|

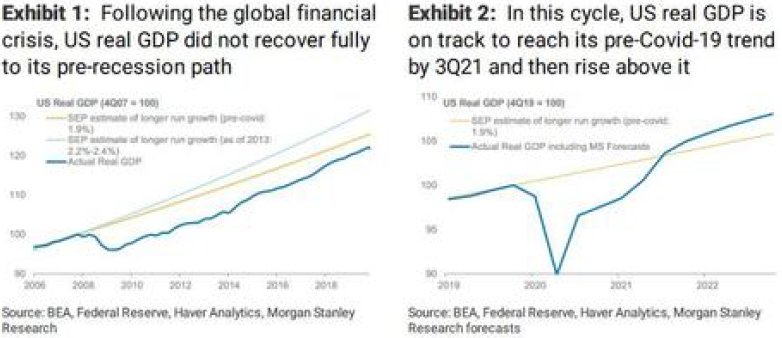

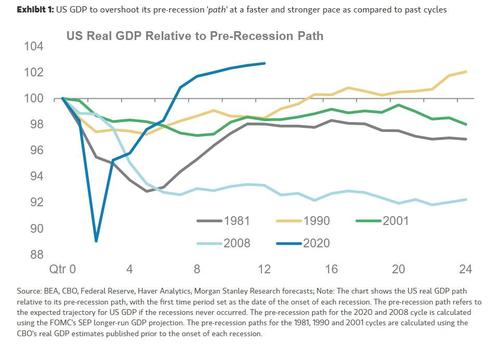

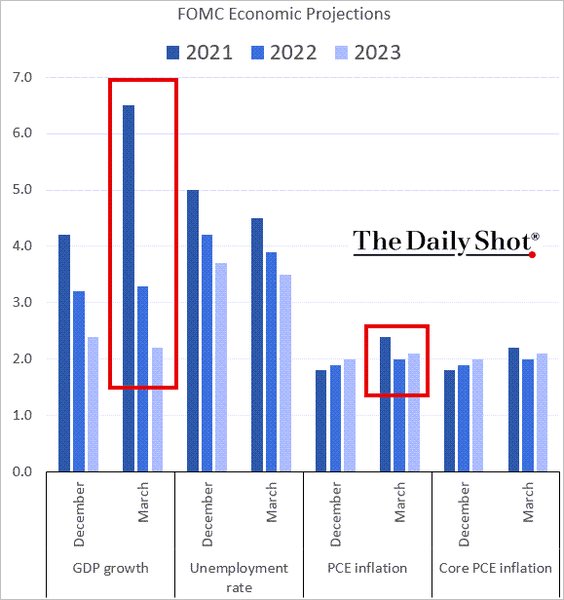

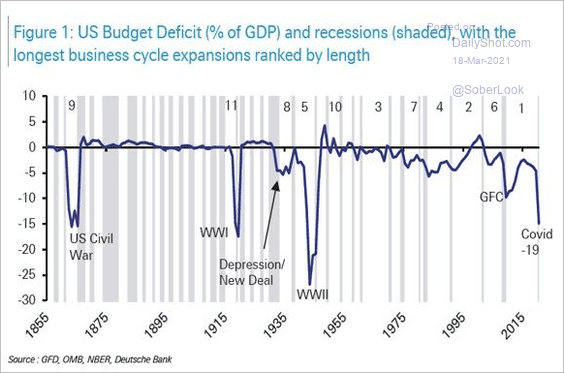

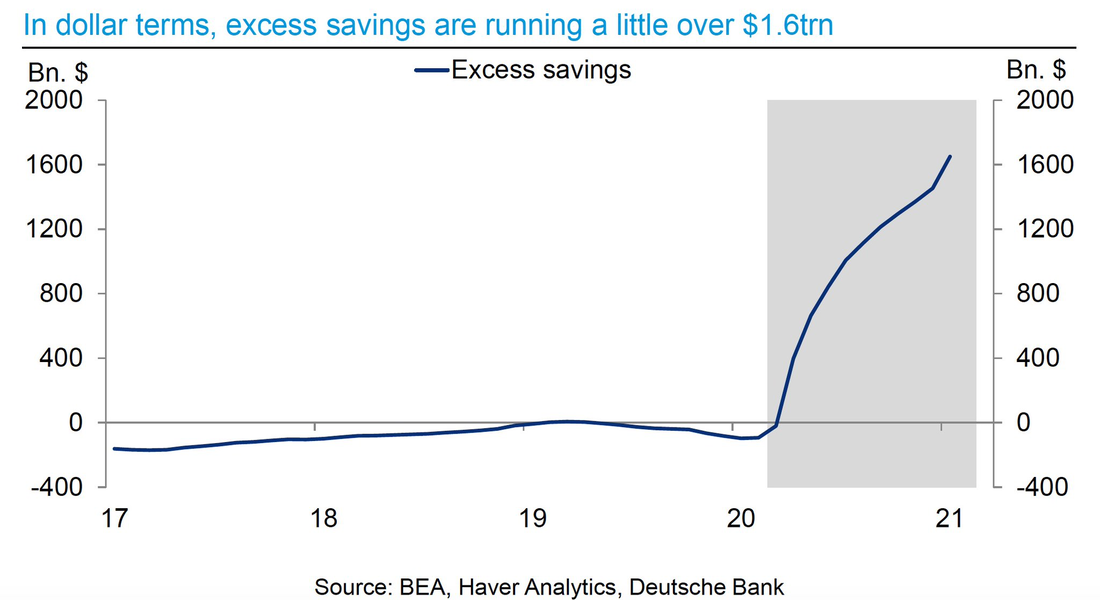

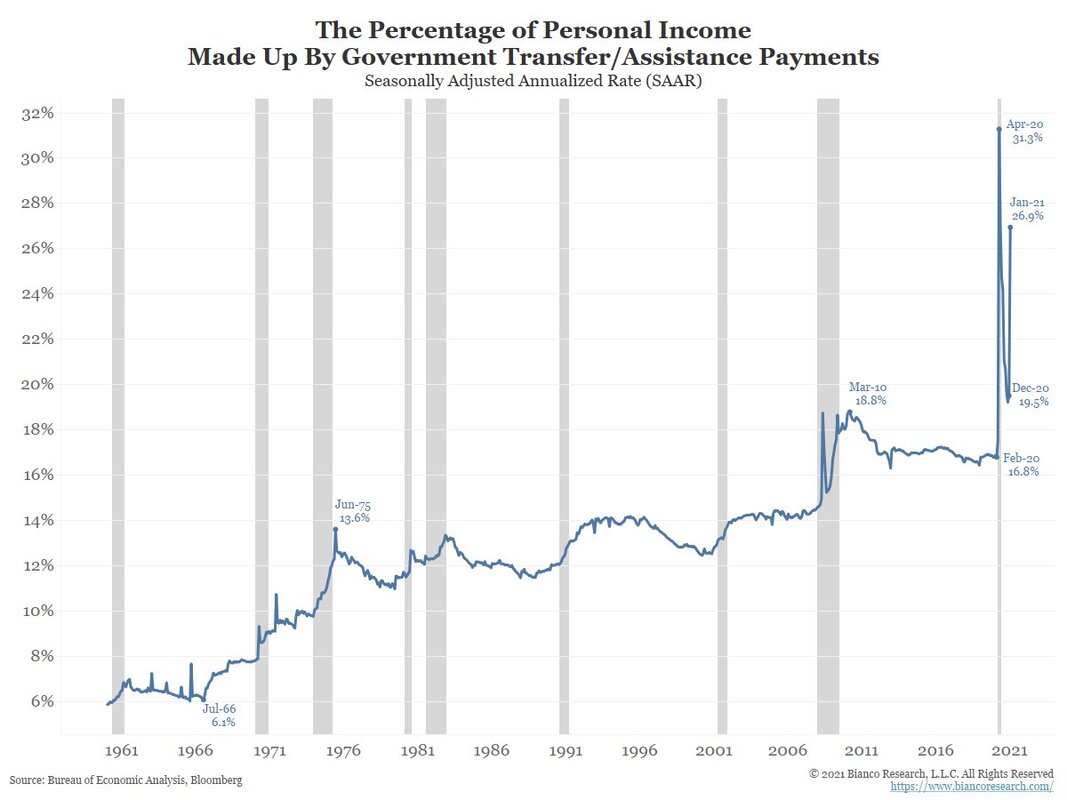

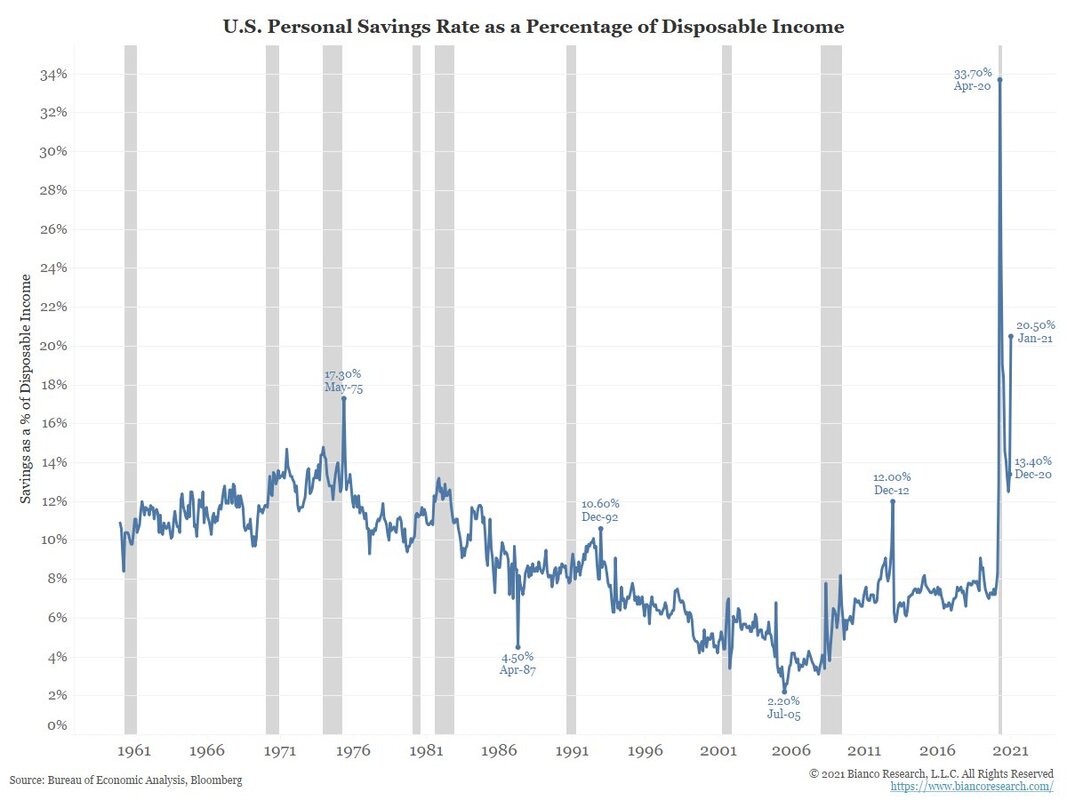

After uselessly engendering the greatest economic contraction and social calamity in the post-war era so as to curb the spread of the kung-flu, policy-makers have then started to desperately try to push the economy to the level of activity it was supposed to be at had none of this ever happened. In classic spoiler fashion, let me just go ahead and declare they have not and are not going to succeed. Nevertheless, those in the media and the economists who feed them this nonsense are always very keen on crying inflation every time the government steps up its deficit spending. For almost thirteen years now we all have been listening to this spiel and for all this period we have been patiently awainting for that technocratic-planned recovery which never arrived, prompting anguish and resentment for the average Joe and Jane. Be that as it may, bearing in mind the colossal amount of money the Democrats are injecting in the economy, $1.9 trn now plus another $3 trn or so later on to be invested in "green" projects, in infrastructure and so forth, the recovery has to be inescapable. If not to the pre-GFC1 (2007-2008) trend, then certainly to the pre-GFC2 (2020) one. Among those who believe the recovery is on the cards are the economists at Goldman Sachs and Morgan Stanley. In a letter written last month, the analysts in the latter bank claimed the fiscal and monetary "stimuli" are creating a "high-pressure economy" that will put the ten million people who have become unemployed back in their jobs (or some new one). For 2021, these economist projected, in February, US GDP to grow by 6.5% in 2021 (7.6% 4Q/4Q) and 5% in 2022 (2.9% 4Q/4Q). These estimates imply that US GDP will rise meaningfully above its pre-Covid-19 path after this year's Q3 and will allegedly be higher in 2022 than what we would have expected in the absence of the pandemic. That is a particularly remarkable outcome, especially when you consider that in the post-GFC period the US economy never really returned to its pre-recession path, as I affirmed above. In view of the regime shift in both monetary and fiscal policy, they assert this accelerating recovery is bound to take place. The shift they are refering to are i) the move to average inflation targeting, on the monetary front, by the Fed, and ii) on the fiscal front, the Biden administration have jacked up their efforts to address the "issue" of inequality by enacting large-scale government transfers to low- and middle-income households.   Furthermore, on their updated estimates, the US economy will reach pre-corona output levels by the current quarter. From the third quarter of this year onwards, US GDP is foreshadowed to overshoot the path it was projected to follow before the recession. The last time GDP rose above its pre-recession path was in the 1990's (above graph). Back then, it took fifteen quarters compared to seven quarters this time around, with these analysts expecting the US economy to reach 103% of its pre-recession path in twelve quarters (i.e., by December 2022) versus twenty seven quarters in the 1990's. In this March update, they are forecasting growth of 7.3% in 2021 (higher than the February forecast) and 4.7% in 2022 (lower than last month's), almost 2 percentage points above consensus this year and 1 percentage point next year. To justify this, they defend this historic fiscal policy, which is the most sizeable during a peacetime (next graph on the left), is doing much more than fill the output hole. Transfers to households have already exceeded the income lost in the recession, causing savings to mushroom (next chart on the right). As reopening gathers pace, the labour market is poised for a sharp rebound, entailing that consumption growth in 2021 will be supported by wage growth and transfers, with little reliance on excess savings. In fact, they think the excess saving stock (savings accumulated by households over and above the pre-kung-flu run rate) will still rise to a peak of $2.3 trn (roughly 10% of GDP) by the end of this summer. Even for 2022, they are building in only a modest drawdown of the excess saving to $2.14 trn (8.7% of GDP) by year-end. Evidently, a faster-than-expected drawdown will pose upside risk to growth. All the same, they see inflation, following a near-term surge in the spring, remaining elevated above 2% this year and the next.

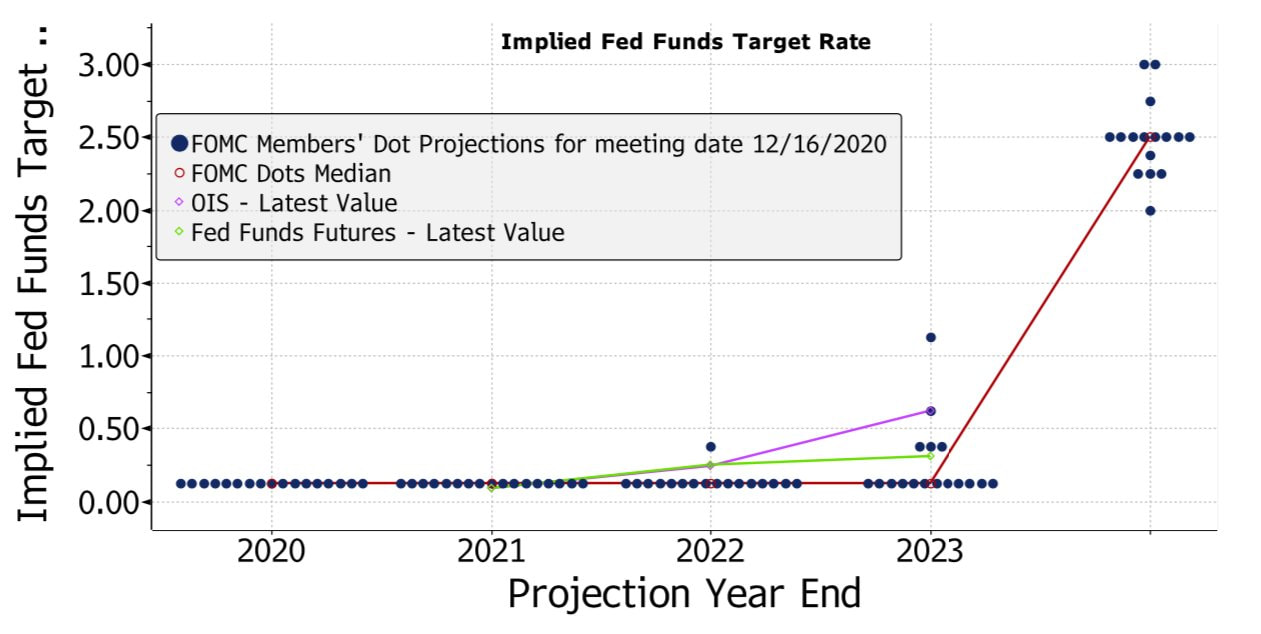

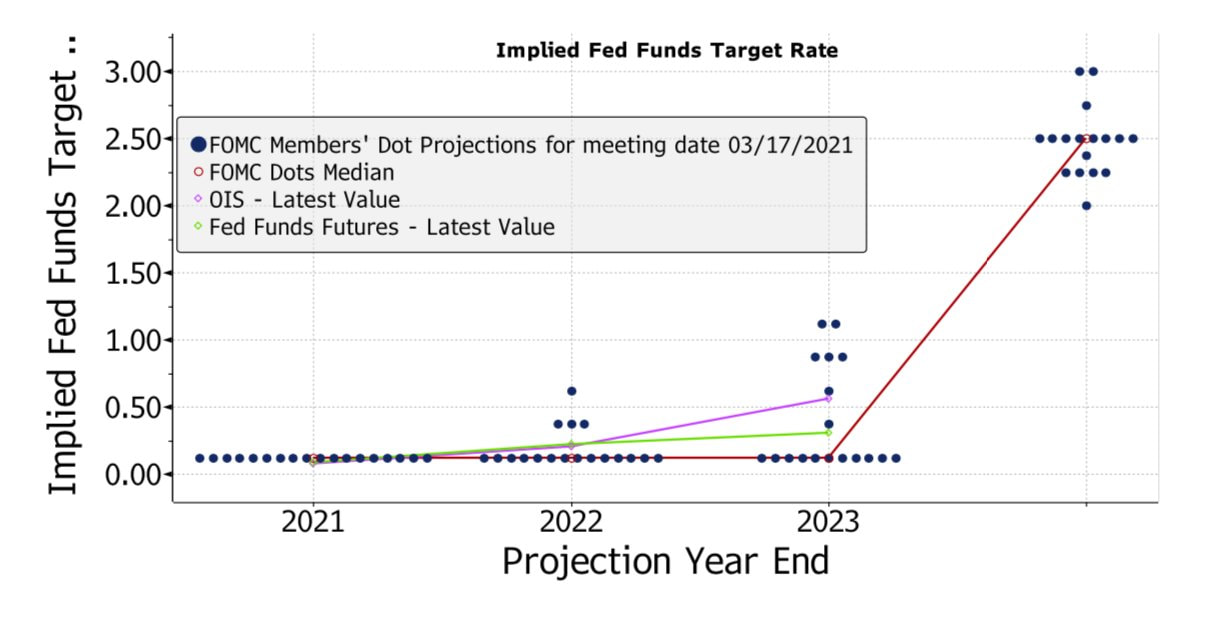

Having already stated the change in its objectives, the Fed is not concerned with the uptick in the "inflation" rate, maintaining this rise in prices to be transitory. Despite the economists' assessment of future inflation and economic performance, the markets are apparently contradicting them, siding with the Fed (top graphs) - or more correctly, the Fed siding with the markets. Even though since 2021 broke out the sentiment has improved substantially among financial and economic analysts, as well as in financial newsrooms and economics departments, the reality is that markets are indicating the immediate and near futures are still terrible. Therefore, federal funds futures and the overnight indexed swap (OIS) on the fed funds rate are telling us that financial conditions have remained tight and, more importantly, are expected to be so in the next couple of years.

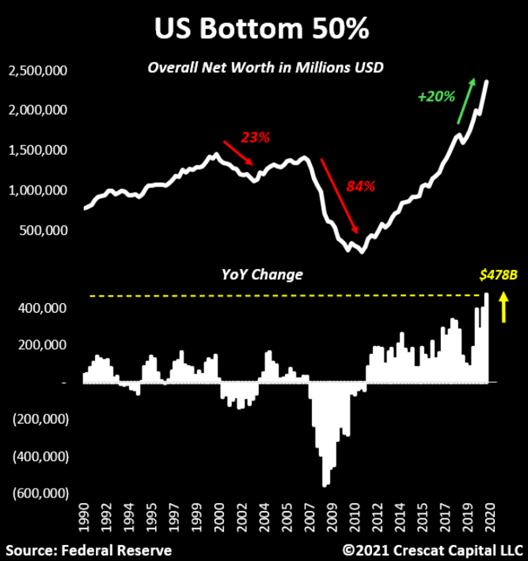

Perhaps the Fed is assuming prices to climb more than 2% transiently because they know the economy is still suffering from a deflationary/disinflationary landscape - definitely not; they are simply following the market signals. Like I said on the March 1 post, "it is not stimmy checks sent by Uncle Sam, or any other government for that matter, that are going to enkindle the much-anticipated inflationary conflagration. Because individuals sense, and rightly so, the government aid is temporary and inconstant, they are not spending money in proportion to what they are gaining in income". Although the surge is staggering, the "stimmies" are not going to cure the economic malaise and turn it into a proper boom. If you have been following my work, you are aware that I alluded to the cause of such malaise many times, albeit never really expounded on it. Once more, on account of that being a topic that requires thorough analysis, I will save it for another day. Regardless, I think you already know the culprit is the gargantuan weight governments worldwide have on the (global) economy. In addition, that whole notion that individuals are swimming in a sea of savings that would put Scrooge Mcduck to shame is absolutely false. A couple of months ago, Real Investment Advice's Lance Roberts perfectly exposed the truth behind those misleading statistics. In short, the accumulation of savings has occurred in the upper-class, while the lower-classes have been living paycheck to paycheck. As a result, were this skew in savings to keep on going this way, seeing that an increase in the savings of the wealthy individuals is not going to change their propensity to consume, the economy is definitely not going to boom. To be fair, the government handouts have been directed at the lower- and middle-classes, having the theoretical potential to boost consumer spending and, consequently, economic growth. Unsurprisingly, "theoretical" is the key word there. In the real world, these poor bastards have every reason to carry on being thrifty. Owing to not having a stable source of income and finding extremely difficult to get a nice job - due to government interventionism creating a lethargic economy and over-regulated labour market -, being dependent on the whims of politicians to get by, and, to add insult to injury, because credit moratoriums and eviction bans cannot last forever, the fact that their savings ballooned and their net worth curiously shot up, which of course never happened during a recession, is not going to change their economic outlook. Revisiting our friends from Morgan Stanley, they believe the impact of the pandemic is likely to fade, and they foresee a surge in demand as the economy reopens this spring. For being forced to accumulate excess saving as restrictions on mobility have limited their opportunities to go out and spend, with warmer temperatures coming and vaccinations set to cover a large part of the vulnerable population, these analysts are confident that the relaxation of restrictions, which has begun in some states, will pick up speed as spring approaches, resulting in the economy ultimately firing on all cylinders. No dice!

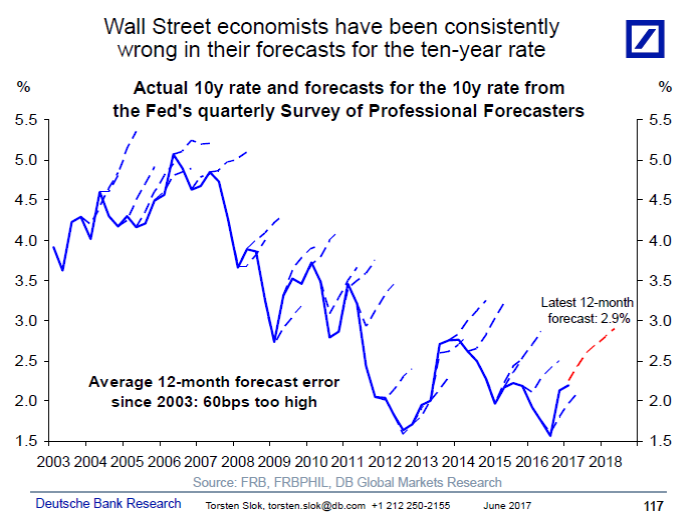

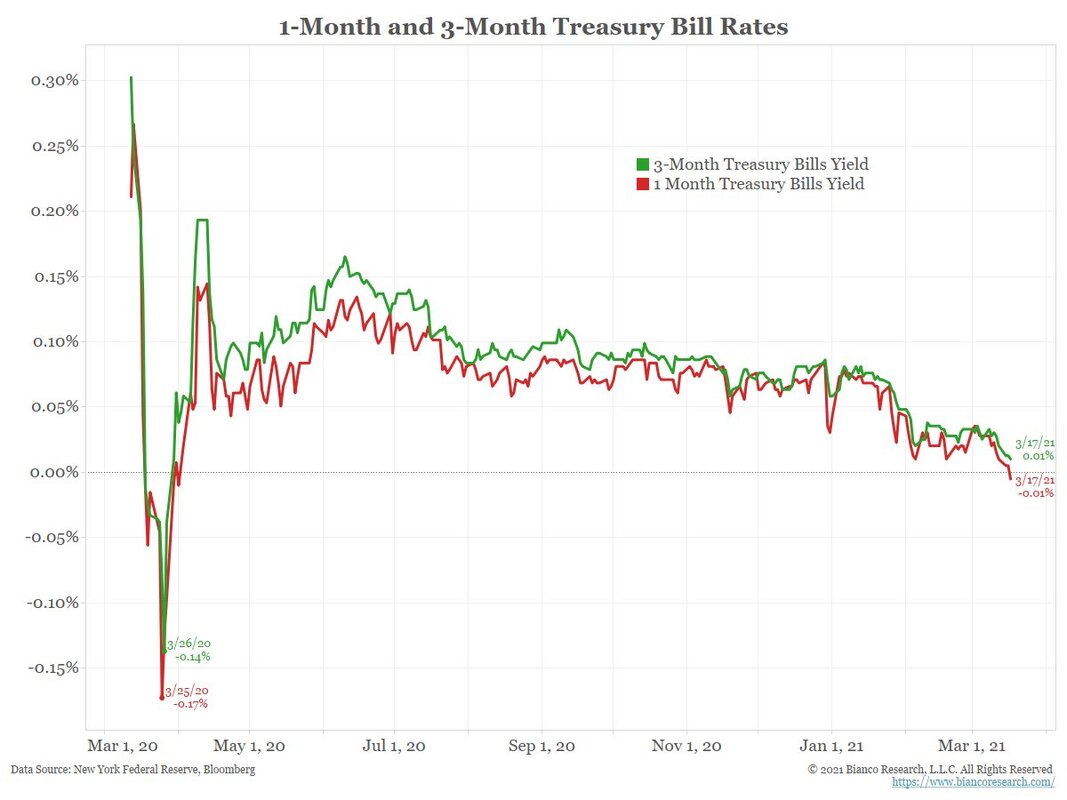

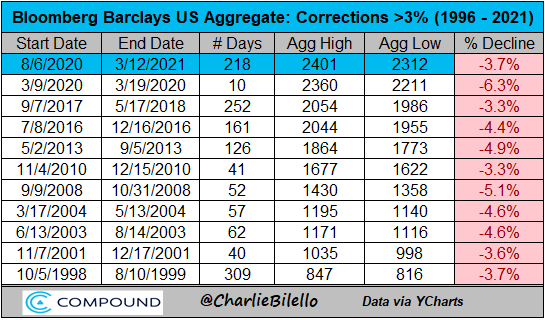

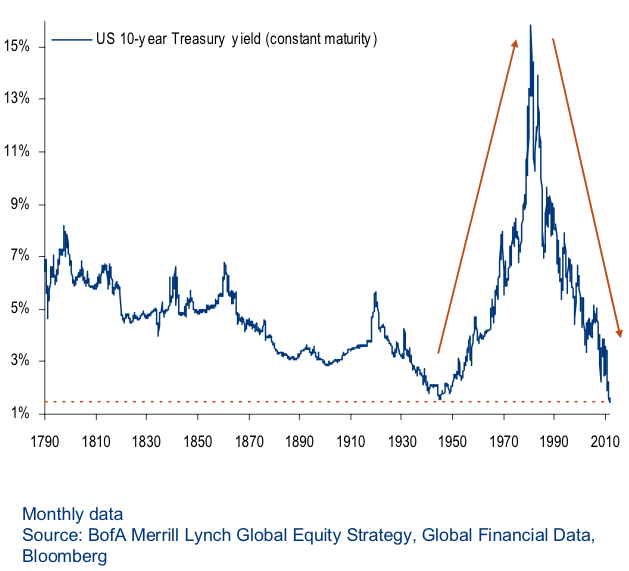

Notwithstanding, insofar as the econometric models suggest the much awaited inflationary recovery is set to materialise, economists take this view. Hence, watch out for the bond rout! As the top left graph demostrates, Wall Street economists might as well change careers to become tarot readers or public health officials. Seeing that they are always overly optimistic about economic prospects and the efficacy of the policies pursued by the government, why will it pan out differently this time around? Obviously, it will not and in spite of all the kerfuffle surrounding the current sell-off in the long-end of the UST market, this has actually been one of the weakest in the last quarter century, as shown in the top right table. Like I mentioned above, economic and financial conditions remain tight. Undoubtedly not as much as they were a year ago, but still enough to momentarily push T-bill rates to negative territory, which is depicted in the bottom left chart. Similar to the economic environment of the last thirteen years, the Great Depression of the 1930's also experienced all kinds of weird phenomenons that have transpired since the GFC. Albeit a topic for another day, as the bottom right graph indicates, the deflationary conditions of that period brought about an insatiate demand for those safe and liquid Treasury securities., despite the tremendous amount of government debt issued to finance the New Deal programmes.

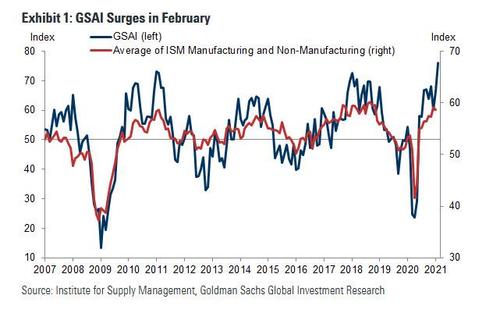

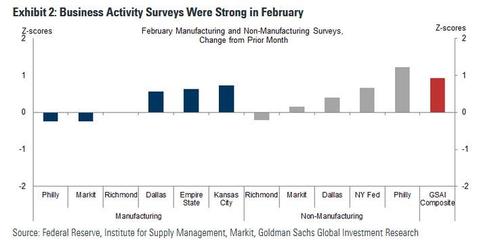

Moreover, the Goldman Sachs Analyst Index (GSAI), which provides a snapshot perspective on the US economy (and thus differs from the BEA's GDP measure which is an average look at output over a period of time), rose 9.4 points to an all-time high of 76.0 in February. The composition of the survey was strong, as the orders, shipments, and employment components all increased. Most regional business activity surveys were very strong in February with Goldman's manufacturing (+0.4pt to 58.2) and non-manufacturing (+1.7pt to 54.2) survey trackers both rising (bottom table).

To break the data down to its various items, one clearly realises the picture is not that rosy, as one may have initially expected. To wit, the sales and shipments component surged +19.0pt to an all-time high of 90.2. The orders component increased (+13.3pt to 76.2) by more than the inventories component (+3.2pt to 53.2), increasing the orders-less-inventories gap to 23.0. The employment component rose to its highest level since December 2018 (+0.9pt to 66.6), and the wages component rose to its highest level since May 2018 (+6.8pt to 81.8). To cap it all off, the output prices component decreased (-4.0pt to 77.3), while the materials prices component increased (+1.4pt to 80.0). Basically, the rebound from the massive depth of the Q2 2020 trough has entailed, without surprise, a surge in activity, along with the stimmy checks like the ones the Trump administration began to send out at the end of last year as a parting gift. What is most noteworthy is the dissonance between the apparent burgeoning demand and the declining output (i.e., consumer goods) prices. The explanation is something that I have discussed earlier this month. To make long story short, the distortions in the supply chains provoked by the paranoia-induced restrictions of all sorts have led to shortages of goods (e.g., computer chips, ship containers, etc) and services (more strikingly in transportation), among other unintended consequences. Ergo, because the transportation industry, chiefly shipping, is impeded to function smoothly, businesses have increased their orders to get as much supplies and as fast as they can get them, in order not to be forced to reduce or halt production outright. Naturally, this has caused even more disturbances in the supply chains, as the PMIs have also captured (below charts). Therefore, higher input prices, though lower output prices on account of lackluster demand.  To conclude, these circumstances are surely not propitious to a rapid adjustment of the productive structure, which is wholly necessary for the economy to fully recover. Besides everything I have presented here, since the supply squeeze is squeezing producers' margins of profit, how is this conducive for them to hire?

Eventually, due to shrinking margins, they will pass part of the cost on to retailers and these, in turn, will pass it to consumers afterwards. However, in view of the unreliable income source for most consumers, these are not going to totally spend their stimmy checks. Thus, retailers and producers and the rest of the supply chain participants are going to be the ones to absorb the costs entirely. Unsurprisingly, a lot of them are not going to manage this squeeze and will certainly be wiped out. On top of that, the government stipends are, on the one hand, lifting demand to higher levels it would otherwise be in a laissez-faire economy and, on the other hand, making it far more costly for businesses to fill their job openings due to the government being unconsciously competing with them by bidding for (potential) workers - these stipends make it much more appealing to stay unemployed and have pratically 100% of leisure time. Therefore, seeing that governments, especially Uncle Sam, are, in addition to hampering the normal functioning of the economy because of the corona-phobia, precluding the swift adjustment of the price and profit system, there is no way the economy is going to break from its deflationary shackles anytime soon. To make matters worse, the growing encroachment by eager politicians and clueless technocrats are sure to reduce the (global) economy's potential even further, depressing its trend henceforth.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed