|

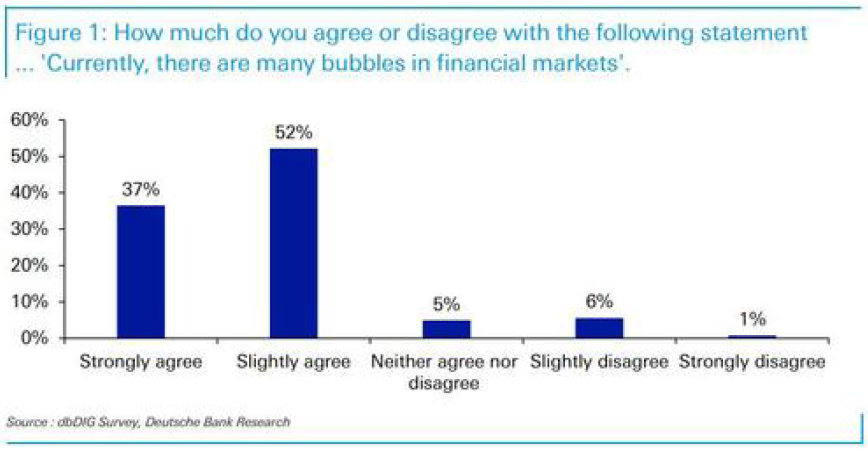

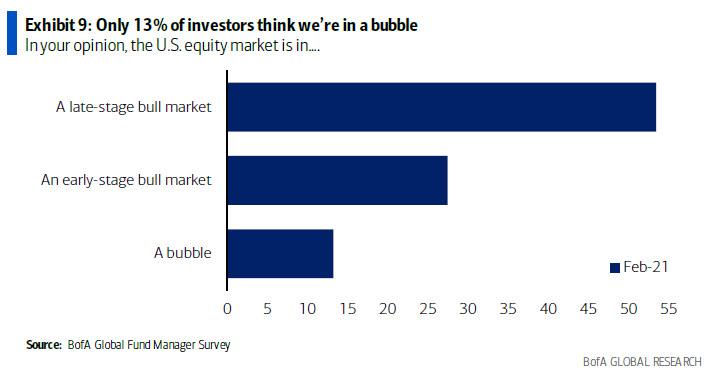

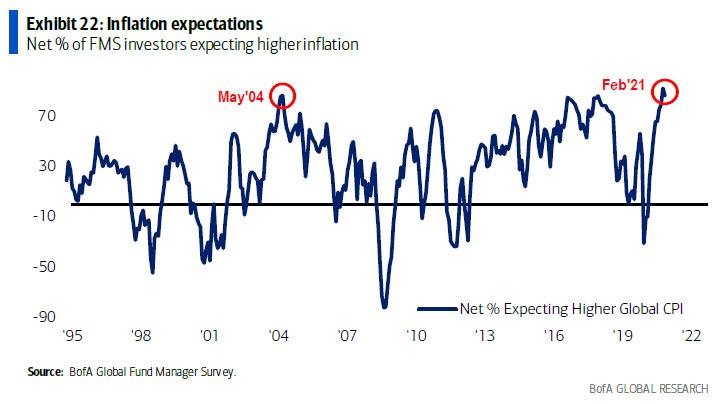

Having a financial crisis after experiencing a tremendous one just a year ago, is something few people are expecting. Regardless, one would be foolish to completely dismiss a crash right around the first anniversary of the last one. However, in spite of being very little reason to suggest a repeat of the 2020 Global Financial Crisis (GFC2), or anything close to it, is going to occur in the following weeks, some indications point for a new financial system meltdown not being as fanciful as the laws of probability would have you believe. Be that as it may, I still think the most plausible scenario is for some correction in the markets, particularly in the stocks' one, due to rising instability as the (winter) quarter-end bottleneck nears. Following the GFC2 and lifting of restrictions during last spring, every market, from stocks to high-yield bonds, has gradually been returning to pre-corona levels, having been driven by the assumption that the (global) economy was going to totally and immediately recover, like the flick of a switch. With all the monetary and fiscal "stimuli" injected in the economy and financial markets, the much hoped for "V-shaped" recovery was in the bag. Although the real economy not experiencing the putative recovery, the presidential election results, the vaccine discoveries, as well as the Blue Sweep in Congress, propelled markets, in general, to assume the economy is bond to roar, 1920's style. Without surprise, the stock markets have been the main adherents to this narrative. Albeit a worldwide phenomenon, let us just focus on the US financial markets. In view of going through such a monumental rally since early November, according to Deutsche Bank, by late January most of the respondents (89%) were seeing some bubbles in financial markets (left graph). Curiously, the Bank of America Global Fund Manager Survey (FMS) of February (right graph) reports that only 13% of the managers surveyed took the view that the US stock market was in a bubble. Notwithstanding, more than half of them felt the bull market was getting exhausted.

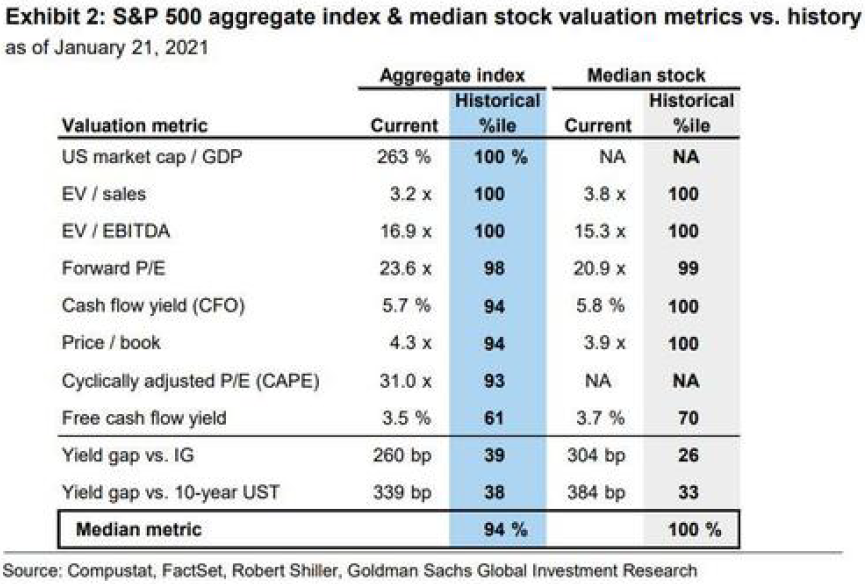

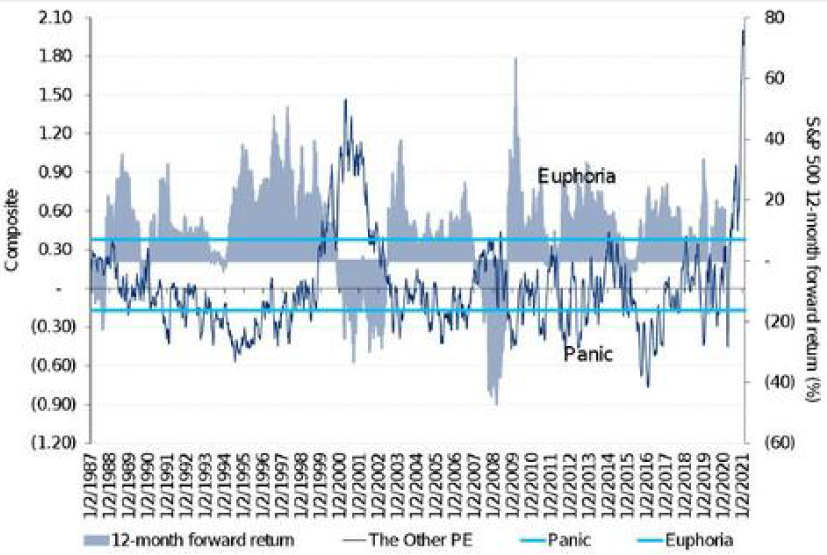

On account of this topic deserving a post (at least) for its own, the discussion about the stock market being at fair value or in a bubble, despite being interesting and important, it is rather irrelevant for today's subject. Surely, there are several of indicators that are, or have recently been, at and near all-time highs, though valuation metrics (left chart) do not tell the whole story. Nevertheless, there has certainly been bubble-like behaviour. Starting with the army of day-trading Robinhooders, receiving their investing tips in highly esteemed financial venues such as Instagram and TikTok, strolling to the relentless amount of IPOs and SPACs that only seems to end when everybody and their mother have one, in addition to the outperformance of stocks with negative earnings, and ending with the short squeeze fueled by r/wallstreetbets crusaders, there are definitely some resemblances to a bubble. As the chart on the right shows, which is Citi's Panic/Euphoria model, investors have never been this euphoric, auguring horribly for the 12-month forward return of the S&P 500.

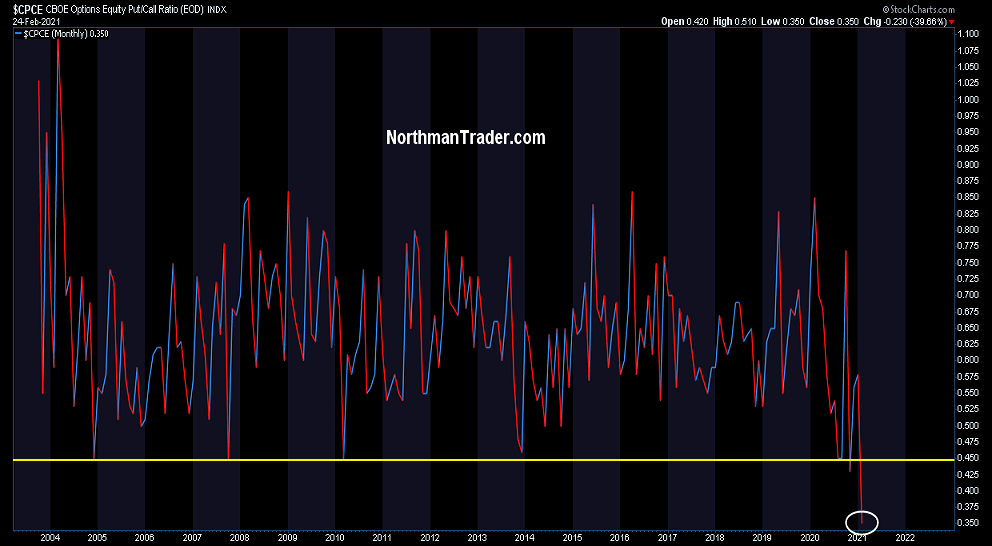

Moreover, the new round of stimulus checks, as part of another $1.9 trn package, which is set to be enacted very soon, "could unleash a $170 bn wave of fresh retail inflows to the stock market, according to Deutsche Bank AG strategists." Therefore, it is no wonder why the demand for puts has not accompanied the surge in call-buying - as demonstrated in the historical low on CBOE's put-call ratio (left chart) -, because ever since the March trough, short-sellers have been slaughtered, as the the graph on the right depicts.

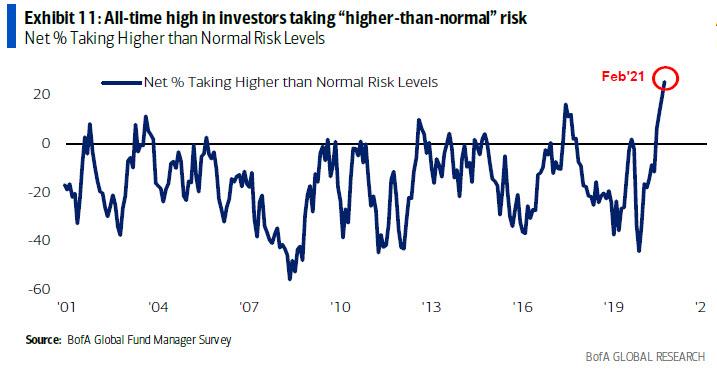

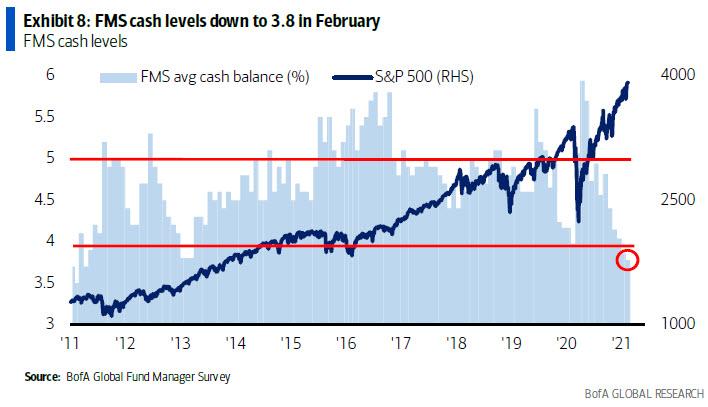

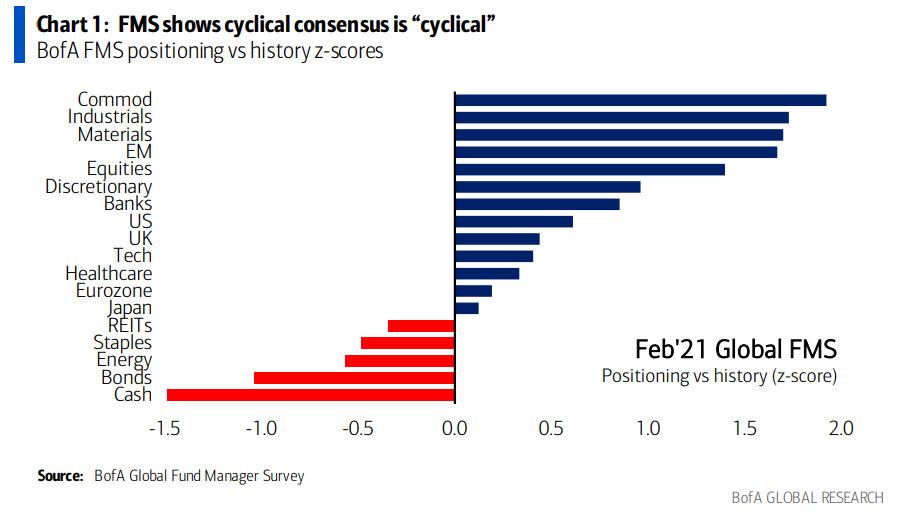

All the same, the reverence for the technocratic institutions responsible for all the record "stimuli" has prompted those in the financial services industry (as reported by the FMS) to take never-before-seen levels of risk. Hence, their cash balances has not been this low since 2011, which proved to be a bad decision by the middle of that year (Eurodollar #2). So, an eventual liquidity stress is far from the managers' minds. What could possibly go wrong?

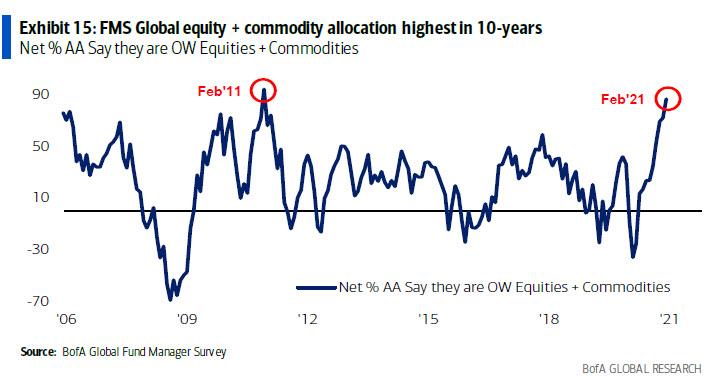

Thus, investors are positioning themselves according to either the "roaring 20's" or the "commodities supercycle" narratives, or more likely both of them. Bearing in mind what I asserted on Monday, "[a]s soon as individuals start seeing their bank accounts ballooning through their own endeavours in the economic system, as opposed to handouts from the political system, consumption will pick up, although that is naturally taking a lot of time to ensue. Nevertheless, one thing is for certain, as long as society holds this collectivist mindset that is beholden to politicians and technocrats, an economic boom, worthy of this designation, will never happen and, thus, a commodity supercycle will have to be deferred".

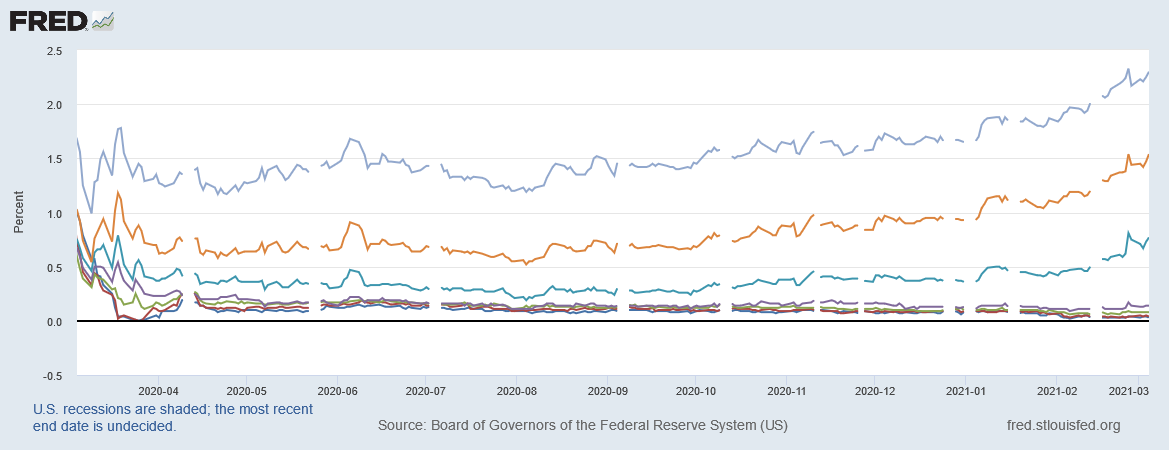

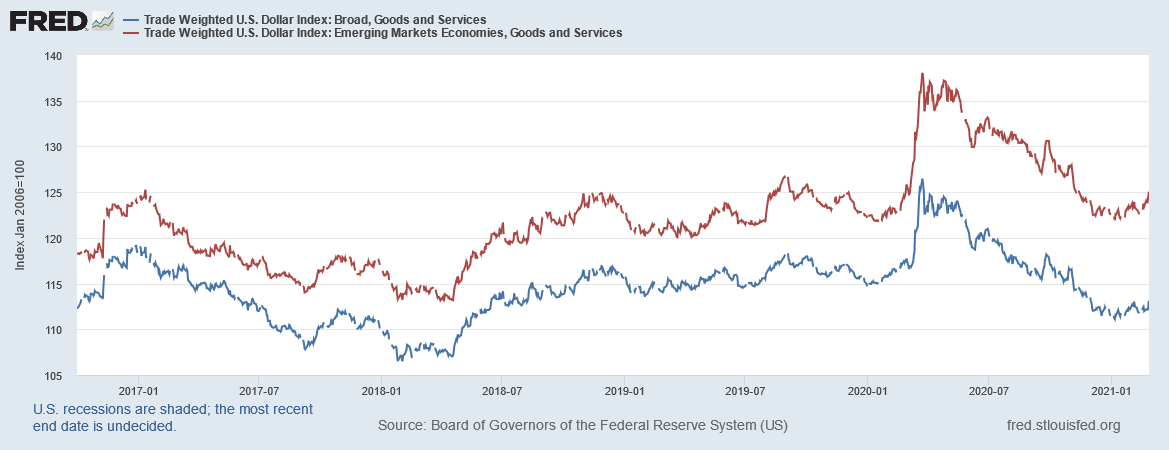

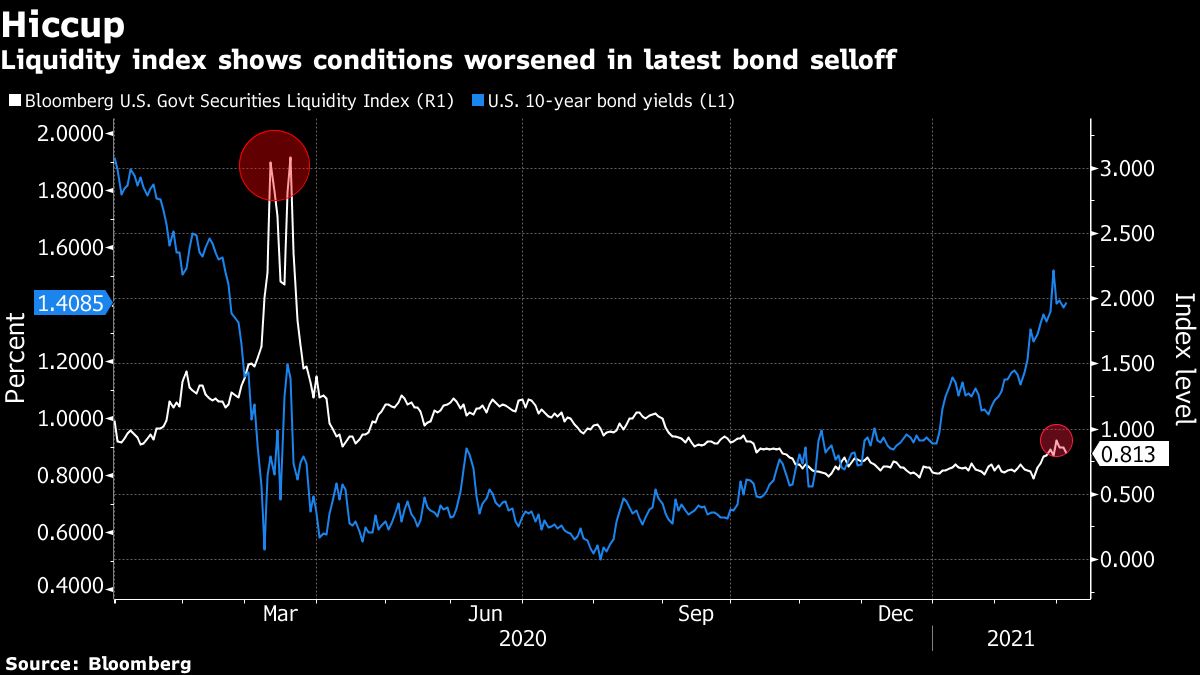

At least one bank is getting worried about the prospects for stocks. According to Bank of America’s Sell Side Indicator, which tracks average recommended stock allocation by Wall Street strategists, by rising to 59.2% it is signaling that bullishness is overextended and is now time to sell. Although that supports the view that equities are overdue for a correction, it does not insinuate that a financial crisis is on the horizon. For that, we have to look at other indicators and markets. Having said this, the T-bills (along with the 2-year; left chart) and the US dollar (right graph) have been implying since the beginning of this year that, as a reflection of the state of the economy, financial conditions have deteriorated. Obviously, this alone does not mean the markets are about to crash. However, it suggests that the financial system (Eurodollar) has been growing more wary of potential deflationary risks, and rightly so.

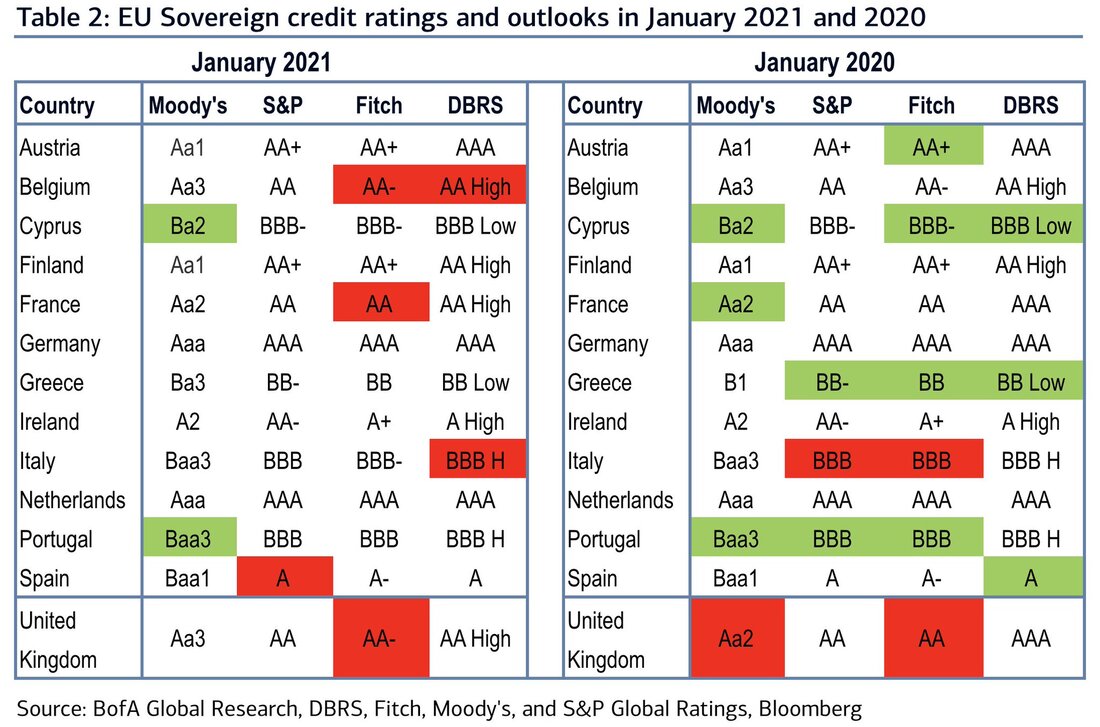

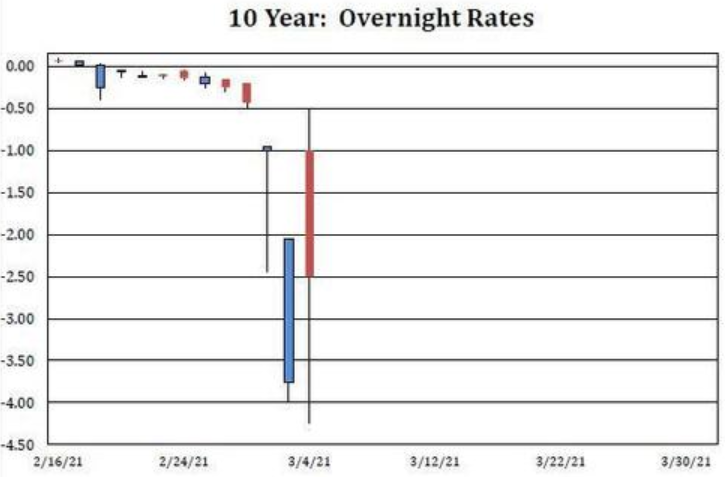

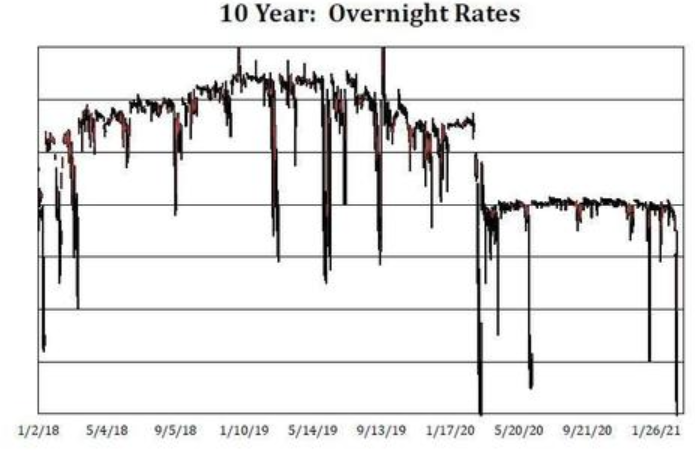

In case it is not clear in the graph above and you have not been paying attention, yields of the T-bills have curiously been dwindling since early November, being extremely close to the zero lower bound. Lately, the explanation for this has been something to do with the Treasury General Account (TGA). More specifically, the TGA is the account the US Treasury Department has at the Fed. Supposedly, due to the release of fiscal "stimulus" engendered by Uncle Sam on the economy, the TGA balance will decline from $1.6 trn to $500 bn by the end of June. Basically, this roughly $1 trn decline will occur either through waves of fiscal spending, which will expand deposits and reserves at large banks or, if spending is too slow to meet the $500 bn target, through bill paydowns. Furthermore, coupon (notes and bonds) issuance will be $1.4 trn over the first half of the year, which will be bought mostly by banks. However, an obstacle arises. The Supplementary Leverage Ratio (SLR), which, as the name implies, supplements the US leverage ratio by taking into account, besides on-balance sheet, certain off-balance sheet assets and exposures - learn more here; what consists exactly is not important, though -, is going to be fully implemented as the regulatory break (enacted during the GFC2) is set to expire on March 31. Unsurprisingly, this re-imposition is going to once again include US Treasury securities and deposits at the Fed (bank reserves) on the calculation of this rule. Allegedly, owing to the SLR, the commercial banks in the US, mainly the primary dealers, do not have the balance sheet at the bank operating subsidiary level to add $1 trn of deposits, reserves, and Treasuries. Unless we get an extension on the SLR relief, banks will have to turn away wealthy households’ and institutions’ deposits, which will then go to money market funds. Despite that, money market funds will face a constraint too. The marginal asset they will direct inflows into, the Fed's overnight reverse repurchase agreement (ON RRP) facility, is capped. Each money fund can place only $30 bn into this facility, which is just too little. In fact, banks’ balance sheet constraint becomes a collateral constraint for money market funds. Even though collateral supply from coupon issuance will absorb this cash over time, money markets react to what happens now, and with $1 trn of new cash, there may be many pockets of collateral scarcity as these flows play out in real time. So as to resolve this, the Fed has to intervene once more and allow intermediaries to park that extra trillion dollars in cash somewhere. Otherwise, if the Fed refuses to uncap the ON RRP facility, T-bills and repo could go negative. Going back a bit, what banks turning away depositors mean is that, in order to avoid complying with the cost of having "too many" deposits, the banks may impose a negative interest rate on those bigger deposit accounts. In addition, unless the Fed steps in aggressively and either grants banks SLR relief and/or the ON RRP facility is uncapped - so that banks have a place to park the "flood" of $1.1 trn in excess cash instead of turning it away - the US dollar Libor-OIS spreads are expected to reach zero by June, on account of foreign banks being the ones holding the bag, warehousing the rush of reserves. In part, I agree with this reasoning, particularly with the assessment the collateral scarcity will lead to lower yields. Yet, that whole point about banks running out of space for the safest and most liquid instruments (US Treasuries, bank reserves and cash) sounds ludicrous to me. As a matter of fact, since 2014, in spite of SLR being online, primary dealers kept on accumulating USTs and deposits without a problem. In my opinion, the plunge in T-bills' yields has been a result of, besides the diminishing supply being issued, rising concerns around the creditworthiness of individuals, businesses and governments as well, like the next table demonstrates. Being presented here the ratings of sovereigns, which are shown to have slipped, you can imagine what it has been like for companies and financial assets like corporate bonds and ABS.  Getting closer to the crux of today's matter, the overnight repo market has shown last week some irregular behaviour. As the chart on the left shows, the overnight repo for the 10-year Treasury traded deeply "special", which means the repo rate is negative, as a result of massive short-selling speculation. In a nutshell, so many investors are short the 10-year UST that there are not enough to go around. Ergo, the rate to borrow the 10-year in the repo market reached a low of -4% on Wednesday, March 3, and printed around -4.25% the following day (left chart). An investor lending out cash for the 10-year notes would end up having to pay, rather than getting paid. Oddly, that is below the -3% charge leveled on users who fail to deliver a security to a counterparty. Besides the colossal short base, the Fed has been taking supply out of the market through its large scale asset purchase programme, QE6. Evidently, this was the lowest print since the absolute record of -5.75% touched during the GFC2. Feeling the urge to act, "the Fed loaned $8.7 bn of its $10.9 bn holdings of US 10-year notes on Thursday, easing the debt squeeze", according to Scott Skyrm, executive vice president at broker-dealer Curvature Securities. By Friday, believe it or not, demand in the ON RRP facility peaked at $11.2 bn, apparently exceeding the Fed's holdings - seems too small an amount, though; perhaps $10.9 bn is what is alloted for this facility.

Moreover, because of the illiquidity/volatility that has impaired the smooth functioning of the financial system, it has not been just the Treasury market to feel the repercutions (right chart). What caused the small uptick in illiquidity was likely a mix of portfolio repositioning (reflation trade) and the "operational error" in FedWire, late last month, which triggered the latest correction in the stock market (left graph). Finally, in order to correct these key issues dealing with market functioning, a lot of people were awaiting for Powell or some at Fed to at least give the markets a hint that they were thinking about reviving Operation Twist, with the new one being the third instalment. In case you do not know, this programme consists of a simultaneous selling of front-end Treasuries (bills and shorter-term notes) and buying of longer-dated paper (bonds and longer-maturity notes). According to the advocates of such a policy, a Twist 3.0 will: i) pull up front-end rates; ii) stabilise back-end rates; and iii) it does so in a reserve neutral way that lessens bank SLR pressure to hold more capital. Hence, part of their solution entails taking from the market even more highly sought assets, even if they are wanted just to be shorted later on. Like I wrote a few paragraphs above, the SLR is no impediment for banks to hold more Treasury bonds and notes. Also, removing even more 10-year notes could precipitate more illiquidity due to shrinking supply of an instrument that is having tremendous demand. Notwithstanding, selling T-bills would surely help to satiate the impressive appetite for these assets, improving the health of the financial system.

Bringing it all together, as the squaring of the books take place in mid-March, and taking into account that illiquidity has been increasing, which has been indicated by t-bills and the US dollar (like was shown above) along with the peculiarities around longer-tenor Treasuries, it is reasonable to be concerned. Because of the ensuing collateral bottleneck that is to be expected, the safest and most liquid instrument, US Treasury securities, are going to be faced with a rush of demand. In view of the longer-dated Treasuries having an extremely big short base, a short squeeze will likely follow, not just pushing yields much lower, but provoking a huge liquidation in other asset classes, especially equities, to pay for the margin and collateral calls and to cover the short positions to boot.

In relation to what was discussed before about the SLR and its implications for short-term rates/yields, there is a real and rather big chance that these will go negative (because of collateral shortage) and, more importantly, stay negative (on account of unrelenting demand for the most liquid instruments). Undoubtedly, such a background emerging is set to feed more vulnerability in the (global) financial system. To conclude, do not let yourself be surprised by a new crash in the following days. Seeing that there are all of these factors causing instability as we approach the notorious March bottleneck, the potential for some serious turmoil is certainly here. However, as I stated in the beginning, a correction rather than a financial crisis is what seems to be more likely to happen in the next few days. Considering that markets participants will gradually awake up to reality and realise the economy is not recovering, with households and businesses going through terrible financial distress, whether the next financial crisis crops up this month or not is immaterial. What is important to understand is that, in all likelihood, one is bound to befall on the world in the near future.

0 Comments

Leave a Reply. |

AuthorDaniel Gomes Luís Archives

March 2024

Categories |

RSS Feed

RSS Feed