|

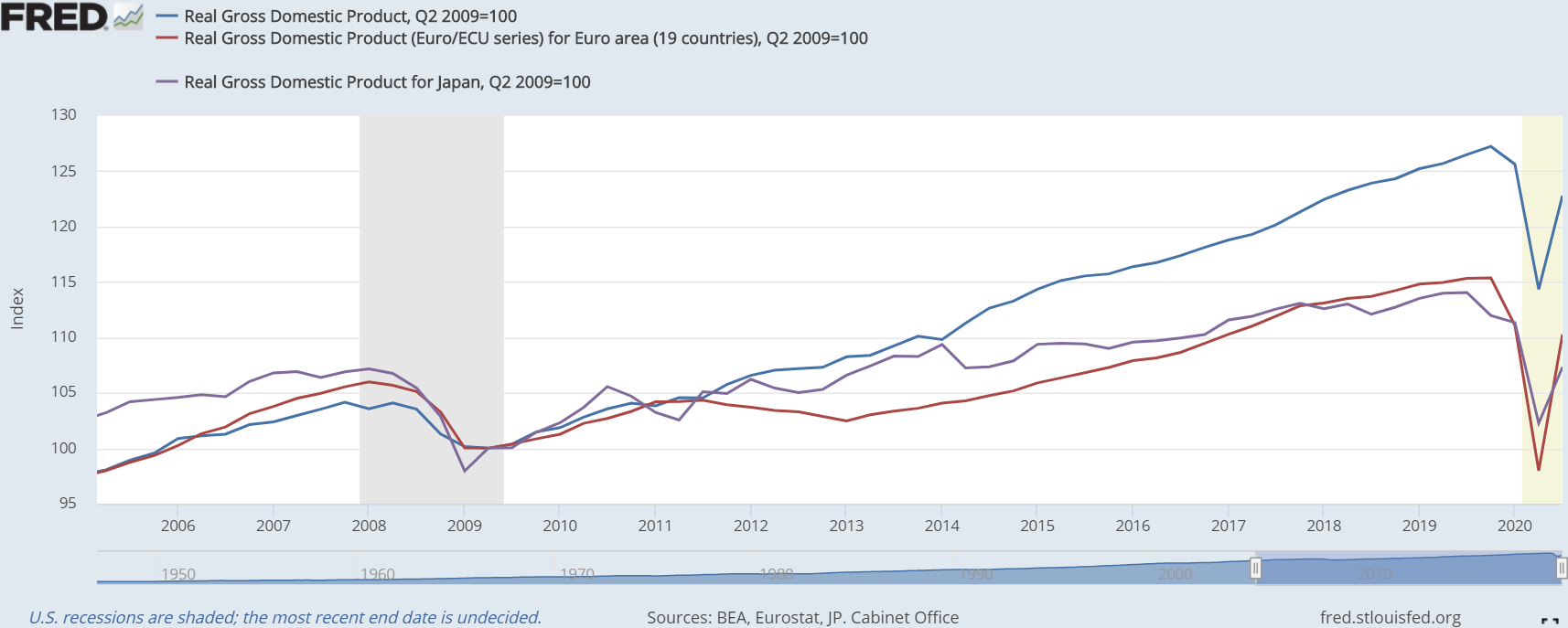

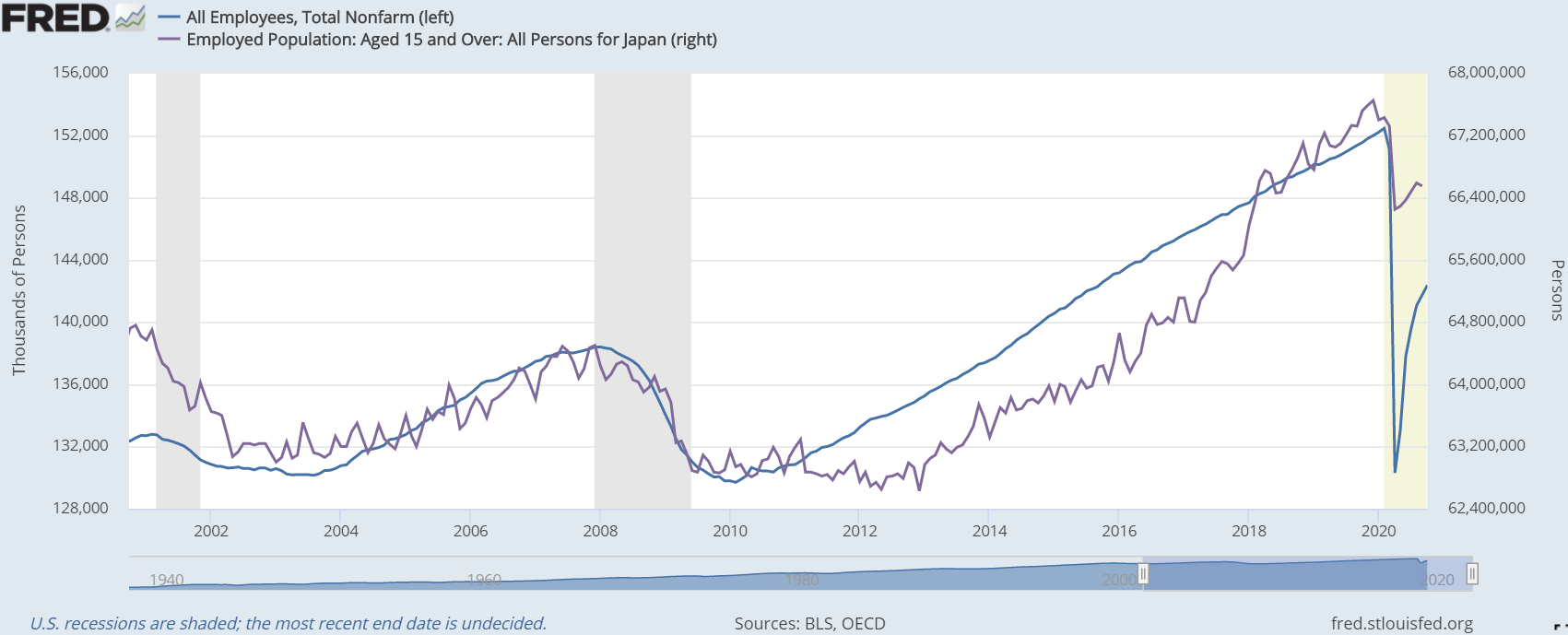

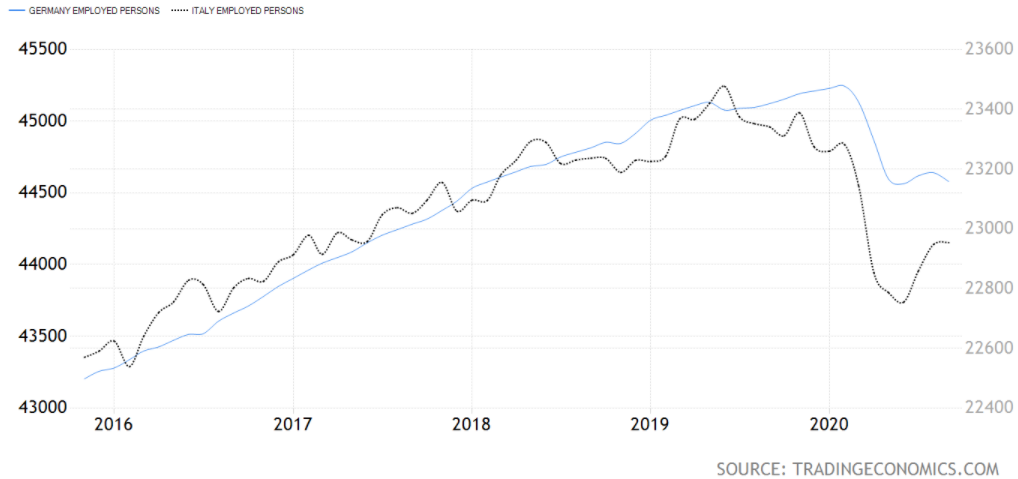

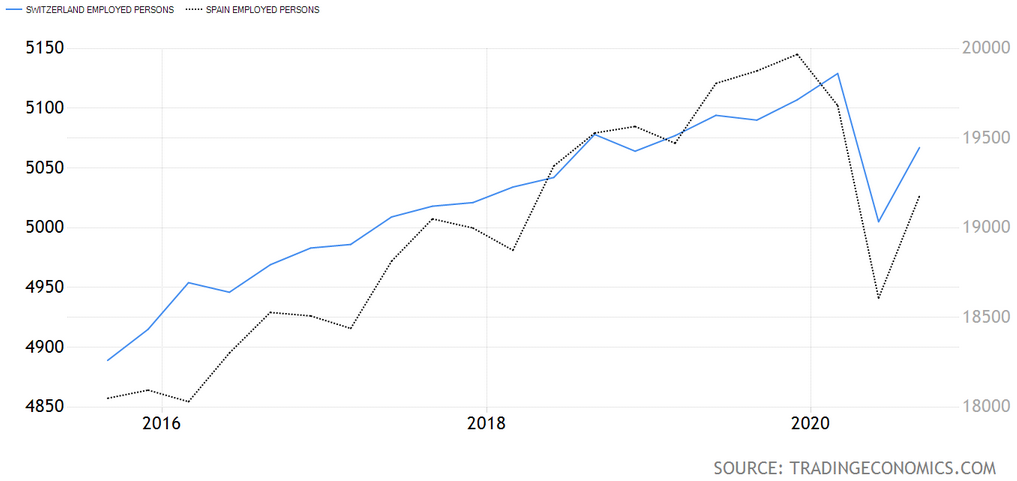

A group of Morgan Stanley strategists unveiled their most recent prospects for the next year, in which they come out very sanguine: "This global recovery is sustainable, synchronous and supported by policy, following much of the ‘normal’ post-recession playbook, (...) Keep the faith, trust the recovery". They have this belief due to more lucid expectations on the coronavirus vaccine, and more certainty on the fiscal and monetary "stimuli" front owing to the ostensible end of the Election Day vagueness - though, it's not over till it's over. Incredibly, Morgan Stanley is not a maverick in the macro analysis domain. In fact, other major banks have expressed the same convictions, such as JP Morgan, Bank of America and Goldman Sachs. In addition, looking at the financial markets and media, a rapid "V-shaped" - or "V-ish", rather - recovery seems to be the common assessment. For instance, according to Jim Paulsen (cited in the last link above), chief investment strategist at Leuthold Group, corporate America’s earnings power may be greatly under-appreciated: "Economic growth has come back a lot faster than people thought and stayed a lot firmer", Paulsen said. "When you take the momentum plus the effect of stimulus plus vaccine discovery, I think growth estimates out there are woefully underestimated for 2021, and that tells me earnings estimates are too". Although the Pfizer and now Moderna vaccine breaktroughs are good news for ending the "casedemic" paranoia, will it also cure the economic malaise? In this three-part series that is the question I am going to answer. To make long story short, the damage is done and we are all going to face its horrible consequences. Hence, this in-depth analysis containing a myriad of economic and financial data is surely going to put this bullish nonsense to rest once and for all (hopefully). To begin with, considering the numbers that have come out since the end of lockdowns and phasing-out of restrictions, on the surface one may feel the economic activity has been resuming at a pace consistent with the "V-shaped" recovery narrative. With that said, on this first instalment, a bunch of data that supports this viewpoint is going to be presented. Nevertheless, do not get your hopes up.  More noteworthily, the GDP growth for the third quarter was the best for most countries in this post-war era. To wit, in the US, the EA and Japan the GDP QoQ rate was 7.4%, 12.6% and 5%, respectively. Surprisingly, these figures caught a lot of people by surprise, not that they were expecting a continuation of the downfall, they just did not believe their belief that such a comeback so quickly was possible. Be that as it may, this single statistic does not tell the whole story. In fact, this spurt is easily explained by the reopening of the economy in the summertime. In spite of resembling a "V", it came up far too short. In order to be a full "V", the right (rising) side has to mirror the left (falling) side. Obviously, the left part is, as of yet, not even half of what it has to be for the "V-shaped" prophecy to be fulfilled. Similarly, employment has soared throughout this period in the small sample of countries that have released the figures of this statistic for the summer months. All the same, one can note a slight deceleration of the job growth, or even, in the case of Germany for example, an inflection to the downside in the more recent months - but I am sure this in no way signals what is right around the corner.

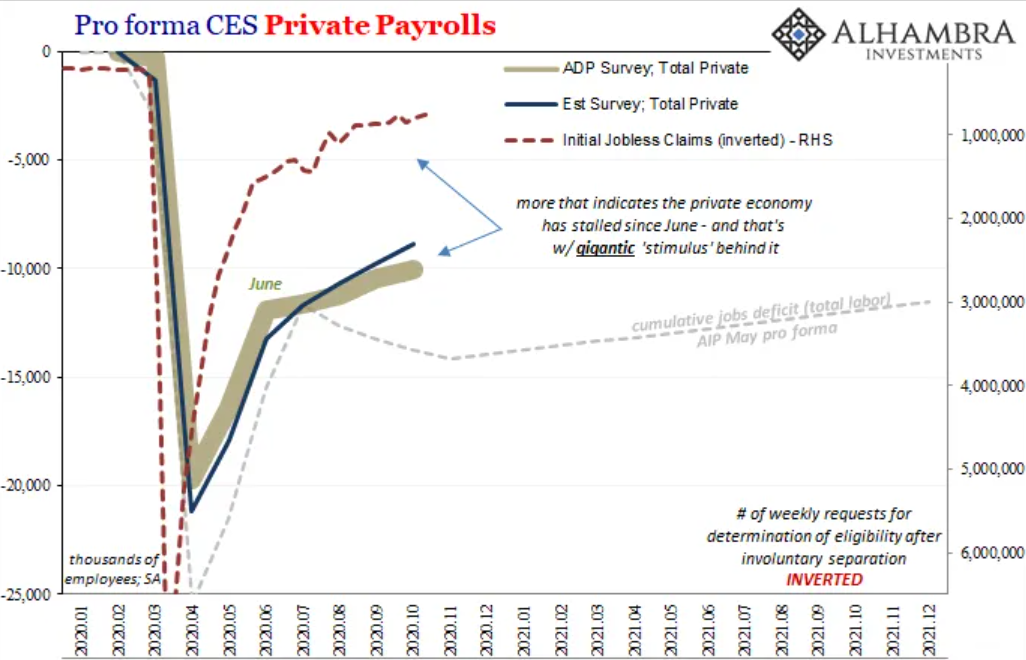

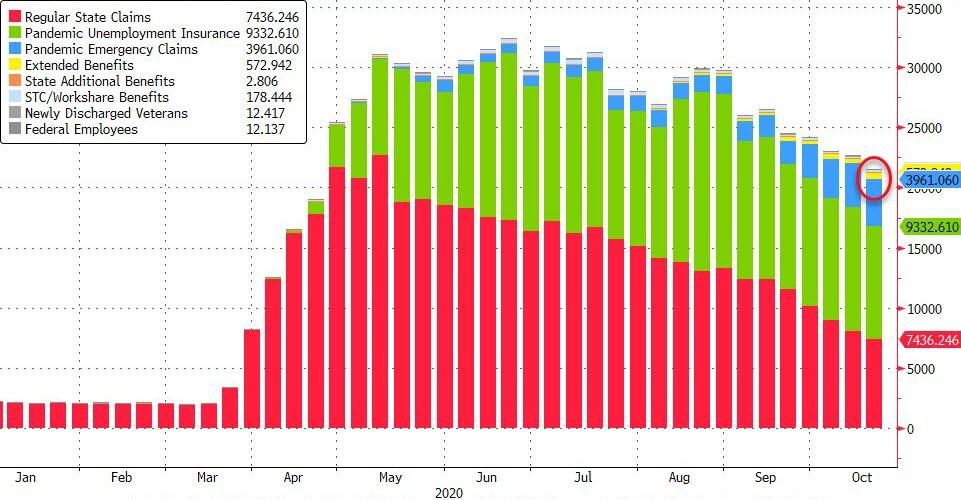

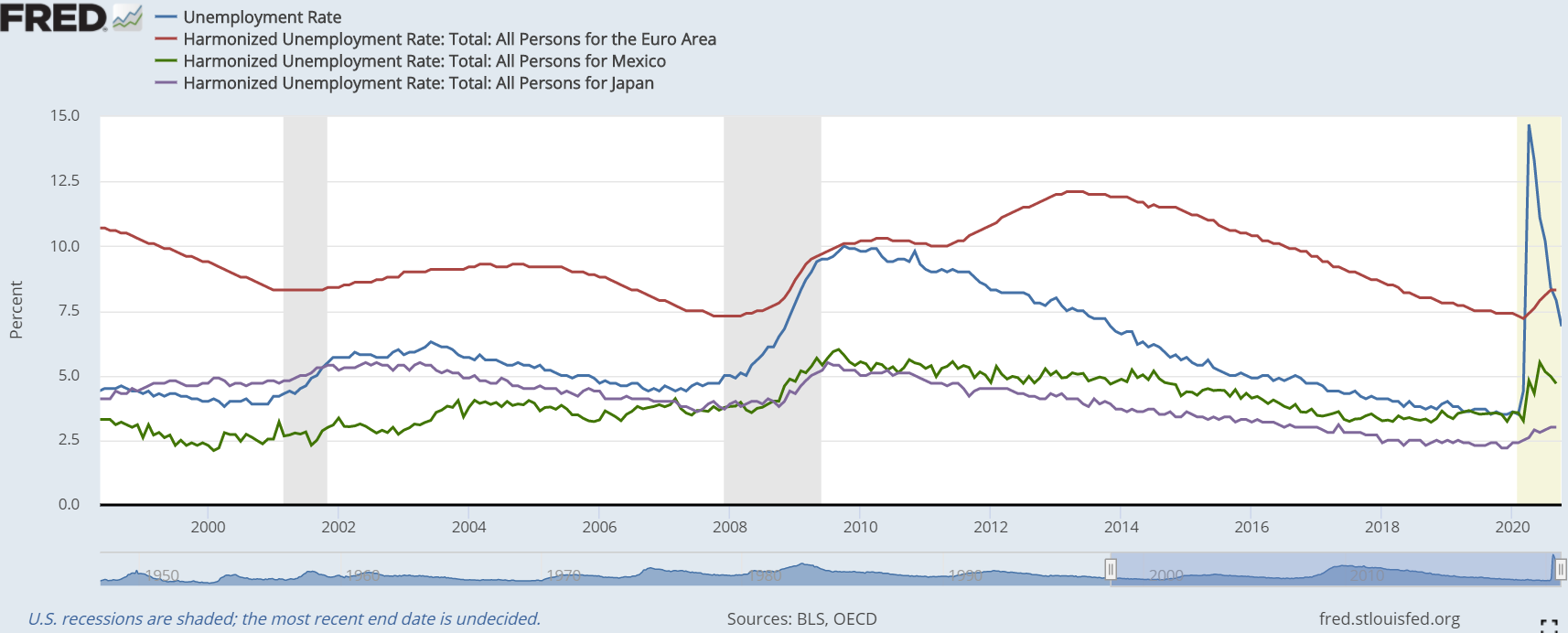

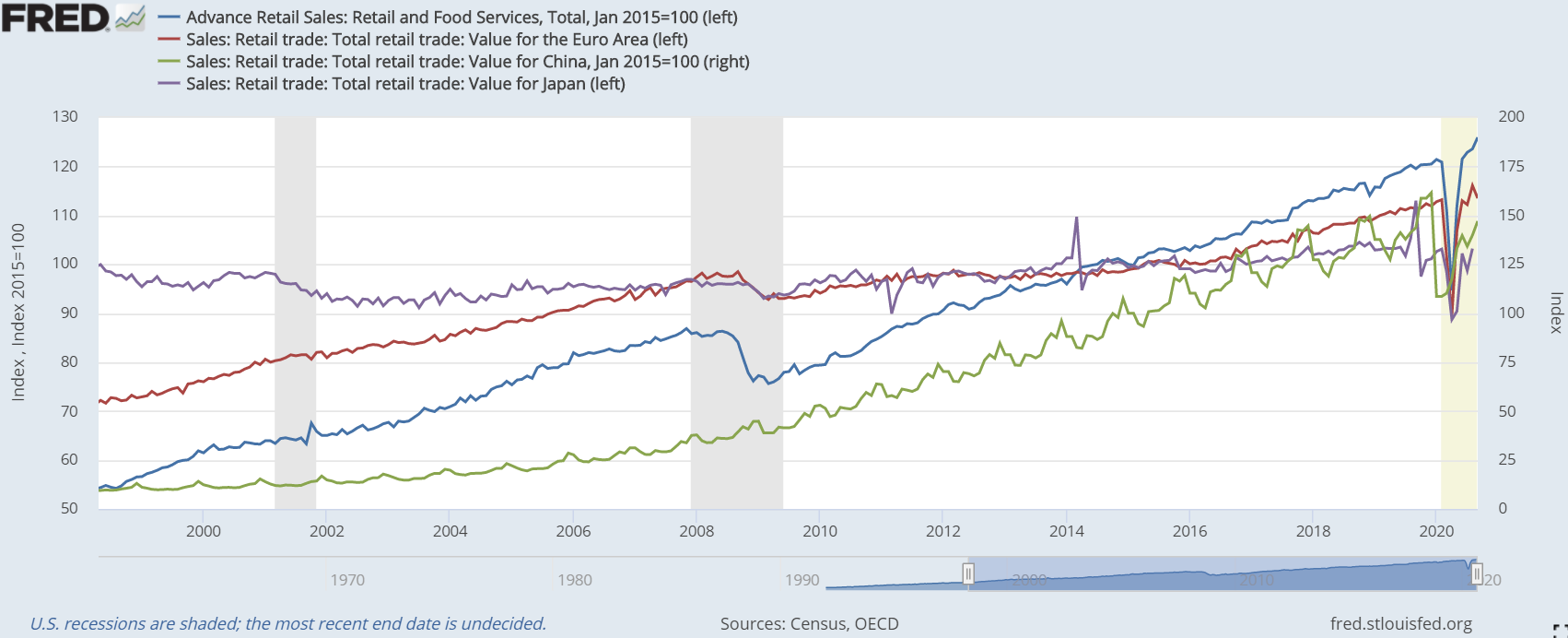

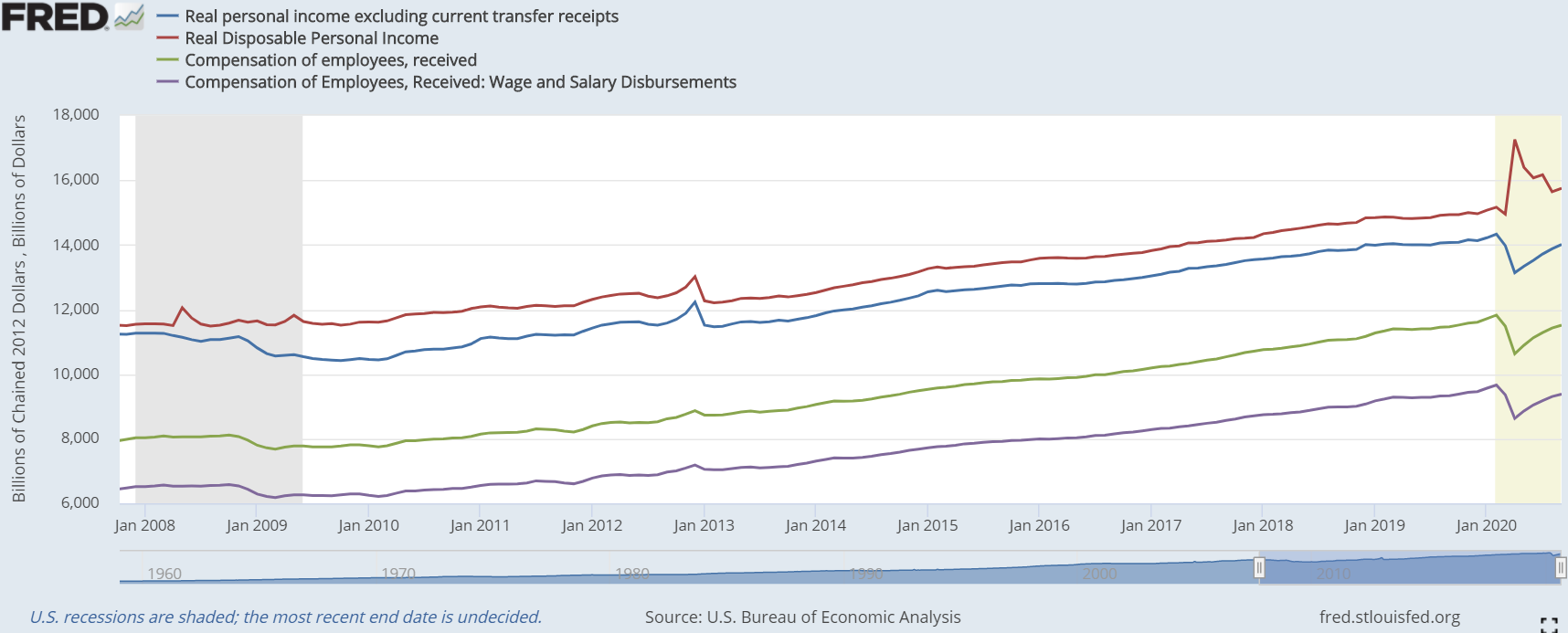

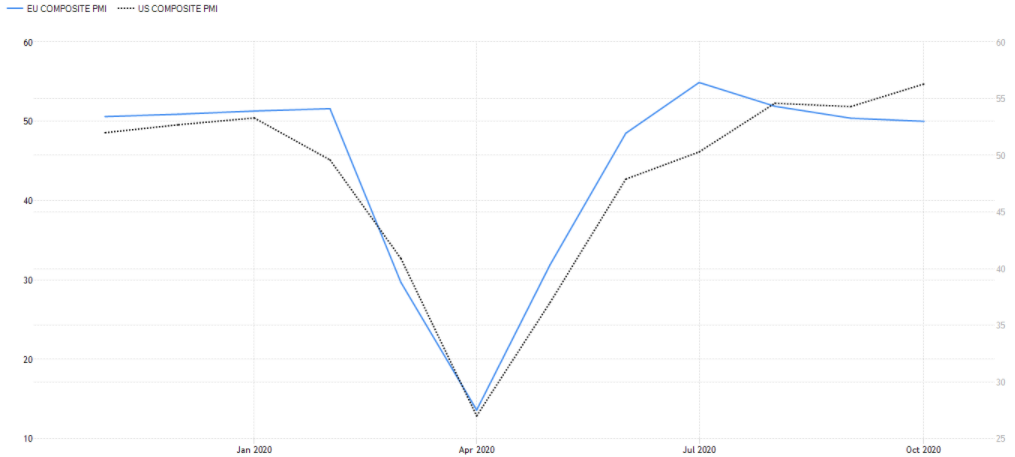

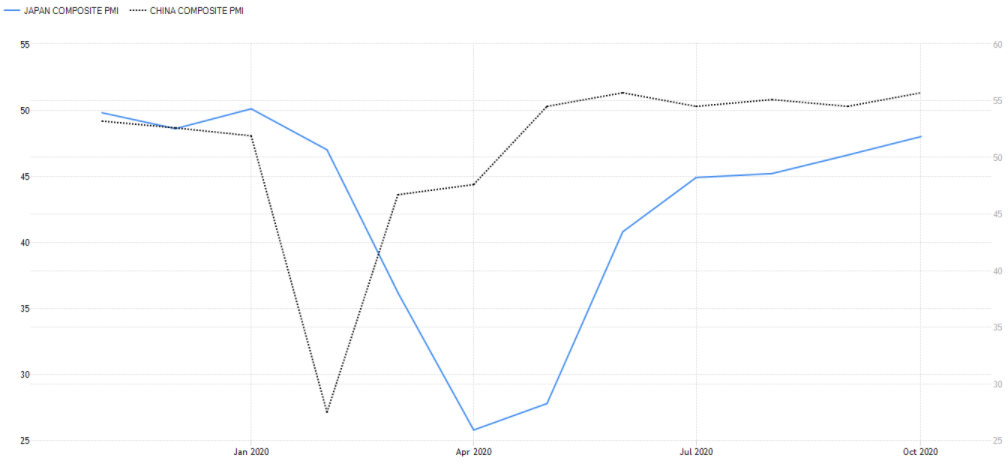

In view of the fact the US has the greatest display of relevant economic data, as well as speed in which they come to public, I am going to focus more on this region than on the others, simply because they have a broader and more detailed information. Thus, to have a better sense of what is happening in the labor market and in personal income, the Land of the free is going to be the sole indicator, acting as a proxy for the state of these parameters worldwide. Therefore, let´s delve in the States job numbers. After the paranoia-driven shutdown of the economy was drawn to a close in late spring, most of those who had been laid off or furloughed began returning to their jobs quickly. However, when we got to June, the reopening momentum started to fade. As you will see, this month comes out in several statistics and markets as a turning point. Moreover, the still huge level of initial jobless claims, when compared to the pre-covid paradigm, indicates that the businesses which maintained their workers, for believing the economic halt would be easily and quickly reversed, are now shedding useless staff members since keeping them would be too costly for the current, and possibly expected near-future, level of demand.   As a matter of fact, the recovery is really taking a much longer time than the "V-shaped" recovery fanatics were antecipating. Just by taking a look above at the evolution of continued jobless (state) claims and the federal unemployment assistance schemes (unit of measure is thousands), there is no doubt the so-called recovery is extremely lethargic - ups! this segment was supposed to be exclusively made of good news; oh well, I tried. Like I stated on the post of November 2, "although state claims are falling rapidly, the extraordinary joblessness benefits brought by the CARES Act are increasing in demand. Therefore, the continued (state) claims are plunging only because the recipients are exhausting their eligibility (each unemployed person has the right to receive unemployment insurance up to 20 weeks). Then, since they still cannot find a job, they move over to the federal level for the unemployment compensation". As a result, the unemployment rate in the US, which skyrocketed in March, has nosedived since. Curiously, other countries, especially in the developed realm, have had a very different experience. In the EA and Japan for instance, have been surging from March onwards relentlessly, though only slightly compared to the upswing in America. This is due to these countries' governments carrying out policies encouraging businesses to furlough instead of laying off employees. Seeing that furloughed workers do not make their way into the unemployment rate, this stat did not escalate during the lockdowns. Notwithstanding, due to suffering the same (or even worse) lack of demand as the US (and government aid has also been waning), companies have been downsizing.  Moving on to the one data point which produced a full "V", retail sales, across the major economies, have reached its pre-covid trend. Mission accomplished! The technocrats were right! Fiscal and monetary stimuli works! Glory, glory, hallelujah! Let's not pull a Biden/DNC and start celebrating just yet, though surely the recovery will go smoothly without any insurmountable hurdle. I mean, everyone in the media says so, therefore it must be true.  On the flip side, and turning our attention once more to the States, personal income had a full "V" performance as well, although it was an inverted one. As a means of countering the reduced economic activity, policy makers brought about a colossal stimulus and relief package, CARES Act, which put a ton of money in the pockets of the populace (shown previously here). Regardless, personal income without government transfers has had a rather mighty recovery, resulting completely from wage and salary increases.  In terms of "soft" data, the prophecy of the desired "V" is apparently in the making. Starting with the PMI's, the index did undoutedly form a "V" whichever region you look. Owing to the PMI's being at pre-hysteria levels or even higher, production must be back at normal, pre-hysteria levels, right? So as to make up for lost time and lockdown-induced slack, these indexes had to be much higher than what they returned since restrictions were lifted. Frighteningly, Japan has to yet yield a positive (over 50) number, meaning that output has been declining since February. Besides, the EA's composite PMI for October was 50, which indicates activity is stalling far too short of a true recovery. Instead of an acceleration in these indexes (numbers much bigger than these ones, at least by 10 points) that would be proof the "V-shaped" recovery was really on track, due to feeble demand,both in developed and emerging markets, the economic comeback is turning sour - damn it! this should have been only about positive news. Interestingly, the right side of the "V" reached its climax in June.

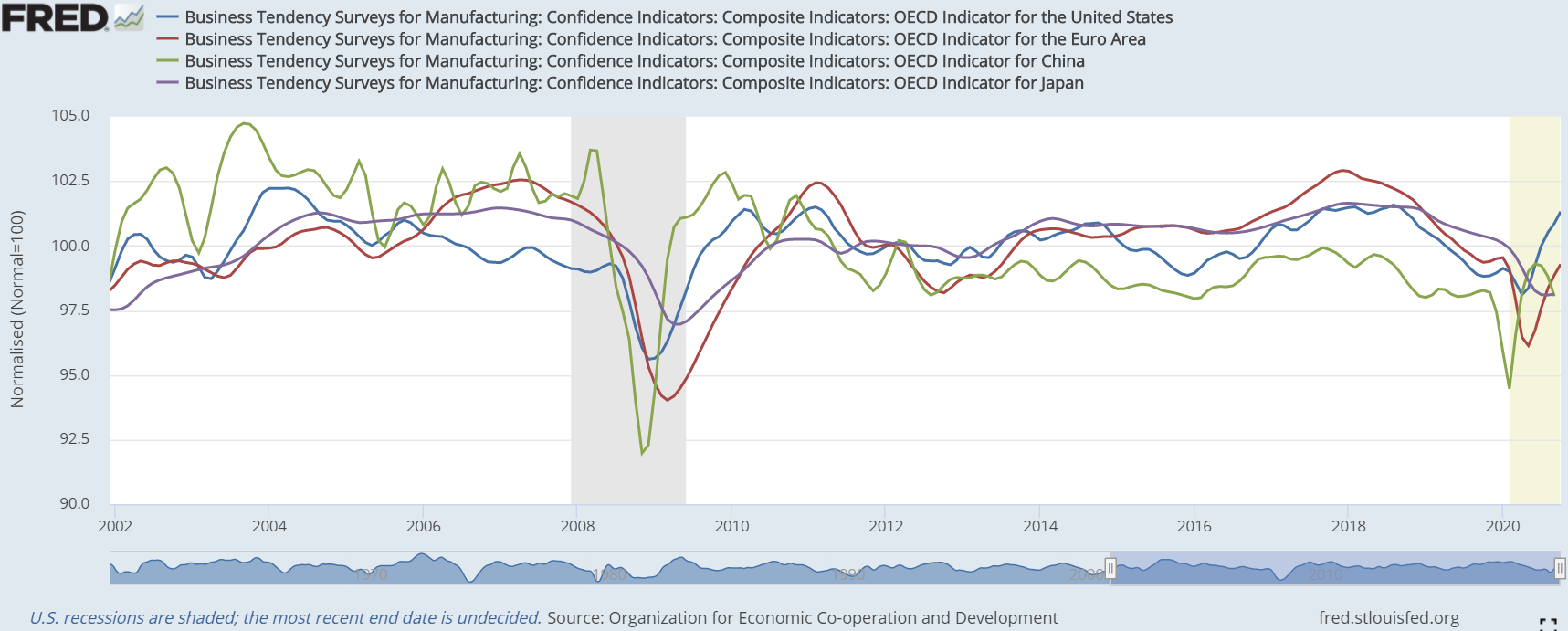

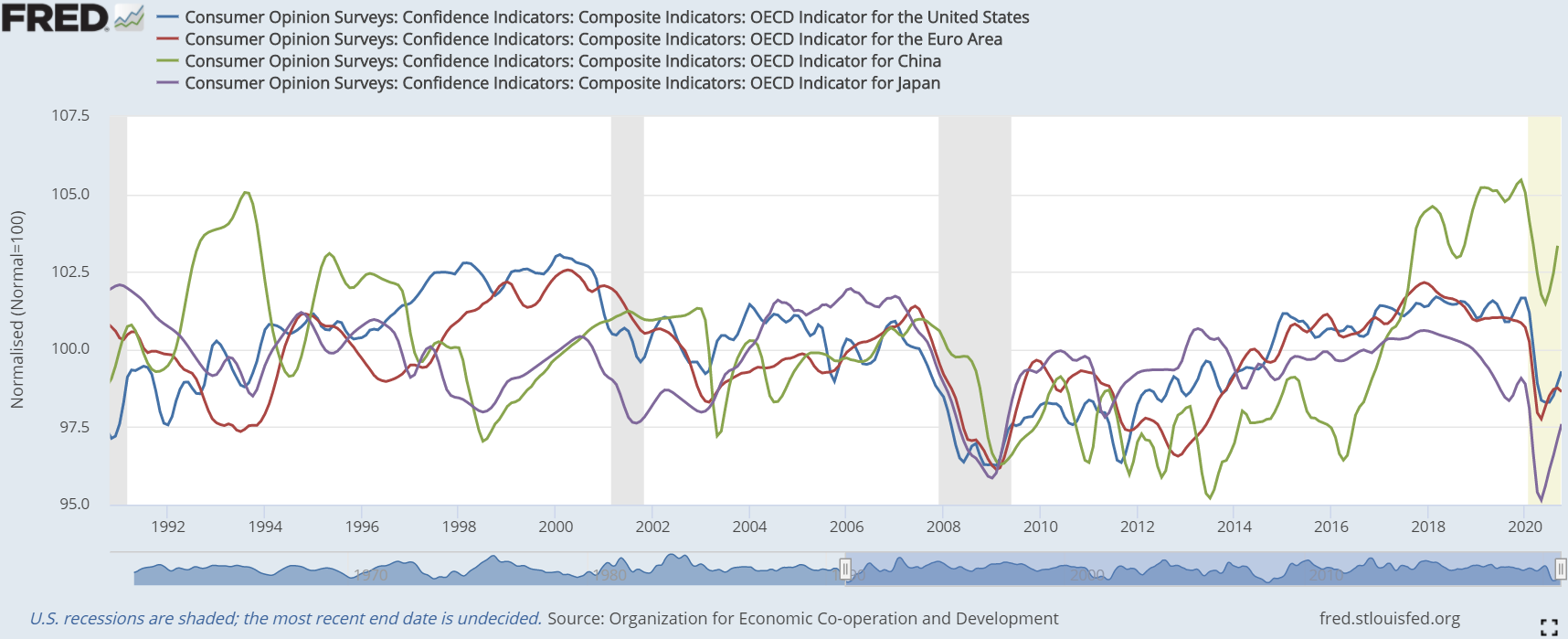

On the bright side, business confidence is on the rise, though only in Europe and America (among the countries depicted below; those indicators are calculated by the OECD using national surveys). Likewise, more so even, consumer confidence has made a nice, quick rebound, bearing in mind there are various reasons to be downbeat. On the one hand, while it seems that japanese businesses, for being swindled by central bankers and fiscal authorities for two decades now, refuse to be fooled again, the niponic consumers are still willing to drink the Kool-Aid. On the other hand, in the Occident, people who pay attention to these matters, particularly in businesses, take the promises made by the technocrats as scripture for some reason. Having failed to meet any of their goals in the last dozen years, it baffles my mind how the majority of the people trust these idiots in power are going to be able to spur the economy into an inflationary boom. Furthermore, while Chinese consumers are still feeling very confident in relation to historical levels, business optimism is waning. Despite appearing odd, this disparate sentiment has an easy explanation. In a nutshell, the Chinese Communist Party, in its most recent 5-year plan, the 14th one, in which they send out small snipetts to the press, has decided to turn its focus to the domestic market. Hence, the Chinese feel appreciated for all this attention, whilst the entrepreneurs in the manufacturing sector, for being export-oriented, are beginning to feel a bit apprehensive. More on this on a future post.

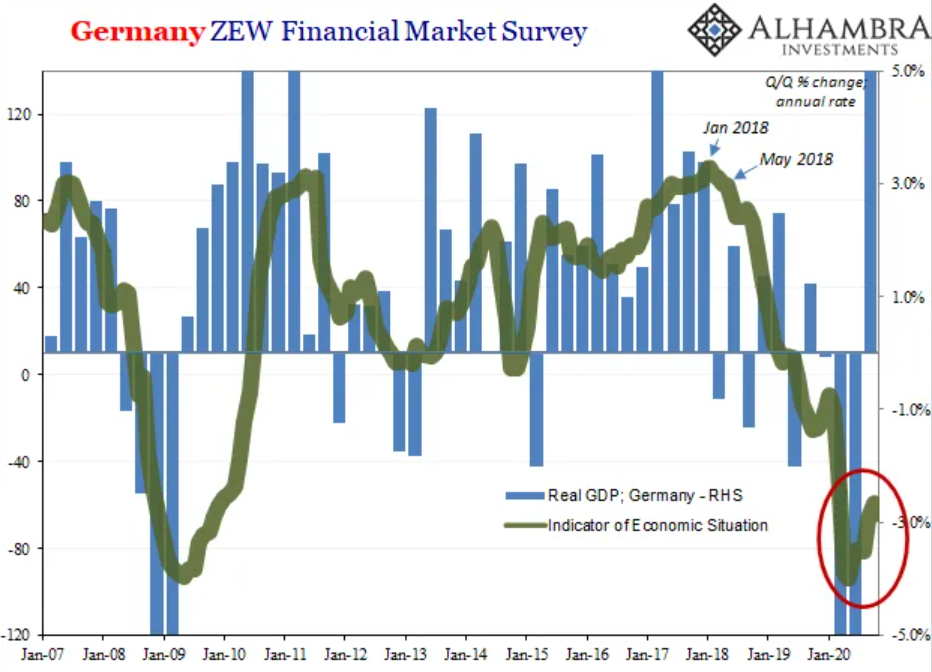

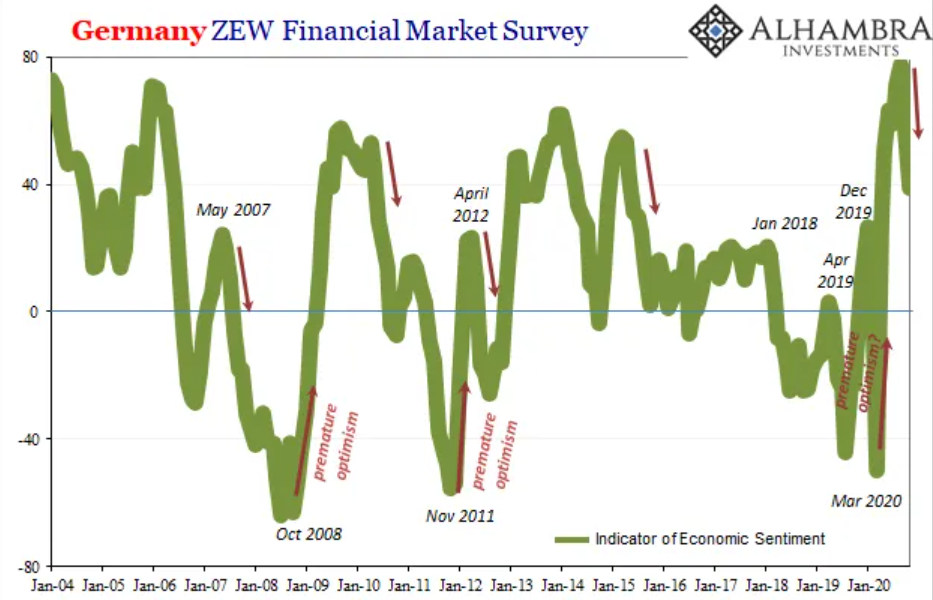

Finally, the ZEW survey for Germany provides an accurate depiction on what is presently occurring and what is already brewing, making it a smooth segway for the next part of this series.

Since employment and output have been improving, despite the increasing sluggishness that I have just shown, it is no wonder the indicator of economic situation (left chart) is jacking up. Au contraire, the indicator of economic sentiment, albeit having surged up to the end of summer, the latest ZEW number for it dropped sharply in November after having done the same already in October. Combined, the index has crashed by 38 points; one of the largest two-month tumbles in the series history (it should be noted that this month’s data was collected before Pfizer’s announcement; it may be that the vaccine news reinvigorates sentimental optimism next month even if the situation doesn’t change – or gets worse again). The last time ZEW sentiment collapsed this quickly, outside of February-March 2020, was in the middle of 2012, when faith in Mario Draghi’s first flood of stimulus (LTRO’s) ran aground of Euro$ #2, pushing Europe even deeper into recession. Ergo, this should sound eerily familiar, which may be what we are seeing in these sentiment estimates. In conclusion, in spite of making an effort to only present the data supporting the bullish "V-shaped" recovery, the truth is that, at this time, the amount of optimistic figures are very scarce and becoming even more so as time goes on. On the second instalment, I am going to present more economic and financial data portraying more clearly how the economy performed since the end of the lockdowns until now. As you will see, the summer rebound came out far too short of expectations, leaving us with a ticking time bomb.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed