|

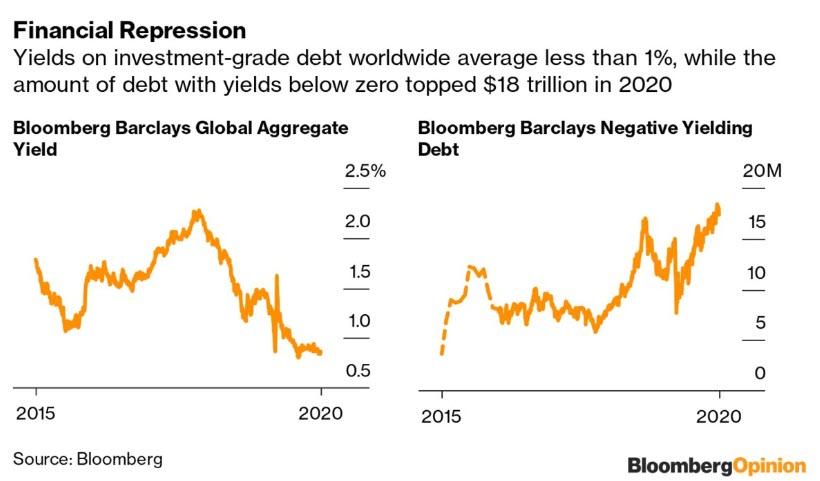

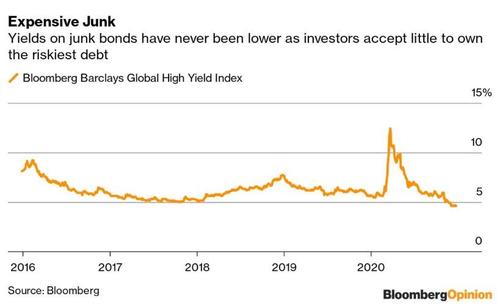

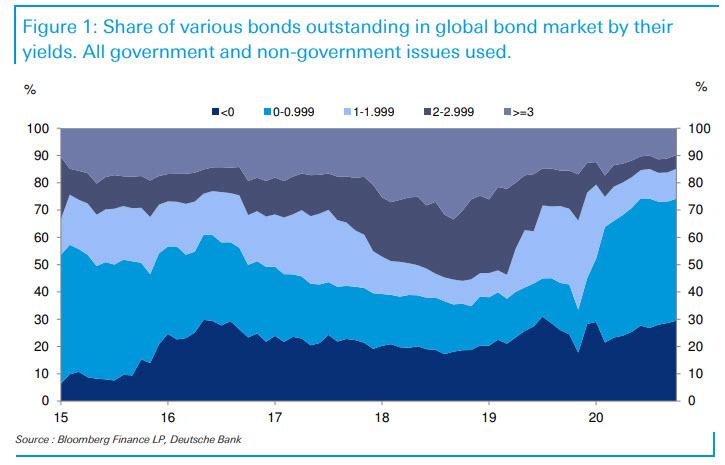

Following the discussion introduced in the previous post about the record amount of worldwide total debt, with a special focus on the governments' debt, today I am zooming in on the realm of businesses. To be specific, the corporate bond market. Regardless, let's first zoom out and take a bird's eye view of the broad bond market. In this way, you will have a comprehensive grasp of what bonds are suggesting, although you should have an inkling of what they have been hinting at - certainly, you will know by the end of this post. On account of a massive deflationary environment brought about by the hysteric corona-phobia, liquidity has been the top concern for participants in the financial markets - in the real economy too, though this analysis does not concern them. Accordingly, investment grade bonds have been an oasis of liquidity during this inhospitable desert that has been the 2020 economy. Evidently, yields have been falling all around the globe to an even lower level than at the onset of the March meltdown, averaging roughly 0.9%. On the same note, the amount of debt carrying a negative yield has surpassed the record set in 2019, reaching the $18 trn mark. To boot, the Fed nor any other central bank is the culprit for this so-called "financial repression" - inflation above interest rates so that the debt-to-GDP ratio gradually comes down. No matter by how long or how much they do their QEs, credit and "liquidity" facilities, YCC, etc, these are all smoke and mirrors aimed at duping you into believing they possess the mastery over financial markets (Eurodollar system: part I, II, III and bonus).  Of course, nobody wants to own bonds that pay next to nothing, or even negative rates, unless they have to for regulatory or other reasons. Hence, it is true there has been a scramble for yield, primarily for the debt obligations of companies and others with below-investment-grade credit ratings, which partly explains the historical strength of the HY bond market. However, I would argue that this market's performance has recently been a victim of the reflation narrative caused by the vaccine development and stimulus exultation. To sum up, due to liquidity concerns and then the reflation fantasy, rising demand pushed yields on bonds issued by these entities to a record low 4.59% worldwide on average. Even so-called frontier nations such as Ghana, Senegal and Belarus are benefiting. Furthermore, the graph on the right depicts extremely well this rush for safety I have been expounding. As you can imagine, the US Treasury debt has a considerable share of the global bond market. Therefore, the big shift that occurred this year, in relation to 2019, from the 1-2% yield range to the 0-1% range, was in large part because of the belly of the UST yield curve (2-year to the 10-year) dropping like a rock in Q1. Overall, the 0-1% bucket has surged from 15.7% to 44.7%, approximately. According to Deutsche Bank calculations, only 14.9% of global bonds have a yield above 2% and only 9.9% carry one above 3%.

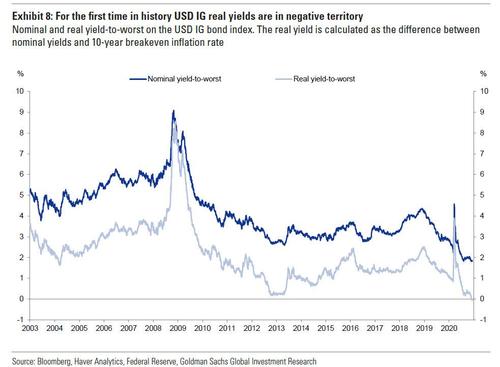

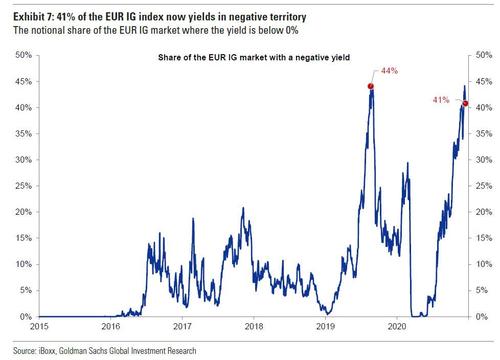

Meanwhile, thanks to liquidity preferences in such a sterile environment, there is an almost record-high level of EUR IG bonds with negative yields. As the following chart on the right shows, as of December 15, 41% of the EUR IG iBoxx index yields in sub-zero territory. This is a level that matches the previous record in August 2019. Even more impressive is the fact that more than 10% of the index now yields below -0.25%, according to the annual recap note published by Goldman's chief credit strategist Lotfi Karoui. Similarly, the US corporate bond market is still somewhat more normal than the one in Europe, it too is starting to Japanify, with USD IG real yields (below on the left) turning negative. This means that while most of the focus on negative yielding corporate debt has been concentrated on nominal yields in the EUR IG market, real yields on USD IG corporate debt have also turned negative for the first time in history.

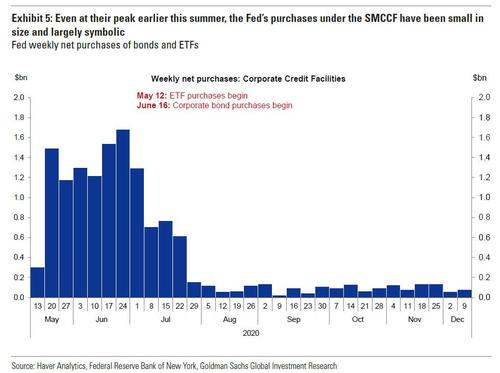

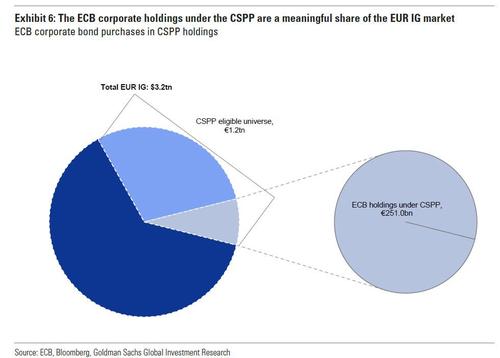

Although the Fed’s announcement has apparently triggered a swift recovery of the new issue market, especially in HY where activity had been paused for a few weeks in March, the Fed’s purchases have been largely symbolic – consistent with a lender of last resort posture. Some have argued that the market's trust on the ability of the Fed to step in "in size", if and when necessary to buy everything, was all it took to restore the normal functioning of these markets. To put this in context, since the Fed's Secondary Market Corporate Credit Facility (SMCCF) buying started in mid-May, a tiny $14 bn of bonds and ETFs (below on the left) have been purchased on a combined, cumulative basis, while the size of the US Investment Grade market is more than $8 tn and the SMCCF eligible universe has a total face value of $1.9 trn (and $520 bn when applying the SMCCF program purchase limits, such as issuer constraints). As a testament to the Fed's jawboning, in recent months the amount of SMCCF purchases has been tremendously light, as the program nears its expiration on December 31, 2020. Notwithstanding, despite the Fed's corporate bond purchases being modest, the same can not be said of Europe, where first Mario Deaghi and then Christine Lagarde have been on an epic bond binge. As a reminder, the ECB started purchasing corporate bonds well before the Fed in March (it did however accelerate its pace of purchases after the March meltdown). As a result, the ECB now owns a record 8.5% of the entire EUR IG market. As Goldman calculates, the ECB continued to deploy its balance sheet in the corporate bond market, growing the size of its portfolio to €272 bn, €251 bn under the CSPP and an additional €21 bn under the PEPP. This compares to €185 bn at the start of the year, and is 24 times more than the Fed's purchases of corporate bonds. In other words, whereas the Fed successfully managed to jawbone the bond market into a state of confidence, where prices do not fall even when the Fed barely transacts, Europe has failed miserably, and bond market participants have now habituated to the ECB buying billions every week - so the story goes anyway. On this account, the ECB currently owns 23% of the eligible universe of securities and 8.5% of the broader universe of EUR IG corporate bonds outstanding.

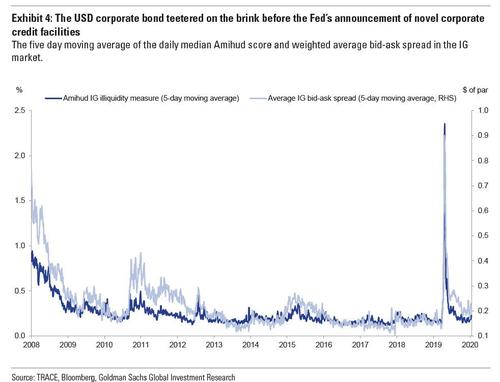

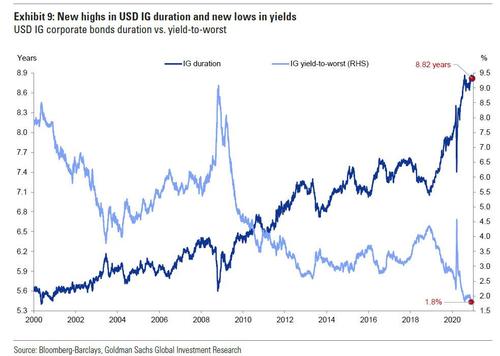

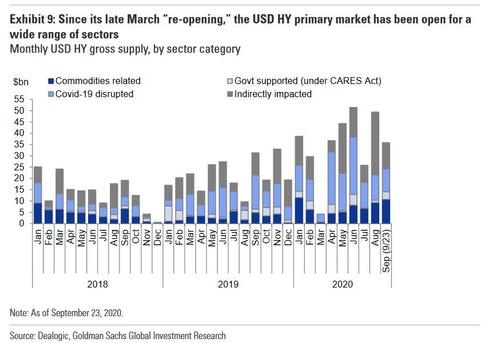

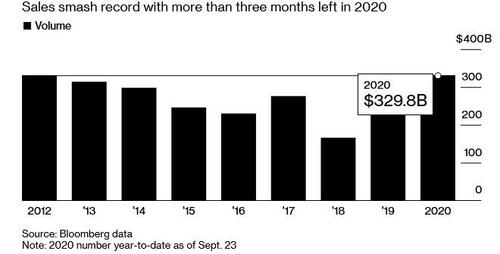

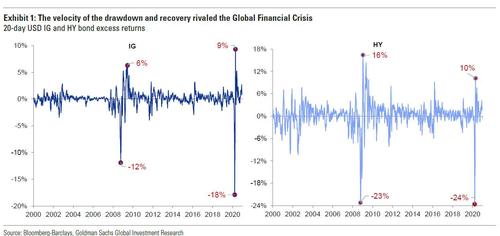

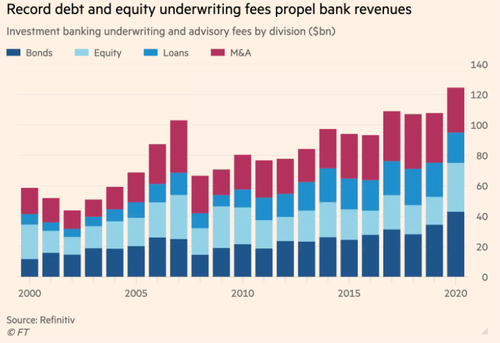

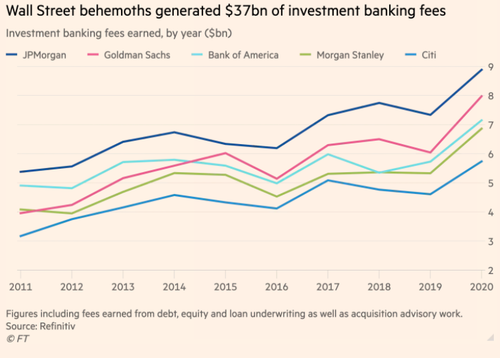

As Goldman declared, the "pandemic pushed market microstructure to the brink of collapse" and at the height of the COVID-19 hysteria, "the USD corporate bond market teetered on the brink of collapse as liquidity dried up faster and more severely than it had during the Global Financial Crisis". The chart below shows just how dramatic these moves were. In just a few short weeks, we went from a well-functioning and relatively liquid market, to the exact opposite as we entered non-linear territory. Then came the day which will live in central banking infamy - March 23 - the day the Federal Reserve announced its "novel" Corporate Credit Facilities, and coincidentally just as fast as liquidity had dried up, it returned. For believers in the central banking mastery, the announcement the Fed would buy corporate bonds in both the primary and secondary market, including investment grade and junk bond ETFs, coupled with the direct injection of over $10 trn in "liquidity" by central banks in the span of just weeks after the March crash, has precluded the collapse of hundreds of trillions of dollars in rate-linked securities. Ergo, the corollary being if the Fed had sat idly by, the western capital markets would have imploded.  A new corporate debt issuance record was set when ten IG bonds priced for $6.85bn on September 29, shattering the monthly sales record for the sixth time in the last seven months. The borrowing spree comes on the back of a lockdown-fueled liquidity grab, as companies sell record amounts of debt at all-time low yield, using the proceeds either to refinance existing debt, maybe to resume buybacks, but mostly to get a comfortable cash cushion. The September monthly IG supply stood at $162.7 bn, passing the $158 bn record total for the 2019 September. Until then, July was the only month since March not to set a new high water mark for the respective month, according to Bloomberg. Despite the record YTD (till September-end) new issuance momentum, supply has slown into year-end with just $150 bn expected in 4Q, down about 20% over the same period last year, as most companies that could take advantage of the wide open issuance window have already done so. This year saw the average duration of the USD IG market materially increase, further extending a trend that started in late 2018. This increase reflects the proactive behavior of corporate borrowers which have been taking advantage of low yields and strong investor appetite to bolster their liquidity positions and extend the duration profile of their liabilities. The flipside of this tailwind for issuers has been a notable increase in the risk profile of IG portfolios.  Likewise, the HY new issue market has been surprisingly receptive to a wide range of sectors since its "re-opening" in late March – including those groups at the epicenter of the corona-phobia disruption. The chart below illustrates this by showing monthly USD HY gross issuance volumes by four broad sector categories: 1) commodities related; 2) government supported, under the CARES Act; 3) directly disrupted by the coronavirus/sudden stop in the economy; 4) and indirectly impacted.  As the above chart shows, directly disrupted and government supported sectors have generated significant amounts of supply in each of the past few months, indicating the market’s continued willingness to lend to groups facing persistent headwinds related to social distancing and business restrictions. Once again, the reason is not the Fed's explicit backstop of the corporate bond market since March, when Powell announced the Fed would purchase corporate bonds and ETFs, but the flight to liquid instruments. In fact, on the prior week, September 23, before the US IG bond market smashed the annual issuance record, sales of high yield - the term is used very loosely these days - debt hit a record $330 bn, surpassing the previous full-year record of $329.6 billion in 2012 (with still three more months to go in 2020).  In a nutshell, the sudden stop in global economic activity and the subsequent policy response sparked the fastest drawdown and recovery in the three-decade history of the USD corporate bond market. This is illustrated in the next graph, which plots the 20-day excess returns on IG and HY cash indices since 2000. While spreads peaked at tighter levels relative to the Global Financial Crisis, the velocity and the magnitude of the downward move was quite comparable, having been even worse now in IG. Ostensibly, as they would have you believe, owing to the strong policy response (both on the fiscal and monetary fronts), the speed of the recovery was even faster than in the aftermath of the Global Financial Crisis. As a matter of fact, since the Fed’s announcement of the Corporate Credit Facilities on March 23, the IG and HY bond markets have rewarded investors with cumulative excess returns to Treasuries of 20% and 28%, respectively.  Moreover, the global capital markets business, such as equity and debt sales, has erupted during the pandemic. Given that liquidity has been the top priority since the corona-phobia began, it was not hard for a large corporations to conduct an equity or debt deal. As a result, investment banks earned a record amount in fees for underwriting various types of deals. According to the Financial Times, 2020 was a record year for companies raising more than $5 trn in debt markets. Naturally, all that money raised means corporate banksters were able to collect handsome fees. "While multinationals first moved to draw down credit lines in March, they quickly shifted to the bond market to lock in longer-term funding," affirmed the FT. In the end, investment banks earned about $42.9 bn underwriting debt deals, up 25% over last year. In addition, David Konrad, an analyst at DA Davidson, said that through equity offerings corporations managed to raise $300 bn this year. In terms of IPO fees, the revenue from underwriting initial public offerings jumped 90% to $13 bn, the highest since the end of the Dot Com bubble (2000). Overall, equity underwriting revenues nearly doubled this year to $32 bn from 2019's $18.3 bn. By the way, compared to last year, merger and acquisition advisory fees fell 10% to $29.6 bn. In total, investment banks across the globe generated a record $124.5 bn in fees this year as companies desperately raised cash to survive the pandemic and, more importantly, whatever scenario lies ahead. Finally, as you can see on the graph on the right, the biggest Wall Street banks (JPMorgan Chase, Goldman Sachs, Bank of America, Morgan Stanley, and Citigroup) earned a combined $37 bn in investment banking fees this year, the highest in more than a decade.

To conclude, because corporations have long ago realised they cannot depend on the banking sector nor, particularly, on the Fed or any other central bank to get their liquidity needs satiated during financial panics, they spent the immediate months after the March meltdown hoarding as much cash as they could.

Even though monethary authorities have been very active cunning the public, with the help from the media and economists, their efforts have been simply irrelevant to bring markets to normalcy. Just think about it. If central bankers are really at the helm of the markets, and the economy as well, would the March meltdown even happened?

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed