|

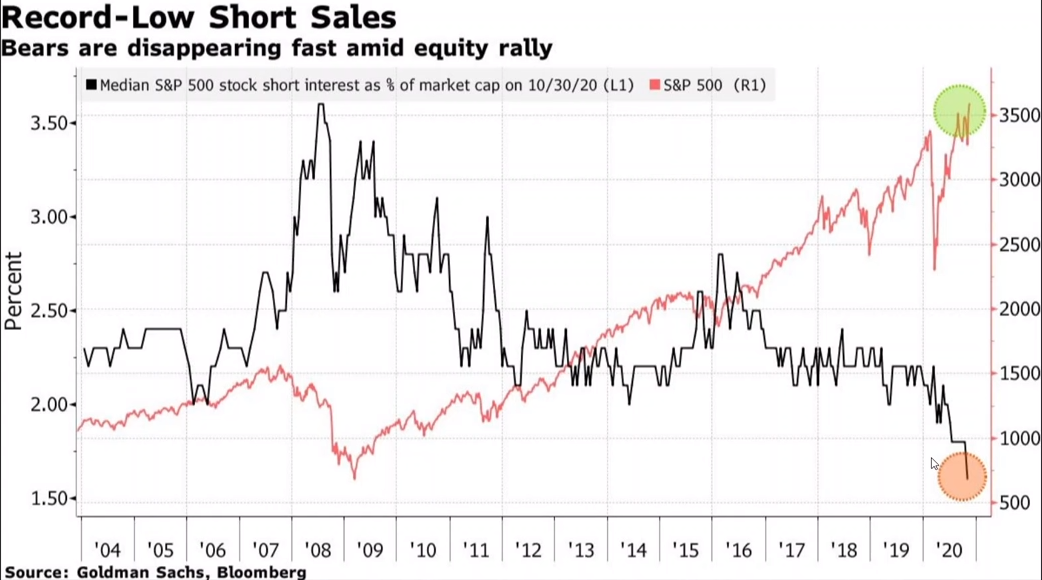

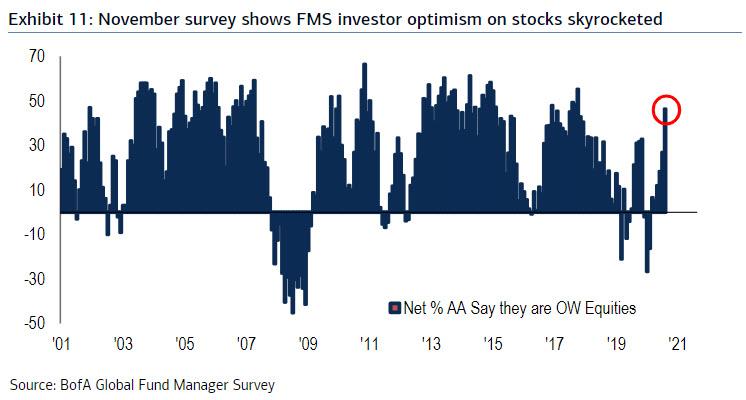

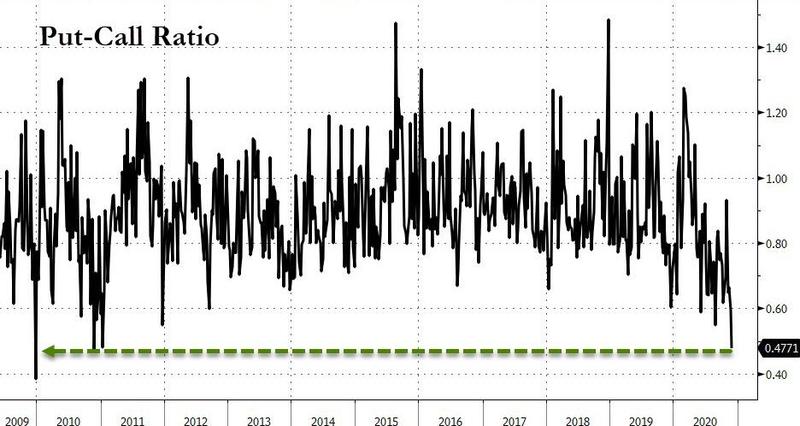

Astonishingly, even after 13 years of failing to deliver on their promises, speculators' trust in central banks and in policy makers is running stronger than ever. On the face of it, all is needed for the economy to boom, jumping all the obstacles popping up on the horizon, is our benevolent government officials and members of parliament, with the help from the (putative) almsgivers at the central banks. Evidently, as I demonstrated several times on this blog, particularly on the three-part-plus-bonus Eurodollar system series (parts I, II, III and bonus), this current monetary system is irredeemable - just like fiat currencies -, despite the smooth talking and alleged mastery central bankers purport. Moreover, the increased government meddling on economic activity has brought about, and will continue to do so, a progressively less dynamic economy with ever more distortions of the production structure, what the Austrian school followers call malinvestments. Accordingly, does the recent renewal in stock markets across the globe, and the financial markets to some extent, have a leg to stand on? Undoubtedly, you already know the answer. Nevertheless, allow me to dig deeper. Due to market participants being full-on risk-on, underestimating, or simply ignoring, all the dangers brewing underneath the surface, complacency is through the roof. One statistic that suggests this is the short interest of the S&P 500 that you see below, which is being historically low. Hence, it is no surprise stocks worldwide are having one of their best months ever.  To back up this upturn, here are two more graphs. On the right, the Bank of America Global Fund Manager Survey (FMS) is telling us that investor optimism, as measured by the equity weighting, has not been this high since 2017, when everybody was on the synchronised-global-growth bandwagon. On the left side, the put-to-call ratio, of the S&P 500, has not been this low since the end of 2009, when the GFC was on the rearview mirror and everyone was assuming growth was going to regain its pre-crisis vigor. Ostensibly, empty promises are an extremely powerful drug. The fact that so little insurance (put options) on the event of a crash is being acquired, it speaks volumes on how delusional, or under the influence, investors are.

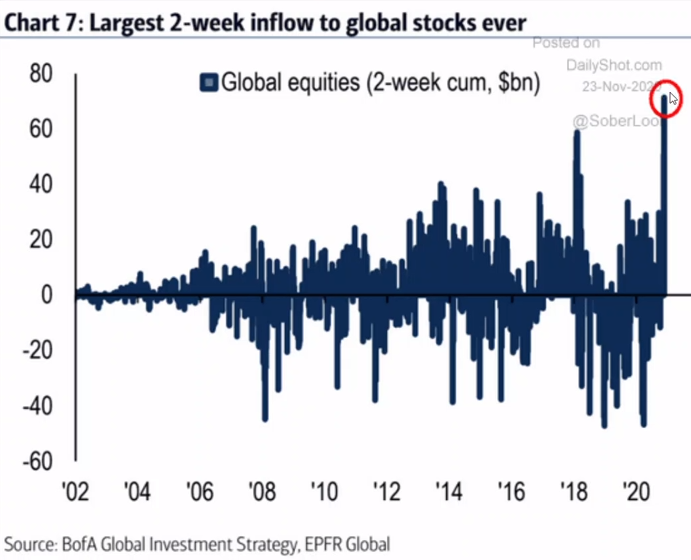

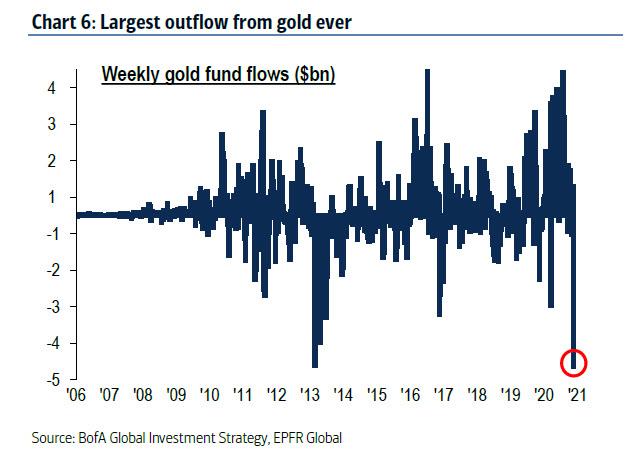

Likewise, fund flows prove speculators are inebriated by the hallucinogenic "stimulus" drug. On the one hand, investors have never piled up this much long positions of global equities, by a fairly big margin. On the other hand, investors are abandoning the gold ship - I guess because gold does not float - at a record pace before it sinks. Although the Eurodollar system must be sighing in relief, in view of the gold demand being inversely related with the confidence in the monetary regime, investors are going to find out that they have made a monumental mistake for the ship is of the space kind.

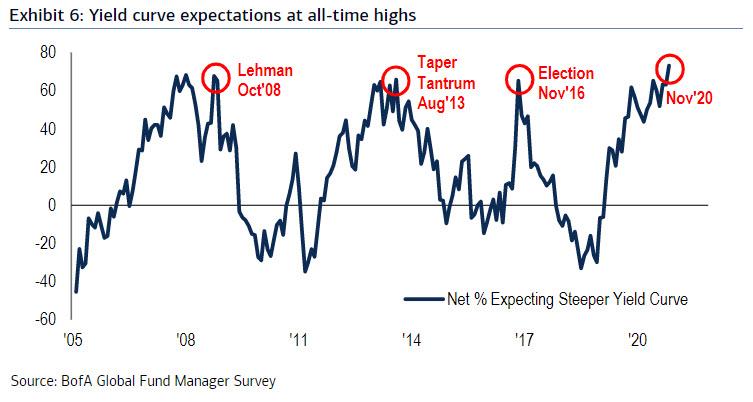

Recalling what I stated on the last instalment of this series, "there has to be more than hope and wishful thinking so as to have the much-anticipated reflationary recovery". Notwithstanding, investors are easily duped by the technocratic scientism. Thus, the FMS is indicating that investors' growth expectations are at levels not seen since the middle of the dotcom bubble. To top this accomplishment, expectations for the slope of the yield curve have never been greater. Unfortunately for investors, both of these bode poorly for stockholders.

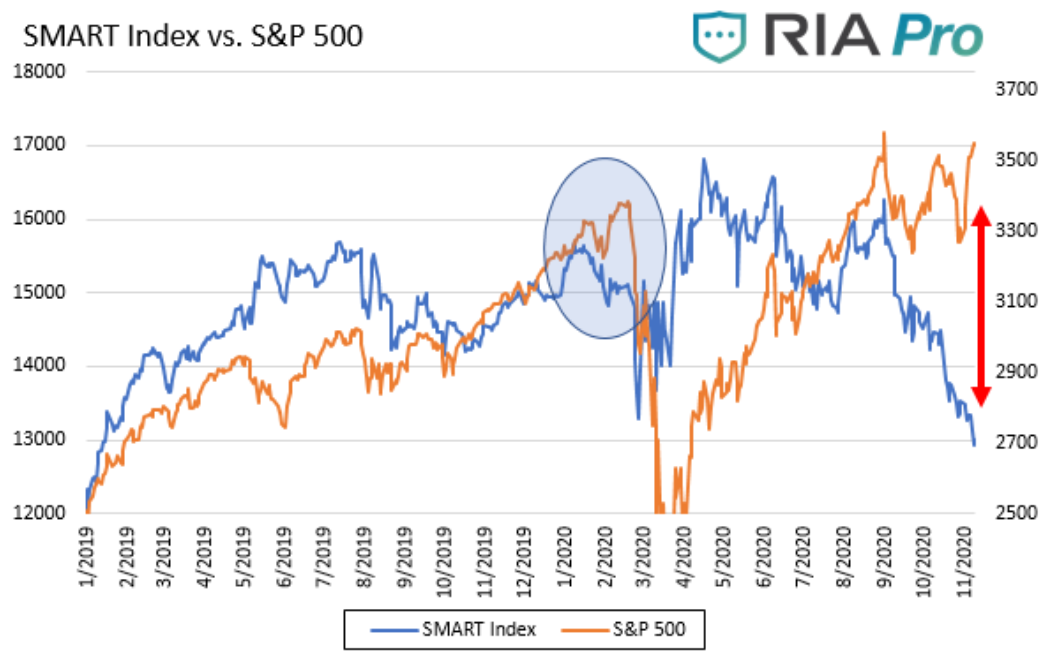

In spite of seeming to be under the influence, the explanation for the rally may be far simpler. Perhaps, market participants are just being greedy. After all, as Milton Friedman said in an interview with Phil Donahue in 1979: "What is greed? Of course, none of us are greedy. It’s only the other fellow that’s greedy". However, they appear, instead, to be following Gordon Gekko's mantra: "Greed is good. Greed is right".  Finally, let's take a look at the Bloomberg’s Smart Money Flow Index, which is a measure of how "smart money" is positioning itself in the S&P 500. The logic behind the index is that smart investors tend to trade near the end of the day, while more emotional-based traders dominate activity in the first 30 minutes of the trading day. Having said this, the index is calculated as follows: yesterday index level minus the opening gain or loss plus the change in the last hour. As shown below, the Smart Index and the S&P were well correlated until late August. Since then, as highlighted by the red arrow, they have diverged sharply. Therefore, it ought to be expected they will converge in time. In addition, the light blue circle shows they also diverged, albeit to a much lesser extent, in January and February as the smart money correctly sensed problems. Curiously, even though since late August the early bird has been catching the worms, these (the worms) are getting wiped out, resulting in the demise of the "dumb money". As a matter of fact, those patient investors, who are led by the macro data and financial conditions in lieu of the "stimulus" and vaccine hype, are ultimately going to be proven correct, feeding on these stupid birds' carcasses, kind of like vultures do - just to maintain the bird analogy.  In conclusion, last week, Atlanta Fed President Raphael Bostic said on CNBC, on Tuesday 17, "the vaccine is definitely positive news and it will definitely lead to a pretty robust recovery once it gets into the population deep enough". Then, he followed this by claiming "[the Fed is] going to be paying really close attention to the numbers moving forward to see whether this weakness in retail sales translates into something more deep".

Despite nobody taking this pronouncement for what they are, this is an admission about the Fed's prospects on the economy. Indeed, Bostic inadvertently acknowledged the economy is not recovering and, to add insult to injury, it is rolling over, as retail sales figures are ostensibly implying. As a result, once investors come out from their heroin-like reflation euphoria trip, the hangover is certainly going to be brutal. Hopefully, no baby is going to die from neglect, although doom and despair will abound.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed