|

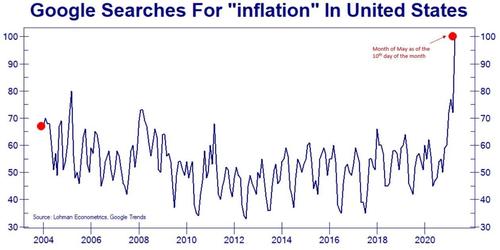

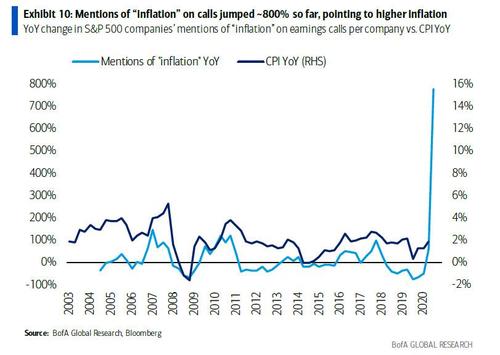

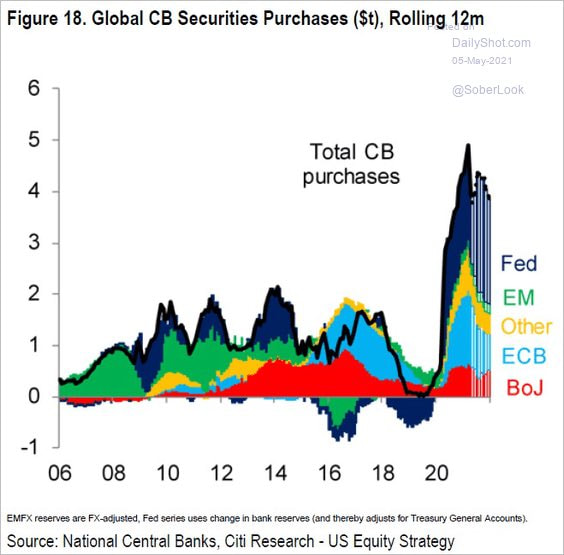

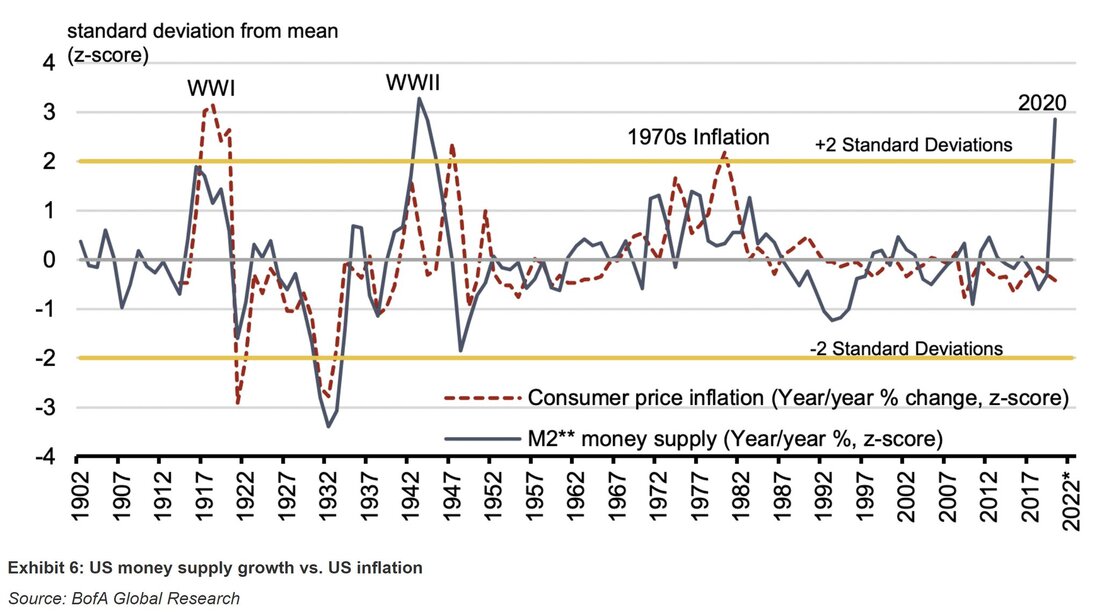

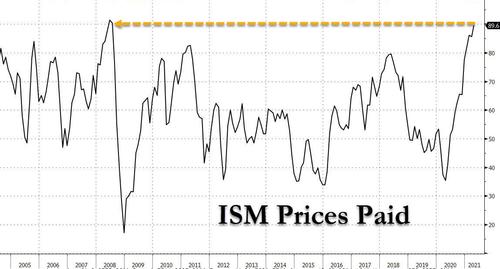

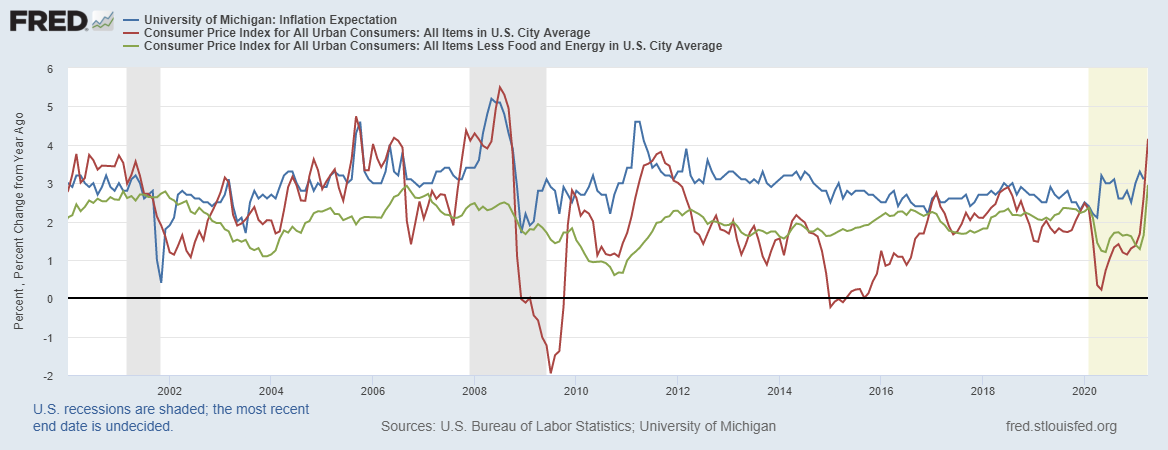

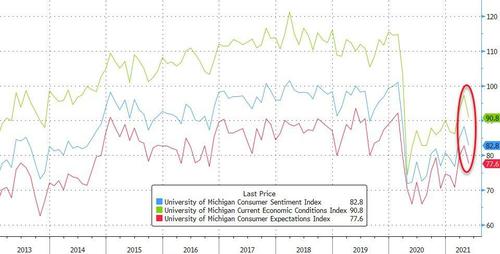

Without a shadow of a doubt, the theme that has pervaded the financial markets this year so far has been inflation, as in, a repeat of the 1970’s is upon us. Like I have been continually reporting, such a scenario, in the foreseeable future, is pure fantasy, having no basis on reality. Notwithstanding, the pundits on tv, the journalists and the “experts” in Wall Street and academia have been very successful in transmitting this narrative to the public. Owing to being bombarded by a barrage of stories and anecdotal evidence of rising prices, the commoners have suddenly grown watchful of the emerging inflation. This much is represented in the top graph that shows the Google searches for the word "inflation". Accordingly, the interest has been soaring like never before. Naturally, due to the data going only all the way back to 2004, you have to take this with a pinch of salt.   However, it has not just been the usual suspects in the media that have pushed this narrative. As the above chart demonstrates, companies have been more vigilant inflation-wise. In comparison to last year’s Q1, the mentions of "inflation" on the earnings calls of S&P 500 companies have jacked up almost 800%. Could this mean that the CPI annual rate could reach double-digit territory, as the graph implies? Obviously not; this statistic is not indicative of anything. In fact, the CPI figures for April have already been released and the YoY rate is a mere 4.2%. Unsurprisingly, after having suffered in Q1 2020 the biggest deflationary shock since the Great Depression, it would be reasonable to assume there would not be a lot of mentions about inflation. Therefore, following that massive Covid crash, which followed a terrible year of disinflation in 2019, where the term "inflation" practically disappeared from the lexicon – as depicted by the chart that shows an almost 100% drop in mentions -, any slight increase in absolute terms would entail an enormous jump in relative ones. Looking at the next couple of charts, how can anyone believe the Pandora's box of inflation has not been opened. The writing is on the wall. Because of colossal large-scale asset purchases by, especially, the major central banks (top graph) since March 2020, the inflationary inferno is bound to be kindled.   If you still have any doubts, just heed the warnings the graph above is sending. On the whole of last year, the monetary aggregate M2, which everyone thinks it represents all (or close to that) the monetary forms, denominated in dollars, in existence, mushroomed at a pace not seen since World War II. Notice what happened to the annual rate of change of consumer prices (red line) in that period; it went up... fleetingly (oh boy!). LIkewise, during WWI and the Great Inflation of the 1970's, consumer prices followed the surge in the M2 aggregate. On that account, why would this time be any different? Surely, prices are going to have to soar at least as much as the decade of the 70's. As the following chart shows, prices paid by the producers, according to the ISM Manufacturing survey, have been climbing at a rate not seen since the middle of 2008 - not a good signal. Hence, it is only a matter of time till the rising costs of production are passed on to the consumers, reverting once and for all the deflationary/disinflationary environment that has hitherto haunted the global economy.  As you know, if this is not your first time here, I am just being provocative. The truth is inflation is controlled by the participants in the eurodollar system, not the central banking technocrats. Thus, proper inflation - meaning rapid growth of the money supply - will only occur insofar as banks and other credit originators perceive the conditions in the economy and the financial system are adequate for expanding credit, like they did prior to the GFC1. Before you start berating me about the quality of the governments' price statistics, which are immensely tampered and not to be trusted, I agree with you. In fact, that was the topic of my first post. In it, using the ShadowStats guidance, I uncovered the shenanigans that the bureaucrats at the Bureau of Labor Statistics (BLS) were doing to hide the true depletion of the dollar's purchasing power. In short, in the mid-1980's, the BLS began doing hedonic quality adjustments. Then, for that not being enough to keep the "inflation rate" under reasonable figures, in the 1990's, the methodology was pushed further into a substitution-based calculation, in which substitution of lower-priced and lower-quality goods in the basket is made with the intent of lowering the reported rate of inflation versus the fixed-basket measure. Be that as it may, in view of the CPI not having suffered any more changes in its methodology since the last decade of the twentieth century, we can safely compare the CPI figures of today and the naughties' ones, prior to the GFC1. Curiously, in spite of all the "money printing" by the central bankers, the CPI rates have actually been lower since then, with the most recent figures breaking the shackles (somewhat) - due to supply squeezes, mainly, and base effects too (top graph). Interestingly, before the GFC, consumers were very accurate in their expectations of inflation, as per the University of Michigan. Despite that, since then, consumers have been terrible at forecasting the BLS' rate of inflation, consistently overestimating the loss in the purchasing power; not just for the next year, but for average of the next five, albeit they have been closer in forecasting the latter one (bottom left chart). Nevertheless, the consumers' perception of economic conditions, both present and future, have been rather dreadful, as the bottom right chart portrays. So, to recap, inflation expectations are climbing, while consumers are sensing a lousy economic landscape. Certainly, "stagflationists" ears must be burning.

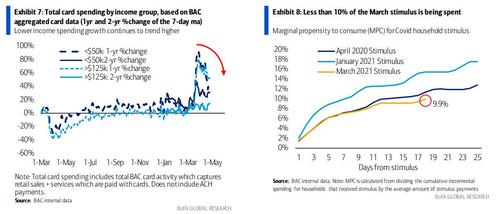

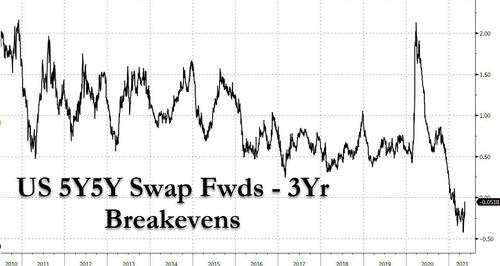

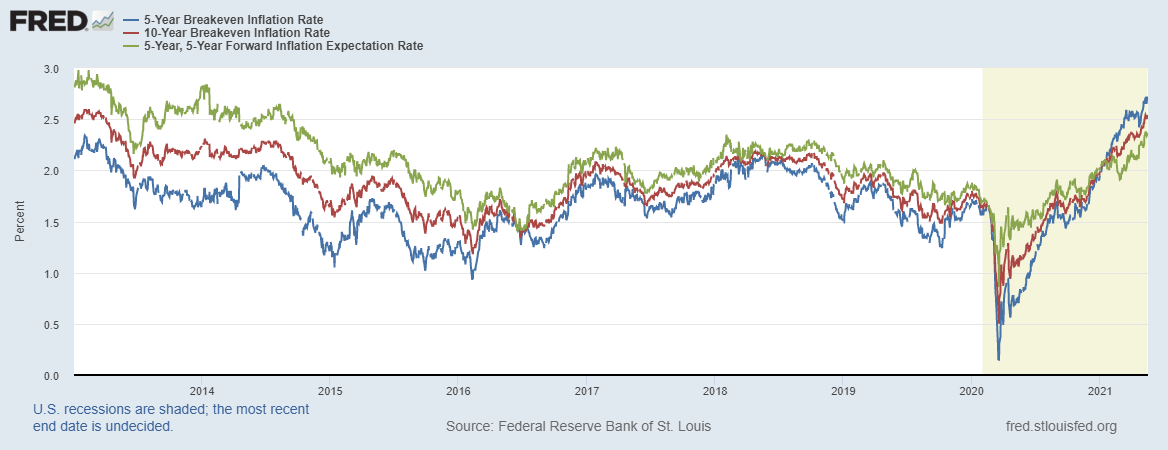

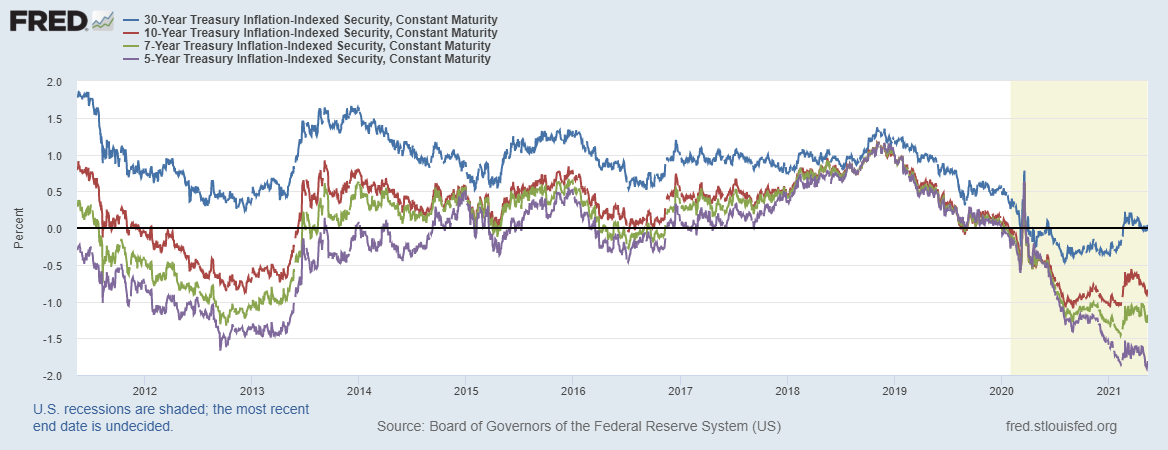

In addition, the annual rate of the CPI soared in April, besides the supply squeeze and base effects, because the US federal government decided to pamper its electorate, sending out three rounds of stimmy checks. Undeniably, the surge in consumer demand that these handouts generated, at a time when production and transportation were being restrained or even outright halted, led to higher prices. Yet, this inflation has remaind largely contained in the realm of producers for not being able to pass the costs on to the consumers. Unfortunately for the Keynesians who have promoted these policies, they are no longer having the desired effect of triggering a consumption-led recovery. As the graph on the righ demonstrates, consumers are preferring to save a bigger chunk of this latest stimmy check in comparison with the other two.  Revisiting the TIPS market and the breakeven rates like we did last week, the message coming from them remains the same. Although prices are rising, they are simply a transitory phenomenon provoked by government-imposed restrictions. Emphatically, the spread between the 5-year forward rate and the 3-year (not forward) breakeven rate (bottom chart) has been considerably negative since the beginning of the year. Despite the spread has gradually been approaching positive territory, on account of the 5-year forward has been climbing a bit, implying higher future expectations of inflation, they are still very subdued relatively to historical standards. The fact that the real yields are close to or at all-time lows tells everything you need to know about the sentiment of those in the financial system.

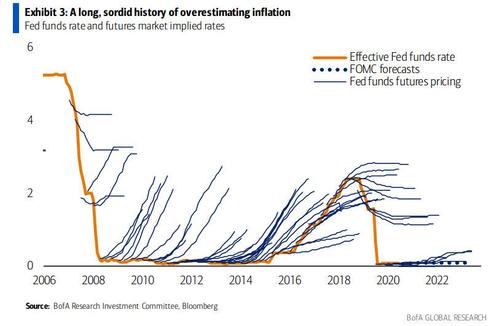

To cap it all off, even though the financial media and FinTwit have been ridden with chatter about the upcoming QE tapper by the Fed, we shall resist the pressures of the echo chamber, remain intelectually honest and guide ourselves only on what is fundamental, tuning out all the noise. In spite of being a market-based indication, Fed funds futures are part of the noise, as the graph below shows. Even if they are right, they are merely suggesting that by the end of 2023 the Fed funds rate will be half a percent. That is still awful, being just a little bit better than the absolute worst experienced last year.  In conclusion, do not get swindled and carried away by the putative experts and the overload of articles and commentary on the brewing inflation. These people do not understand how the monetary and financial system works, owing to believing the central banks are exactly that, playing a pivotal role in the expansion of money and, more importantly, in the direction of the economy. In a nutshell, the system evolved, but the experts did not; the eurodollar regime completely changed the way credit is formed and provided, throwing all prior conceptions of financial intermediation to oblivion, and still these fools, both the "stagflationists" and the mainstream economists and central bankers, are absolutely unaware of the implications of such monetary revolution. Regardless of such stubborness, the eurodollar system remains in place, albeit languishing and awaiting for its replacement. In view of not having any new setup ready and standing by, though there may be some in the making (e.g. DeFi and CBDC), we are going to have to wait awhile for what will hopefully be an upgrade - better pull up a chair. In the meantime, try to knock some sense into their heads, despite how hard that may be and how closed-minded they are.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed