|

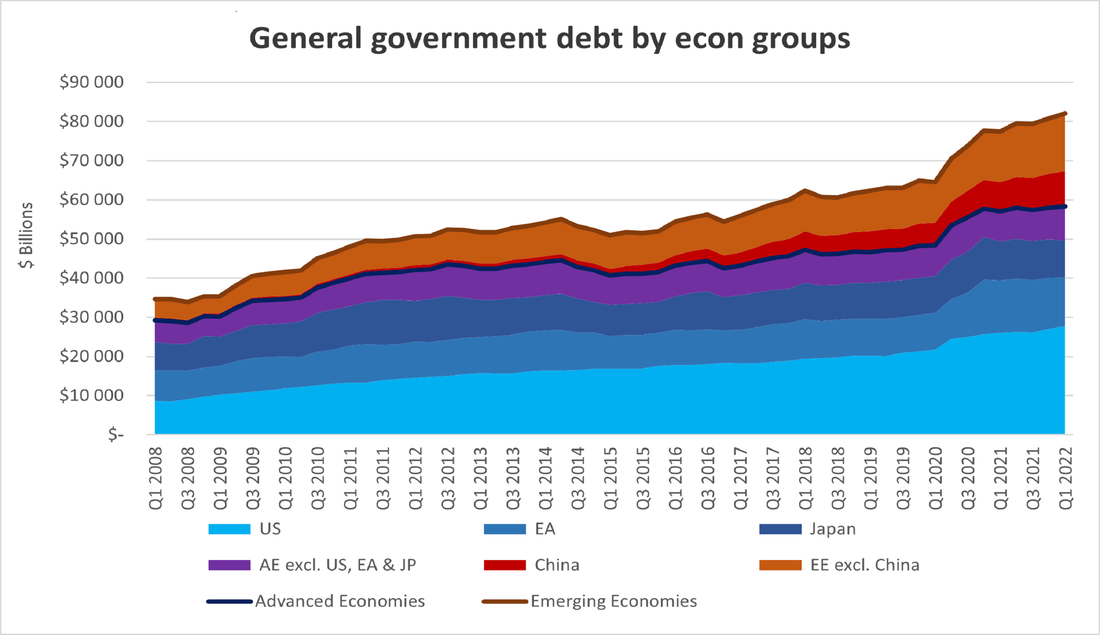

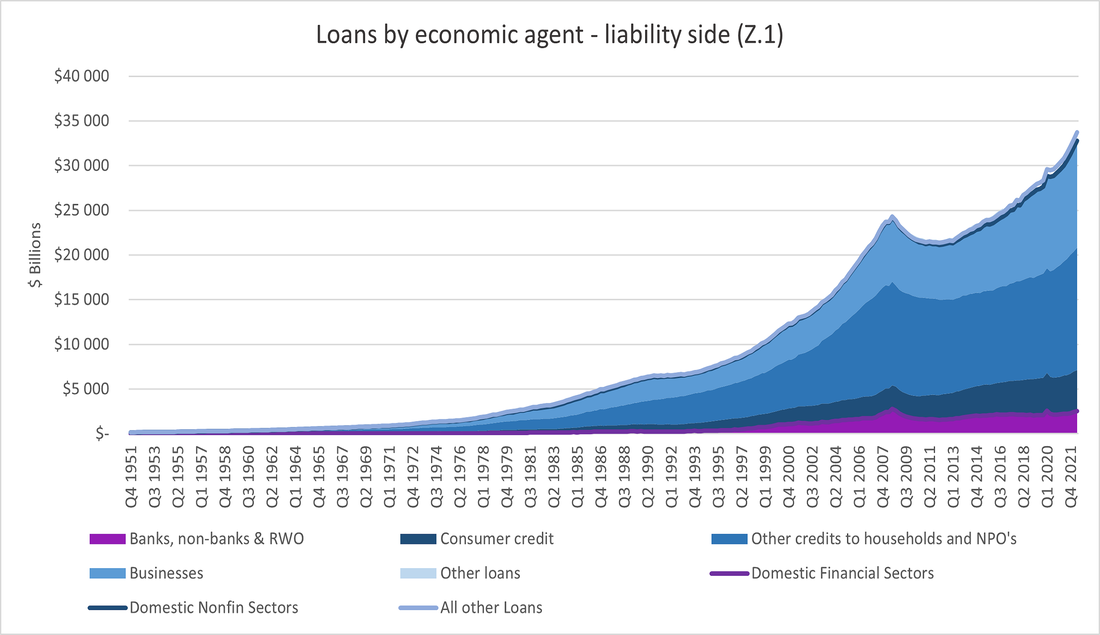

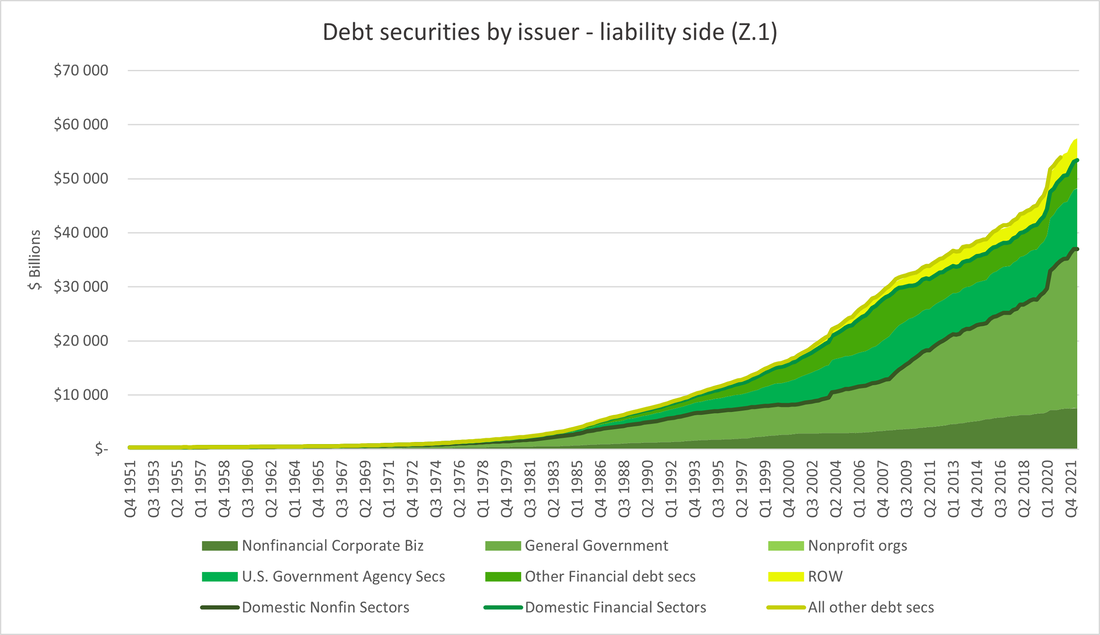

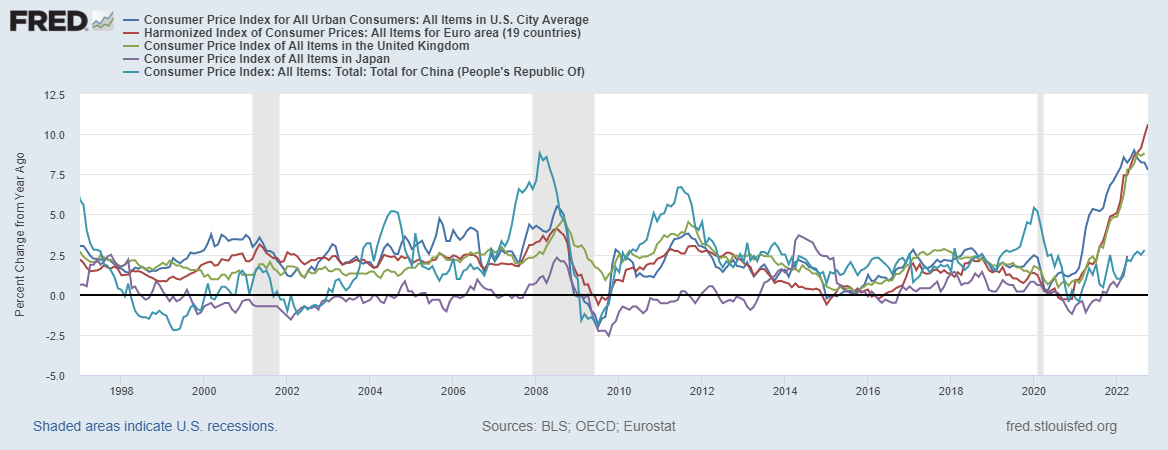

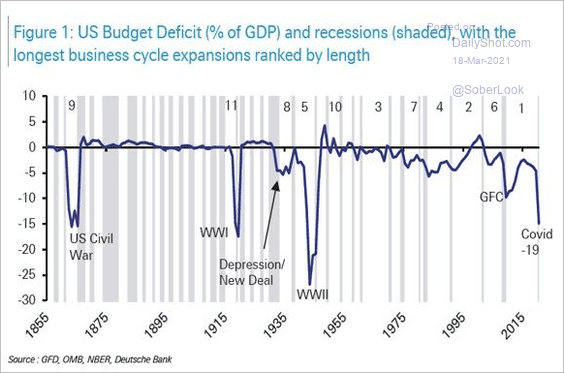

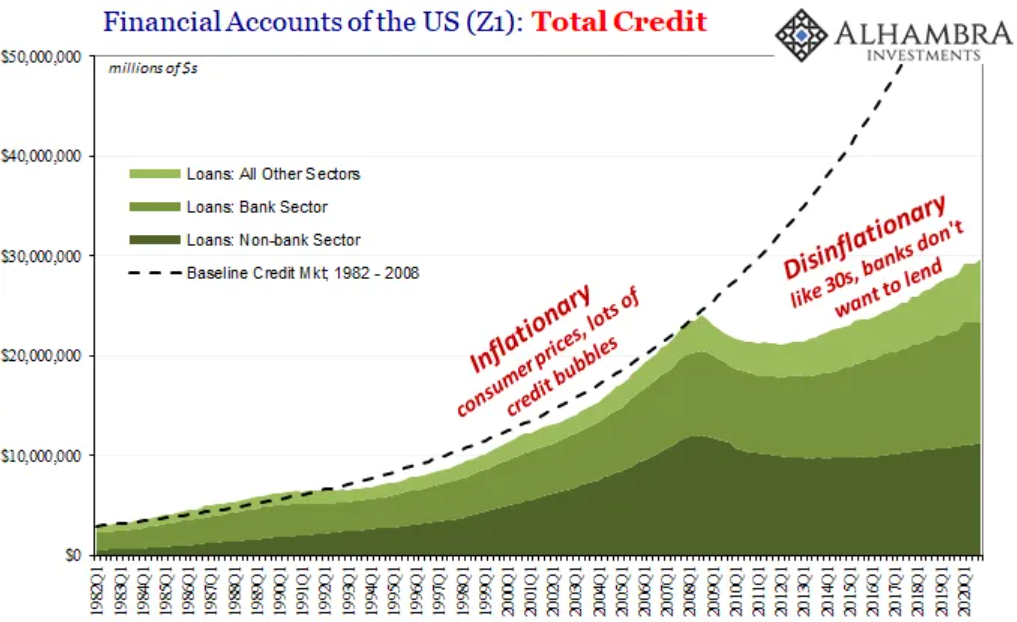

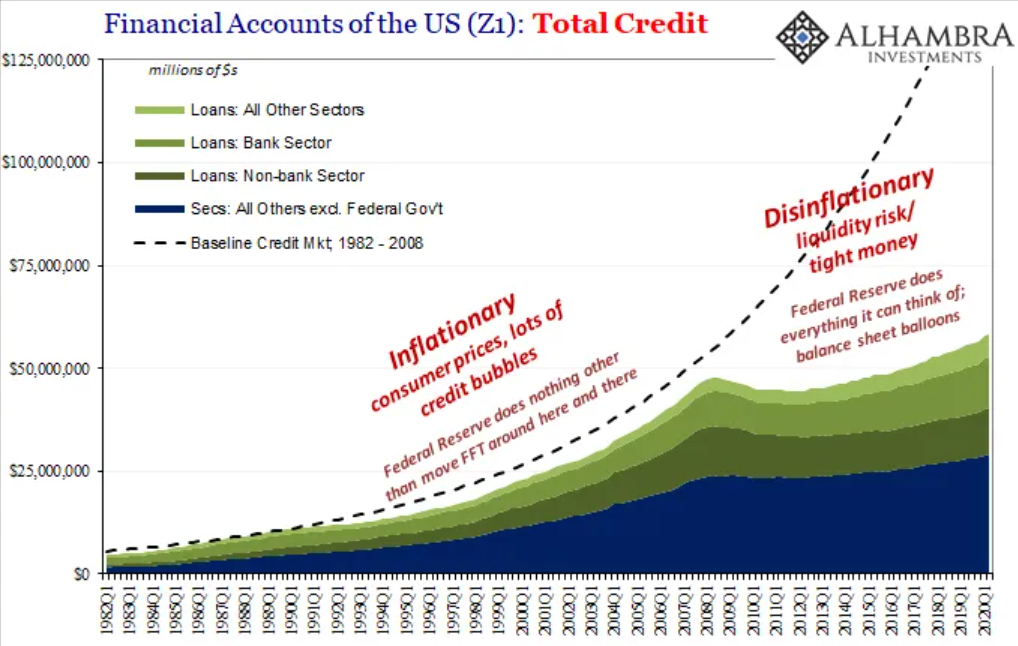

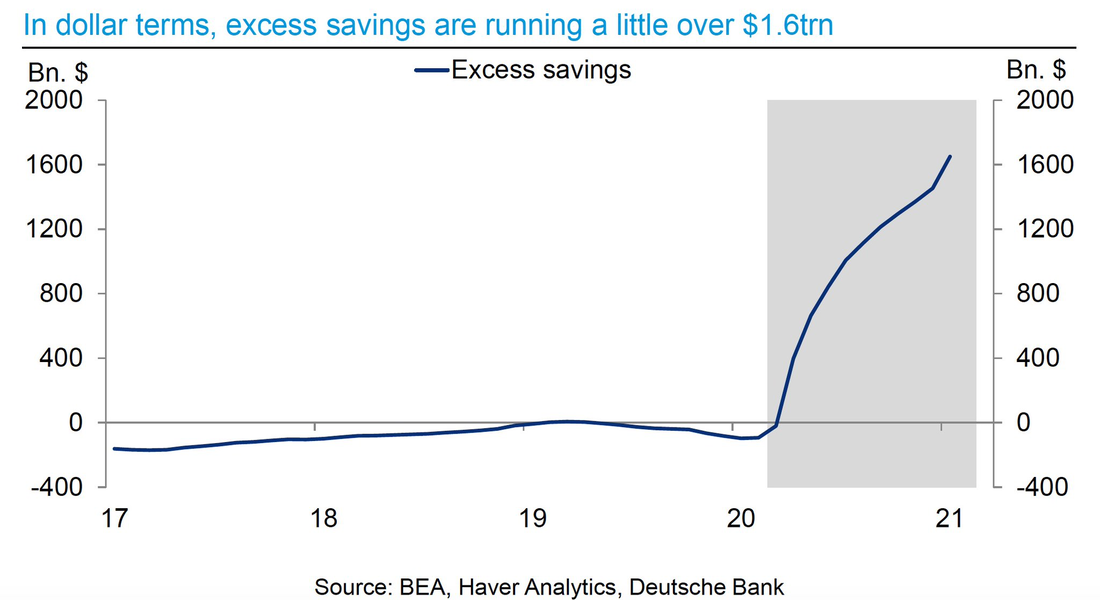

After a 16-month hiatus, I am getting back on the horse to resume analysing the economy and financial matters, as well as their prospects, of course. In view of the fact that the “inflation” rate has been higher than the markets, Keynesian economists, most financial analysts and myself too had expected since I last dropped a line, I felt it was high time I reviewed my reasoning so as to find out what I missed. Having said that, I must admit I was wrong about both the persistence and magnitude of the price increases of goods and services. What did escape my reasoning, you ask? In short, I never thought banks and other credit institutions would be so stupid and reckless as to open their spigots so damn hard and keep them open until now. Hence, the topic of today’s post is exactly this: the various factors that led to this relentless, but still transitory, “inflation”. Since that last article on June 2021 was published, the rate at which prices in the real economy grow has reached levels not seen in a very long time nor in a manner as pervasive and all-encompassing as this. Afterall, developed countries, which will be the focus of this post, have not experienced these rates since the Great Inflation era that ended at the onset of the 1980’s. Ever since then, high “inflation” had only been a malaise afflicting the poorer, developing countries. Before we continue, I have to remind the readers of the distinction between inflation and “inflation”. Basically, inflation is the expansion of the quantity of money and credit, which may cause an increase in prices in general, while “inflation” is the modern definition that means an increase of the general level of prices – check out the last link to see what is wrong with that definition and with actual inflation. Moreover, according to Positive Economics (i.e., Keynesians, Monetarists, etc) – though we can just dub them all Keynesians seeing that, as Milton Friedman declared, “we are all Keynesian now” – a moderate pace of “inflation” is good because it is an indication that inflation is occurring and, therefore, this must mean more credit financing more business activity, consumption and investment. This is true. However, the consequences of the boom and bust cycle that this renders are disastrous, as the Austrian business cycle theory teaches. Moving on to today’s agenda, to grasp this development, we ought to look at the demand and the supply sides separately. Beginning with demand, up until the end of the first half of 2021, the main factor on the demand side was government debt used to fund enormously profligate fiscal policies implemented in the advanced economies. Like the following chart demonstrates, governments all around the world started showering their citizens with love in the form of financial aid. The most notorious one being direct contributions to individuals accounts or home addresses, more commonly referred as stimmy checks. As the name indicates, these were employed to, besides assisting those who had lost their jobs and were having difficulty making ends meet, stimulate consumption. In the Keynesian universe, this is necessary to maintain the economy at full-employment, whatever that level is – this is complete nonsense as you should know by now.  Unsurprisingly, Advanced Economies (AE) were more free-handed than the Emerging ones (EE). Because of the nature of the eurodollar system that favours the most liquid assets and financial instruments, which means the more reliable and predictable asset classes, owing to being the more creditworthy, AE spent more simply because they can. At the same time, companies began looking for funding to pay their bills lest they downsize their payrolls. Obviously, governments provided a lot of that assistance. Nevertheless, due to the fickleness of political expediency, businesses leaned more to the financial sector. When the pandemic broke, suddenly companies tapped on their credit lines or begged for new ones, corporations issued a ton of bonds and banks and other credit providers – to avoid repetition, from now on, I will use these terms interchangeably - were more than willing to oblige. If you recall, this experiment was supposed to have ended after a fortnight. It certainly should not have lasted two years. For assuming this interruption of our normal lives and of economic activity would be extremely ephemeral, and seeing that there was a tsunami of credit flowing out of financial centres and rushing into our shores, everybody became complaisant. The case of the US is an excellent testament to this. If you pay close attention to the picture below, consumer credit jumped right at the onset of Covid, only to dwindle and then grow at a slower pace than the post-GFC average after that. Naturally, in view of consumers being awash in savings (i.e., stimmy checks), they had very little need do borrow to keep their indulgent lifestyles.  On the flip side, credit to businesses and mortgages (represented in the above graph as other credits to households and nonprofit organizations) shot up and continued to increase, though not at such a careless fashion. This has persisted until as recently as the first quarter of this year, for which we have the latest available data. As you will see, the short-sightedness of banks is the principal key, apart from governments (shown by the next chart), to explain our current situation regarding “inflation”, not the Fed. As I have already pointed out, companies accrued massive amounts of debt (also depicted in the following graph) to fund their operations. Be that as it may, they also had other objectives. Noticing that households were being inundated with money, industries started experiencing a tremendous surge in demand for their goods. The services sector only lately has felt this surge on their activity for obvious reasons.  Therefore, a scramble for materials and intermediate goods to produce the final goods to retail, on the one hand, and a severely disrupted global supply chain on the other, resulted in the costs of production to skyrocket. At a time when travel and trade became immensely hindered due to the restrictions imposed worldwide to allegedly fight the kung-flu, was when the western couch potatoes decided to binge on Amazon and ordering out with Uber Eats, Glovo or DoorDash. To make matters worse, owing to the ultra-low or even negative interest rate environment, or in other words, the prudent behaviour of bankers facing prospects of low opportunities in this – do I dare say – disinflationary landscape, forced them to seek only the safest and most liquid investments. Thus, real estate became even more attractive, causing a rise in demand and, consequently, home builders intensified their activity. This is demonstrated in the previous chart, with US Government’s agency securities (i.e., mortgage-backed securities). As you ought to remember, lumber prices soared like never before, in part helped by obstacles in the normal functioning of sawmills and transportation.

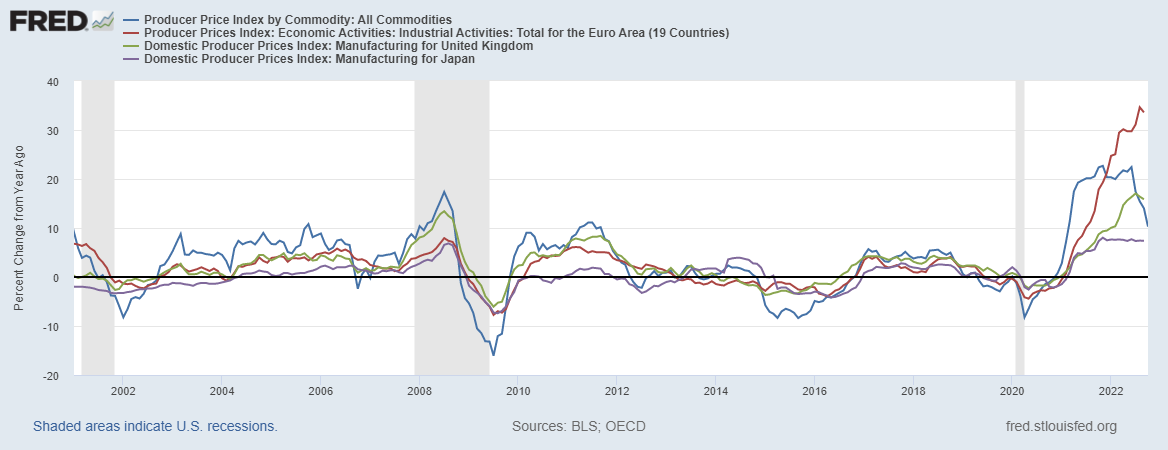

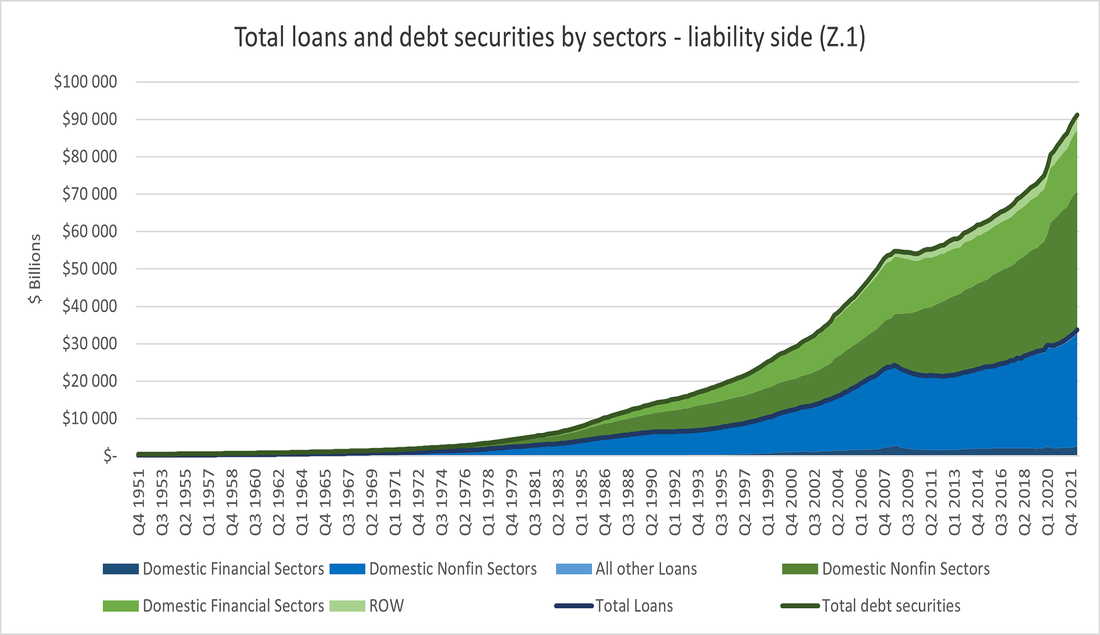

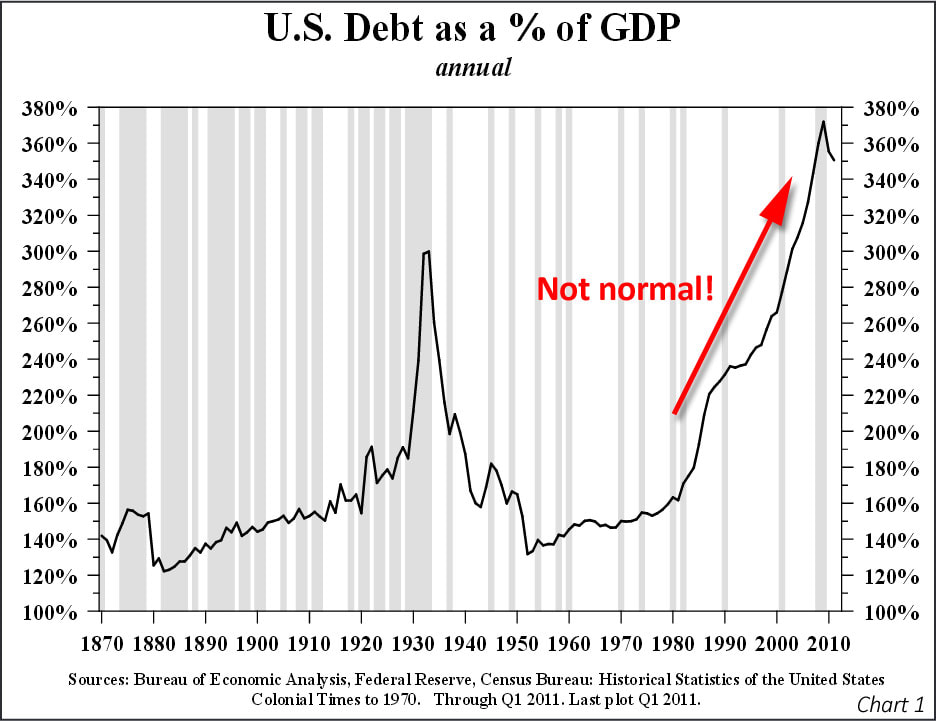

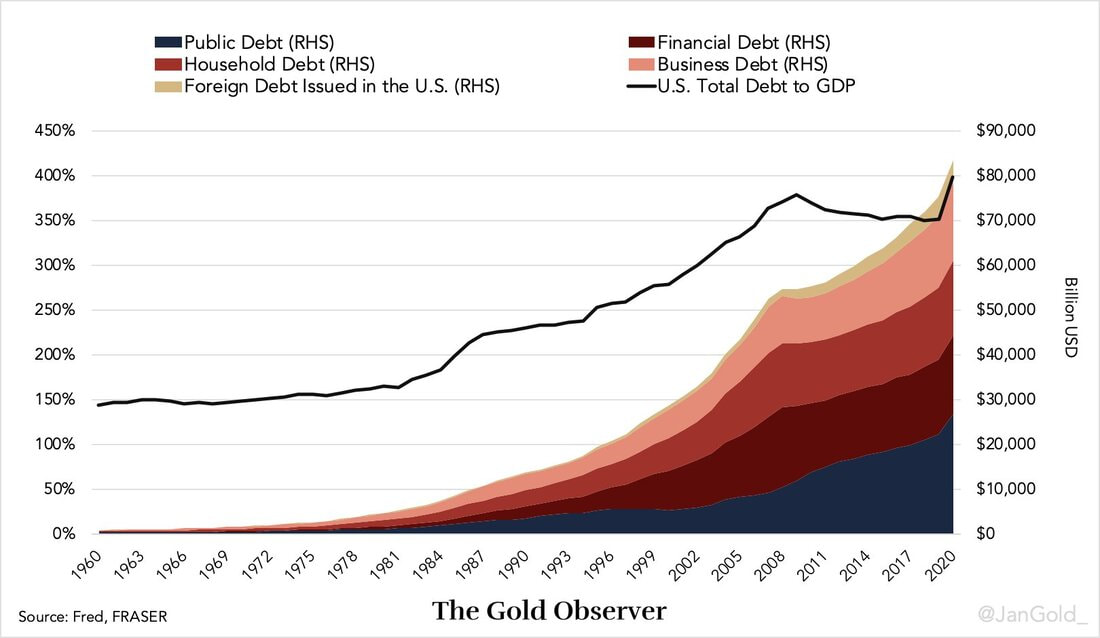

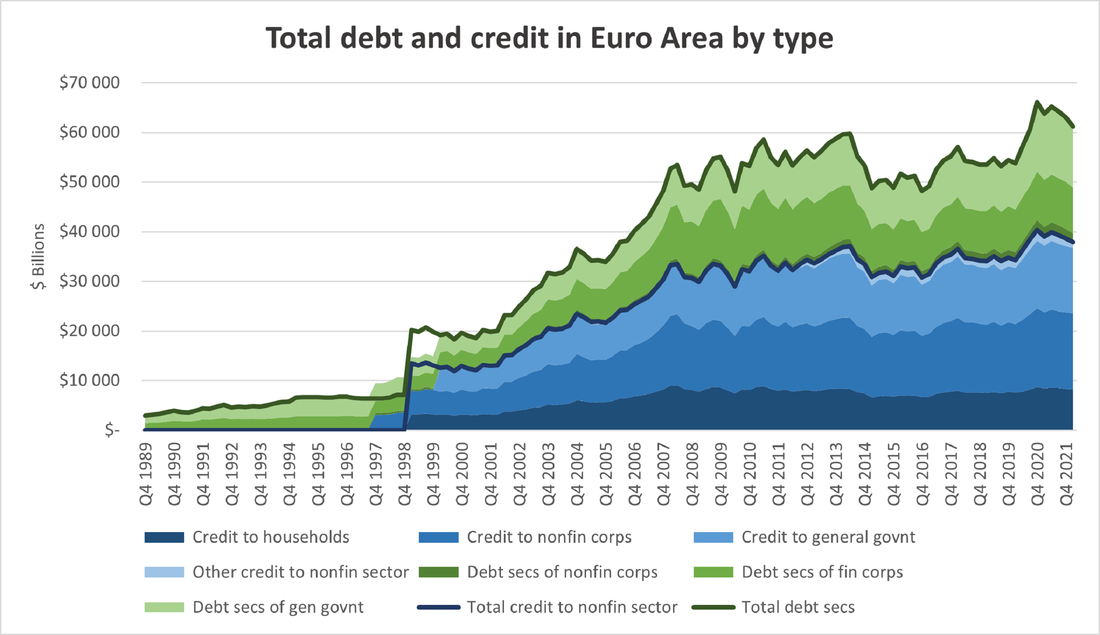

In spite of the colossal elevation of transportation costs, as shown right above, the fact is that the economy has been adjusting, despite all the criminal Covid policies, and correcting the escalation of freight costs. Furthermore, compared to previous “inflationary” periods, this one just seems like a minor inconvenience. Although, to be fair, factoring all production costs, on average (PPIs shown top graph below), we have not lived through such a paradigm since the 1990’s, at least. Even the oil-induced “inflation” of the noughties did not rival with today. Evidently, the surge in production costs had its effect on the PPI’s retail counterpart, the CPI (bottom chart). Still, the increase is limited by consumers’ purchasing power. Accordingly, since businesses have to stay competitive to keep and attract customers, they could not raise prices more intensely than their costs increase, resulting in consumer prices climbing at a slower pace than its producer analogue.   Indeed, consumption is a factor of production, more precisely of productivity, which means wages, and consumer credit. Picture a parallel reality where people focus on production and improving productivity to ameliorate their lot and raise their living standards, not only is this going to lead to reduced costs and falling prices (ceteris paribus, of course), but they will not have to be so irresponsible and keep on feeding this debt-based beast that goes by the name Eurodollar. In a nutshell, instead of actual inflation, meaning an increase in the quantity of money and credit, in turn devaluing the currency, prices have increased at a higher rate chiefly because of a mismatch between demand and supply. Albeit undeniable that debt went up, greasing the wheels of “inflation”, actually, the main culprits have been governments at first, followed by banks. On the first stage, from the beginning of the lockdowns in March 2020 till the second quarter of 2021, when the last and biggest round of stimmy checks were disbursed by the White House, governments had been the chief instigators. However, on the second stage, which I think has ended, banks took the baton and ran “inflation” to rates akin to the pre-GFC era. Noticeably, the conflict between Russia and Ukraine has taken its toll on the global economy, constraining international trade and reducing the supply of vital commodities, such as crude oil, gas and wheat, thus affecting the costs of transportation and production. Besides the bellicose nature of the conflict, the hostilities encompassing economic and financial sanctions have added insult to injury. Notwithstanding, the impact has been limited to some geographies and it has mostly dissipated.  By looking at the exhibit above, total debt flowing through the American economy, at least the one captured by the government statistics, has recently evolved in a similar manner as the periods known as Great Inflation (began in the mid-1960’s and lasted up to 1982) and Great Moderation (started after the climax of the Great Inflation, and ended at the onset of the GFC, on August 9, 2007). As I have indicated, government spending was the trigger, which is clearly displayed by the jolt in the graph above (under the label Domestic Nonfinancial Sectors). In addition, other countries have had an identical pattern as the US. Like I mentioned before, States extended their debts insofar as the markets gave them their blessings.

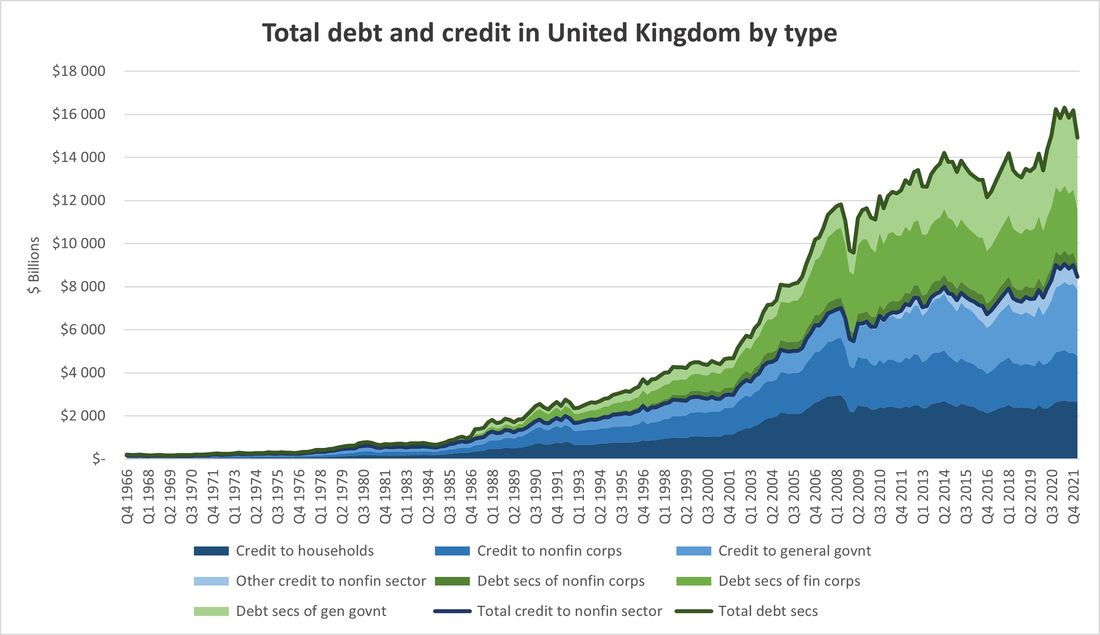

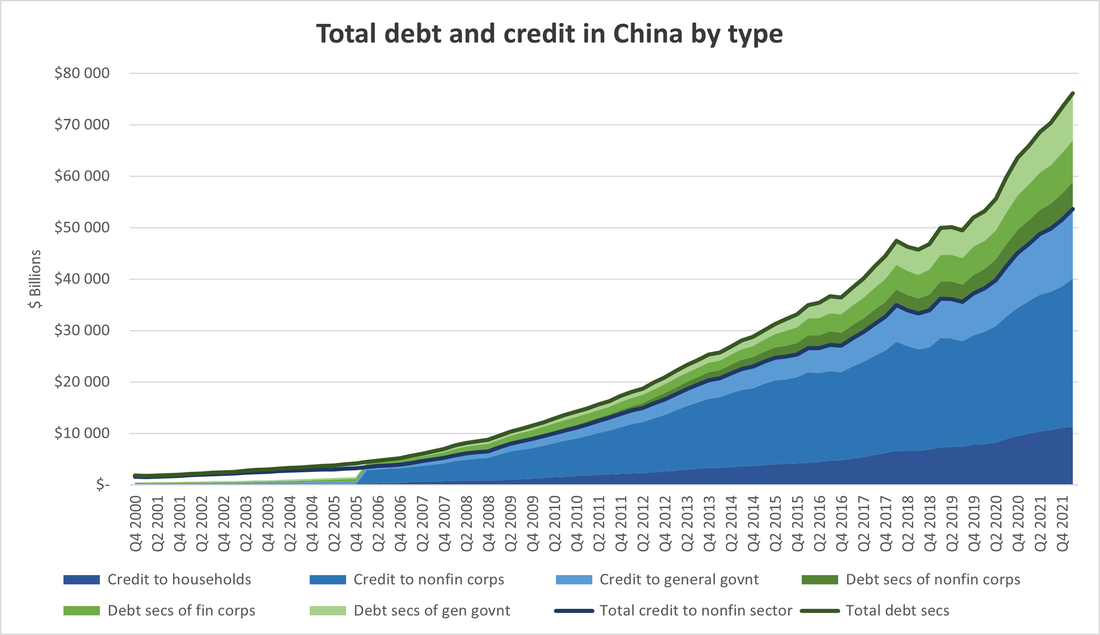

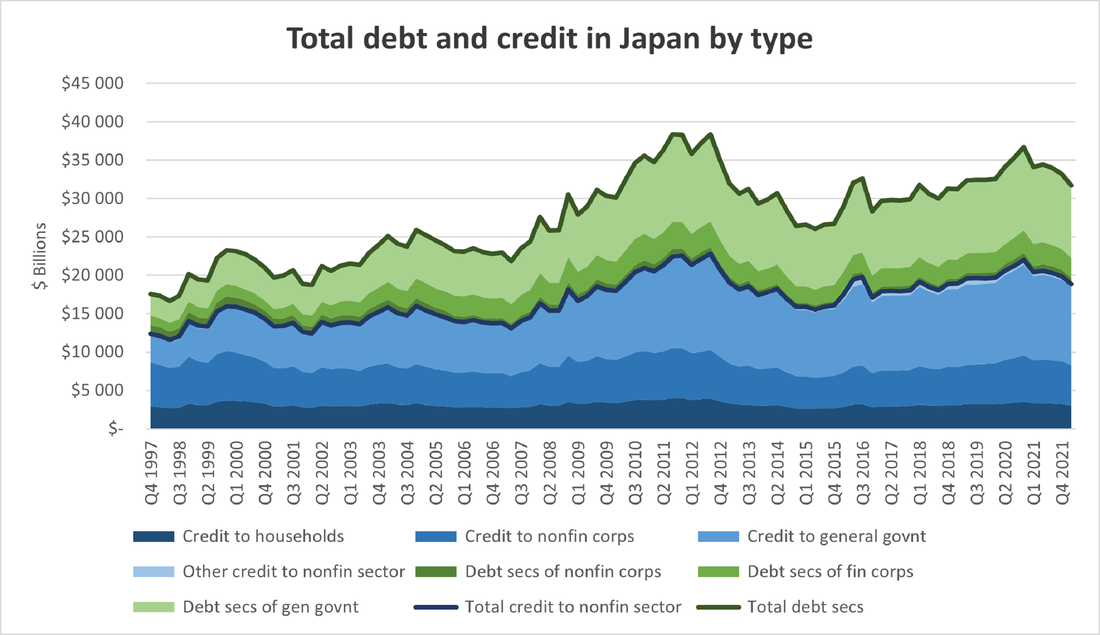

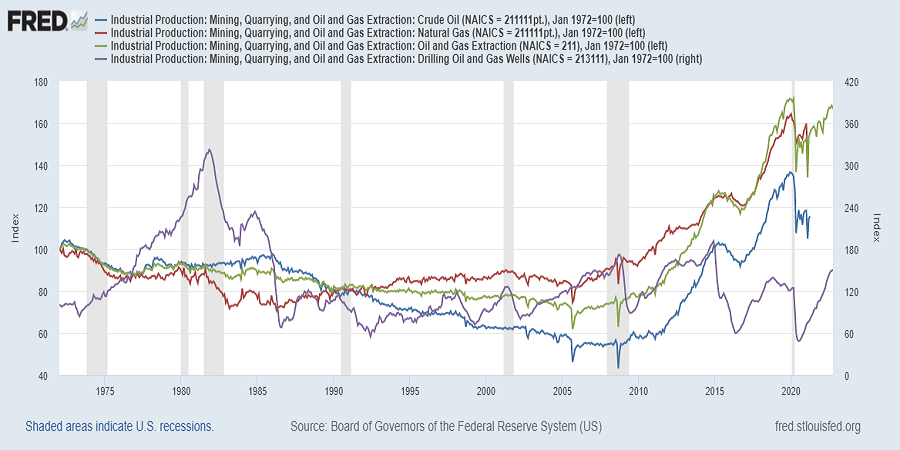

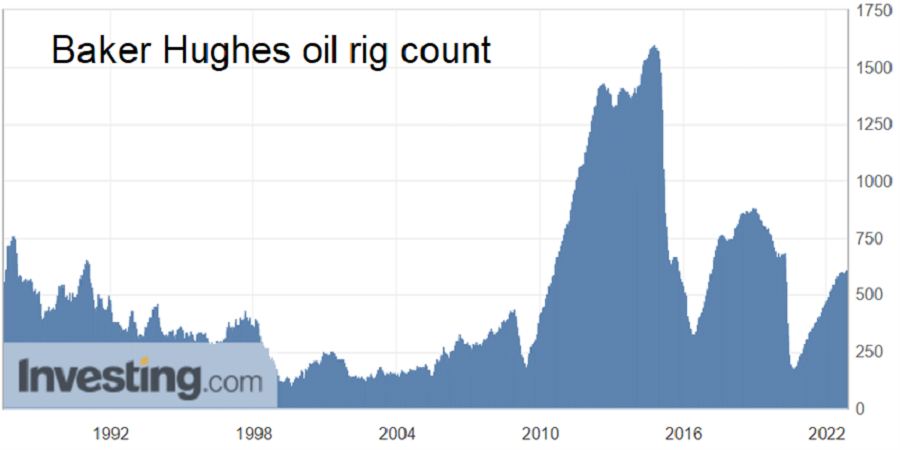

Interestingly, even though governments of the countries depicted above injected billions of euros, pounds and yens into their economies to kickstart growth and activity, banks did not get the memo and failed keep the momentum going. Besides their contractual obligations to provide open credit lines to their clients, banks have ostensibly been very heedful by trying to reduce their exposure. In fact, EA’s and Japan’s respective total debts both peaked in the fourth quarter of 2020, while the total debt of the UK climaxed in the second quarter of 2021, in spite of interest rates only starting to rise at the beginning of this year, as a reaction to increased expectations of rate hikes by the central bankers to control “inflation” – there is so much wrong with this reasoning that I am going to address it on another day. Of those four countries/regions represented in the previous four graphs, only China has maintained an incessant pace of credit creation. Although every aggregate of economic agent class has increased borrowing, government has been the most profligate too, much like the US. Curiously, despite all this credit expansion, prices have not soared as much as in the West. The explanation has to be that the demand-supply imbalance did not become acute. Moreover, oil and gas extraction or, more precisely, the lack of it has played a decisive role in the supply side of this demand-supply imbalance that has caused the “inflation” post-Covid. This topic deserves a post of its own, hence I will be succinct. Whether you like it or not, fossil fuels – let’s just call it that, though I do not believe they come from fossils – provide the necessary energy to power the economy, even to fabricate and run wind power generators, solar panels or electrical vehicles. On that account, when they become scarce their prices jack up, rendering energy bills more expensive. Evidently, this means that individuals have a smaller space in their budgets for discretionary spending. In addition, this hampers businesses’ ability to produce, possibly even turning some ventures unfeasible. For this reason, companies may have to either reduce production and staff, or push the costs onto their clients in the form of higher prices. Keep this in mind. All the same, there is something I must indicate about the following couple of charts. The one on the left shows that oil and gas extraction is almost at pre-Covid levels, which means they are close to all-time highs. However, the Baker Hughes oil rig count hints at a totally different story. According to this indicator, active oil rigs in the US equal in amount those in the late 1980’s, when the count kicked off, and are well below those in 2014, when the fracking activity reached its zenith. What I can surmise is that due to the “green” policies brought about by the anthropogenic climate change fraud, oil companies have been increasingly pressured to divest and encouraged to avoid further exploration. Regarding, the discrepancy between the two graphs, I take the view that it is a result of hedonic-quality adjustments, just like the CPI and GDP numbers go through. If the IP figures were accurately measured, I feel it would reflect the reality of much lower extraction and prospection activity. Inside the oil and gas industry, refining has been constrained as well. The worsening refining bottleneck, especially in the US, was explained by Mike Wirth, the CEO of oil giant Chevron, who on June 3 of this year told Bloomberg TV that there's not enough refining capacity to meet the demand for gasoline and diesel because no new refinery will ever be built in the US again. The CEO Wirth explains his reason: "You're looking at committing capital ten years out, that will need decades to offer a return for shareholders, in a policy environment where governments around the world are saying, 'We don't want these products to be used in the future.’”

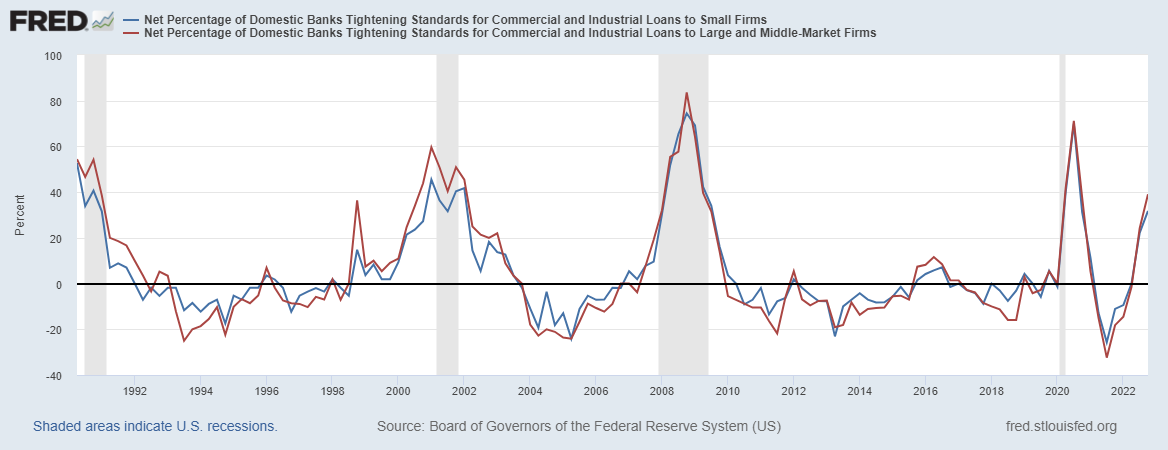

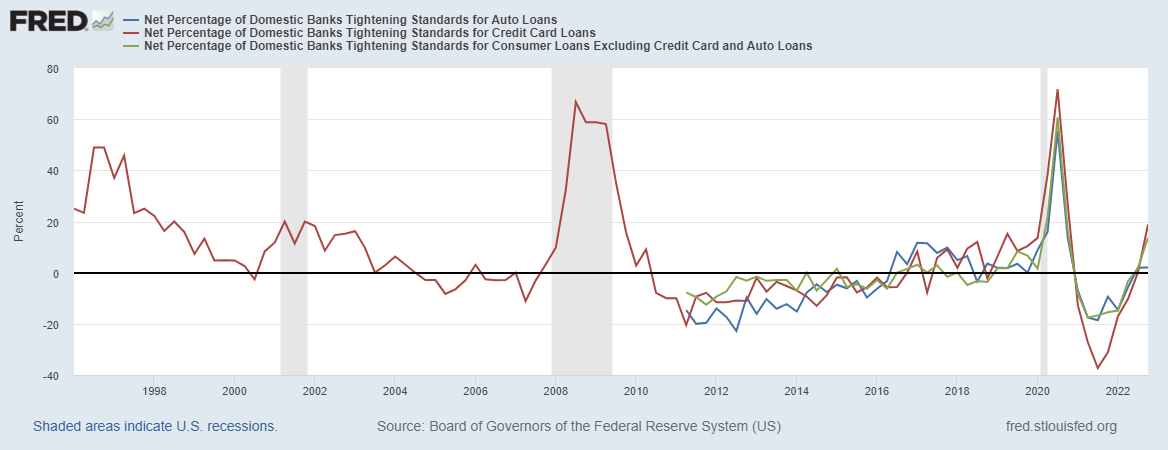

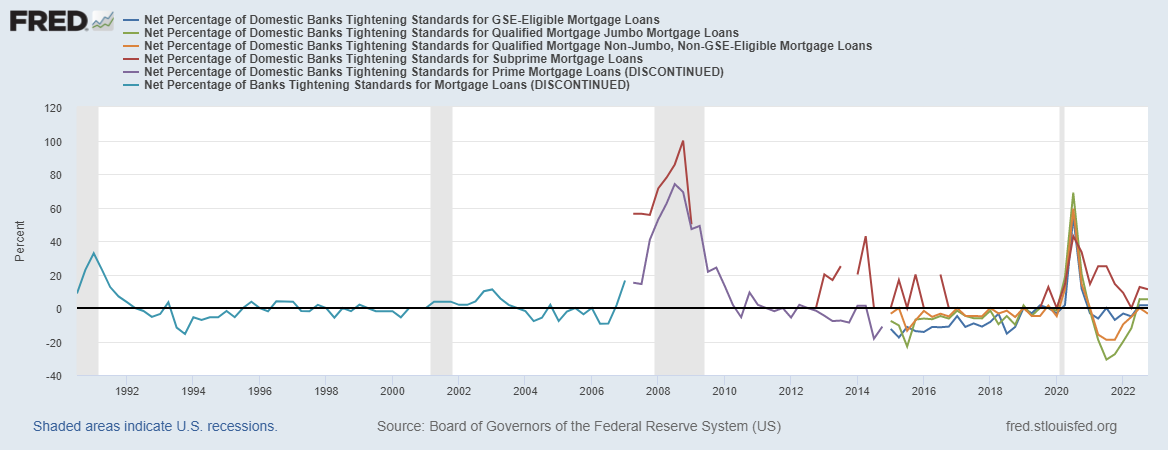

Finally, after analysing the trajectory of banking activity and debt issuance, we have recognised Europe and Japan have been in the doldrums for more than a year, while the US and China have been the two main engines keeping the world economy afloat. In any case, to be honest, I think that if the CPI and GDP figures were precisely measures, with no hedonic adjustments or tampering with the weights, it would show that the whole globe is in a recession or worse. For the AE, especially Japan and European countries, I presume they have not even come close to reaching 2019 levels – of course, this inevitably makes us question if we ever bounced back from the Great Recession. Apparently, since 2022 began, banks in the US have tightened their standards for giving out loans, whatever they may be. This is a plain attestation of the poor state of the economy, both businesses and households. Even the “primiest” prime mortgage loans are also being curtailed.    According to the Austrian business cycle theory, we are going through/towards a much needed and welcomed downturn to cure the malinvestments and distortions suffered in the last two years. Like a hangover that occurs after a night of recklessly gulping down alcohol, the body carries out its detox processes to get rid of the toxins and get your organism back to health. Evidently, if we keep making that same mistake over and over again, or hinder the organism from executing the corrections necessary, then we are always going to be sick. Therefore, if governments continue to intervene on the economy whether it is to halt it or to boost demand beyond the capacity of the productive structure, they are going to destroy it, as well as the fabric of society. To conclude, the escalation of prices is a symptom of a greater distress. During the pandemic, the structure of production suffered multiple blows, from the lack of workers that were better off staying unemployed to the heightened fuel and energy costs. Unmistakably, this relentless meddling by bureaucrats and technocrats is rendering the future much more unpredictable. To make matters worse, geopolitical tensions and protectionist policies becoming trendy add to the uncertainty and to more inefficient supply chains. In this scenario, productivity gains are inhibited, spoiling advancements in our living standards, impeding a faster decline in the “inflation” rate. Ergo, entrepreneurs turn more discouraged to invest in new or improving existing technologies, correcting processes or simply creating more stuff and hire more workers. Furthermore, individuals in general have less opportunities for work in a less dynamic labour market, which hampers their standard of living in a material way, although it also demoralises them. For that reason, keeping the US constitution as a reference, Life, Liberty and the Pursuit of Happiness is severely frustrated. Because of its nature, “inflation” is transitory. Indeed, prices can only stick with its ascension at ever increasing rates if demand outpaces supply at a continuously faster pace. Nevertheless, this imbalance will ultimately reach a breaking point, just as it happened in 1982, when the Great Inflation culminated in a double-dip recession in the US and several other crises throughout the world. Alternatively, a country may lose its ability to pay its obligations, having a unique solution: austerity. However, there are two roads that are extremely destructive and which lead to the same destination. Either it opts to devalue its currency or accruing even more debt. The former leads directly to very high inflation or even hyperinflation if the ruler is incredibly thoughtless and foolish. The latter results in markets losing confidence in that country’s creditworthiness leading creditors to increasingly refuse to accept this country’s currency, ultimately ending up at the same place as the former. As reasoned on the post titled Putting the E in EM, this could very well occur in emerging economies. Despite all the alarmism and prattle, the truth is that prices are not about to spiral out of control at any moment. Perhaps in EE countries they are but not in AE ones. Obviously, this could change in the future, though, for the time being, no chance. Those who claim the contrary, some have no clue what the eurodollar system is, others acknowledge their existence but have no idea how powerful and dominant it is, because they were not taught these in college, and the rest are merely imbeciles that are aware banks originate most of the debt but still affirm the central bank wizards make magic by pulling their levers.

0 Comments

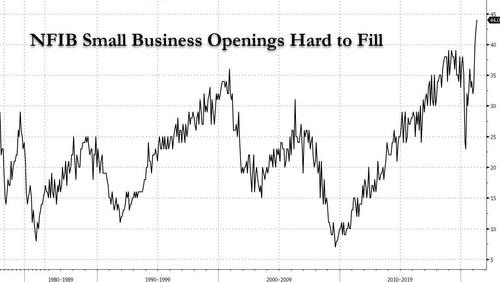

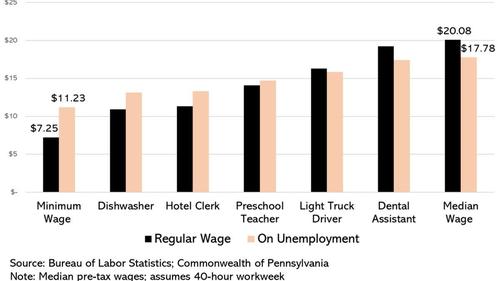

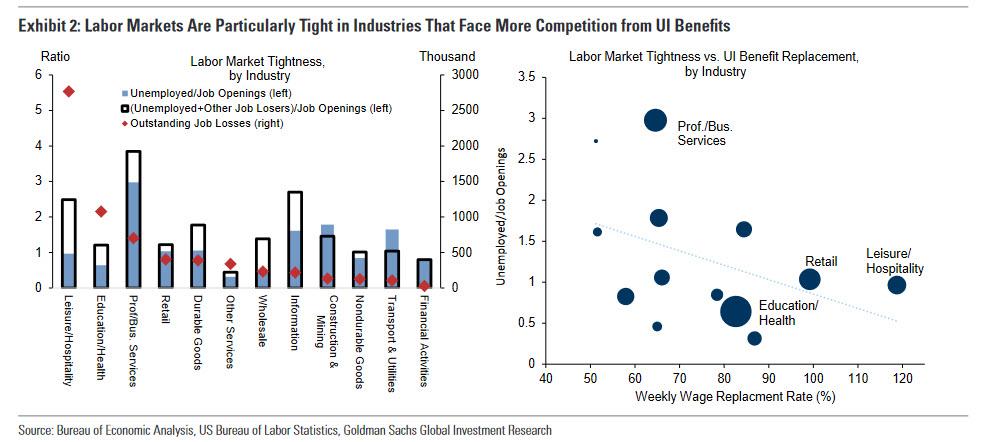

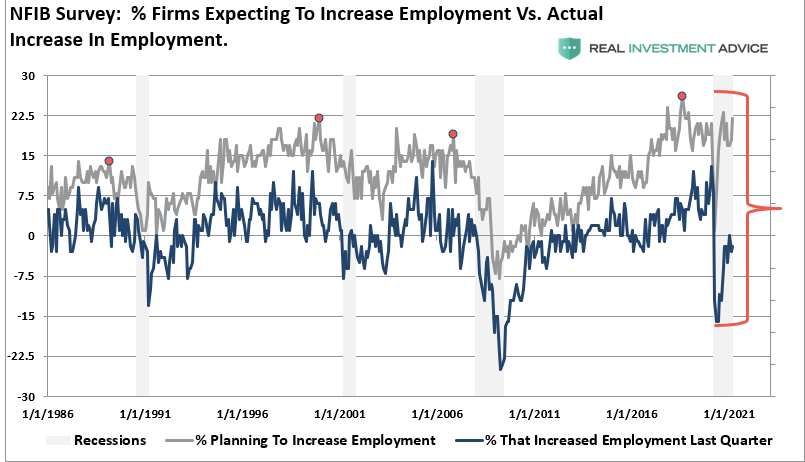

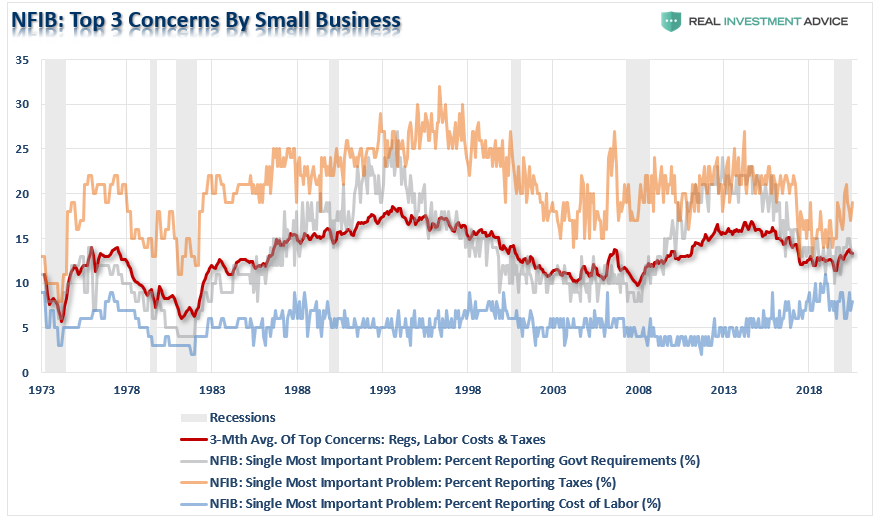

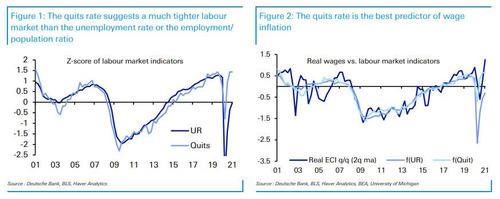

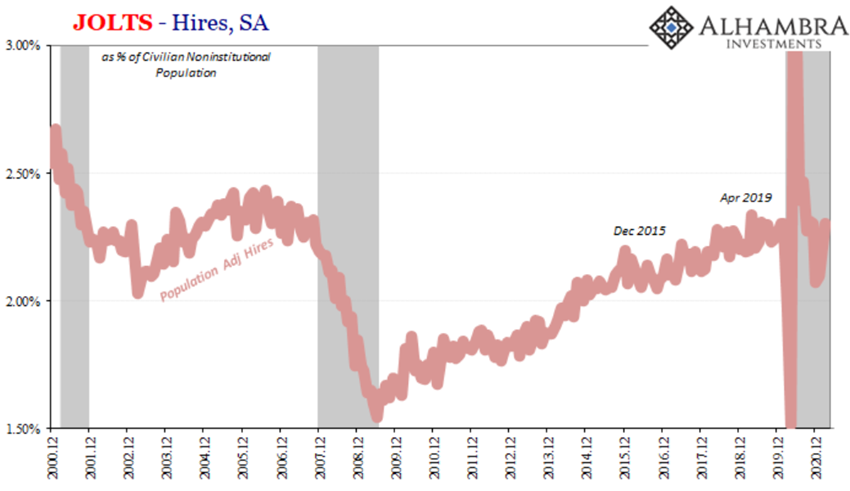

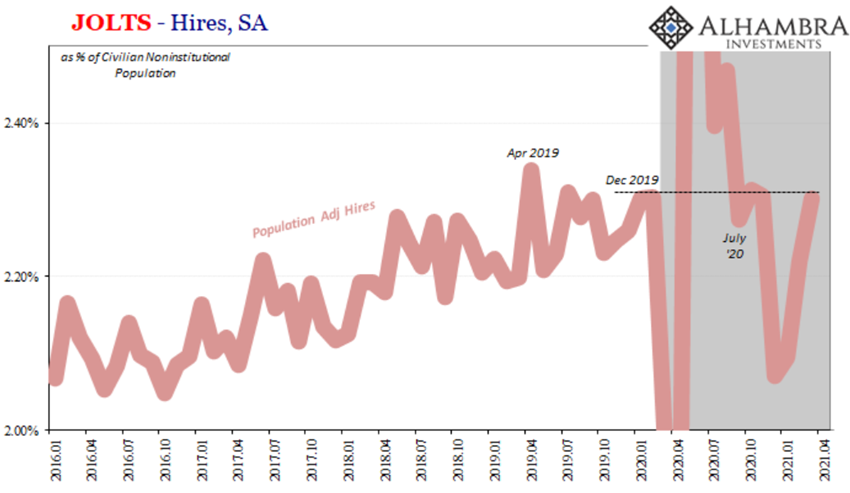

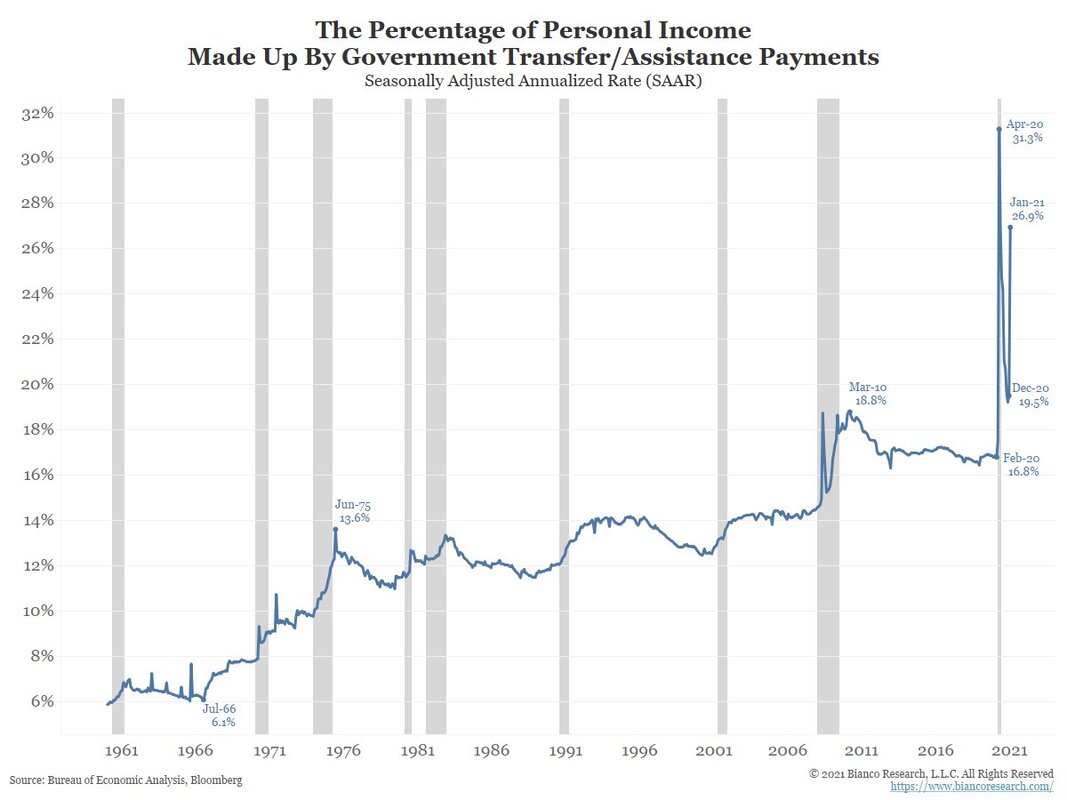

Resuming our recurring subject about the economic recovery (or, more appropriately, the lack of one; such as this or that), the latest NFIB report should not have surprised anyone who has been looking at the data objectively and ignored the mainstream economists and analysts. According to the National Federation of Independent Business, in April, an unprecedented 44% of small businesses struggled to expand their payrolls. which is clearly a great sign, right? That is what the government and the spin doctors want you to believe.  For the bulls, this conspicuous recovery (for some a supercycle) is grounded on those multiple "stimmy checks" handed out by Trump and Biden, as well as governments all around the world, and the unparalleled scale of monetary "accommodation" released by central banks. On paper and if you do not think much about it, it seems like a good plan. However, the consequences are disastrous. Despite this attack (on economic soundness) being two-pronged, impacting demand and supply in distinct ways, the end result is equally bad. As you can easily discern, consumption of goods (not services since the plandemic annihilated them) skyrocketed as a result of these handouts. Unsurprisingly, because businesses were seeing their inventories dwindling, manufacturers began to receive more orders, leading them to increase production. To do this, they have had to expand their staff. Thus, a widespread scramble for workers, initially gave the appearance of a rapid, V-like recovery, coming out of the hole in record-breaking time. However, those hopes turned out to have been completely wrong. In spite of the continual implementation of useless lockdowns and other moronic measures, to "flatten the curve" or something of this sort, definitely leaving a dent on the economy and its prospects for recovery, there has been an extremely detrimental factor for the experienced lethargy. If you have not surmise it by now, the next chart will show you the answer. Quite simply, companies have found enormous difficulty in getting workers due to the government making joblessness so damn desirable. Wouldn't you put off looking for a job if you were making more money laying on the couch, in front of the tv and sleeping all day than you were at your previous crappy job. Considering all that plus the stress and cost associated with the daily commute, even those earning a median wage may have been better off unemployed.  On a positive note, though, there is still a smidge of common sense in the Republican party. In the last month, realising the harm these federal policies are doing to their economies, most Republican-led states have ended, or passed laws to soon terminate these unemployment benefit schemes. As Iowa Governor, Kim Reynolds, affirmed: "Federal pandemic-related unemployment benefit programs initially provided displaced Iowans with crucial assistance when the pandemic began. But now that our businesses and schools have reopened, these payments are discouraging people from returning to work." Backing this assertion, Goldman Sachs has made the same findings. On the left, what one takes from it is that the sectors which had the largest job losses tend to have fewer people applying for a job in those very same sectors. On this account, Goldman's economists, just like every mainstream one, assume that this is an indication of severe tightness in the labour market, especially in the lower-wage industries as the graph on the right demonstrates.  Be that as it may, is the labour market really suffocatingly tight? Although there are those that point at overwhelming tightness, there are other indicators that indicate otherwise. Regarding the following couple of charts, these two, which come from the same survey, nevertheless send mixed signals. The top one, depicts a great struggle to arrange suitable workers. While the other one shows that labour costs have not become more concerning since this covid hoax started. In spite of arousing demand, the "stimmies" effect is short-lived. They merely pull demand forward. After the stimuli do their thing, the demand reverts back to its potential, i.e. whichever level/trend the productive structure is able to generate, which we are yet to discover what it is in this "New Normal" paradigm - maybe Klaus Schwab and Bill Gates already know. In view of the fact that wages are the biggest cost for any business, in order to increment hiring activity, companies have to feel rather confident about the economic prospects. Notwithstanding, the economic potential is tremendously constrained due to the increasing regulatory and taxing strangleholds across the globe, creating all kinds of frictions and raising costs in production, consumption, investment and trade in the whole world economy.   All the same, the Keynesians believe this is all conducive to an inflationary environment. Why? They just rely on spurious correlations between labour data and the CPI or the PCE deflator. For instance, the next couple of charts show that real wages have decoupled from the unemployment rate (UR). Hence, so as to continue rationalising the economy is on the path to recovery, the economists at Deutsche Bank simply ditch the UR and employ (pun unintended) the Quits figure from the BLS' JOLTS survey.  Alternatively, what I think is more likely to explain this high Quits rate is the misleading analysis from these economists and then reporting by the media, which entices disgruntled workers, particularly of those industries bashed by the insanely destructive covid mandates like Leisure & Hospitality, to pursue a higher-paying or more fulfilling career. Obviously, there is nothing inherently wrong about ambitioning a better lifestyle. Yet, they are being deceived about the true state of the economy and its outlook. Sadly, they are going to find out the hard way. Furthermore, another interesting data point from the JOLTS survey is the Hires one. Naturally, if we were in a truly inflationary boom, the amount of hires would have looked more like the reopening months of May and June of last year. Taking into account the freezing cold in Texas and other places in February that froze the labour market too, the March number for Hires should have been much higher. Certainly not on the same level as December 2019, which was a time, mind you, already on the brink of recession with several indicators hinting at that.

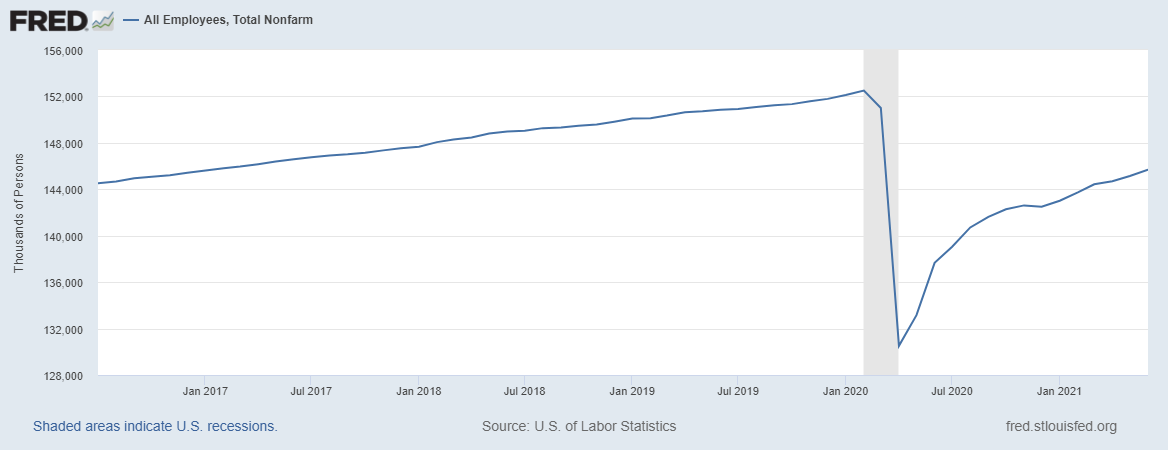

Moreover, to corroborate my point, the total nonfarm payroll is still horribly far from reaching the pre-covid level, not to mention that it is light-years away from what is should have been at had the plandemic never happened and the economy kept on growing at trend. To add insult to injury, the rate of change of labour growth (second derivative) is apparently falling. If it continues like this, which I think it will, then the recovery is not going to occur, similarly to the aftermath of the Global Financial Crisis (the Silent Depression, as Emil Kalinowski dubbed it).  To conclude, seeing that the multiple rounds and various types of subsidies fomented a false sense of economic resilience and vivacity, during a period where the deck is actually stacked against a booming expansion or renaissance - remember there were people truly believing we were entering a new edition of the Roaring 20's; is actually sad how Keynesians fool themselves -, soon the economy is going to fold in epic proportions.

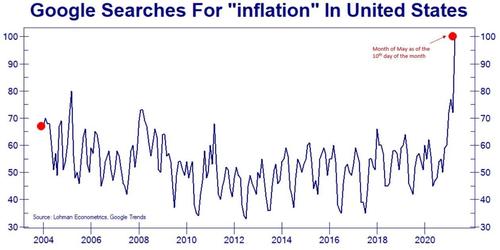

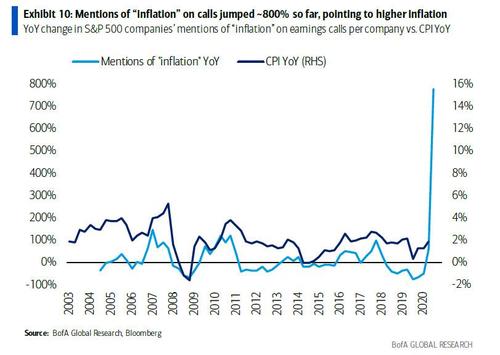

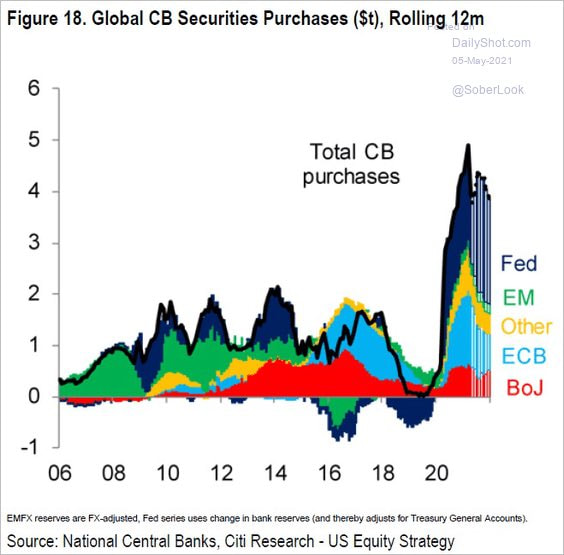

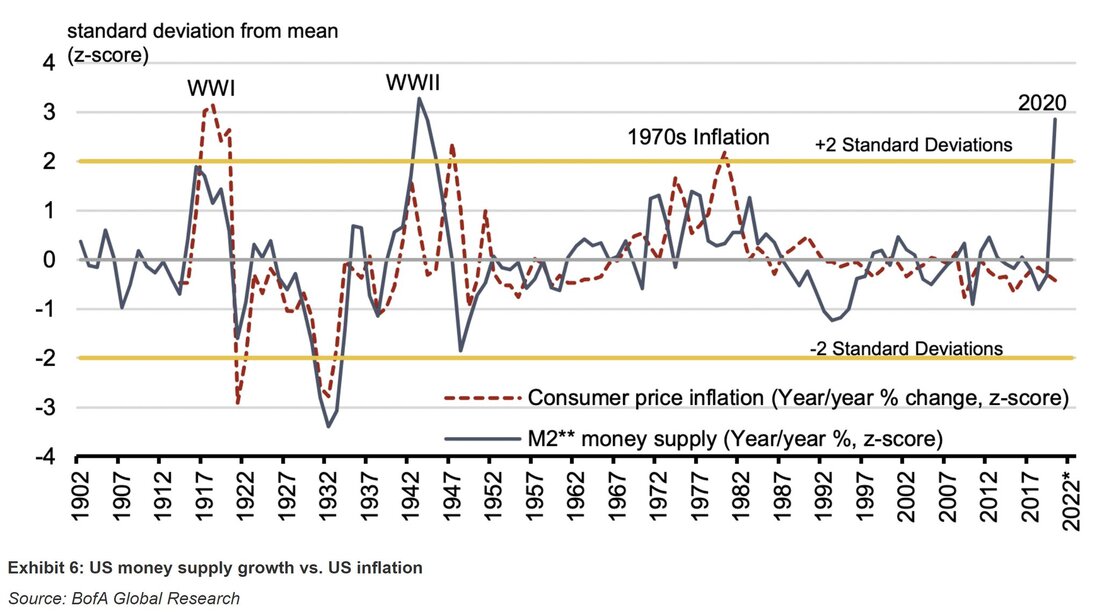

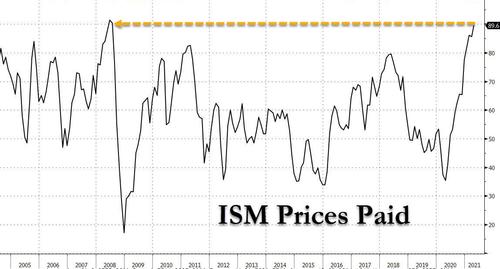

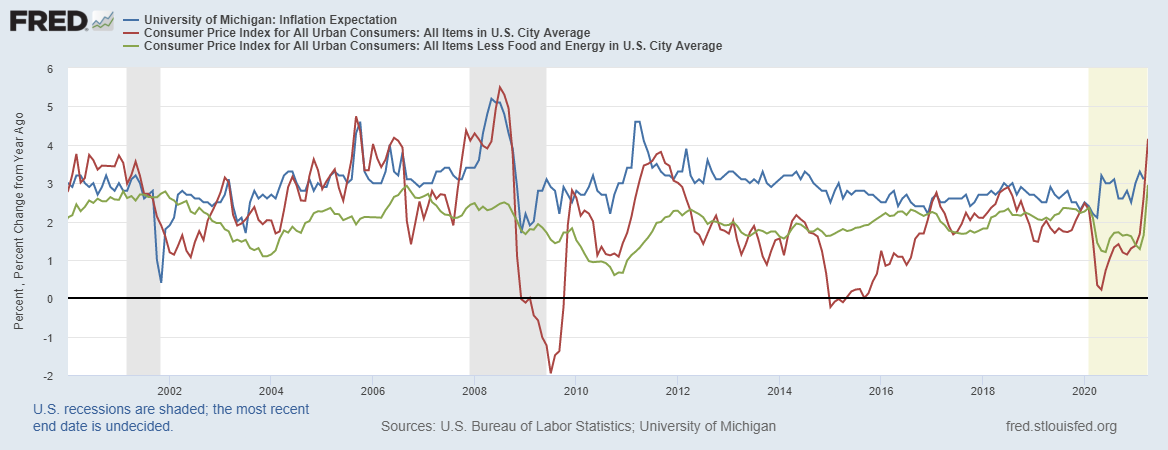

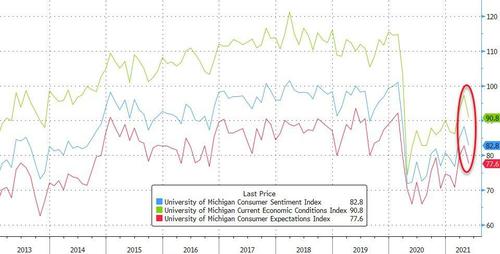

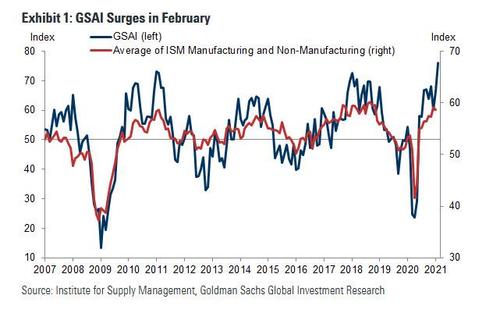

To make matters worse, if the never-ending public health tyranny refuses to cease its devastation, the cost of commodities, labour and transportation is going to continue to rise, taking its toll on the (global) economy, smashing our living standards. Perversely, this will probably lead to more "red-hot economy" and "tight labour market" indicators that will leave the experts scratching their stupid, empty heads. Hopefully, by then, both workers and prospective ones will have wised up to it. Without a shadow of a doubt, the theme that has pervaded the financial markets this year so far has been inflation, as in, a repeat of the 1970’s is upon us. Like I have been continually reporting, such a scenario, in the foreseeable future, is pure fantasy, having no basis on reality. Notwithstanding, the pundits on tv, the journalists and the “experts” in Wall Street and academia have been very successful in transmitting this narrative to the public. Owing to being bombarded by a barrage of stories and anecdotal evidence of rising prices, the commoners have suddenly grown watchful of the emerging inflation. This much is represented in the top graph that shows the Google searches for the word "inflation". Accordingly, the interest has been soaring like never before. Naturally, due to the data going only all the way back to 2004, you have to take this with a pinch of salt.   However, it has not just been the usual suspects in the media that have pushed this narrative. As the above chart demonstrates, companies have been more vigilant inflation-wise. In comparison to last year’s Q1, the mentions of "inflation" on the earnings calls of S&P 500 companies have jacked up almost 800%. Could this mean that the CPI annual rate could reach double-digit territory, as the graph implies? Obviously not; this statistic is not indicative of anything. In fact, the CPI figures for April have already been released and the YoY rate is a mere 4.2%. Unsurprisingly, after having suffered in Q1 2020 the biggest deflationary shock since the Great Depression, it would be reasonable to assume there would not be a lot of mentions about inflation. Therefore, following that massive Covid crash, which followed a terrible year of disinflation in 2019, where the term "inflation" practically disappeared from the lexicon – as depicted by the chart that shows an almost 100% drop in mentions -, any slight increase in absolute terms would entail an enormous jump in relative ones. Looking at the next couple of charts, how can anyone believe the Pandora's box of inflation has not been opened. The writing is on the wall. Because of colossal large-scale asset purchases by, especially, the major central banks (top graph) since March 2020, the inflationary inferno is bound to be kindled.   If you still have any doubts, just heed the warnings the graph above is sending. On the whole of last year, the monetary aggregate M2, which everyone thinks it represents all (or close to that) the monetary forms, denominated in dollars, in existence, mushroomed at a pace not seen since World War II. Notice what happened to the annual rate of change of consumer prices (red line) in that period; it went up... fleetingly (oh boy!). LIkewise, during WWI and the Great Inflation of the 1970's, consumer prices followed the surge in the M2 aggregate. On that account, why would this time be any different? Surely, prices are going to have to soar at least as much as the decade of the 70's. As the following chart shows, prices paid by the producers, according to the ISM Manufacturing survey, have been climbing at a rate not seen since the middle of 2008 - not a good signal. Hence, it is only a matter of time till the rising costs of production are passed on to the consumers, reverting once and for all the deflationary/disinflationary environment that has hitherto haunted the global economy.  As you know, if this is not your first time here, I am just being provocative. The truth is inflation is controlled by the participants in the eurodollar system, not the central banking technocrats. Thus, proper inflation - meaning rapid growth of the money supply - will only occur insofar as banks and other credit originators perceive the conditions in the economy and the financial system are adequate for expanding credit, like they did prior to the GFC1. Before you start berating me about the quality of the governments' price statistics, which are immensely tampered and not to be trusted, I agree with you. In fact, that was the topic of my first post. In it, using the ShadowStats guidance, I uncovered the shenanigans that the bureaucrats at the Bureau of Labor Statistics (BLS) were doing to hide the true depletion of the dollar's purchasing power. In short, in the mid-1980's, the BLS began doing hedonic quality adjustments. Then, for that not being enough to keep the "inflation rate" under reasonable figures, in the 1990's, the methodology was pushed further into a substitution-based calculation, in which substitution of lower-priced and lower-quality goods in the basket is made with the intent of lowering the reported rate of inflation versus the fixed-basket measure. Be that as it may, in view of the CPI not having suffered any more changes in its methodology since the last decade of the twentieth century, we can safely compare the CPI figures of today and the naughties' ones, prior to the GFC1. Curiously, in spite of all the "money printing" by the central bankers, the CPI rates have actually been lower since then, with the most recent figures breaking the shackles (somewhat) - due to supply squeezes, mainly, and base effects too (top graph). Interestingly, before the GFC, consumers were very accurate in their expectations of inflation, as per the University of Michigan. Despite that, since then, consumers have been terrible at forecasting the BLS' rate of inflation, consistently overestimating the loss in the purchasing power; not just for the next year, but for average of the next five, albeit they have been closer in forecasting the latter one (bottom left chart). Nevertheless, the consumers' perception of economic conditions, both present and future, have been rather dreadful, as the bottom right chart portrays. So, to recap, inflation expectations are climbing, while consumers are sensing a lousy economic landscape. Certainly, "stagflationists" ears must be burning.

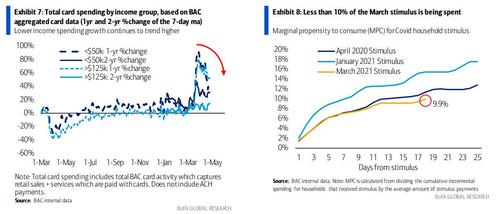

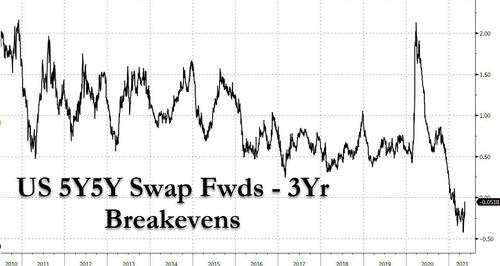

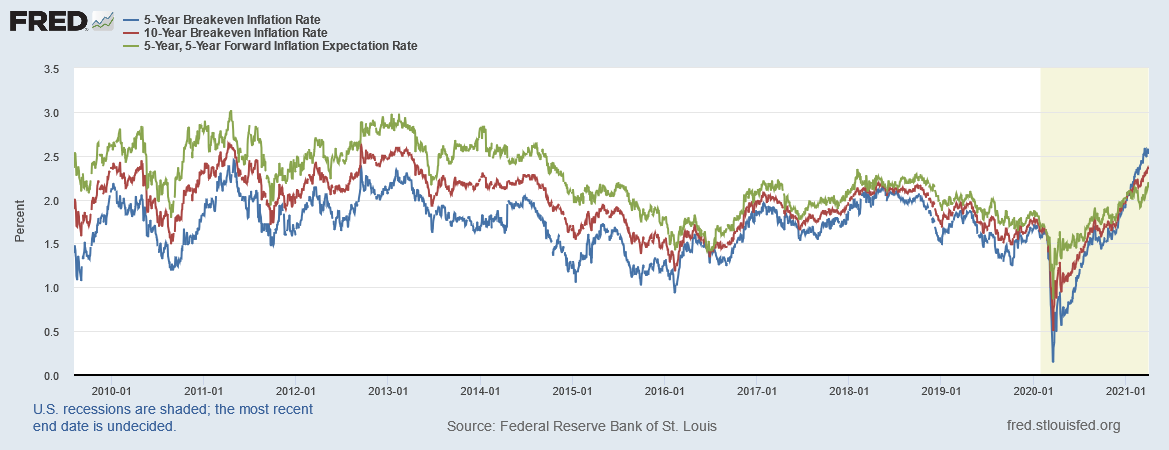

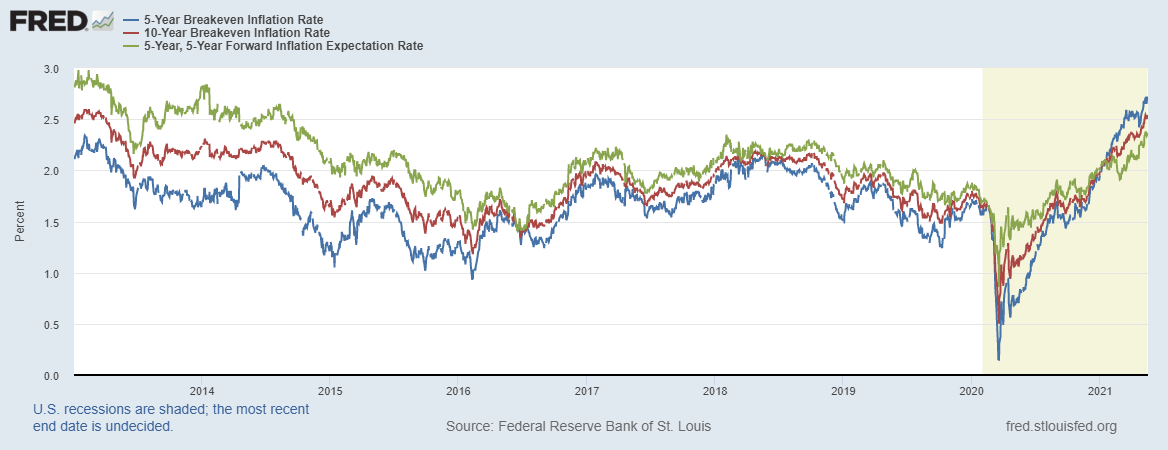

In addition, the annual rate of the CPI soared in April, besides the supply squeeze and base effects, because the US federal government decided to pamper its electorate, sending out three rounds of stimmy checks. Undeniably, the surge in consumer demand that these handouts generated, at a time when production and transportation were being restrained or even outright halted, led to higher prices. Yet, this inflation has remaind largely contained in the realm of producers for not being able to pass the costs on to the consumers. Unfortunately for the Keynesians who have promoted these policies, they are no longer having the desired effect of triggering a consumption-led recovery. As the graph on the righ demonstrates, consumers are preferring to save a bigger chunk of this latest stimmy check in comparison with the other two.  Revisiting the TIPS market and the breakeven rates like we did last week, the message coming from them remains the same. Although prices are rising, they are simply a transitory phenomenon provoked by government-imposed restrictions. Emphatically, the spread between the 5-year forward rate and the 3-year (not forward) breakeven rate (bottom chart) has been considerably negative since the beginning of the year. Despite the spread has gradually been approaching positive territory, on account of the 5-year forward has been climbing a bit, implying higher future expectations of inflation, they are still very subdued relatively to historical standards. The fact that the real yields are close to or at all-time lows tells everything you need to know about the sentiment of those in the financial system.

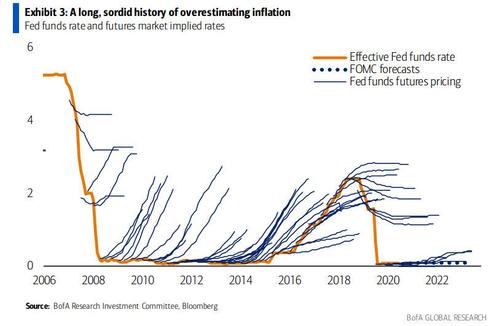

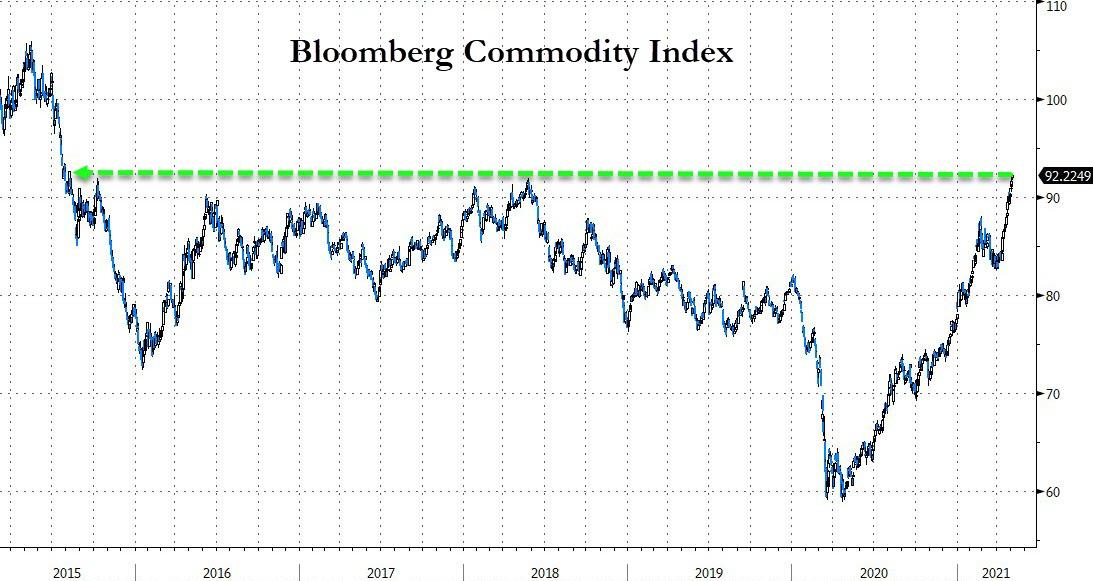

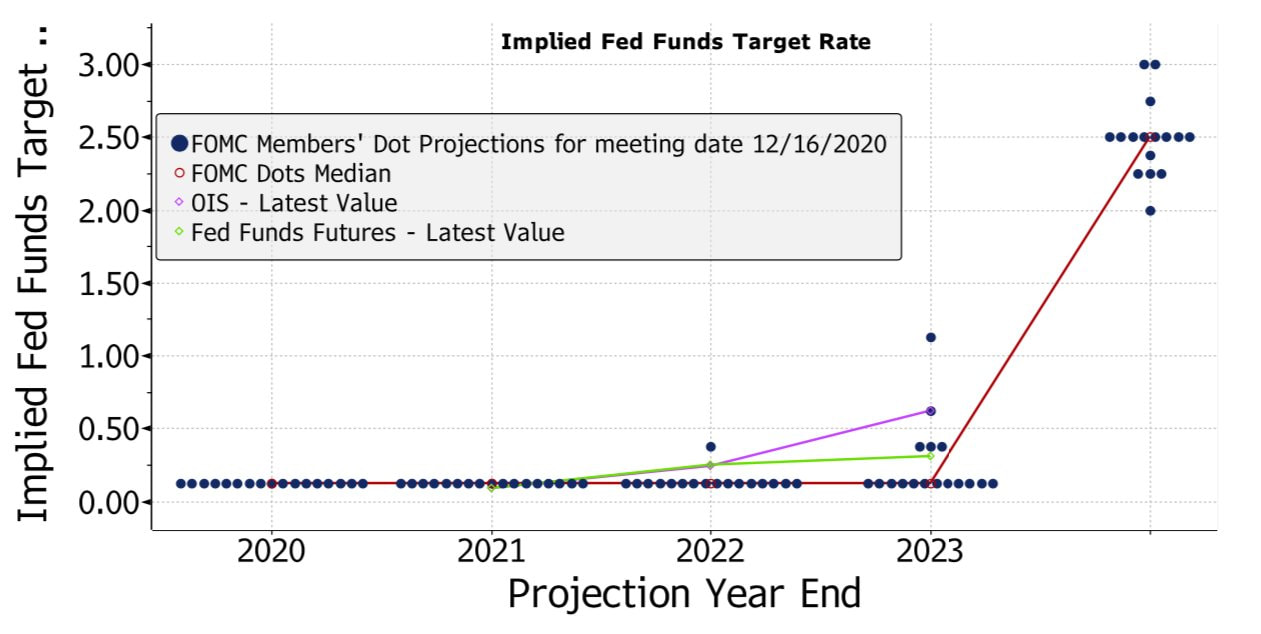

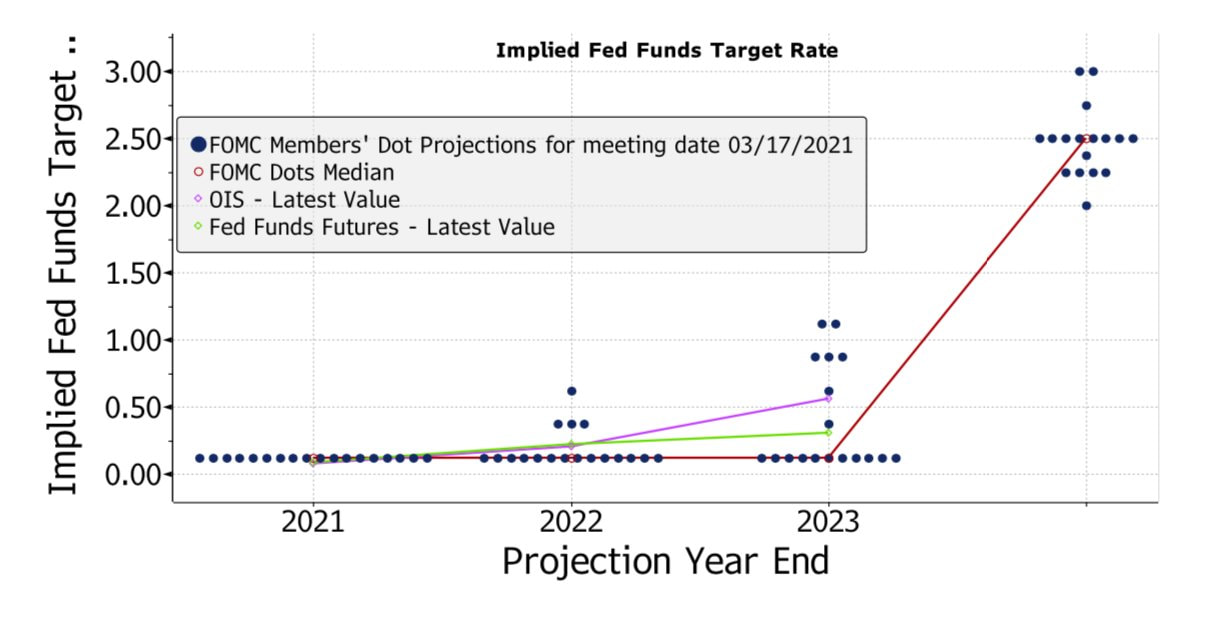

To cap it all off, even though the financial media and FinTwit have been ridden with chatter about the upcoming QE tapper by the Fed, we shall resist the pressures of the echo chamber, remain intelectually honest and guide ourselves only on what is fundamental, tuning out all the noise. In spite of being a market-based indication, Fed funds futures are part of the noise, as the graph below shows. Even if they are right, they are merely suggesting that by the end of 2023 the Fed funds rate will be half a percent. That is still awful, being just a little bit better than the absolute worst experienced last year.  In conclusion, do not get swindled and carried away by the putative experts and the overload of articles and commentary on the brewing inflation. These people do not understand how the monetary and financial system works, owing to believing the central banks are exactly that, playing a pivotal role in the expansion of money and, more importantly, in the direction of the economy. In a nutshell, the system evolved, but the experts did not; the eurodollar regime completely changed the way credit is formed and provided, throwing all prior conceptions of financial intermediation to oblivion, and still these fools, both the "stagflationists" and the mainstream economists and central bankers, are absolutely unaware of the implications of such monetary revolution. Regardless of such stubborness, the eurodollar system remains in place, albeit languishing and awaiting for its replacement. In view of not having any new setup ready and standing by, though there may be some in the making (e.g. DeFi and CBDC), we are going to have to wait awhile for what will hopefully be an upgrade - better pull up a chair. In the meantime, try to knock some sense into their heads, despite how hard that may be and how closed-minded they are.  In the midst of all the kerfuffle around the recovery (or lack of it) coming from the financial media, Wall Street analysts and FinTwit luminaries, despite disagreeing profoundly on the soundness of the recovery, if there is actually one, these enlightened clairvoyants assert in unison that high inflation, or even hyperinflation, is on the cards. Whether it is of the Great Moderation kind or of the Great Inflation sort, the global economy, having been infested by deflationary/disinflationary disease since the GFC1 (2007-08), is going to see inflation make a comeback. As a matter of fact, we do not have to wait any longer. For the last six months, though mainly since this year broke out, prices for all sorts of goods have skyrocketed. No other market/sector has personified this belief more clearly than commodities . From lumber to corn and from copper to steel, all eyes are on commodities. Yet, there seems to be some markets, very important ones, that are oblivious to these developments. In view of not being necessary to inspect each and everyone of the markets of the commodities' domain, it suffices to analyse it in broad terms. Having soared more than 50% since the 2020 GFC2's trough, the Bloomberg Commodity Index (BCI; below graph) seems unstoppable in its ascent to the moon. Obviously, reaching a more-than-five year high, surpassing the apex of the eurodollar reflation #3 (as Jeff Snider calls it) in 2018, it clearly indicates the (global) economy is booming.  Notwithstanding, is it that obvious though? You know where I am going with this. On March 1, I presented my refutation of the "commodities supercycle" that several analysts have been clamoring about. Therefore, I am not going to dwell on it here. Succinctly, the rise in commodities' prices were triggered by disturbances in production and in supply chains, which were caused by the corona-phobia-fuelled restrictions and shutdowns, as well as the various drops of "helicopter money", predominantly in the US, that allowed consumers to splurge far more than they would otherwise. Owing to most of the service sector being shutdown, consumers directed their "stimmy" checks towards goods, exarcebating the constraints in production and supply chains. By zooming out on the BCI (below chart), you can see that commodities have just escaped its historic bottom, even though this index still remains at a historically depressed level. This is surprising, of course, considering all the assertive prattle that comes out of your tv and phone screens. Perhaps, they only show and examine the graphs of commodities' prices that will tilt yours and the public's perceptions to their camp (the inflationists), ignoring those pesky ones that refuse to comply with the inflation and the supercycle narratives.  In spite of being true that most commodities are reaching multi-year highs or even all-time highs, with lumber being the epitome of this climb, the overall picture looks as dire as it were before the kung-flu came to light. Albeit, commodities are currently hinting at better conditions, both present and future, than they were last year. Still, this does not excuse opening the champagne. To be fair, most commentators on the inflation camp do not view this as a good circumstance. In lieu of interpreting the increase in the prices of commodities, and of goods in general, as a sign of a burgeoning economy, quickly recovering from the government-imposed depression, they have the discernement to recognise, through other data points, the economy is still in bad shape and, consequently, they do not foresee the economic malaise to pass anytime soon. In other words, they are expecting a period of stagflation, like the Great Inflation of the 1960's and 70's. On the one hand, you have economists and central bankers that maintain the greater pace of price surges are temporary, being ultimately curbed by the still weak labour market and high uncertainty. Nevertheless, they contend that as soon as the economy reopens completely and everyone gets their vaccine jabs, due to the fiscal and monetary "stimuli", the economic activity will fully recover and possibly even "roar" like the 1920's. On the other hand, the "stagflationists" have the perspicacity to know that growth and progress do not arise from government decree and central planning, but from entrepreneurs in a free-market system. Despite that, they are in error when they assume central banks are able to "print" money - in the current framework that is not possible (eurodollar system) - and that the markets are going to, sometime in the future, reject the low-yielding government bonds (and notes and bills), punishing their profligacy and recklessness. Hence, in this scenario, central banks have to perform their lender of last resort duties and buy the debt securities issued by their respective governments, expanding the money supply as a side effect. In the end, an inflationary spiral will emerge.

What these two stars of the FinTwit are saying above is exactly that. Although prices are rising, the central bankers have to downplay it so as to excuse their "accommodative" policies and keep on doing them. In addition, the central bankers resort to manipulative techniques, the so-called Fed speak, to prevent the public from thinking that the rising cost of living is not their fault. Instead, they defend themselves affirming the pandemic is the culprit. Just look at what happened this week, Janet Yellen apparently told the truth about the need for rates increases in order to fight the "overheating" economy. As a result, stocks plunged on these remarks. Once she realised the errors in her ways, she backedtracked the next day and stocks rallied, proving that stocks, the whole financial system and, thus, the economy are proped up by central banks' and governments' largesse, In case they remove the punch bowl, the entire house of cards collapses. Naturally, though it pains me to admit, I agree with the central bankers on this particular issue (just to be perfectly clear). In spite of being true that the annual price variations in both the baskets of consumer and producer goods (the CPI and PPI, respectively) have risen, especially in the latter cohort, closing in on the central banks' target levels, the figures for the last couple of months (February and March) were and the next couple of ones will still be greatly dictated by base effects. Be that as it may, consumers have been suffering the brunt of the soaring costs in the grocery stores, the petrol stations, the car dealers and so on. Because of supply shortages, there has been some companies in the consumer staples sector, such as Colgate-Palmolive, Nestlé and Procter & Gamble that confessed the need to raise their products' prices. However, insofar as credit origination remains in the doldrums, the inflationary inferno will not be kindled. To make long story short, revisiting the March 23 post, I raised the question that "since the supply squeeze is squeezing producers' margins of profit, how is this conducive for them to hire?" I concluded that "due to shrinking margins, they will pass part of the cost on to retailers and these, in turn, will pass it to consumers afterwards. However, in view of the unreliable income source for most consumers, these are not going to totally spend their stimmy checks. Thus, retailers and producers and the rest of the supply chain participants are going to be the ones to absorb the costs entirely. Unsurprisingly, a lot of them are not going to manage this squeeze and will certainly be wiped out." Furthermore, I claimed that the government stipends are interfering with the normal functioning of the labour market, discouraging former workers, distinctly low-skilled, from rejoining the labour force and getting a job. As a result, the recovery processes of the bust phase are precluded on account of "the swift adjustment of the price and profit system" being restrained. As the following charts demonstrate, the bond market is ostensibly agreeing with my assessment. Despite shooting up steeply for a couple of months or so, the reflation in bonds, chiefly outside of the US, has been suggesting curiously since the FedWire disruptions in late February that the perceptions about future conditions have stopped improving. In fact, their fall since then indicates that those perceptions have deteriorated.

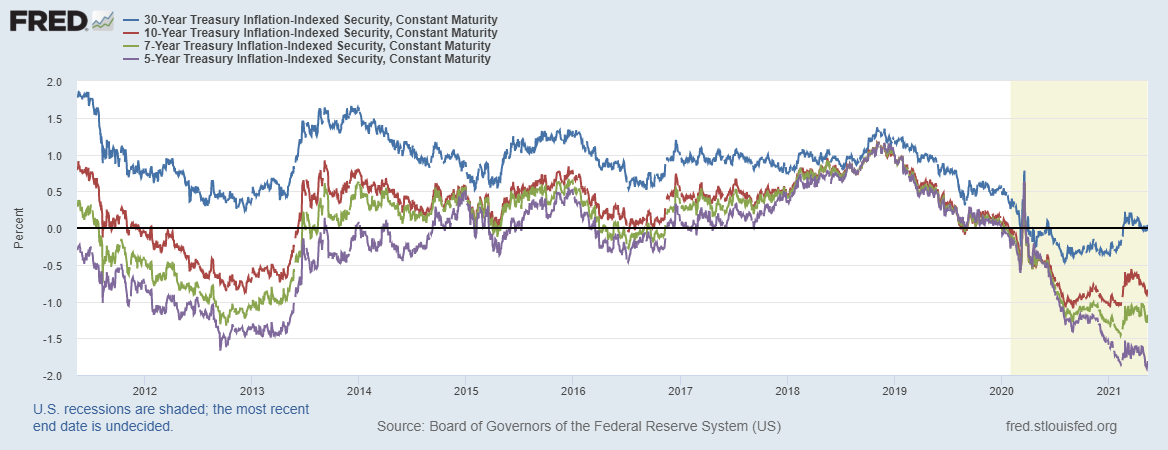

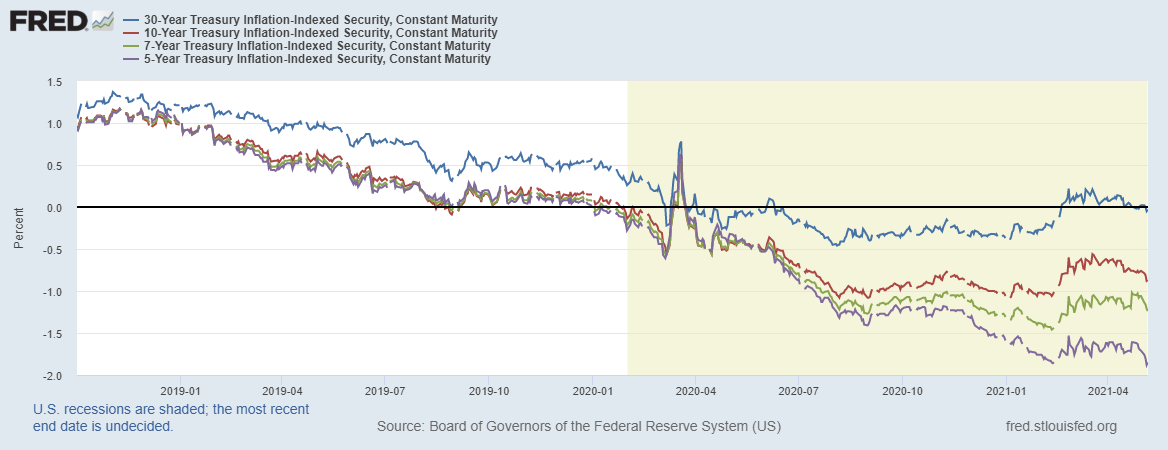

Undeniably, present and near-term conditions, as implied by the T-bills and the 2-year note too, continue to be dreadful. Only in the middle of this decade will conditions start to ameliorate and by the end of it will we get to the pre-pandemic circumstances. None of this is good, merely better than the absolute worst experienced last year. By the same token, the TIPS market - Treasury Inflation-Protected Securities - tells a very similar story, though an even more lugubrious one. On the left graph, the inverted breakeven rates portray the temporary (higher) inflation provoked by the supply squeeze. Notice how market participants are anticipating "normal" levels of inflation, around the magnitudes of the reflation #3, in the long-term, as expressed by the 5-year forward inflation rate. Notwithstanding, the graph on the right of the UST real yields is what paints a tremendously dismal picture. The demand for the safest financial instruments is so elevated that they do not mind seeing their returns being completely destroyed by the loss in the US dollar's purchasing power, not even for the next thirty years.

Astonishingly, the (global) bond market appears to be absolutely unaware of the economic and inflation prospects that the most prominent economists and analysts are projecting. Alternatively, they are aware but, due to being so obstinate, refuse to accept the truth postulated by those astute and gifted experts. If not these reasons, then what? Are bonds deaf? Those are the only logical explanations, right? Surely, the reason has to be at least one of these if they refuse to comply with the echo chamber. While we are on the subject, can someone also reprimand gold for not following the directives. Clearly, rising gold prices are a sign of growing uncertainty in the stability and health of the financial system and the economy in general. Despite popular belief, the current gold price and its trajectory are signaling the persistent deflationary/disinflationary environment is not fading, even though those in the inflation camp take this as an indication of escalating inflation expectations. That is not to say that in a truly inflationary inferno gold price does not shoot up or even drops. Simply put, gold prices climb whenever there are imbalances in the monetary system, either inclined to the inflation or the deflation sides. Therefore, on account of deflation pervading the economy (ever since the GFC1) gold is currently running counter to the inflation and the recovery narratives.  In conclusion, even if bonds are deaf that is totally irrelevant. Just like the genius Beethoven did not need to hear in order to compose the greatest musical masterpieces, the bond market can afford to ignore the cacophony coming out of orthodox-and-textbook-ridden financial media, concentrating solely on the conditions of the shadow eurodollar regime, and produce the most ingenious judgements of what is on the horizon and beyond.

Resuming this two-part series, after describing the primary features of the ABCT, I am now going to dwell on the secondary ones, as well as the role of government, finishing off with the proper course of action. Accordingly, some secondary features may develop. One of them is the deflationary credit contraction, although it is not a certain condition throughout a bust. The contraction phase begins with the end of the inflation, as you saw in the first installment, and can carry on without any further changes from the monetary camp. Nevertheless, deflation has almost always set in. Undeniably, after bankruptcies and financial woes amongst borrowers pervade the economy due to the excessive credit creation, the money supply starts to contract. However, there is no need for deflation to arise. Understandably, it is often posited that seeing that entrepreneurs can find few viable projects in a depression, business demand for loans plummets and, consequently, loans and money supply will shrink. Regardless, this argument overlooks the fact that banks, if they are willing, can purchase securities, thereby sustaining the money supply by increasing their investments to compensate for dwindling loans. Needless to say, this condition brings about some important implications that I am going to elucidate afterwards. Having said this, contractionist pressures always stem from banks and not from business borrowers. Be that as it may, the terrible economic landscape that is accompanied by widespread business failures could lead to questioning the banks' health and solvency state. Therefore, the money supply will decrease because of bank runs or "shadow bank" runs - like I showed previously. Even just the fear of such runs, owing to banks being inherently bankrupt in a fractional reserve system (or in sort of one), is enough for banks to tighten their positions. Furthermore, another common secondary trait of the bust is the surge in the demand for money. This "scramble for liquidity" as is frequently referred to, is provoked by three factors: i) people expect falling prices on account of the flagging economy and the emerging deflation, causing them to save more money and spend less, awaiting the drop in prices; ii) borrowers will try to pay off their debts, which are being promptly called by banks and other creditors, by liquidating other assets in exchange for cash; iii) the torrent of business losses and insolvencies makes businessmen wary of investing until the financial distress and the liquidation process cease. With the supply of money waning, and the demand for it rising, general falling prices are a consequent attribute of most busts, chiefly in its most gruelling stage. Notwithstanding, declining prices overall is precipitated by the secondary, rather than by the inherent, features of busts. In spite of regarding that the readjustments induced during the contraction phase should be permitted to unwind, almost all economists (not just the Keynesians) take the rather unfavourable view that the deflation and the general price fall that derives from it unnecessarily aggravate the severity of recessions. Despite that, this notion is incorrect for they have beneficial effects and definitely do not exacerbate the economic contraction. Firstly, on account of the general subside in prices, the demand for money can more easily be fulfilled because lower prices mean that the same total of cash balances have greater command over goods and services. As a result, the desire for increased real cash balances has now been satisfied. In the end, the demand for money will decline as soon as the liquidation and adjustment processes are finished. Once the liquidation is completed, the uncertainties surrounding the lousy financial panorama vanish and the scramble for liquidity terminates as well. So, a quick unhampered drop in prices, both in general (adjusting to the credit reduction) and especially in goods of higher orders (adjusting to the malinvestments of the boom), will speed up the recovery processes and remove expectations of further downturn. In defiance of prices waning as a whole, the important characteristic to note of the primary adjustments is that the prices of producers' goods plunge more rapidly than do consumer goods' prices. Secondly, the deflationary credit contraction is tremendously helpful to the recovery processes in the accounting of companies. Considering that firms record the value of assets at their original cost, when prices increase altogether, what seems to be a large profit may only be just sufficient to replace the now higher-priced assets. During an inflation, business profits are greatly overstated, with consumption of capital being greater than it would be if the accounting illusion were not operating - perhaps capital is even consumed without the entrepreneur realising it. On the flip side, in a period of deflation, the accounting illusion is reversed since what seem like losses and capital consumption, may actually mean profits for the firm due to assets now costing much less to be replaced. By merely thinking that he is replacing capital, the businessman is in reality incrementing the investment in his company. Thus, this overstatement of losses encourages saving, while restricting consumption. Finally, credit contraction will have yet another beneficial effect in promoting the recovery. Since credit expansion distorts the free-market by lowering price differentials between stages of production (lower differences between selling prices and costs), the curtailment of credit, au contraire, mangles the free-market in the opposing direction by diminishing the amount of funds in the businesses' hands, distinctly in the higher stages of production. Specifically, in view of the demand for factors in the higher stages dwindling, factor prices and incomes follow suit, increasing price differentials. Ergo, it encourages the shift of factors from the higher to the lower orders. Despite being abhorred by most economists, credit contraction returns the economy to (true) free-market proportions much sooner than otherwise. The more the government intervenes to delay the market's adjustment, the longer and more gruelling the depression will be, and the more difficult will be the road to complete recovery. Government hampering aggravates and perpetuates the depression." What is then the correct course of action that governments ought to pursue? If governments wish to see the economy actually recovering, breaking the shackles of the deflationary constraints and return to the suitable productive structure that respects society's time preferences, as quickly as possible, the first and clearest prescription, albeit very broad and basic, is not to interfere with the market's correction processes. Basically, the more the government intervenes, aiming at curing the economic malaises of the bust, those much-needed corrections are simply deferred. As a result, the deflationary/disinflationary environment will linger for longer, hindering "the road to complete recovery". As a matter of fact, were we to list the several ways that governments can hamper market adjustments, we would find that we had precisely catalogued the favourite measures of curbing recessions that make up the governments' fiscal and monetary arsenals. To wit, here are the ways the adjustments can be hobbled: 1. Preventing or retarding liquidation by keeping the credit spigots open, such as putting up a credit facility or guaranteeing loans backed by government; 2. By inflating further, the necessary fall in prices, mainly in the higher order goods, is blocked, thus delaying the corrections and prolonging the recession. The expansionary fiscal policies carried out by profligate governments that resort to debt and the accommodative monetary policies of central banks, in case they are actual "money printers", preclude the required structural reshaping to beget the recovery; 3. Keeping wage rates up insures permanent mass unemployment. In addition, when prices are declining because of deflation, trying to peg the rate of nominal wages results in pushing real wage rates higher. In the face of plummeting business activity and, accordingly, demand for labour, this aggravates immensely the unemployment problem; 4. Keeping prices up, above their true free-market levels, will create unsalable surpluses and prevent a return to adequate and sustained growth; 5. Stimulating consumption and discouraging saving worsen the shortage of saved funds even further, which is of course not conducive to a speedy recovery, being in fact a colossal drag. So as to encourage consumption, governments can provide all kinds of "helicopter money" payments, from food stamps to "stimmy" checks. Conversely, it can discourage saving and investment by increasing taxes, particularly on the wealthy, on corporations and estates. In case you do not know, any increment in government spending will discourage saving and investment, while spurring consumption, since government spending boils down to consumption. Although some of the private funds would have been saved and invested, all of the government funds are consumed (or rather wasted). Therefore, any amplification in the relative size of government in the economy, among other consequences, shifts the societal consumption/saving ratio in favour of consumption, extending the recession; 6. Subsidising unemployment via "insurance" payments or any other welfare programme will protract joblessness indefinitely, deferring the reshuffle of workers to the sectors where jobs are available. It is indeed probable that more harm and misery have been caused by men determined to use coercion to stamp out a moral evil than by men intent on doing evil." To conclude, credit expansion sets into motion the business cycle in all its phases. Beginning with the inflationary boom, marked by the swelling of the money supply and by malinvestment, then the crisis comes into light when the credit origination ceases, exposing the malinvestments, and reaches its finale when the corrections of the production structure are carried out. Ultimately, the economy gets back to the most efficient ways of satisfying consumers' wants and needs. Nevertheless, there is one huge caveat. Seeing that in the real world governments always feel the urge to save the day and rescue its constituency from the distress that crises generate, mainly for the public wanting a paternalistic State, the recovery phase is always restrained. Hardly ever does economic activity recover swiftly from its trough, at the full potential growth of a true free-market regime. Hence, government interventionism with the mission of combating the downturn and restoring the upward trajectory of the economy as fast as possible, will emphatically have the opposite effect. Bearing in mind that the banks, while reducing loans to businesses during the crisis phase, they stock up on securities, because of liquidity preferences. As you know, in times of outright financial panic or just meagre growth, the most liquid, meaning the safest, assets are the most sought after. These assets happen to be the debt securities issued by the governments of the most predominant and developed economies, such as the US, Germany, Japan and so on. For that reason, the prices of these government bonds (and notes and bills) skyrocket due to being in high demand, causing their interest rates (yields) to plunge. Despite becoming more prevalent since the inception of the eurodollar system, with its Markowitz foundations, these processes have abided by these methods, vis-à-vis liquidity preferences, since long before then (as the next graphs demonstrate). Consequently, noticing the low cost of servicing their debts, governments feel compelled to act. Obviously, they cannot refuse this invitation of profligacy. How could they? It is simply too tempting. Thus, the adjustments required to bring about a rapid recovery will be inhibited.

Moreover, even though banks are able to trigger another boom by resuming their inflationary proclivities, if they perceive that economic conditions and their prospects are grim, they are not going to return to the prior "easy money" ways, owing to the outlook not being fitting to do so. Taking into account that banks are always looking for opportunities to lend to businesses in order to improve their profits, the fact that they refrain from doing so - the more governments butt in, the more they shy away from lending -, it really tells you a lot about the harm that government interference engenders.

Ergo, the best thing that governments can do is to essentially get out of the way and enact policies that adhere to the principles of laissez-faire capitalism. Fundamentally, let entrepreneurs find the best manners to satisfy the desires of the people, by getting rid of all kinds of arbitrary rules and regulations that erect barriers and hindrances which prevent the smooth functioning of the free-market system. To cap it all off, applying this philosophy to the banking industry and the monetary system, in general, is of the utmost importance to prevent the endless recurrence of the boom and bust cycle. On that account, only then can we grow and develop at the maximum rate imaginable, lifting along the way the standards of living at a pace never before witnessed. Above all, it would be done in a sustainable fashion, in view of conforming to the societal time preferences and the actual amount of savings. Otherwise, the governmental meddling acts as a tremendous drag on economic growth and all the things associated with it. Evidently, technological progress, social advance and rising living standards become gradually constrained. Therefore, the do-gooding politicians and technocrats that claim to know what is best for us, the commoners can very well, though unwittingly, turn a run-of-the-mill bust, a mere recession if you will, into a prolonged and dreadful depression. In this day and age, the most widely held belief on the cause of the business cycle is that it is endogenous to the capitalism system. In plain English, this means that the free-market is intrinsically unstable and fallible, though creating growth and progress, it also begets its own demise. In the turn of the 20th century, Ludwig von Mises presented his theory to the world explaining the puzzling and all-encompassing fluctuations in the economic landscape. Picking up where the Currency School of British classical economists left off in the early 19th century, his view holds that business cycles stem from disturbances generated in the market by monetary intervention. This monetary theory contends that money and credit - will be interchangeably mentioned - expansion, launched by the banking system (including all sorts of credit originators), triggers booms and busts. Because a cycle takes place in the economic realm, a valid cycle theory must be integrated with general economic theory, or as it is more commonly known, macroeconomics. Despite the followers of Keynes being the presumed superior economists owing to dominating economic thought worldwide, across academia, media and government agencies, the theory engendered by Mises is one of the only two (the other being Schumpeter's) that has been integrated into general economics. In fact, various neo-Keynesians have advanced cycle theories. However, they are integrated not with general economic theory, but with holistic Keynesian systems, which are very partial. There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved." To begin with, I ought to describe the theory credited to Mises, the Austrian business cycle theory (ABCT). This theory came about because Mises detected that a cluster of business errors would suddenly emerge, causing an economic contraction. Clearly, such widespread failures cannot be provoked by business fluctuations due to changes in consumers' preferences or by entrepreneurs out of the blue becoming terrible at their jobs, which is to anticipate future economic conditions. Regarding business fluctuations, these are not the same thing as business cycles. On account of shifts in consumer tastes, in time preferences, in the labour force's quantity, quality and location, in natural resources' availability and in technologies, business activity is constantly mutating. Thus, we may expect specific business fluctuations all the time. Be that as it may, a special "cycle theory" is not necessary to account for them, being instead products of changes in economic data and are fully explained by economic thinking. Despite many economists attributing general business slump to weaknesses effected by a reduction in one or a few sectors of the economy, declines in specific industries can never ignite a general contraction, either a recession or a depression - the latter being an acute and/or a long period of substandard growth, stagnation or even continuous plunge of output. In view of shifts in data that will result in surges in activity in one field and declines in another, there is nothing here that points to general economic contraction, which is a phenomenon of the actual "business cycle". In relation to the pervasive mistakes made by the entrepreneurial class, this can only occur due to some external factor from the free-market. Since we live in a society of constant and unending change, this can never be precisely charted in advance. Although people try to forecast and anticipate changes as best as they can, such forecasting can never be reduced to an exact science. Nevertheless, entrepreneurs are in the business of foreseeing variations on the market, both for conditions of demand and of supply. While the more successful ones make profits, insofar as their judgements are accurate, the unsuccessful forecasters fall by the wayside. Hence, the successful entrepreneurs will be the ones most adapt at anticipating future business conditions. Needless to say, the forecasting is always imperfect, leading entrepreneurs to continuously differ in the success of their assessments and choices. Indeed, if this were not so, no profit or losses would ever be made in business - that is, they would operate in a market of perfect competition, which never transpires in the real world. Therefore, the market provides a training ground for the reward and expansion of successful and shrewd entrepreneurs, while weeding out the failed and unperceptive ones. In order to uncover the origin of the bust part of the business cycle, one must explain why there is a sudden cluster of business errors. This is the first and foremost peculiarity any cycle theory must account for. In spite of business activity moving along nicely with most businesses turning a profit, without notice, conditions change and the bulk of companies begin experiencing losses, revealing to have made grievous mistakes in their projections. On that account, a general review of entrepreneurship is now in order. As a rule, only some businessmen suffer losses at any other time; with the large majority either breaking even or making a profit. How, then, to justify the curious phenomenon of the crisis when almost all entrepreneurs accrue losses or simply earn less than they were expecting? How did these astute businessmen come to make such miscalculations together? And why were they all promptly unveiled at this particular time? Seeing that it is the duty of entrepreneurs to forecast future conditions, some of which being abrupt, it is then not legitimate to reply that instant changes in the data are responsible. Accordingly, you have to wonder why their analyses failed so abysmally. Another common feature of the business cycle calls for an explanation as well. Interestingly, throughout the cycle, capital goods industries oscillate more widely than do the consumer goods industries. Comparing to the latter group, the former one, chiefly the industries supplying raw materials, construction and equipment to other industries, scale up much further in the boom, being ultimately hit far more drastically in the bust. Lastly, a third feature of every boom that needs explaining is the expansion in the quantity of money in the economy. On the flip side, there is generally, though not universally, a decrease in the money supply during the bust. Bearing in mind those considerations, what immediately springs up as the explanatory element for the general movements in business is the general medium of exchange, money, for it is the mechanism of exchange (a.k.a., money) that links all economic activities. If one price of a particular good goes up and another one goes down, one may conclude that demand shifted from one industry to the other (with supply remaining the same). Having said this, if all prices, by and large, move up or down together, then something must have happened in the monetary sphere. In a nutshell, general price fluctuations are driven by changes in the supply of and demand for money. On the one hand, an increase in the money supply, with demand for it remaining constant, will cause a fall in the purchasing power of each monetary unit, occasioning a general rise in prices; vice versa, a drop in the money supply, ceteris paribus, will precipitate a general decline in prices. On the other hand, an increase in the general demand for money, the supply staying the same, will cause lead to the purchasing power of the currency to climb and, consequently, prices to wane overall; while a fall in demand will cause a general surge in prices. Ergo, when people are willing to hold in their cash balances (demand for money) the exact amount of money in existence, the purchasing power of money will remain constant. If the demand for money exceeds the stock, the purchasing power of money will soar until the demand is no longer excessive, clearing the market. Conversely, a demand lower than supply will subdue the currency's purchasing power, raising prices on average. Even though it has to be the case that any cycle in the economy as a whole must be transmitted through the mechanism of exchange, this relation between money and prices alone does not give the grounds for the business cycle. In short, why should this generate a business cycle? More importantly, why should it bring about a depression?  According to the ABCT, it is due to the total disregard shown the banking institutions (including all types of credit originators) towards the people's time preferences. As we learned on the last couple of posts (parts I and II), time preferences give us the pure interest rate and its mirrored consumption-to-saving/investment ratio. Succinctly, a lower time-preference rate will be reflected in greater proportions of investment to consumption, a lengthening of the structure of production and a building-up of capital, and vice versa. Moreover, the market rates of interest consist of the pure interest rate plus entrepreneurial and inflation risks. What is crucial to understand is that the resulting rates manifest themselves as the interest rates on the loan market. In practice, the interest rates are derived from the price differentials between businesses' selling prices and costs of production, that is the profit rate. Unsurprisingly, as banks expand credit to companies, giving the impression the supply of saved funds for investment has increased, the money enters the loan market, perhaps lowering or not the loan rates of interest - whether or not that happens is totally irrelevant. However, price differentials are, as a result, reduced. This occurs on account of businessmen being misled by the bank inflation into believing that the savings are greater than they actually are. Hence, when saved funds, are perceived to have increased, entrepreneurs invest in "longer" processes of production. In other words, the capital structure is lengthened, especially in the "higher" orders, most remote from the consumer. Essentially, entrepreneurs, using their newly acquired funds, bid up the prices of capital and other producer's goods, stimulating a shift of investment from the "lower" (near the consumer) to the "higher" (furthest form the consumer) orders of production. All in all, an "artificial" shift of investment from consumer goods to capital goods industries ensues. Soon, the new money percolates downward from the business borrowers to the factors of production: in wages, rents and interest. Unless time preferences moved lower, people will spend their higher incomes in the old consumption/investment proportions. In sum, capital goods industries, to a greater extent than the consumer goods sector, will find that their investments have been in error. What they thought profitable really fails for lack of demand by their entrepreneurial customers in the lower orders. Therefore, the higher orders of production have turned out to be highly wasteful (not all of it, of course) and the malinvestment must be liquidated. Owing to the credit expansion, beyond the true level of savings, ubiquitous bad decisions are committed. Naturally, the crisis arrives when the consumers come to reassert their desired proportions. The bust is for that reason the process by which the economy adjusts to the wastes and errors of the boom, re-establishing (or at least trying to) the efficient service of consumers' wants and needs. . . . additional investment is only possible to the extent that there is an additional supply of capital goods available. . .. The boom itself does not result in a restriction but rather in an increase in consumption, it does not procure more capital goods for new investment. The essence of the credit-expansion boom is not overinvestment, but investment in wrong lines, i.e., malinvestment on a scale for which the capital goods available do not suffice. Their projects are unrealisable on account of the insufficient supply of capital goods. . .. The unavoidable end of the credit expansion makes the faults committed visible. There are plants which cannot be utilised because the plants needed for the production of the complementary factors of production are lacking; plants the products of which cannot be sold because the consumers are more intent upon purchasing other goods which, however, are not produced in sufficient quantities. . .. The observer notices only the malinvestments which are visible and fails to recognise that these establishments are malinvestments only because of the fact that other plants - those required for the production of the complementary factors of production and those required for the production of consumers' goods more urgently demanded by the public - are lacking. . .. The whole entrepreneurial class is, as it were, in the position of a master-builder [who] . . . overestimates the quantity of the available supply [of] materials . . . oversizes the groundwork . . . and only discovers later . . . that he lacks the material needed for the completion of the structure. It is obvious that our master-builder's fault was not over-investment, but an inappropriate [investment]." In view that the inflationary boom precludes the efficient allocation of resources that a real free-market would generate by satisfying voluntarily expressed consumer desires, including the public's relative preferences for present and future consumption, the productive structure gets distorted, no longer serving consumers properly. Thus, the crisis signals the end of this inflationary distortion, and the contraction is the process by which the economy returns to the efficient service of consumers. Undeniably, far from being an evil scourge, the ensuing economic contraction is the necessary and beneficial return of the economy to normal. As a result, the boom plants the seeds for its future bust. Whether it becomes a garden-variety recession or a profound depression depends solely on the degree of government meddling, as I am going to demonstrate later on. Furthermore, the boom can last for a longer period than one would reasonably expect because banks tend to delay the day of reckoning. Seeing factors bid away from them by consumer goods industries, finding their costs surging and themselves short of funds to boot, the capital goods firms turn again to the banks. If the banks keep the credit spigots open, the borrowers are kept afloat. Once more, the new money pours into businesses and they can again bid factors away from the consumer goods industries. On the whole, as credit is relentlessly expanded, the wasteful enterprises can be shielded from consumer retribution. Clearly, the greater the credit swelling and the longer it goes on, the longer will the boom last. Without surprise, the boom will end when the inflationary credit expansion ceases at last. The longer the boom proceeds or the more intense it is in originating credit, the more imprudent errors are perpetrated, requiring more rigorous corrections and readjustments of the productive structure. On that account, some key features of the bust-recovery phase are going to emerge inevitably. For one, wasteful projects must either be abandoned or scaled down, with inefficient companies liquidated, completely or just partially, or turned over to their creditors. In addition, prices of producers' goods must dwindle, particularly in the higher orders of production, including capital goods, lands and wage rates. Just as the boom was marked by an illusory fall in the pure interest rates, although not necessarily in the market rates of interest, entailing that the price differentials between stages of production were too subdued, the bust consists of a rise in this interest-differential. This means that the prices of the capital and producers' goods must drop relative to prices in the consumer goods industries. Besides the indispensable price decreases of certain machines, whole aggregates of capital such as the stock market and real estate have to see their values contract. Finally, since factors of production must journey from the higher to the lower orders of production, some "transient" unemployment will materialise during the contraction phase, even though it does not have to be any greater than the unemployment corresponding to the shifts in production. In practice, the level of joblessness will be aggravated by the numerous bankruptcies and the vast malinvestments laid bare. Albeit it still needs to only be temporary. Simply put, the speedier the adjustment, the more fleeting will the unemployment be. Notwithstanding, if wage rates are kept artificially elevated, preventing them from falling, the unemployment will progress beyond the "transient" stage, assuredly becoming very alarming and harmful for the prospects of recovery.  Due to being extensive and having still much to unravel, I will continue this discussion another day. Meanwhile, I would invite to read the other articles in this blog, if you have not already read them.