|

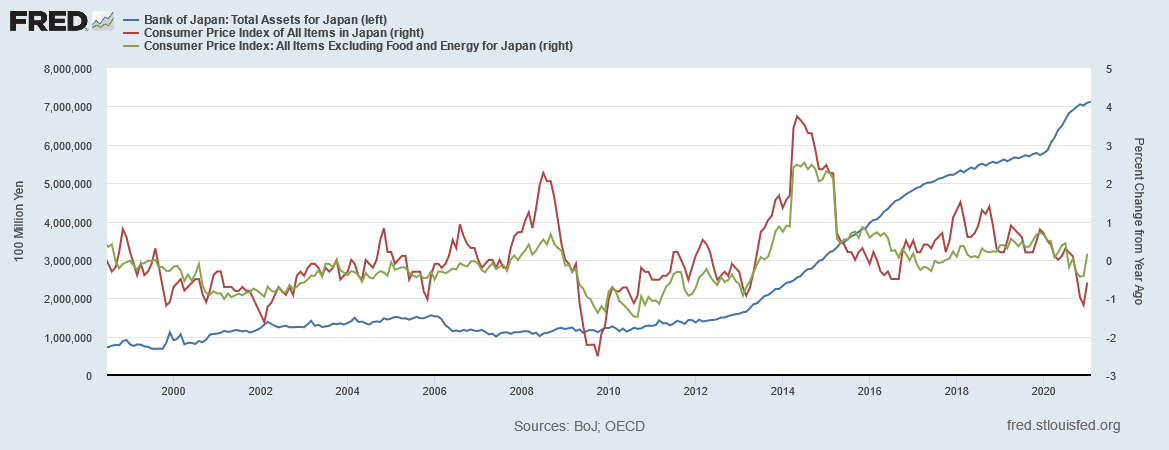

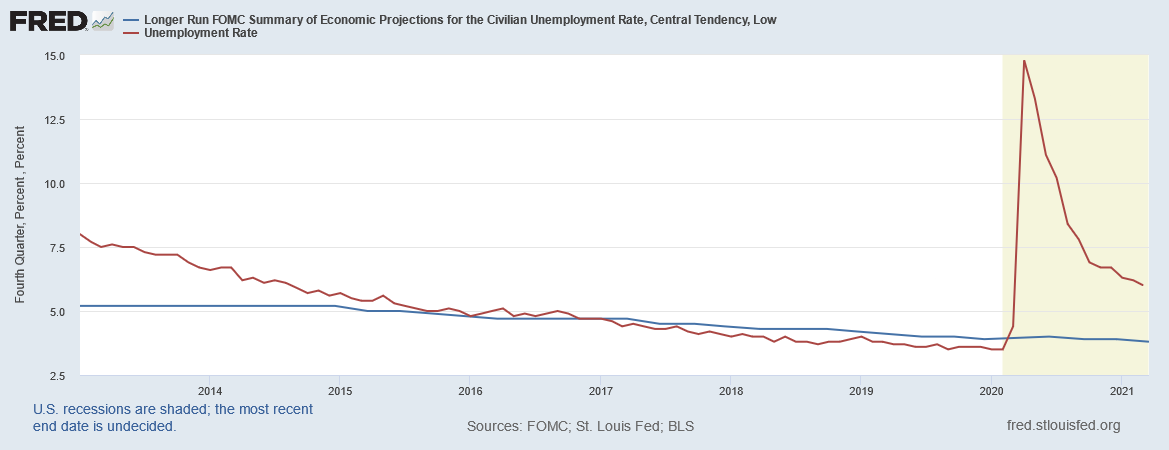

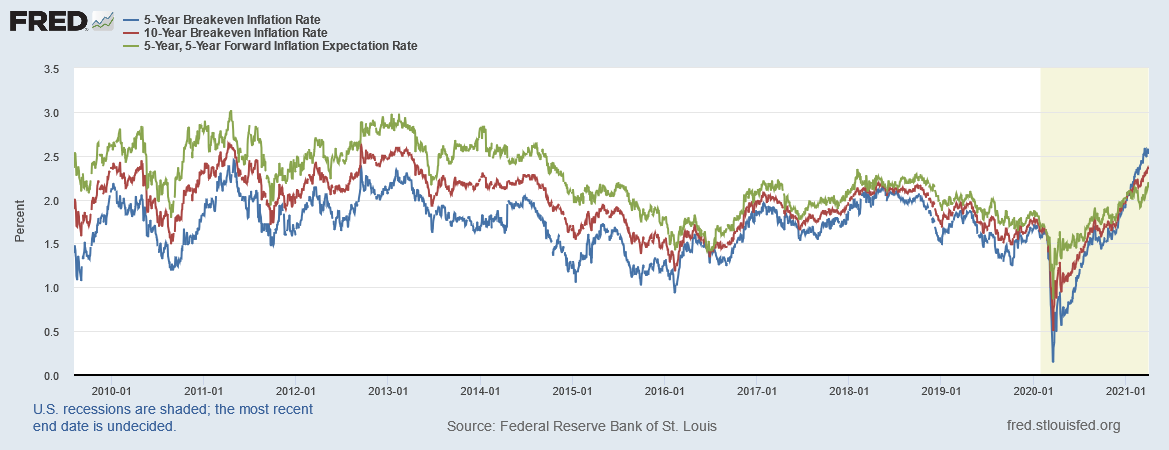

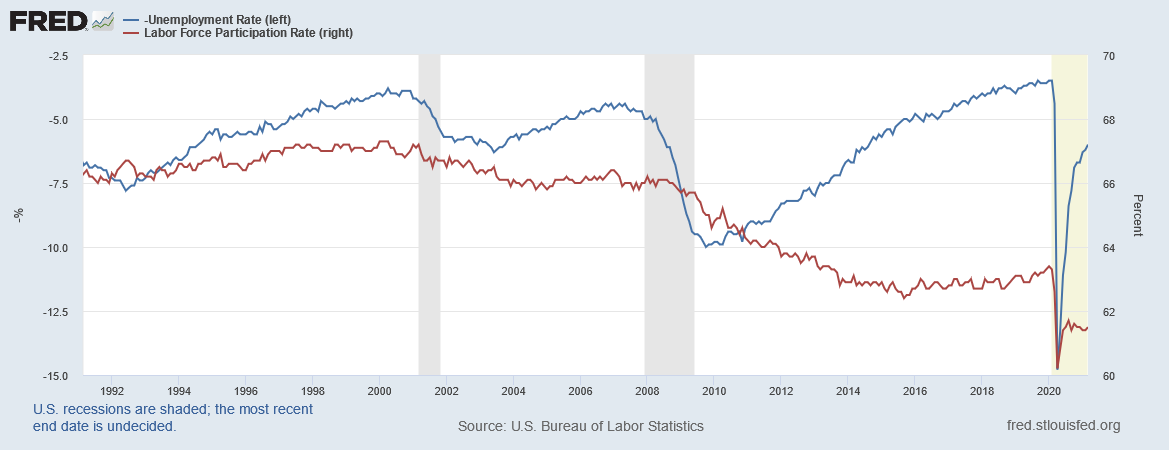

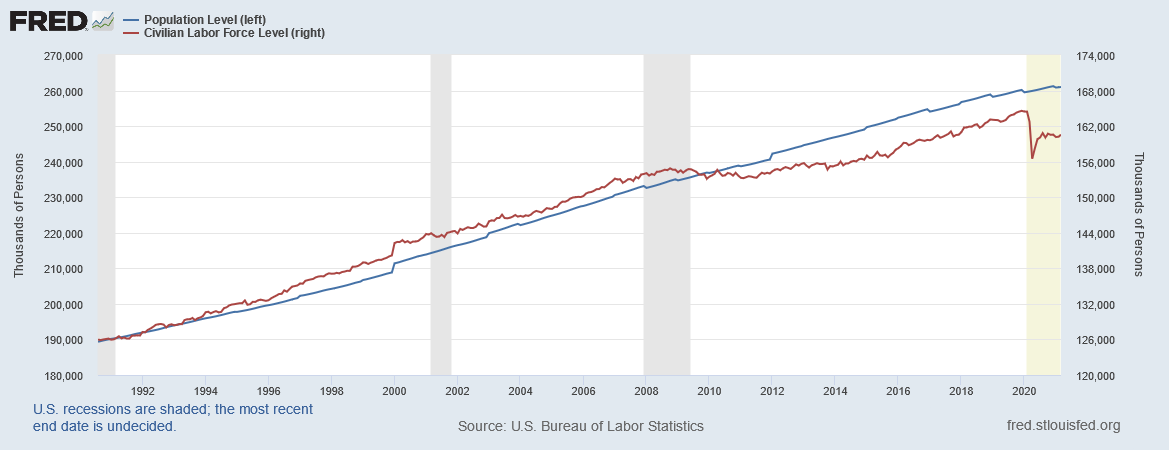

In spite of not knowing the origins of this holiday, the customs have spreaded worldwide, being celebrated with hoaxes and pranks, especially by the media. As you may be aware, today is April Fools' Day, though I am not going to do any practical joke. Instead, I am dedicating today's post to my favourite fools: central bankers. To be fair, it is not just the technocrats in the monetary domain that, in my book, have earned the right to be labelled this way. Be that as it may, and having already discussed other domains, particularly the shamans of public health, this post is about the plan that the monetary wizards have been adopting recently, which is ostensibly gaining traction across the globe. On August 27 2020, during the annual gathering at Jackson Hole, Wyoming, Chairman Jay Powell unveiled the Fed's updated blueprint. As part of its November 2018 announcement of a grand strategy review, the Fed hosted 15 Fed Listen events which "engaged a wide range of organizations - employee groups and union members, small business owners, residents of low- and moderate-income communities, workforce development organizations and community colleges, retirees, and others - to hear about how monetary policy affects peoples' daily lives and livelihoods". While those were taking place, a conference was organised on June 2019, where some of the most prominent (keynesian) economists presented their econometrics-filled papers. Then, on the following month, July 2019, the FOMC arranged 5 individual working groups, each consisting of teams of the brightest mainstream analytical staff, grinding away over arrays of data in order to supply the FOMC with every bit of information they managed to process. As a result of all this arduous labour, the new policy framework would have been devised in the most unassailable manner possible. Given away by the title of this post, the novel strategy revolves around the advanced mandate of average inflation targeting (AIT), as opposed to the ancient and outdated inflation targeting, which was typically a 2% annual rate. Firstly, this is not at all ground-breaking, not even in the US. As is usually the case, the Bank of Japan (BoJ) was the first central bank to introduce this policy, naming it "inflation-overshooting commitment". On Sptember 21 2016, the BoJ announced its newfangled plan, Quantitative and Qualitative Monetary Easing with Yield Curve Control (QQE with YCC). In this revised framework, besides aiming at fixing the yields of the JGB's market - which they cannot do; it is simply a trickery -, "[t]he Bank will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds the price stability target of 2 percent and stays above the target in a stable manner". Despite the belief that this development in monetary policy, combined with the expansionary fiscal policy carried out by Shinzo Abe's government, was going to navigate Japan's economy toward overcoming deflation and achieving sustainable growth, the reality is that this was an absolute failure.   Moving over across the Pacific, although it was not dubbed average inflation targeting, on May 2018, the Fed released a statement claiming to be following a new mandate for inflation, which consisted of running the annual inflation rate "near the Committee’s symmetric 2 percent objective over the medium term". Obviously, a long run average inflation target is no different than the medium-term inflation symmetry. Nevertheless, you may be wondering why are they splitting hairs? In short, they have to make you believe they have various tools in their monetary kit so that you keep trusting their words and regarding them in high esteem to boot. Long ago, sometime during the 1960's or 70's, central bankers realised they were not central to the monetary system due to not being the ones producing the money. In fact, they were (and still are) not able to find a big chunk of it. Therefore, they resorted to inflation expectations management, in lieu of expanding the actual money supply. Hence, what all of this nonsense comes down to is a desperate attempt to prevent the illusion from shattering. Owing to coming up short for more than a decade (and in Japan for two decades now), these wizards are pinning the blame on the zero- or effective-lower bound (ZLB or ELB - same thing). Allow me to explain. The Great Recession was so bad because of the Global Financial Crisis (GFC), which demanded an immensely forceful monetary policy response. In nominal terms, it would have meant interest rates being pushed down much further than they could have been if the ZLB was not standing in the way. Having only 525 basis points (bps) to work with at its onset, looking back on it, maybe the Fed needed 750 bps or a 1000 bps to properly offset the GFC and the Great Recession. Seeing that accommodative monetary policy, if you believe these things, is what contributes to recovery, not being able to introduce the right amount of it from the start put the economy into a sort of policy deficit. This is the moment QE enters the picture, with the mission of circumventing the ZLB by targeting real rather than nominal rates. In other words, to manage inflation expectations. This is precisely what the Fed's Vice Chairman Richard Clarida meant to convey on a speech delivered for the Peterson Institute for International Economics, on August 31 2020. In addition, he went on to affirm, encapsulating the rationale behind the BOJ's decision to do this "inflation-overshooting", that inflation expectations were of limited use because the Fed had spent decades positioning itself as an inflation fighter. On account of the public and the markets, he implied, regarding the central bank in that way, the 2% inflation target has come to be viewed as an inflation "ceiling". Once the economy generates 2% inflation, everyone presumes the Fed will come in and take away the punch bowl (even if it might still be needed). Ergo, the Fed had to steal from the page of the BoJ's playbook where it is defended that a commitment has to be made "that allows inflation to overshoot the price stability target so as to strengthen the "forward-looking mechanism" in the formation of inflation expectations." Secondly, although the focus has been on the inflation rate target, there was another monumental reassessment in this grand strategy review, which also considers a key rate that indicates the soundness of the economy. Not only is the absence of recovery implicit in this symmetry and average inflation targeting nonsense, the strategy document also spells out the most important part of it all: the unemployment rate conundrum. In view of being guided by a dual mandate (inflation and employment), "deviations of unemployment from the Committee’s assessments of its maximum level" set the course of action. As you will notice here, that part was stricken and, in its place, "shortfalls of employment" from the estimated maximum level made the entrance. By dropping "deviations" - plural - and replacing it with the term "shortfalls", the idea that employment could be "too much", therefore requiring the Fed to raise rates (and other "tightening" hocus-pocus) to cool off an overheated labour market, is apparently no longer maintained. According to the Phillips Curve, a labour market running too hot can be inflationary. Clearly, they still hold this belief, though they are making it clear that such a scenario is far from their minds so as to reinforce their goal to manage inflation expectations. Moreover, the grounds for making this change is one that have left first Janet Yellen's and then Jay Powell’s central bankers scratching their heads. Time and time again, the estimates for what they call maximum employment (i.e., full-employment) had been reduced, because in late 2014 and early 2015 the actual unemployment rate would have dropped underneath the lowest long run calculation (top graph). With no inflation in sight, and expectations for it falling hard (bottom graph), the Fed’s statisticians had no choice but to go back to the drawing board and redraw their picture for full-employment. So they did, a laughable 12 times in all. If you are left with the impression they are really not cut out for their jobs, having no clue of what they are doing, then welcome to the club.   Unsurprisingly, the headline unemployment rate (U-3 in the US) must have been flawed and, consequently, extremely misleading. The flaw of this statistic lies in the labour force participation, rendering this rate to be enormously deceptive all the way from 2008 to today. Basically, the unemployment rate’s denominator, the labour force, had all along left way too many out of it (meaning it had been, and still is, a mathematical problem for both the numerator and the denominator). As the next couple of charts demonstrate, the proportion of people that left the labour force remained subdued after plummeting as a consequence of the brutal shock derived from the GFC and the decaying economic landscape engendered by government interventionism to curb that shock. Hopefully, the corona-phobia-induced recession may still resolve itself differently, recovering to the employment and participation levels, as well as the growth trend, of the pre-kung-flu era. However, the prospects do not bode well for the future like I explained last week.

What had moved inflation expectations if not full-employment or even favourable views on the faulty unemployment rate? The obvious answer was available the whole time and not just in the TIPS market. From nominal rates to swap spreads to the dollar’s exchange value, and several others, the Eurodollar system is shown to be in charge of everything. As a matter of fact, the direction of financial markets (even stocks at times) in addition to the global economy are dictated by the overriding condition in the global monetary regime and its true reserve currency. Finally, it seems this central banking "novelty" has crossed the pond and reached the European shores (oh boy!). In an interview with Philip R. Lane, member of the Executive Board of the ECB, for the Financial Times, he stated that, and bearing in mind that a strategy review is in the making at the ECB (which was announced in January 2020), "if there is a strategic commitment that following a period of undershooting you signal that the correction phase is not just going to the target but going moderately above the target for a period (...) I think there is a very strong logic to that." Evidently, logic is one of their strengths. Notwithstading, all options (whatever they are) are on the table. Although "[t]here is a very strong analytical case for flexible average inflation targeting, (...) there are other options that may also be successful in anchoring inflation expectations." Thus, AIT is still not guaranteed to be implemented here in Europe, though between you and me, we know it will since they have nothing else up their sleeves. Sadly, we also know that nothing will change, with the deflationary/disinflationary environment continuing to haunt us.  To conclude, despite the efforts made to elaborate the strategy review and the scientific appearance of its conclusions, the central bankers' mandates and tools have been the same since (at least) the advent of the Eurodollar system. Whether they create more bank reserves (the actual "money printing") or less, or make ever more grandiose promises and more creative labelling, it is the global monetary regime that has the final saying, no matter how many times and how many of them swear to "never gonna give you up, never gonna let you down" - you really have to watch this; it will make your day.

Therefore, for being extraordinarly pig-headed about the inner workings of the monetary system and the scope and efficacy of their mandates, central bankers have merited to make this day all about them. Congratulations!

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed