|

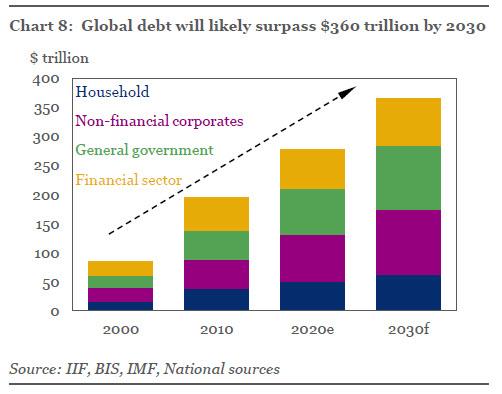

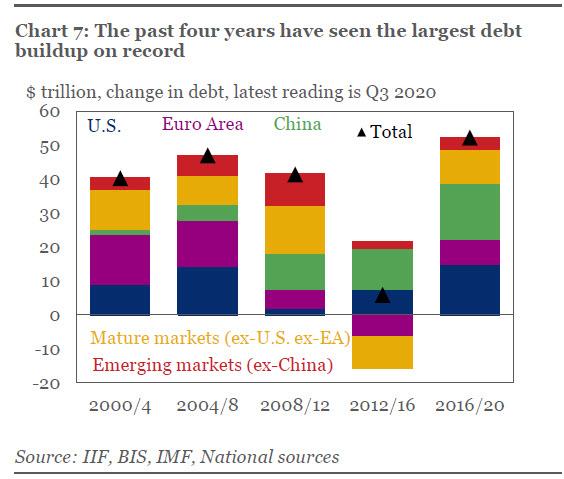

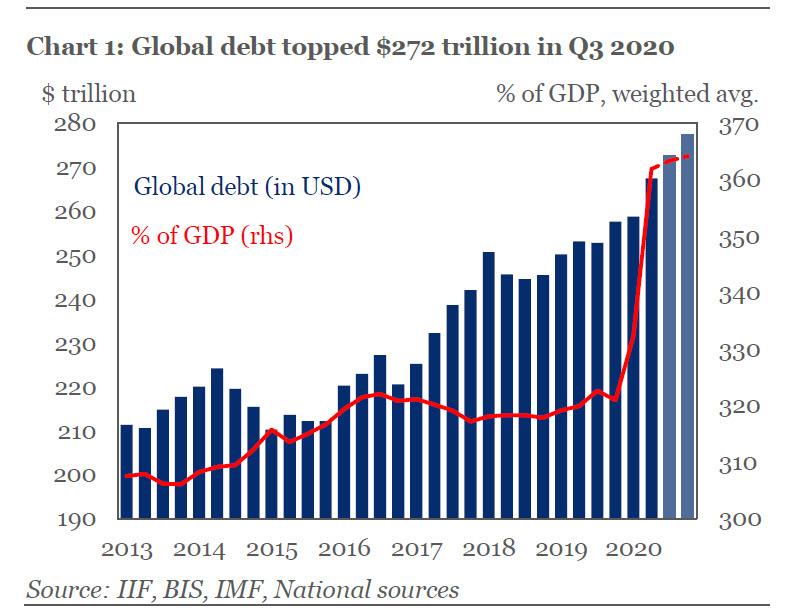

Since Christmas is the time of giving and being with the ones you love, I thought this most wonderful time of the year was also the most appropriate time to check what the ones that give and love the most had done this year to show how much they care about their fellow man. Obviously, I am talking about our warmhearted politicians and technocrats. Albeit a lot could and, in due time, will certainly be said about the governments' (over)reaction, all over the world, to the kung-flu, on this post, I am only going to consider the fiscal side, the debt, which was record-breaking. Notwithstanding, despite all the hardship that this year presented us, individuals (households) and businesses (non-financial corporations) have indulged on a borrowing binge never before witnessed on a global scale. In a nutshell, the growth of total debt worldwide, since the paranoia-driven economic shutdown in March, has been alarmingly strong because "the pace of global debt accumulation has been unprecedented". Accordingly, up to the third quarter of this year, total debt surged $15 trn, which adding to the previous three years totals $52 trn, the Institute for International Finance declared. In relation to the previous four-year periods, this is the first time debt growth has accelerated since the GFC. To be specific, the biggest contributor to make this debt increment a historic one has been China. In spite of increasing their debt levels in the last four years, neither one of the other aggregates has increased its debt by a record amount. Shifting our attention to the chart on the right, one can clearly notice the total debt growth has kept pace with the expansion of the output. In fact, global debt in percentage of global GDP had been fairly consistent since 2013 till the first quarter of this decade, skyrocketing in the following two quarters, reaching the all-time high of $272 trn in Q3. What's more, the global debt is expected to soar even more by the end of the year to $277 trn, which would represent a debt-to-GDP percentage of 365%.

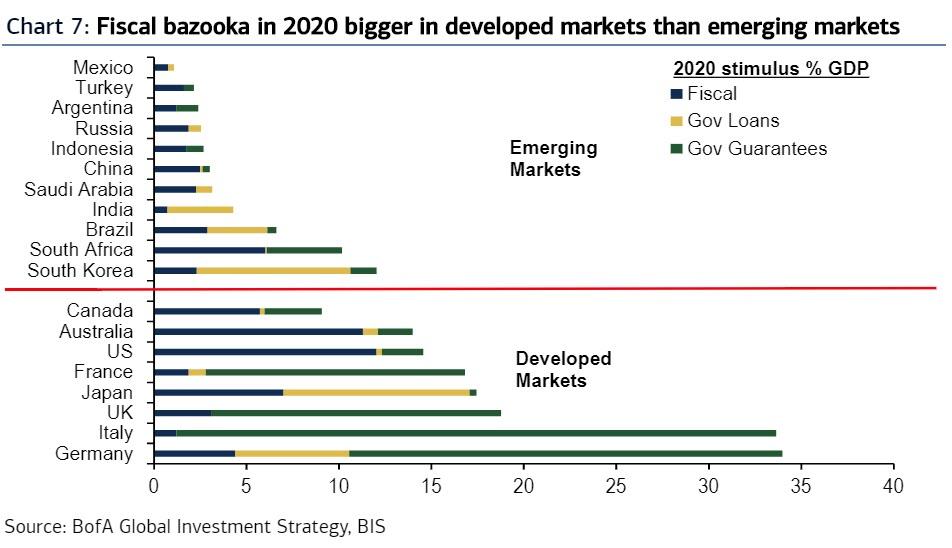

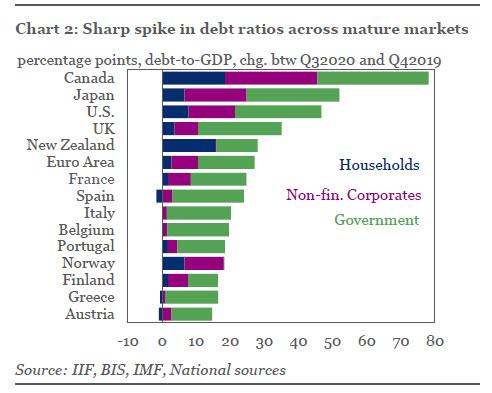

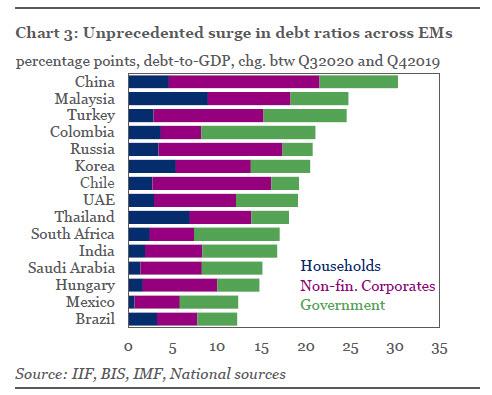

Moreover, the debt build-up has been different among countries, in both quantity and quality, especially between developed and emerging markets. On the one hand, in the DM realm, governments have been the main driver of debt accumulation, particularly in Europe, counting for nearly half the upturn. However, more remarkably in North America and Japan, non-financial corporations have really gone at it this year, with households surprisingly joining the party (to some extent). Among advanced nations, total debt surged above 432% of GDP in the third quarter, a 50 percentage points hike from 2019. In more detail, government action in the EA led to an increase of $1.5 trn in public debt this year alone, to reach $53 trn in total debt. Across the pond, total US debt is forecasted to swell $9 trn through the full course of 2020, hitting $80 trn by the end of the year. On the other hand, the greatest borrowers among emerging nations have in general been the businesses, though governments have not been far behind. Approximately, total debt-to-GDP ratio of the entire aggregate has swollen 25 percentage points to 248% by the end of the third quarter, very much skewed by China's 335% ratio. As I demonstrated on October 24, the "surge at the beginning of the pandemic is explained by the rolling out of lines of credit directed to businesses [from banks and governments] in order to keep up with current expenses, such as salaries, rent, etc., by making up for the diminishing revenues".

On a sidenote, the point has to be made that the EMs' businesses have been taking the brunt of the hysteria-induced economic collapse on account of their governments not having the creditworthiness of the governments in the West. Besides, even more overriding factor, these countries' currencies are not transacted as much nor are these exalted the same way as the major currencies from the putative developed economies, owing to being less liquid (smaller market with fewer buyers and sellers) and/due to market participants having less confidence and use for these currencies - afterall, this is the Eurodollar system. Hence, the monetary situation in the EMs are extremely dependent on the volume of foreign exchange that goes through their economies, chiefly the US dollar (check out the US vs the World part I and II). In turn, in periods of (euro)dollar shortage resulting from global trade contracting (or perhaps just slowing down) and/or financial institutions that take part in the Eurodollar regime being (even more) unwilling, for whatever reason, to supply these very vital dollars (or euros, yens, etc), the banking activity in the form of credit creation is severely impacted in these developing economies. As a result, the economic activity decelerates or contracts, if there is too big of a shortage, because of deflation - the true definition, not the keynesian. Now that I am through with all the explanatory notes, I think it is rather evident why the EMs have what appears to be a fiscal musket compared to the DMs' fiscal bazooka. Basically, the poorer the institutional framework (rule of law, economic freedom, transparency, accountability, etc), the less creditors trust the country and, thus, the more he is wary of lending to that country. Ergo, a higher premium for the inferred risk is demanded, leading to higher interest rates and more pricey interest expenses. To make long story short, the endgame could be 1) a sovereign debt crisis with some high inflation as the ones in Latin America in the 80's or in Eastern Europe in the 90's, or 2) a hyperinflationary crisis of the likes of Venezuela or Zimbabwe that occurred recently.  Furthermore, seeing that the monetary system is debt-based, the amount of credit has to balloon relentlessly so as to keep on the expansion of economic activity, as well as to stave off the otherwise inescapable financial and economic turmoil - FYI, in a "hard money" system, the output can increase without the debt/money supply ramping up, insofar as the ideals of liberalism and an entrepreneurial mindset are present, technological progress would ensue, resulting in greater productivity gains, which would lead to more output. Be that as it may, in view of the fact we live in the debt-based Eurodollar system and noone - specially our rulers and the businesses and individuals who have gained tremendously with all this inflation - wants to experience a deflationary event, the debt gorge must go on. Unsurprisingly, the level of global debt is forecasted to soar till 2030 by roughly $100 trn.  To conclude, it would be one thing if this debt surge came just from the private sector. In this case, only those who accrued them would be the ones to service the debt, and if they for some reason became uncapable of servicing the debt, they would be the only ones in distress. However, because our governments and legislators cannot prevent themselves from smothering us with their love, we are all going to have to chip in since we have all benefited from their largesse (in some form or the other), whether you asked for it or not. Surely, they even have a list full of names to keep track - possibly divided in naughty and nice. Perhaps it is not in the stocking you ought to be looking at. You'd better take a look outside. What is that? What are those piles made up of? Is it snow? Maybe the carol singers have the answer. Oh, the virus outside is frightful But the vaccine is so delightful And since we've no place to go Let it borrow, let it borrow, let it borrow Man, it doesn't show signs of stopping And the auctions are really popping The yields are turned way down low Let it borrow, let it borrow, let it borrow

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed