|

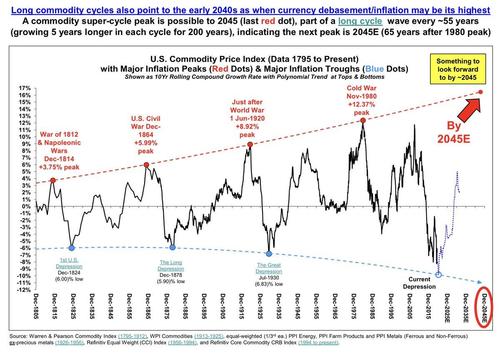

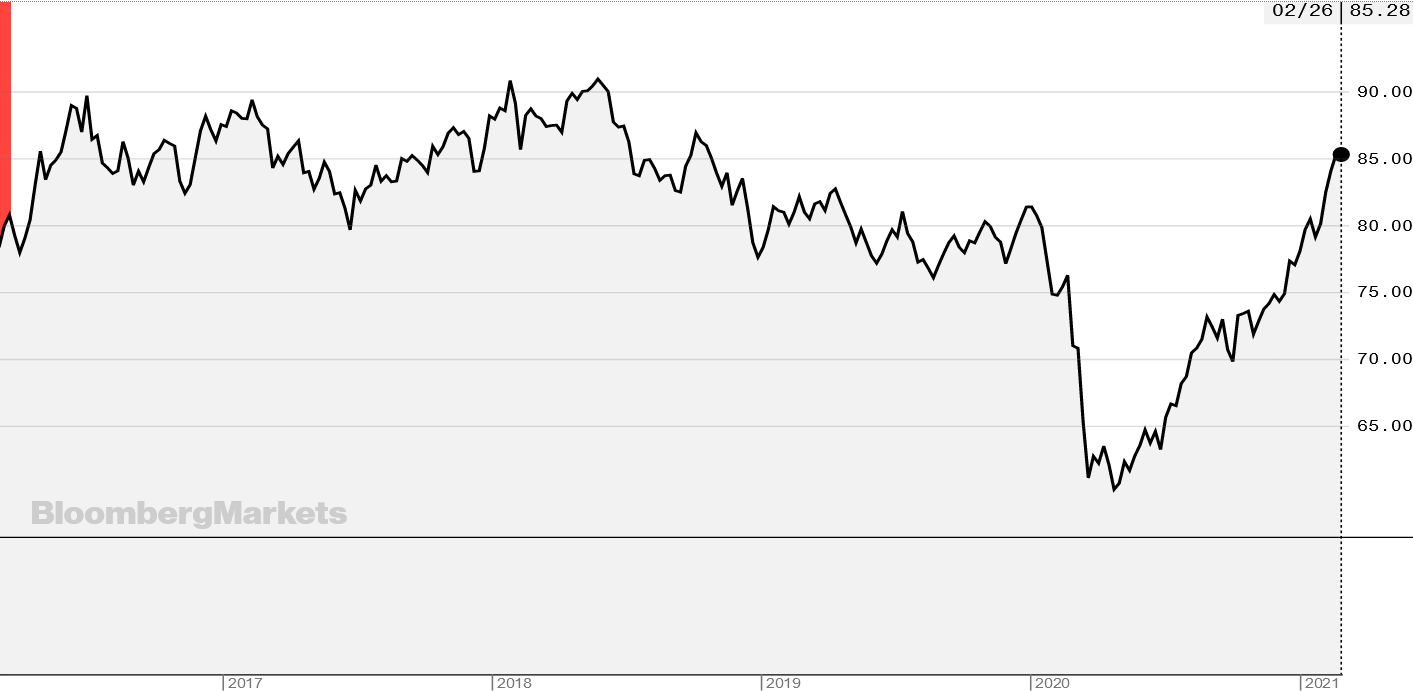

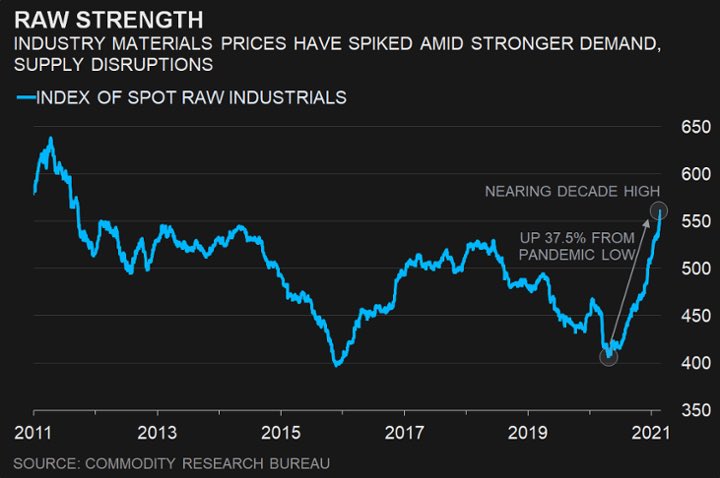

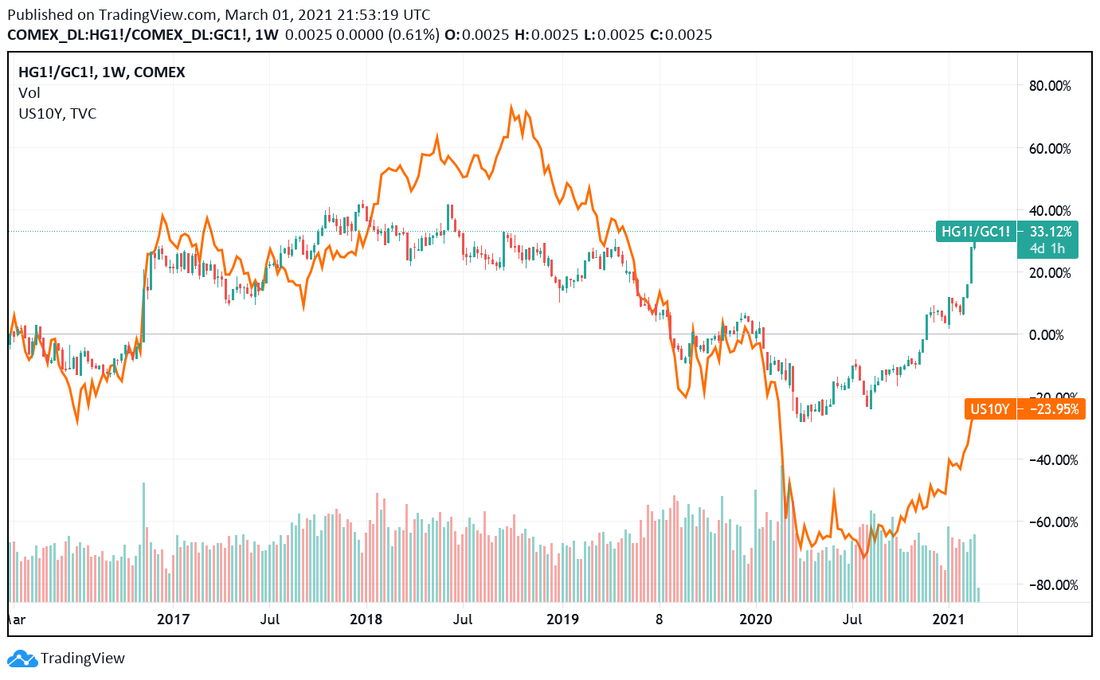

For almost four months, since the honourable and ultra-charismatic orator Joe Biden rallied a record number of voters (that even raised the dead), to get fascism and white supremacy out of the White House, and the discoveries of vaccines for the kung-flu, sentiment on the part of pretty much everybody has improved. On the one hand, the vaccines "injected" a sense that life would return to normal, the "old" normal, and not stuck in this twisted and abhorrent "normal" we have been told to be necessary (to flatten the curve, not to kill granny, or something like this). On the other hand, as the medical community was on a crusade to find the vaccine, the stimulus and financial aid which were going to be put together by governments, especially the ones engendered by the Biden administration and the soon-to-be Democrate-controlled Congress, were aimed at supporting the economy so that the house of cards would not collapse in the meantime. As a result, and because of the public's reverence for technocrats to boot, (most) markets began to price in an economic recovery, or at least the initial steps of one, as businesses started to perceive a better economic outlook than previously surmised, albeit households do not appear to share the same view. To wit, some of the markets that have been hinting at recovery more strikingly are the commodities. Although that is what some analysts take from them, are commodities really suggesting an inflationary boom? Are the "Roaring 20's" staging a comeback? Among the financial institutions which take this view there are JP Morgan, Bank of America and Goldman Sachs. In their opinion, the commodities secular rally will be a story of post-corona-phobia economic recovery, as well as "ultra-loose monetary and fiscal policies". In addition, commodities may also jump as an unintended consequence of the fight against climate change, which threatens to constrain oil supplies while boosting demand for metals needed to build renewable energy infrastructure and manufacture batteries and electric vehicles, namely cobalt and lithium for example. Furthermore, commodities are typically viewed as a hedge against inflation, which has become more of a concern among investors. In the end, as if we are in some post-war period in which there is a large-scale effort to rebuild what was destroyed, owing to tremendous demand, prices of raw materials are going to skyrocket for the next quarter of a century, following the depiction below.  For now, commodities' prices have indeed surged since the lows of the March Meltdown, having even reached multi-year highs, as the next couple of charts show. In spite of the rally in the Bloomberg Commodity Index (top graph) seeming to be somewhat extraordinary, its performance pails in comparison to the one in the Index of Spot Raw Industrials (bottom chart). By taking a look at this, it makes you wonder if the inflation spigot has been tapped at last.   Notwithstanding, on Friday, February 28, "[t]he return on commodities as measured by the 23-member Bloomberg Commodity Index dropped the most since April as a strengthening dollar reduced the appeal for raw materials priced in the currency. Meanwhile, a surge earlier this week in US government bond yields has fed into increasing concerns that accelerating inflation could lead to easing monetary policy support", Bloomberg reported. To begin with, as I have explained in the Eurodollar system series (see part I, II, III and bonus), rising UST's yields are indicative of improving financial and economic conditions (i.e. money creation is easy), which always happens after an economic contraction or just deceleration reaches its trough. Similarly, the US dollar falls in relation to its peers, particularly those in the EM domain, when growth prospects are favourable. Thus, affirming the accelerating inflation has arisen on account of the "accommodative monetary approach [(translation: low yields)] that helped fuel the recent price gains", having just in the previous sentence alluded to the recent uptick in the dollar, it tells you something is amiss. By turning our attention to the next graph on the left, the yield of the 10-year Treasury (orange line), even though it has climbed quickly, meaning market participants are foreshadowing an improvement in the monetary landscape in the long-run, the copper-to-gold ratio implies much more pronounced growing expectations, albeit still short of pricing in the much-awaited recovery. On the flip side, seeing that the dollar, has not only stopped dwindling, but has, since this year broke out, gone up a bit, financial conditions have, according to the greenback, been getting uptight lately.

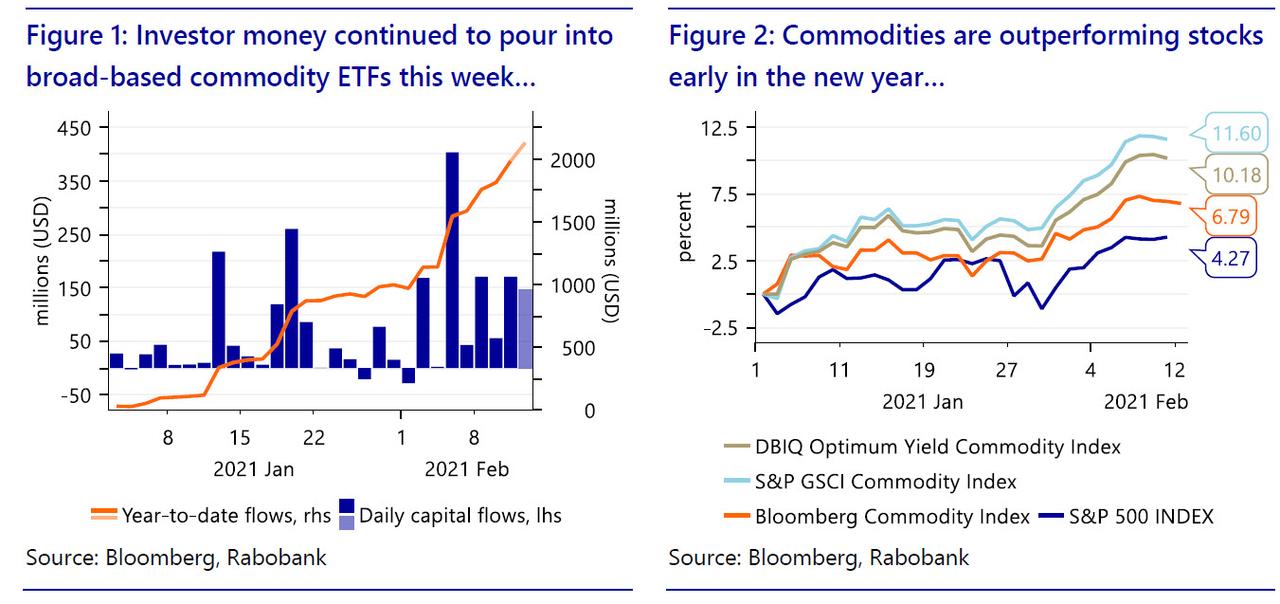

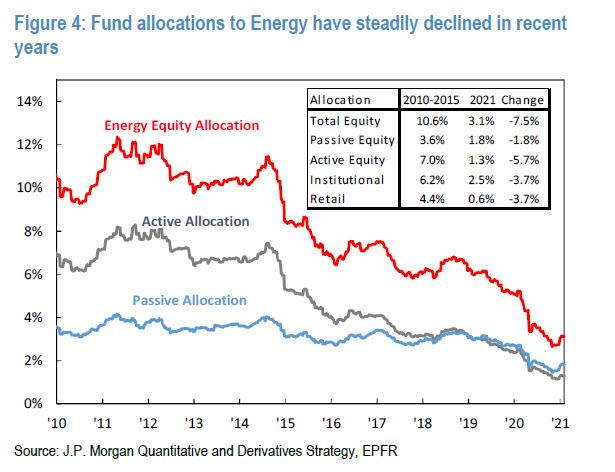

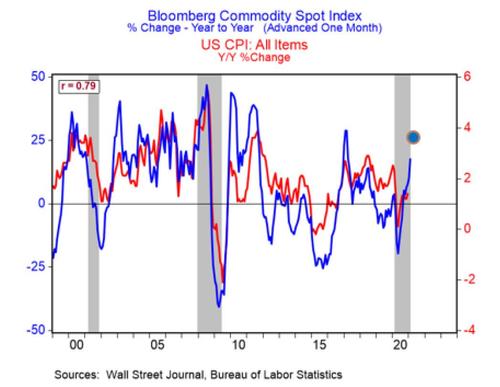

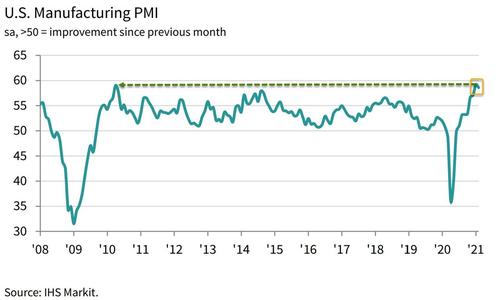

Hence, despite troubles in the present, a burgeoning economy awaits us in the (distant) future. As the saying goes, patience is a virtue. However, as they have demonstrated many times throughout the times, investors seem to lack several virtues, patience being one of them. Since the beginning of the year, investors have piled in the commodities realm (left chart), greatly contributing for the commodities' outperformance in relation to the stock market (right chart). Curiously, this current "mania" has, on the face of it, bucked the decade-long trend in energy fund allocations (bottom graph). If the supercycle in commodities is actually in the cards, then stocks like the energy sector are the bargain of a lifetime.   Moving on to the real economy, the soaring prices for raw materials have been taking their toll in the economy, probably causing more harm in the near-future. "Timber growers across the US South, where much of the nation's logs are harvested, have gained nothing from the run-up in prices for finished lumber. It is the region's sawmills (...) that are harvesting the profits", writes the Wall Street Journal. In fact, the glut of timber is so great "that mills are paying the lowest prices in decades for logs." Evidently, the corona-phobia, and the measures imposed because of it, has led sawmills to run "close to capacity", rendering them "unable to keep up with lumber demand." Moreover, according to Bloomberg, the corona-phobia "upended food supply chains, paralyzing shipping, sickening workers that keep the world fed and ultimately raising consumer grocery costs around the globe last year", leading to farmers, which for instance raise cattle, hogs and poultry, "getting squeezed by the highest corn and soybean prices in seven years (...) [lifting] the costs of feeding their herds by 30% or more." In the coming months, "higher price tags for beef, pork and chicken around the world" will be the consequence of producers seeing their profit margins being squeezed. The CPI is not going to reach YoY 4%, as commodities are suggesting on the next chart, in view of consumers lacking the purchasing power to sustain such an increase in prices. Because of mass unemployment, few jobs openings and poor wage growth, consumer demand is going to take some time to return to 2019 levels, which, by the way, was a terrifying year on account of being on the verge of recession. Therefore, retailers are only going to pass the higher costs to consumers when they can no longer squeeze their margins any further.  By the same token, the transportation segment of the supply chains have also been obstructed, mainly the shipping industry. The Shanghai Containerized Freight Index (SCFI), which represents weekly spot container freight rates (export) from the port of Shanghai, has a current reading which more than triple its levels in May of last year. Likewise, other freight indices tell a similar story. In a nutshell, the reasons are quite simple. For one, supply growth has shrunk considerably in recent years, with three major shipping alliances having become far more disciplined around capacity. Furthermore, recent supply chains disruptions from a lack of containers (boxes in the wrong place), the kung-flu (lack of staff), geopolitical tensions (China-Australia spat) and weather (US East Coast cold snap; and in Europe to some extent as well) have not helped matters either. Then, on the demand side, consumers have been propped up by government handouts and, more importantly, the vaccines coming online has, like I said above, led many to believe the pre-corona normality is returning in a jiffy. Therefore, due to being aware of these disturbances in the supply chains, companies have been preparing in advance, prompting them to acquire the supplies they need before these get jammed in traffic. Accordingly, the IHS Markit Manufacturing PMI figure, which came from 59.2 in January to the current 58.6, was wrongly buoyed by a substantial lengthening of supplier delivery times amid significant supply chain disruption. Ordinarily a signal of improving operating conditions, longer lead times for inputs reportedly stemmed from supplier shortages and transportation delays due to government-imposed restrictions. The extent to which wait times lengthened was the greatest since data collection began in May 2007. While orders remain nottably lagging, prices of inputs exploded to their highest since 2008 - when oil was trading at $140. As Chris Williamson, chief business economist at IHS Markit, stated, "shortages of raw materials have become a growing problem, with record supply chain delays reported in February, contributing to the steepest rise in material costs seen over the past decade", leading to prices "charged for a wide variety of goods coming out of factories [being] consequently rising, which will likely feed through to higher consumer inflation."

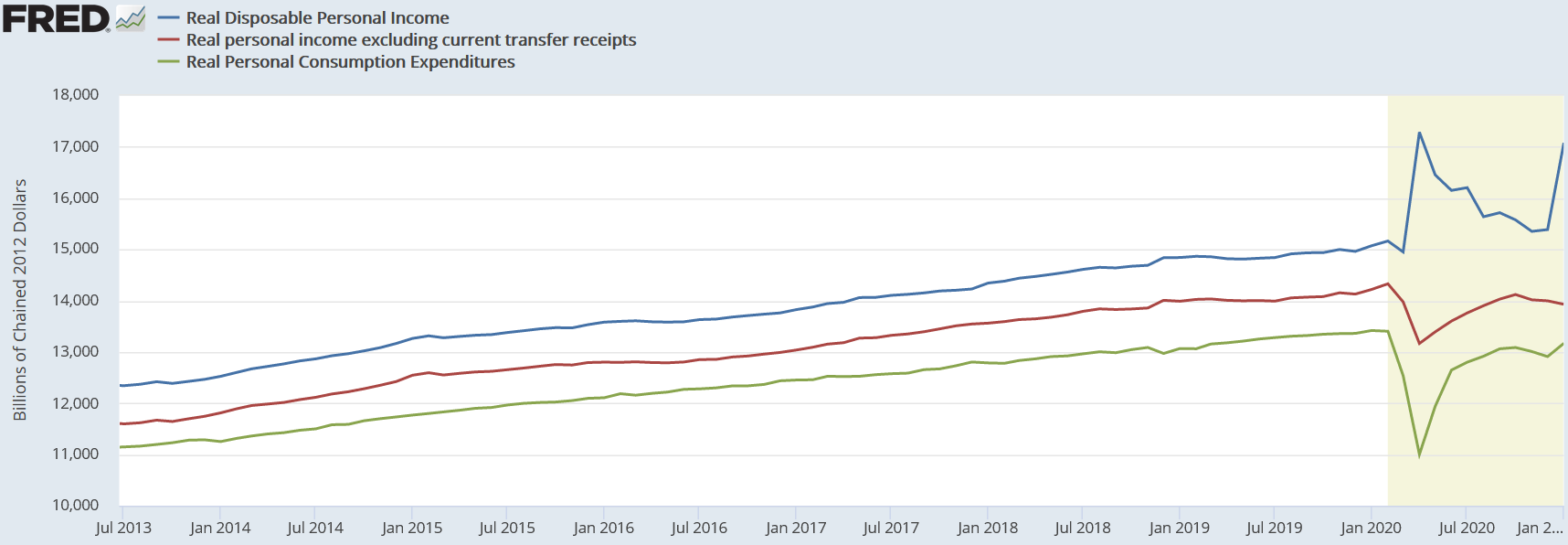

So, we now know why commodities have spiraled lately. Regardless, there is very little backing this trend. For being chiefly caused by government-imposed hindrances because of the corona-phobia, these higher costs will come down as restrictions are lifted. Longer-term trends point to a cooling down for some materials. For starters, the energy transition that heralds a bright new age for green metals such as copper would be built on the decline of oil. Even producers of iron ore, the biggest market of mined commodities, expect prices to weaken over time as Chinese demand starts to decline and new supply comes online. On the coal front, there is an even bleaker outlook with producers looking to exit the market altogether, as the world switches away from the heavy-polluting fuel. Being the major beneficiaries of China's industrial expansion that resulted in the last commodities supercycle, iron ore, coal and oil prospects augur horribly to this conjectured one. On the oil front, prices have recovered as demand rebounded more strongly than many had expected, after reaching the never-imagined $-42 per barrel. Early in 2021, the Organization of the Petroleum Exporting Countries (OPEC) and its allies were holding back crude equivalent to about 10% of current global supply. Long before that, market fundamentals have shifted, especially in the US with the emergence of shale oil. Ergo, haunting traditional producers is the prospect that a prolonged period of high prices would trigger a new flood of supply beyond OPEC’s control, pulling down prices. Despite copper being on a tear in early 2021 thanks to rapidly tightening physical markets as governments plow cash into electric-vehicle infrastructure and renewables, insofar as the iron ore, coal and oil markets dwarf copper in scale, the crank up of its usage along with other methals like lithium and cadmium are going to have an extremely limited impact on the broad commodity basket. To cap it all off, while agricultural commodities have their own particular dynamics, soybeans and corn have rallied to multiyear highs, driven by relentless buying from China as it rebuilds its hog herd following a devastating pig disease (African swine flu). Owing to being more dependent on global economic and population growth, rather than the decarbonization trend underpinning excitement in metal, agricultural commodities have very weak fundamentals to justify prices these high as the world moves forward from the kung-flu. Finally, it is not stimmy checks sent by Uncle Sam, or any other government for that matter, that are going to enkindle the much-anticipated inflationary conflagration. Because individuals sense, and rightly so, the government aid is temporary and inconstant, they are not spending money in proportion to what they are gaining in income, as the next graph shows. As soon as individuals start seeing their bank accounts balloning through their own endeavours in the economic system, as opposed to handouts from the political system, consumption will pick up, although that is naturally taking a lot of time to ensue. Nevertheless, one thing is for certain, as long as society holds this collectivist mindset that is beholden to politicians and technocrats, an economic boom, worthy of this designation, will never happen and, thus, a commodity supercycle will have to be deferred.  Hence, the question remains: what is super about this? As it is usually the case, investors' and analysts' short-sightedness, of course.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed