|

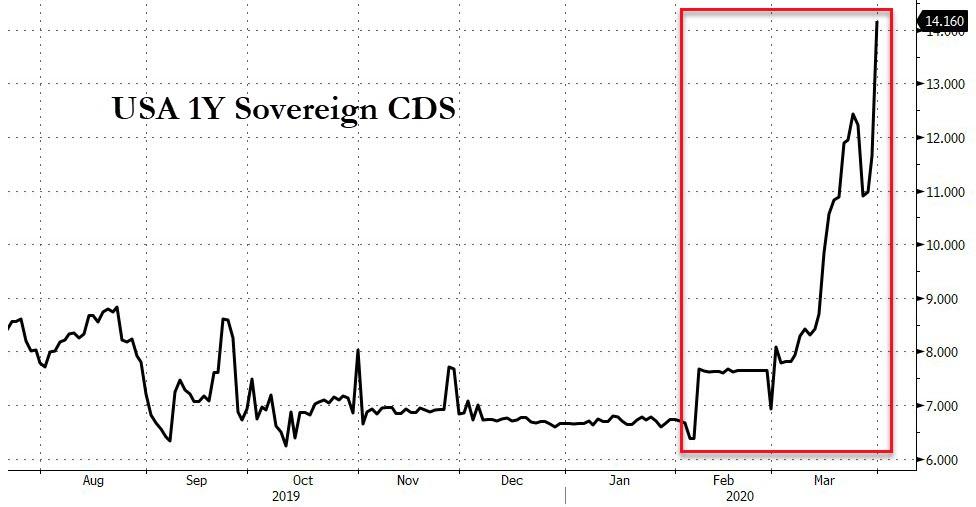

On the post, Painted into a corner: the Keynesians have just checkmated themselves, I claimed foreign governments and central banks would start to liquidate Treasuries, among other USD-denominated assets, in order to fulfill their dollar obligations: "(...) foreign governments will also be liquidating Treasuries to obtain dollars to satisfy their liquidity demands. As of now, Treasuries are still regarded as safe havens. However, when investors realise US insolvency risk is rising (look at the graph below), the safe haven status will fall. In any case, foreigners are getting the dollars they need via other means. One of those is the dollar liquidity swap lines between the Fed and foreign central banks. The Fed has had agreements in place since 2013 with 5 other central banks: ECB, Bank of England, Bank of Japan, Swiss National Bank and Bank of Canada. Yesterday, the Fed announced temporary dollar liquidity swap lines with 9 more central banks in Australia, Brazil, Denmark, Mexico, New Zeland, Norway, Singapore, South Korea and Sweden. It will not be long for them and others to lose faith in the Treasury creditworthiness. Additionally, foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. Nations with dollar-centric supply chains in their domains, such as China, South Korea or Taiwan, will probably have to unwind their long-dollar fx swap positions and sell Treasuries in order to release the necessary liquidity." Well, it seems the liquidity swap lines provided by the Fed has not sufficed. In the week ending March 25, the holdings of Treasuries in custody at the Fed on behalf of foreign monethary authorities dropped by $58 billion, taking the total weekly average to $2.891 trillion. This is the lowest amount since April 2017, when the national debt was $19.8 trillion, almost $4 trillion lower than today's $23.7 trillion.  In monthly terms, March saw those Treasury holdings in custody plummeting by a record $109 billion.  In addition, according to lagged Fed data, primary dealers' holdings of Treasuries had surged to $272 billion as of March 18, from $193 billion at the start of February. Interestingly, this could be an indicator that central banks are getting rid of their USTs, as foreigners sold their positions to dealers. Hence, just from these two - Treasuries held in custody at the Fed and official accounts at the primary dealers -, during the month of March, foreign central banks and the like dumped, at least, $190 billion worth of Treasuries. In response, on Tuesday March 31, the Fed announced a procedure similar to the repo operations the Fed has been doing, since September of last year, with the primary dealers. Accordingly, the new operation is targeted at foreign and international monethary authorities (FIMA) and, thus, it is called FIMA Repo Facility. Naturally, foreign central banks are going to be allowed to exchange Treasuries held in custody at the Fed for US dollars. Furthermore, just a week after the Fed expanded its liquidity swap lines and included nine other non G5 central banks to the list of counterparties, it has found that this is not working and is now handing out dollars straight against US securities, mainly Treasuries. But why are those swap lines insufficient? Could it be because of prohibitive interest rates? Hardly. the (annualised) interest rates on swaps with the G5 central banks have ranged between a mere 0.37% and 0.45%. That does not seem at all disadvantageous. Therefore, in my opinion, foreign central banks and other authorities are not liquidating Treasuries relunctantly so as to get the greenbacks to meet their obligations. They could easily be getting them through the swap lines. Obviously, foreigners are worried about the creditworthiness of the US government to pay its debt, and about the stability and value of the dollar.  Additionally, the purpose of this facility is, according to the Fed, to allow FIMA account holders, i.e. central banks and other monetary authorities with accounts at the New York Fed, to enter into repurchase agreements with the Fed. In these transactions, FIMA account holders exchange their Treasuries held with the Fed for dollars, for a period of up to three months, which can then be made available to institutions in their jurisdictions. In its statement, the Fed also claims "[t]his facility should help support the smooth functioning of the U.S. Treasury market by providing an alternative temporary source of U.S. dollars other than sales of securities in the open market".

Moreover, the reason the Fed is persuading these foreign entities not to sell Treasuries and other US securities is that the Fed is the only buyer. Seeing that such a liquidation would result in higher yields in Treasury securities and the US government cannot afford to service greater debt expenses, the Fed would have to absorb them to keep the yields at low levels. However, this would crank up the Fed's balance sheet, inflating the currency supply. Consequently, the dollar will carry on devaluing, completely smashing the faith in it and, hence, in this debt-based economic system. To conclude, the Fed does not want any selling of Treasuries as the world's most liquid market is now suddenly extremely illiquid, and ongoing sales will only further destabilize it. In addition, this program is supposed to be temporary, lasting only until the impact of the COVID-19 vanishes and everything goes back to normal, to the greatest booming economy in the history of manking. Right? As I have been explaining, the dollar standard is doomed due to the extreme debt magnitudes finally crashing the system, meaning that the Fed is going to keep this facility, not until it chooses to do so, but up to the point when the foreign monethary authorities get fed up. No pun intended!

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed