|

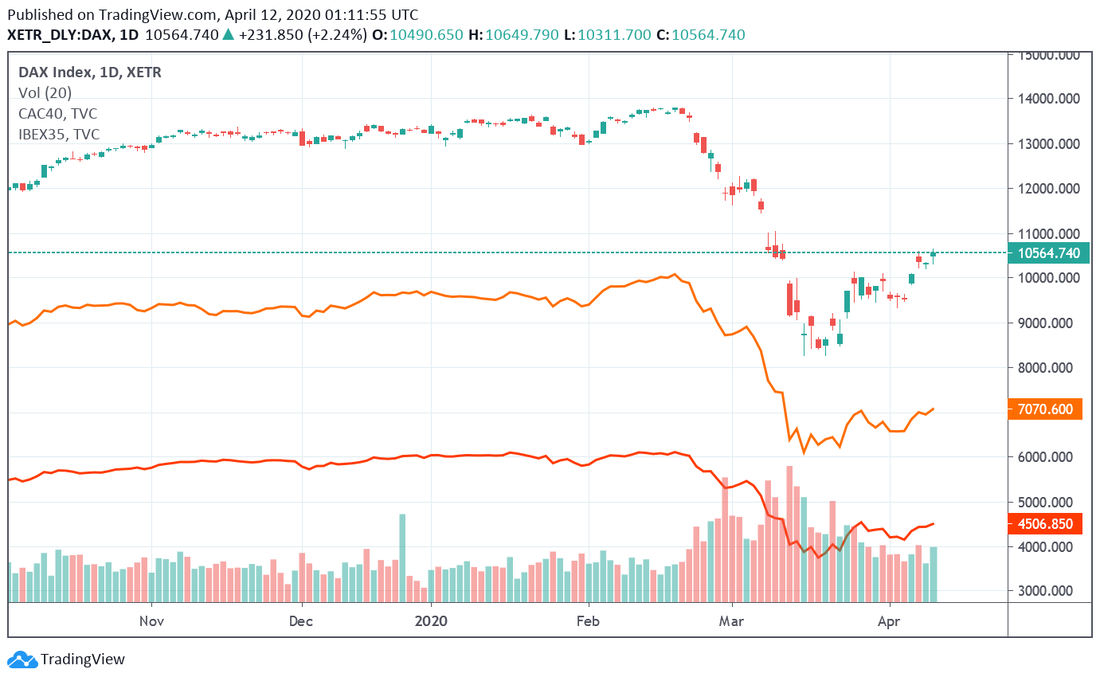

In this week, stocks went higher, sovereign bond yields remained constant overall and spreads of the corporate bond yields became tighter, in both sides of the Antlantic. Foreigners continue to sell US Treasury securities, while the Fed's liquidity swap arrangements with other central banks have apparently plateaued. The Fed has also kept on collecting Treasuries and the dollar has been losing strength, though liquidity contraints seem to be disappearing. However, the real world carries on crumbling down. To begin with, on the US stock market, the S&P closed up 12.1% this week, for its best week since October 11, 1974 when the S&P gained 14.12%; it is 17.79% below its intraday all-time high of 3,393.52 from February 19; and it is 27.28% off its 52-week low of 2,191.86 on March 23. In addition, the Dow Jones closed up 12.67% this week, for its best week since March 23-27, when the Dow gained 12.84%, and the second best week since June 1938; it is 19.78% below its intraday all-time high of 29,568.57 from February 12; and it is 30.23% off its 52-week low of 18,213.65 on March 23.  In the midst of a global economic freeze, how can stocks be surging at one of the fastest paces ever? Answer: the Fed in tandem with the US Treasury coming up with innovative ways to intervene in the markets and prevent prices and rates from reflecting reality. Besides all the facilities and rate cuts the Fed has made or commited to make, on this Thursday, April 9, the Fed announced that it will provide as much as $2.3 trillion in additional loans during the coronavirus pandemic, including starting programmes to aid small and mid-sized businesses, as well as state and local governments. Moreover, these Fed's loans and facilities are based on the additional capital the Treasury has made available under the CARES Act. Of the total $454 billion that Congress appropriated to backstop Fed facilities, this morning’s announcement appears to commit $195 billion, leaving the majority of funds available for other purposes or to expand these programs if necessary - which they will. In a nutshell:

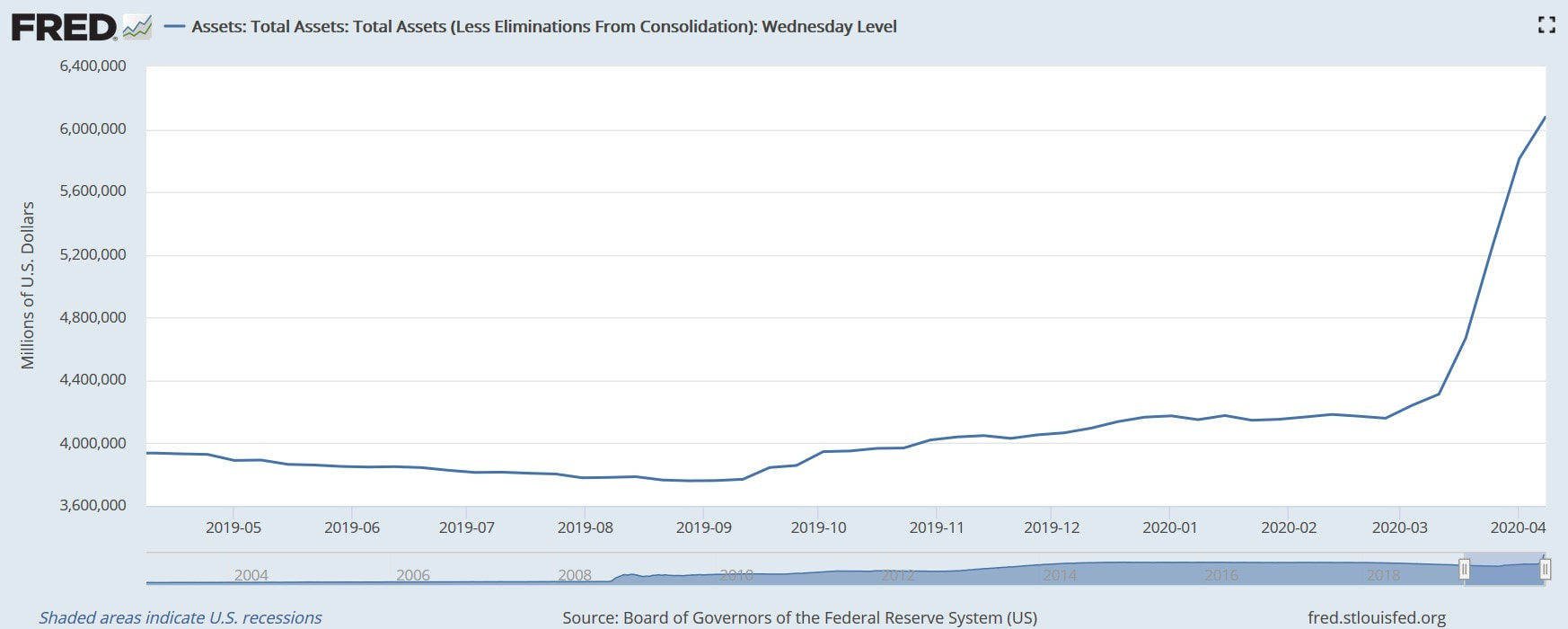

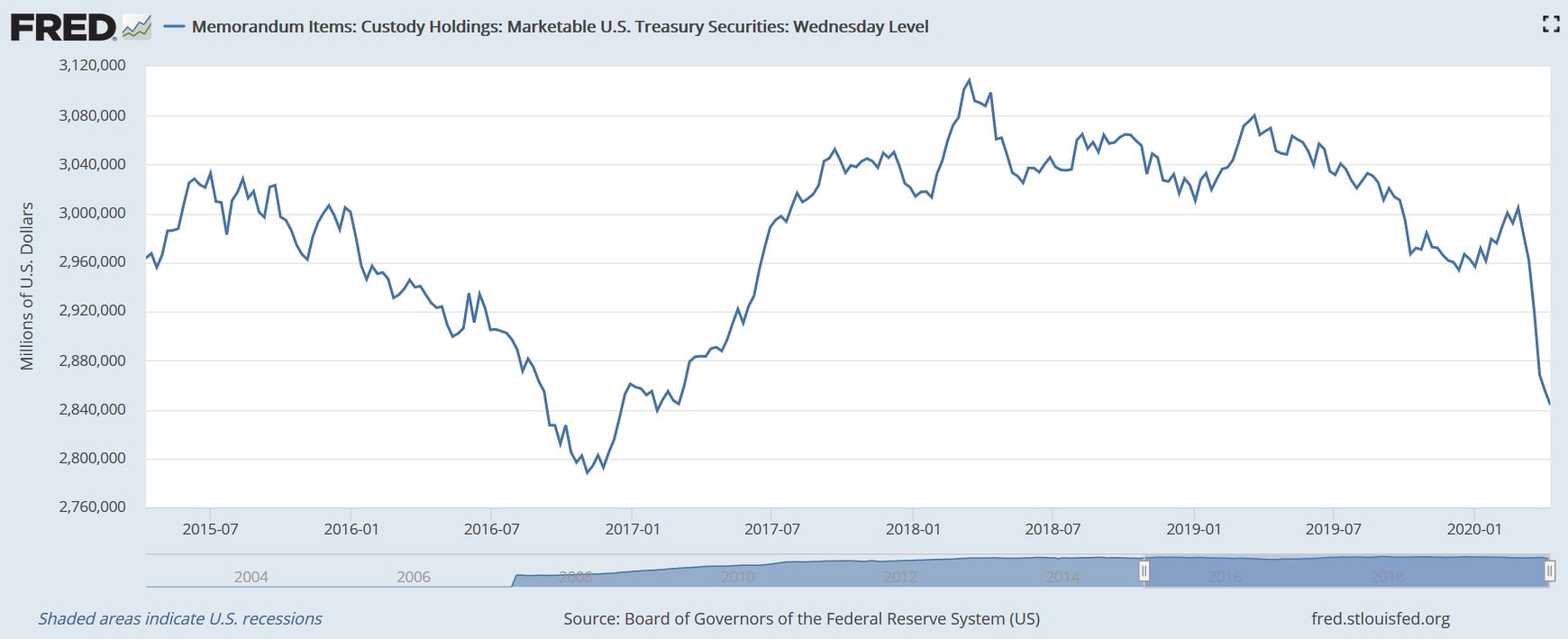

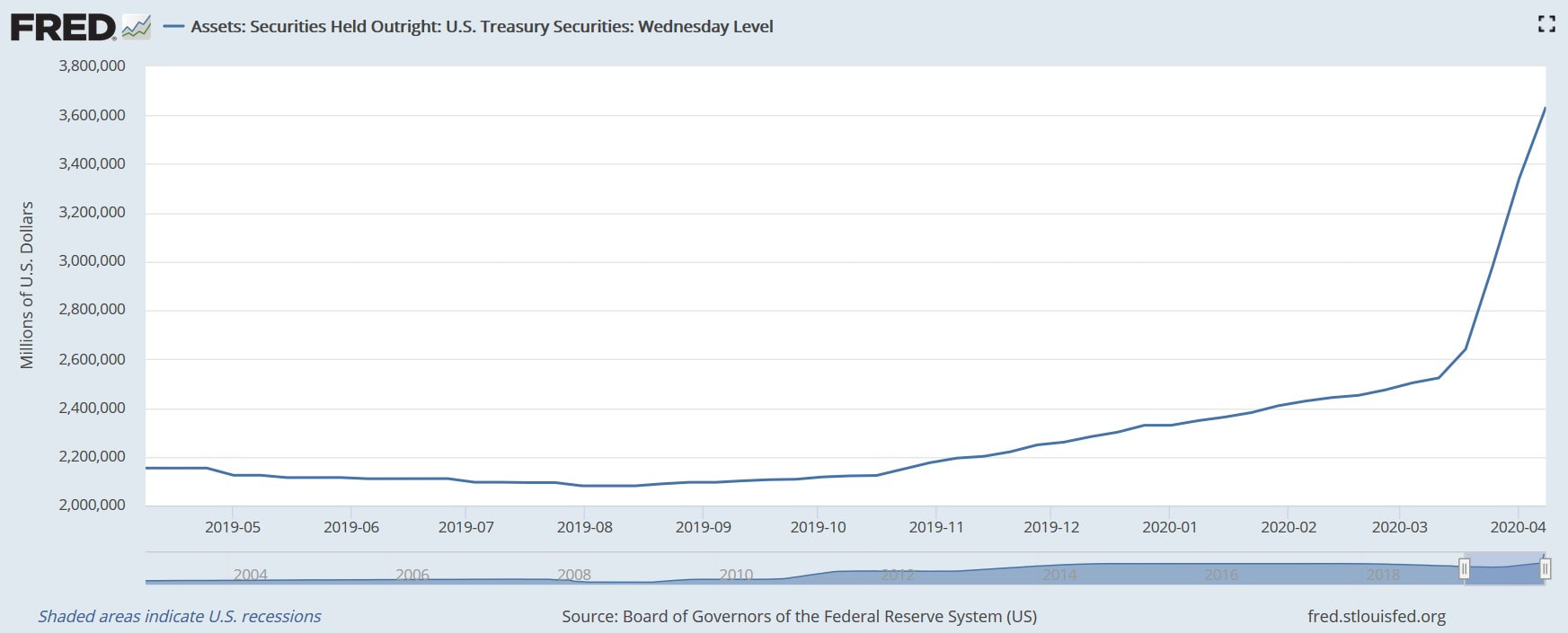

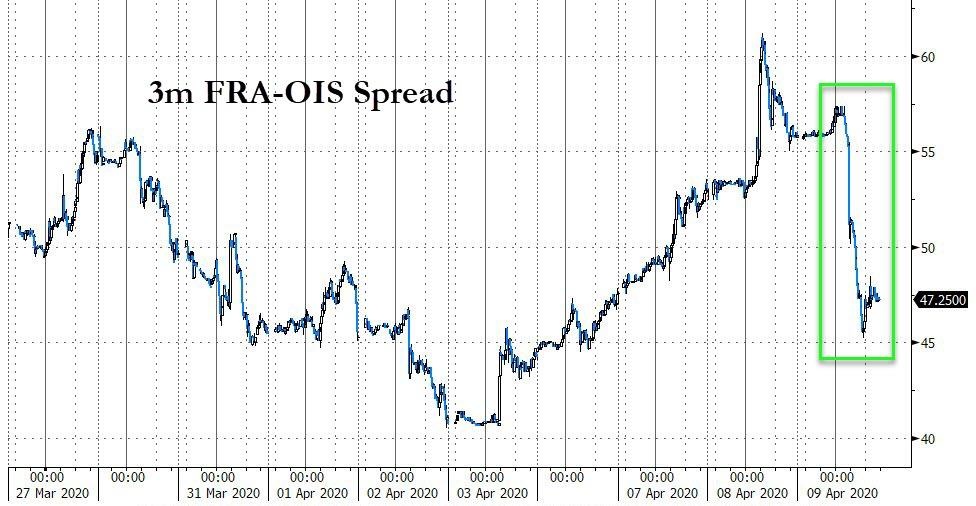

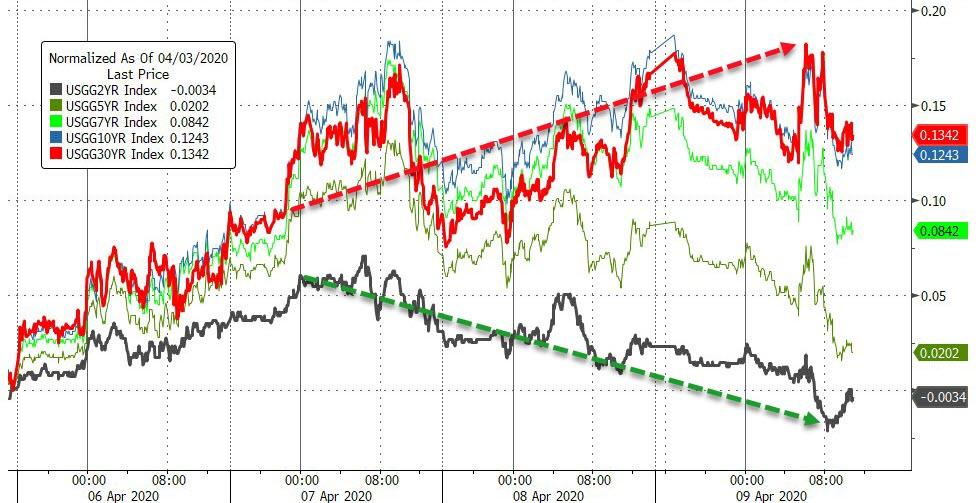

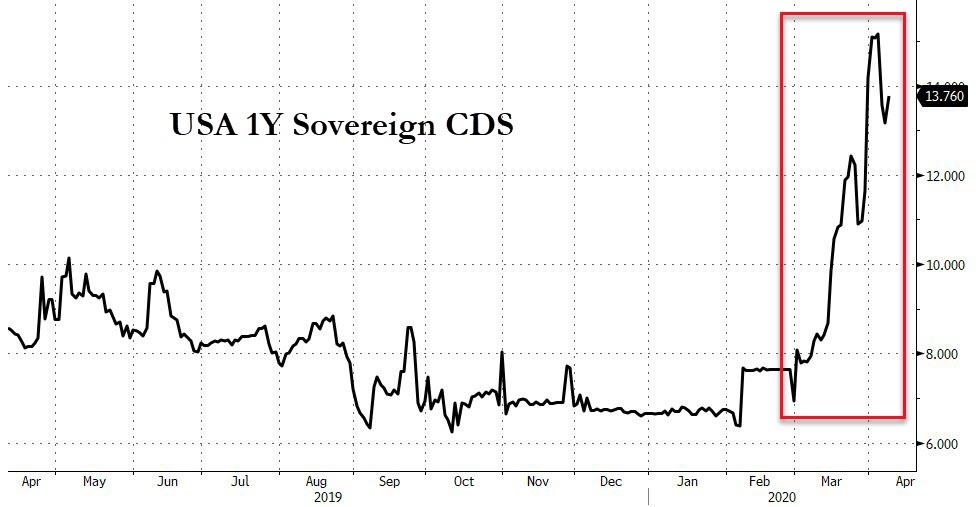

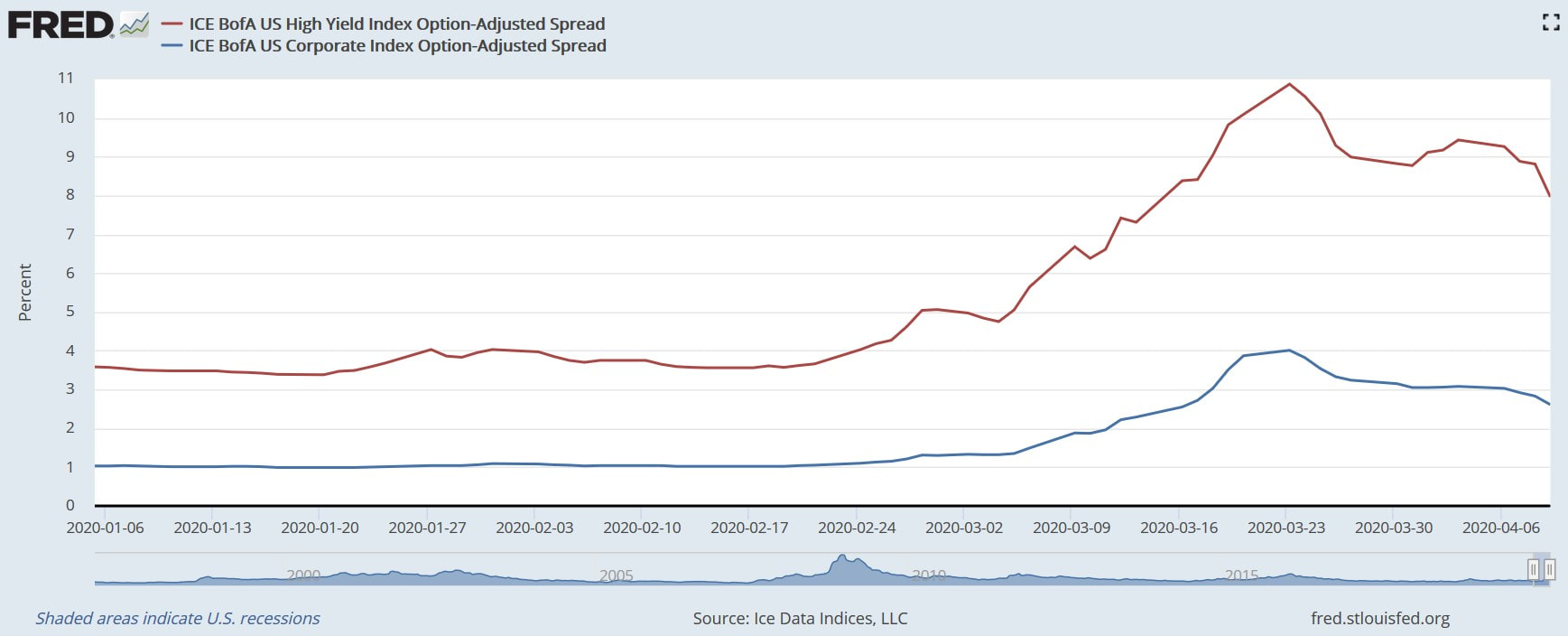

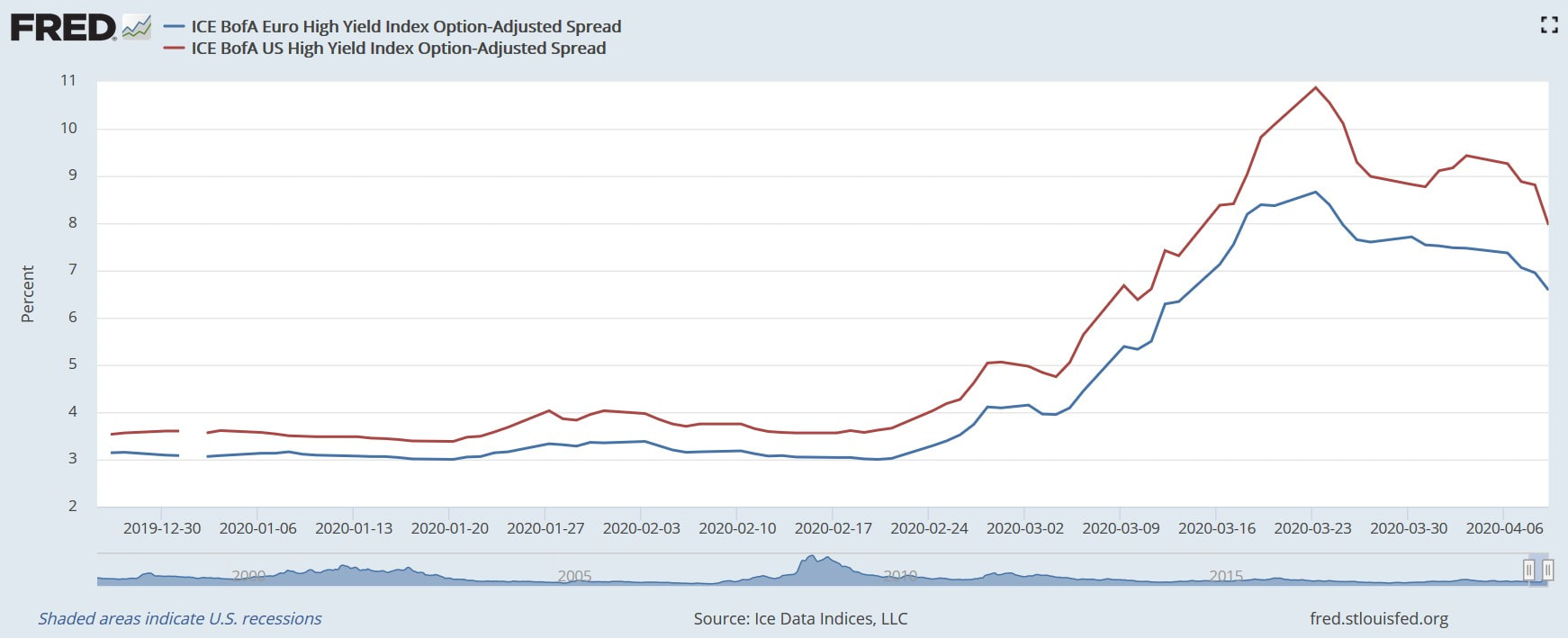

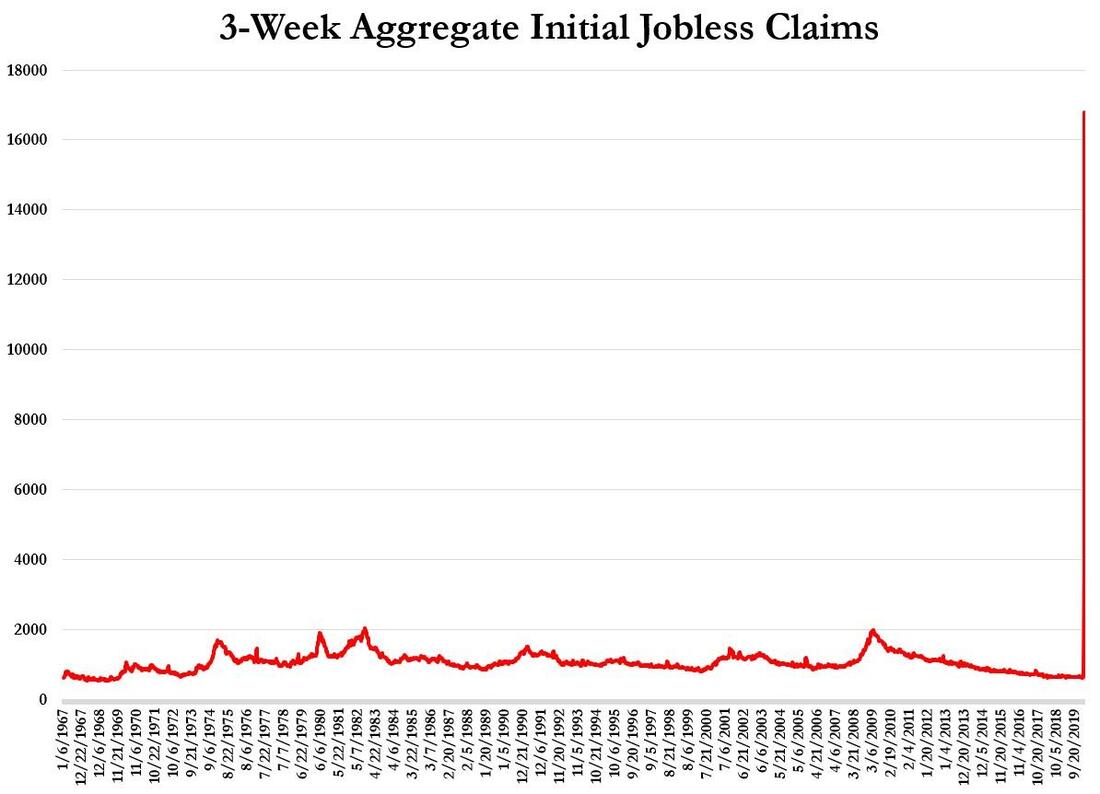

Likewise, the Fed's balance sheet has been soaring at ludicrous speed. Just in the week ending April 8, the total amont of assets in the Fed's possession was $6.083 trillion. Since March 11, total assets increased by about $1.771 trillion.  As I previously stated, the Fed expanded its central bank liquidity swap lines and established the FIMA repo operations to deter foreign monetary authorities from getting rid of their UST holdings and, consequently, to prevent the yields of the Treasuries from shooting up, so that these foreigners would get their much needed dollars from other sources. Hence, for the last weeks, the amount outstanding on those dollar swap lines have been increasing, though they remained at the same level this week compared to the previous one: on March 19, $162.49 billions; on March 26, $308.06 billions; on April 2, $395.86 billions; and on April 9, $396.65 billions. Additionally, the foreign holdings of US Treasuries held in custody at the Fed continues to plummet. On March 11, the amount in custody was $2,961.62 billions. That value diminished to $2,843.67 billions on April 8. Therefore, in the last 4 weeks, foreign officials and other international authorities with accounts at the Fed dumped, aproximately, $118 billions.  This decline may be explained by the FIMA repo operations. In such scheme, these foreign authorities are able to exchange Treasuries held in custody at the Fed for USDs. In spite of the alleged scrambling for dollars via the FIMA repos, the amount of Treasuries held by the Fed has gone up much more than what would be enough to absorb those repos. On March 11, the USTs held by the Fed added up to $2,523 billions. In the folowing four weeks, the amount increased by around $1.111 trillions to $3,634.39 billions, on April 8. This means the Fed now owns something like 15.1% of the federal government debt, which surpassed the $24 trillion mark this week.  By looking at the graph below, you can see the dollar liquidity became more stressed till Wednesday, April 8, having alliviated significantly on Thursday. Accordingly, only when those facilities mentioned above were announced, did liquidity concerns rest.  However, the dollar decreased nonstop all week. Although there had been liquidity uneasiness, there was no rush to cash. Usually, when this kind of stress arises, there are flights to safe havens, such as the greenback. Thus, seeing that the USD went down at the same time liquidity stresses were present, this could be a sign the faith in the dollar is being lost.  Moving on to Treasury yields, despite the Fed having accumulated more US notes and bonds in its possession, their yields rose, implying that the demand for them decreased.  Yet, the perceived sovereign credit risk has waned slightly. Since the US risk of insolvency went down while the yields of bonds plus the stock market climbed, investors must be thinking the global lockdown is about to end. Or is there another reason?  Furthermore, corporate bond yields are having their spreads tighten, specially the HY bonds which is not a surprise when you bear in mind the Fed is going to take as collateral (or purchase rather, to speak correctly) junk bonds.  Across the pond, sentiment has ostensibly started to turn around. Even though the daily number of cases and deaths due to COVID-19 refuses to subside, investors seem to take the view the worst has passed.  Although the Euro Area finance ministers failed to reach an agreement to aid the poor and fragile South in supporting their economies, the European stocks rallied this week. (CAC 40 in red and IBEX 35 in orange)  Inversely, in the actual world, the lockdowns persist and the economic indicators have begun to rear the economic halt's ugly head. This week's figure of the US jobless claims stands at 6.606 million. In the last three weeks ending on April 8, 16.78 million people have applied for unemployment benefits, as the chart below demonstrates.  Finally, considering that the economy is contracting at an unheard of pace to most of us, how come are the stock and corporate bond markets surging, the US sovereign credit risk lowering and the dollar liquidity constraints vanishing as well? The reason are the machinations of the central bankers and the keynesian technocrats. With the Fed commiting to intervene in every realm of the financial spectrum, the Fed has become the BUYER of everything. In addition, its interventions preclude the healthy and essential process of price discovery. Therefore, there is no asset price that is still brought about by market participants acting in their best interest, without the distorting influence of the Fed. Instead, everyone has become complacent in this Fed ruled paradigm, where everyone expects the Fed to come to the rescue once problems ensue, even if it means the Fed and the other central banks have to buy every asset of every market, in order to prevent losses for the participants. On that account, it is no wonder the price-to-earnings ratio (P/E) of the S&P 500 has just exceeded, by some estimates, the previous high of the Obama/Trump bull market, reaching a multiple of 19.4x.  To conclude, the pretext for what has been happening in the last few weeks with the utterly opposing trends in the financial markets and the real economy is the Cantillon effect - check out the Inflation section to find out more - on steroids. The US stock market has had one of its best 3-week performance, while the economy is halted almost completely and with the joblessness numbers skyrocketing to levels never seen before. Therefore, there is no shadow of doubt the markets have been moving, not by the fundamentals of the actual economy, but by the inflation whims of the Fed and the other central banks.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed