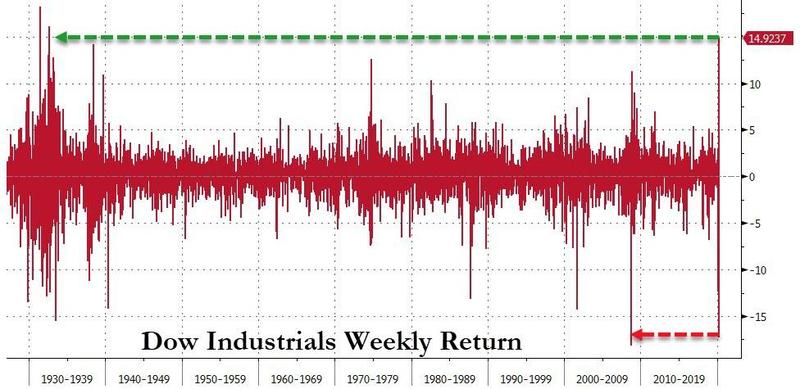

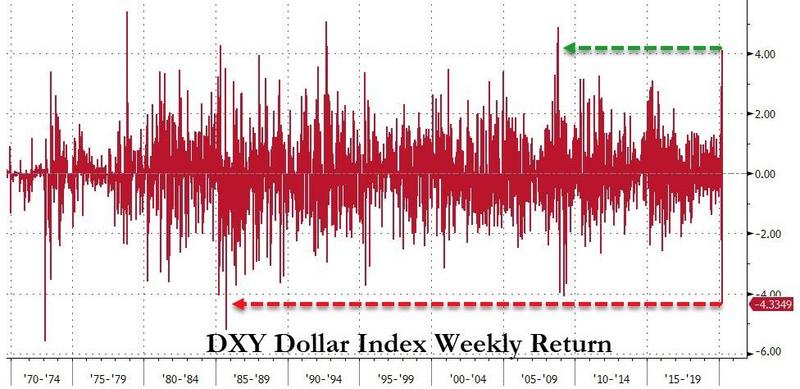

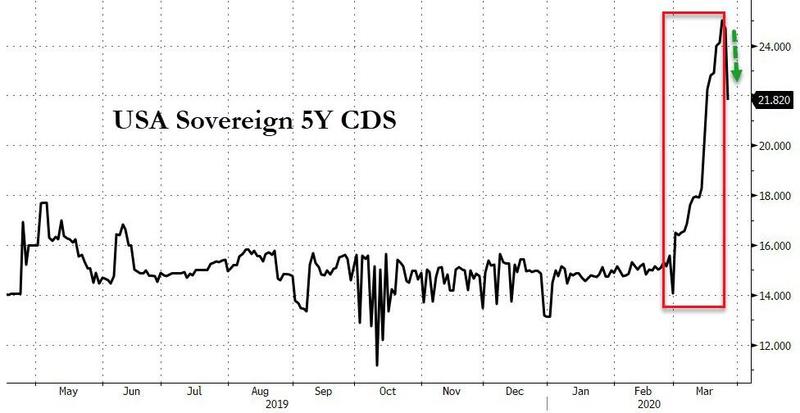

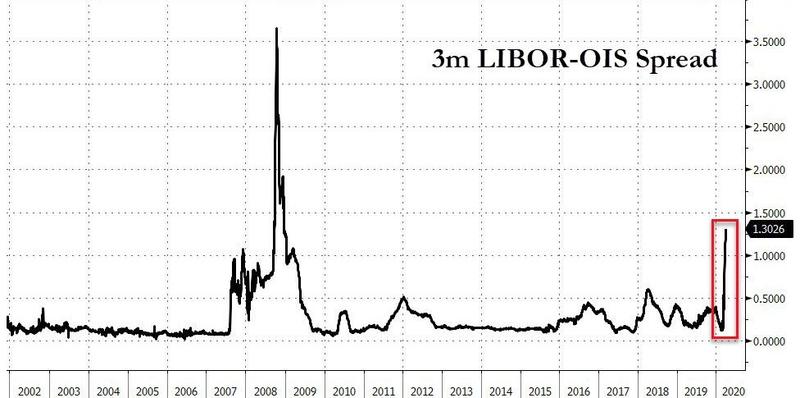

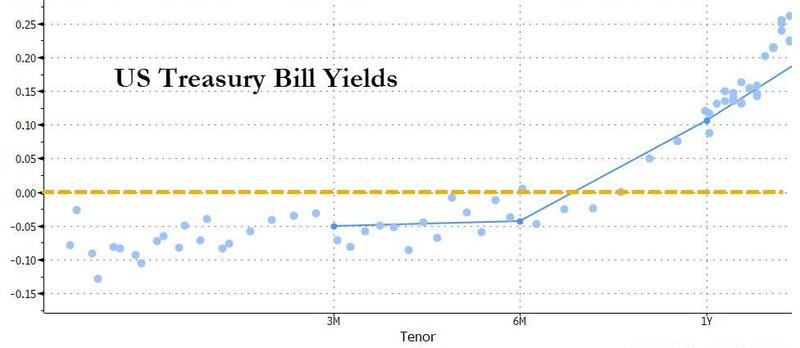

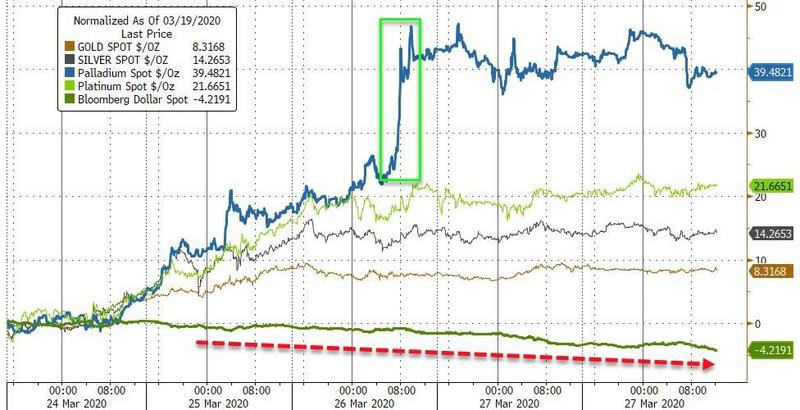

By looking at the stock market this week, one would assume the lockdowns have been lifted and the economy was back on track. Business as usual, right? Do not get fooled by the stock's head fake. Once you delve into the other financial markets, you will find out more problems are arising. To begin with, there are three reasons behind this week's surge in the stock market: the passing of a $2 trillion "stimulus bill" in the Senate; the acceptance of equity securities (shares) as collateral in the Fed's Primary Dealer Credit Facility; and the spurt of the Fed's balance sheet.   Although stocks may have soared this week, with the Dow having its best weekly performance since August 1932 - from Tuesday's open to the close in Thursday, it even achieved bull market status, having jacked up 21.3% -, the greenback had its worst since September 1985, right when the Plaza Accord took place.  In additin, the US dollar is going down while there is still extreme dollar shortages, as the spread between the forward rate agreements (FRA) and the overnight index swaps (OIS) continues to widen.  Moreover, the Treasury notes and bonds (2 to 30 year maturities) were all bid this week. To be more specific, their prices and, consequently, their yields remained approximately the same until Thursday and then yesterday investors rushed to get them, with the long-end (10 and 30 year) outperforming.  Additionally, after rising up to Thursday, the perceived risk of a US government default plummeted yesterday to such an extent that this indicator went down for the week, which explains the move on the Treasuries.  Furthermore, banks are no longer trusting each other. The expanding spread between the LIBOR and the OIS hints at swelling counterparty risk and, thus, ever more troubles in the credit market.  In addition, investors are preferring to park their dollars in T-bills than in the banks, even as these yield negative returns. Obviously, this is related to the graph above. Investors would rather lose a little bit of their money than most. or even all, of it in a Lehman-type event.  Despite the scrambling for liquidity due to dollar shortages, the precious metals have all climbed for the week.  Finally, the massive drop in the dollar this week, whilst the shortage of dollars persists, signals that the faith in the greenback is dwindling. Inversely, the creditworthiness of the US Treasury seems to be holding, even though President Trump approved the $2 trillion stimulus bill and the economic activity is coming to a halt, as the surge to 3.28 million in jobless claims depicts.

Moreover, the growing counterparty risk among financial intitutions is making them dependent on the Fed and the Treasury to get liquidity and to store their cash. Once investors lose confidence in the ability of the Treasury to pay its debt, a tremendous selloff of USTs will ensue and, hence, the Fed will have to absorb them all, inflating the currency supply. As a result, the dollar will carry on devaluing, completely destroying the trust in it. To conclude, the financial system as we know it revolves around the US dollar and the Treasuries. The greeback is the world's reserve currency. With the US having negative Current Accounts, rendering it a debtor country, the globe is flood with dollars. The rest of the world then uses those and purchases dollar-denominated assets, specially USTs for being the safest ones. To make long story short, all financial markets are built upon the confidence the world as a whole has on the dollar and the Treasuries. Accordingly, the diminishing faith in them both is going to lead to the collapse of the dollar standard.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed